Medical Device Design and Development Services Market Size, Share & Industry Analysis, By Service Type (Product Design & Engineering Services, Prototyping & Validation Services, Regulatory, Quality & Compliance Services, & Others), By Device Class (Class I, Class II, & Class III), By Device Type (Diagnostic Devices, Therapeutic Devices, Surgical Devices [Minimally Invasive Surgical Tools, Robotic Assisted Systems, & Others], Patient Monitoring Devices [Wearable Health Monitors, & Others], and Others), By Provider (Medical Devices Companies, CDMOs, & Others), and Regional Forecast, 2026-2034

Medical Device Design and Development Services Market Size and Future Outlook

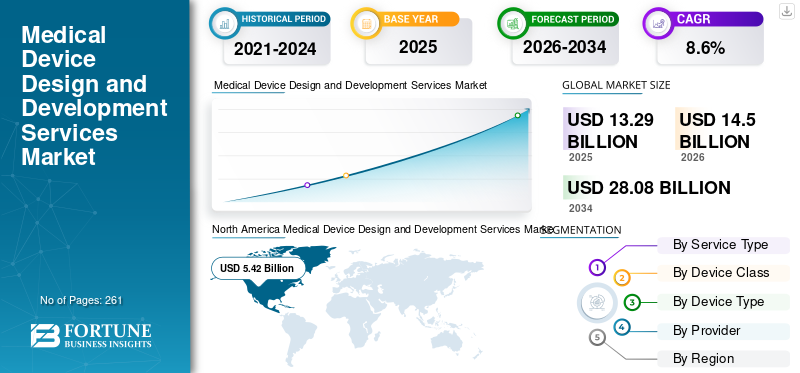

The global medical device design and development services market size was valued at USD 13.29 billion in 2025 and is projected to grow from USD 14.50 billion in 2026 to USD 28.08 billion by 2034, exhibiting a CAGR of 8.6% during the forecast period. North America dominated the medical device design and development services market with a market share of 40.78% in 2025.

Medical device design and development services refer to a systemic methodology that requires specialized services that support medical device companies across their device lifecycle, from concept ideation and industrial design to prototyping, engineering, verification, validation, and regulatory approvals. The growing burden of chronic conditions, aging population, expansion of healthcare infrastructure, and growing demand for technologically advanced therapeutic and diagnostic devices are further resulting in a rising adoption rate of these products in the market. This, along with the growing outsourcing of medical devices among the manufacturers, is also supporting the adoption rate of medical device design and development services in the market.

- For instance, according to the 2024 data published by the Centers for Disease Control and Prevention (CDC), about 1 in 20 adults aged 20 and older has coronary artery disease in the U.S.

Furthermore, the rising R&D activities among the major players, such as Paragon Medical, Capgemini, among others, are further contributing to the demand for these products in the market.

Download Free sample to learn more about this report.

Medical Device Design and Development Services Market Key Takeaways

- 2025 Market Size: USD 13.29 billion

- 2026 Market Size: USD 14.50 billion

- 2034 Forecast Market Size: USD 28.08 billion

- CAGR: 8.6% from 2026–2034

- North America dominated the medical device design and development services market with a 40.78% share in 2025.

- The diagnostic devices segment accounted for the largest market share of 32.3% in 2025.

- The medical device companies segment is projected to hold a 46.7% share in 2026.

North America

North America led the market in 2025 with a valuation of USD 5.42 billion, maintaining its dominant regional position.

Europe

Europe is projected to reach USD 3.75 billion by 2026, supported by a 7.4% growth rate and the second-largest regional share.

Asia Pacific

Asia Pacific is estimated to reach USD 3.55 billion by 2026, ranking as the third-largest regional market.

U.S.

U.S. The market is projected to reach approximately USD 5.11 billion by 2026.

Japan

Japan The market is estimated to reach approximately USD 0.78 billion by 2026.

Read More

Medical Device Design and Development Services Market Trends

Technological Advancements in these Products to be a Significant Market Trend

There is a rapid innovation in digital engineering solutions and product manufacturing toolchains, which is becoming a prominent trend, boosting the demand for medical device design and development services globally. The medical products companies are adopting advanced simulation and virtual prototyping, such as Computational Fluid Dynamics (CFD), Finite Element Analysis (FEA), and human factors modeling, to validate performance earlier, which reduces physical iterations and minimizes development timelines.

