Medical Equipment Maintenance Market Size, Share & Industry Analysis, By Service Type (Preventive Maintenance, Corrective/Breakdown Maintenance, and Operational/Performance Maintenance), By Device Type (Imaging Equipment, Life Support Equipment, Patient Monitoring Equipment, Surgical & Endoscopy Devices, Laboratory & Diagnostic Equipment, Dental Equipment, and Others), By Service Provider (Original Equipment Manufacturers, Independent Service Organizations, & Others), By End User (Hospital & ASCs, Clinics, Diagnostic Imaging Centers & Others), and Regional Forecast, 2026-2034

Medical Equipment Maintenance Market Size and Future Outlook