Furthermore, the increasing adoption of digital twins and model-based design is also resulting in the development of faster design optimization across complex systems such as drug-device combination products and others, which is increasing the number of medical device submissions, thereby fueling the adoption rate of these products in the market.

- According to 2023 data published by MedTech Dive, it was reported that the FDA received 19,100 submissions as compared to 18,800 in 2022.

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Rising Burden of Chronic Disorders to Fuel Market Growth

The increasing burden of chronic diseases is a major market driver fueling the demand for medical device design and development services, as manufacturers and healthcare facilities are emphasizing earlier diagnosis, long-term disease management, and patient-centric care delivery. The rising prevalence of these disorders, including neurovascular disease, diabetes, respiratory disorders, cardiovascular conditions, and others, is boosting the demand for a broad range of products such as monitoring systems, drug-delivery devices, and connected homecare technologies, among others.

- For instance, according to 2025 data published by the International Diabetes Federation (IDF), it was reported that about 590 million people have diabetes globally.

Additionally, the growing burden of chronic diseases is shifting the preference beyond acute hospital settings toward outpatient and home-based facilities, augmenting the demand for portable and minimally invasive devices, further strengthening the demand for specialized development capabilities, including miniaturization, which supports the outsourcing services for these medical devices. Therefore, the factors above are expected to contribute to the global market growth.

Market Restraints

High Cost Sensitivity and IP Concerns to Hamper Market Growth

Despite strong demand for advanced devices, the market faces notable limitations, including cost sensitivity and Intellectual Property (IP) concerns among medical device companies. The outsourcing of design and development services can reduce long-term costs; however, the upfront investment required for comprehensive end-to-end services remains significant, especially for small and mid-sized firms operating under constrained research and development budgets.

Additionally, concerns around IP protection and data security continue to influence outsourcing decisions, particularly for proprietary technologies. Medical device firms are focusing on developing breakthrough diagnostic platforms or AI-driven devices to reduce risks associated with knowledge leakage.

- For instance, according to the Cybersecurity Outlook 2022, the prevalence of indirect cyberattacks and successful breaches that target businesses through third-party entities has risen from 44% to 61% in recent years.

Market Opportunities

Growth of Startups and Innovation-Led MedTech Ecosystems are Creating New Opportunities

There is a rapid innovation of medical technology facilities and start-ups in developing nations, such as India, Mexico, and others. The early-stage medical technology companies often lack the regulatory experience, internal infrastructure, and cross-functional expertise required to develop novel products from ideation to commercialization.

The startups are increasingly partnering with specialized medical device design companies to de-risk development and minimize timelines owing to increasing venture capital funding in diagnostics, digital health, and minimally invasive technologies, thereby creating a lucrative opportunity in the market.

- According to 2025 data published by AdvaMed, there are about 6,500 small- and medium-sized enterprises in the U.S.

Market Challenges

Limited Contract Development and Manufacturing Organizations (CDMOs) in Emerging Countries to Hamper Market Growth

There is a growing demand for innovative medical devices among the patient population. However, lack of developed infrastructure, limited healthcare spending, coupled with a shortage of technologically advanced devices, particularly in emerging countries, are resulting in a limited number of establishments of contract research organizations.

Moreover, gaps in regulatory expertise, limited exposure to global standards, including ISO 13485, IEC 62304, IEC 60601, and FDA design control requirements, and inadequate clinical research infrastructure further constrain the ability of emerging market contract research organizations to support global commercialization strategies.

- For instance, according to 2024 statistics published by Access to Medicine Foundation, only 43% of all clinical trials analysed in the 2024 Index are conducted in any Low- and Middle-Income Countries (LMICs), despite being home to nearly 80% of the global population.

Other Prominent Challenges

- Stringent regulatory approvals are hampering the market growth.

- Longer validation cycles to limit the market growth.

SEGMENTATION ANALYSIS

By Service Type

Increasing R&D Investment Led to Product Design & Engineering Services Segment Dominance

Based on service type, the market is classified into product design & engineering services, prototyping & validation services, regulatory, quality & compliance services, and others.

To know how our report can help streamline your business, Speak to Analyst

The product design & engineering services segment held the largest revenue share in 2025. The growth is due to the increasing development of products, from concept generation and functional design through to engineering validation and production readiness. This, coupled with the growing R&D investment among the key players for product designing and engineering services, is further expected to contribute to the global medical device design and development services market growth.

- For instance, according to the 2025 annual report published by Medtronic, the research and development expenditure was USD 2.732.0 million.

The regulatory, quality & compliance services segment is expected to grow at a CAGR of 8.9% over the forecast period.

By Device Class

Wider Applications Range of Class II Led to Dominance of Segment

Based on device class, the market is segmented into class I, class II, and class III.

The class II segment dominated the global market and held the share of 46.5% in 2025. Class II devices, including surgical instruments, infusion pumps, diagnostic imaging systems, and others, are characterized by moderate to high risk and therefore require special controls. This, along with the majority of medical devices falling in this category, is resulting in a rising number of products outsourced for class II devices, and is also anticipated to support the segmental growth in the market.

- For instance, according to the 2025 data published by Amplelogic, it was reported that class II medical devices account for 53% of device applications and represent a broad spectrum of product types, including blood transfusion devices, powered wheelchairs, contact lenses, and others.

The segment of class III is set to flourish with a CAGR of 9.0% across the forecast period.

By Device Type

Growing Number of Diagnostic Devices Approvals Led to Dominance of Segment

Based on device type, the market is segmented into diagnostic devices, therapeutic devices, surgical devices, patient monitoring devices, and others. Diagnostic devices are further segregated into imaging systems, in-vitro diagnostic tools, and others. Therapeutic devices are divided into drug delivery devices, implantable devices, and others. Surgical devices are segmented into minimally invasive surgical tools, robotic assisted systems, and others. Patient monitoring devices are divided into wearable health monitors, connected medical devices, and others.

The diagnostic devices segment dominated the global market and accounted for 32.3% market share in 2025. The growth is due to the growing prevalence of chronic conditions, including cardiovascular conditions and neurological diseases, among others, resulting in an increasing number of diagnostic device submissions and approvals globally, thereby contributing to the segmental growth in the market.

- For instance, according to the 2025 statistics published by The Medical Futurist, the FDA has cleared about 1,250 AI-based medical devices, including the majority of diagnostic devices globally.

The segment of therapeutic devices is set to flourish with a growth rate of 9.3% across the forecast period.

By Provider

Increasing Number of Medical Device Companies Led to Segmental Dominance

Based on provider, the market is classified into medical device companies, Contract Development and Manufacturing Organizations (CDMOs), and others.

The medical device companies segment dominated the market in 2025. The growing prevalence of chronic conditions, the rising number of medical device companies, and increasing healthcare expenditure, among others, are some of the key factors supporting the growth of the segment in the market. Furthermore, the segment is set to hold a 46.7% share in 2026.

- For instance, according to 2025 statistics published by AdvaMed, there are about 6,500 medical technology companies in the U.S.

In addition, Contract Development and Manufacturing Organizations (CDMOs)’ segment is projected to grow at a 9.1% CAGR during the forecast period.

Medical Device Design and Development Services Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Device Design and Development Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 5.00 billion, and also took the leading share in 2025 with USD 5.42 billion. The increasing prevalence of chronic diseases, a strong medtech ecosystem, FDA-driven compliance outsourcing, and regulatory standards, among others, are some of the factors supporting the growth of the regional market.

- For instance, according to 2024 data published by the Centers for Disease Control & Prevention (CDC), it was reported that the prevalence of Inflammatory Bowel Disease (IBD) is estimated between 2.4 and 3.1 million among the patient population in the U.S.

U.S. Medical Device Design and Development Services Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 5.11 billion in 2026, accounting for roughly 35.2% of global sales.

Europe

Europe is projected to record a growth rate of 7.4% in the coming years, which is the second largest market share among all regions, and reach a valuation of USD 3.75 billion by 2026. The medical device regulations and contract engineering demand for medical devices are likely to support the market growth.

U.K Medical Device Design and Development Services Market

The U.K. market is estimated at around USD 0.70 billion in 2026, representing roughly 4.8% of global revenues.

Germany Medical Device Design and Development Services Market

Germany’s market is projected to reach approximately USD 0.86 billion in 2026, equivalent to around 5.9% of global sales.

Asia Pacific

The Asia Pacific market is estimated to reach USD 3.55 billion in 2026 and secure the position of the third-largest region in the market. The cost-effective research and development hubs and growing device manufacturing are likely to support the growth of the market.

Japan Medical Device Design and Development Services Market

The Japan market is estimated at around USD 0.78 billion in 2026, accounting for roughly 5.4% of global revenues. Japan has historically reported a relatively increasing prevalence of chronic conditions, with rising demand for designing and development services in the medical device industry.

China Medical Device Design and Development Services Market

China’s market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 1.08 billion, representing roughly 7.4% of global sales.

India Medical Device Design and Development Services Market

The Indian market size is estimated at around USD 0.59 billion in 2026, accounting for roughly 4.1% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.72 billion in 2026. The growth is due to the gradual growth tied to emerging healthcare investments in these regions. Middle East & Africa is also expected to grow due to rising outsourcing activities and improvement in regulatory scenario in the region.

South Africa Medical Device Design and Development Services Market

The South Africa market is projected to reach around USD 0.16 billion in 2026, representing roughly 1.1% of global revenues.

GCC Medical Device Design and Development Services Market

The GCC is set to reach a value of USD 0.27 billion in 2026.

Competitive Landscape

Key Industry Players

Expansion of Medical Device Design and Development Services to Support their Dominance

A significant services portfolio, coupled with a rising focus on strategic initiatives globally, is one of the prominent factors supporting the dominance of players in the global market. Paragon Medical and Capgemini are major companies in the market in 2025. Moreover, the rising focus of key players on the expansion of medical device designing services is likely to strengthen their presence, further supporting the global medical device design and development services market share.

- For instance, in July 2025, Capgemini highlighted the increasing convergence of digital technologies with physical product development in healthcare and life sciences, focusing on how digital engineering, data-driven design, and connected technologies are reshaping medical device innovation. This reinforces the company’s positioning in end-to-end medical device designing services.

Other key players, including Infosys and others, are also growing in the market, primarily due to their increasing focus on research and development activities to strengthen their presence in the market.

List of Key Medical Device Design and Development Services Companies Profiled in Report

- Paragon Medical (U.S.)

- Abbott (U.S.)

- Medtronic (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Capgemini (France)

- Infosys (India)

- StarFish Product Engineering Inc. (Canada)

- PRESTO Engineering (France)

- Simbex (U.S.)

- Siemens Healthineers AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Medtronic received FDA approval for the MiniMed 780G system for use with the Instinct sensor for insulin-requiring type 2 diabetes. This helped the company in strengthening its presence.

- November 2025: Johnson & Johnson Services, Inc., a player in cardiac arrhythmia treatment, presented clinical and real-world data for its integrated-by-design VARIPULSE Catheter in Pulsed Field Ablation (PFA) procedures for Atrial Fibrillation (AF).

- September 2025: Tata Elxsi, a player in design and technology services, announced the inauguration of the 'Bayer Development Centre in Radiology' at Tata Elxsi, India.

- August 2025: Wipro Limited, a AI-powered technology services company, acquired the Digital Transformation Solutions (DTS) business unit of HARMAN, a Samsung company, that will accelerate Wipro’s mission to deliver next-generation Engineering Research & Development (ER&D) services across technology, industrial, aerospace, healthcare, and consumer industries.

- July 2025: Elevaris Medical Devices, a Contract Development and Manufacturing Organization (CDMO) for industry-leading, multi-national healthcare companies, global medical device manufacturers, and emerging technology companies, is leaning into live prototyping to help manufacturers accelerate the research and development cycle, reduce costs, and increase speed to market.

- July 2024: Presto Engineering, a European company in Application-Specific Integrated Circuit (ASIC) design, engineering and production services, announced that it has passed EN ISO 13485 certification, the internationally recognized quality benchmark for medical device manufacturers.

- September 2020: Infosys acquired Kaleidoscope Innovation, a product design, development, and insights company focused on the medical device market, for USD 42.0 million. This helped the company to strengthen its brand presence.

REPORT COVERAGE

The report provides a detailed global medical device design and development services market analysis and focuses on key aspects such as leading companies and market segmentation, including service type, device class, device type, and provider. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service Type, Device Class, Device Type, Provider, and Region |

| By Service Type |

|

| By Device Class |

|

| By Device Type |

|

| By Provider |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 13.29 billion in 2025 and is projected to reach USD 28.08 billion by 2034.

In 2025, the North America regional market value stood at USD 5.42 billion.

Growing at a CAGR of 8.6%, the market will exhibit steady growth over the forecast period (2026-2034).

By service type, the product design & engineering services segment is the leading segment in this market.

The provision of novel medical device design and development services is one of the major factors driving the markets growth.

Paragon Medical and Capgemini are the major players in the global market.

North America held the highest market share in 2025.

The growing prevalence of chronic conditions, the increasing demand of medical device design and development services, among others, are some of the prominent factors anticipated to boost the adoption of these products globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us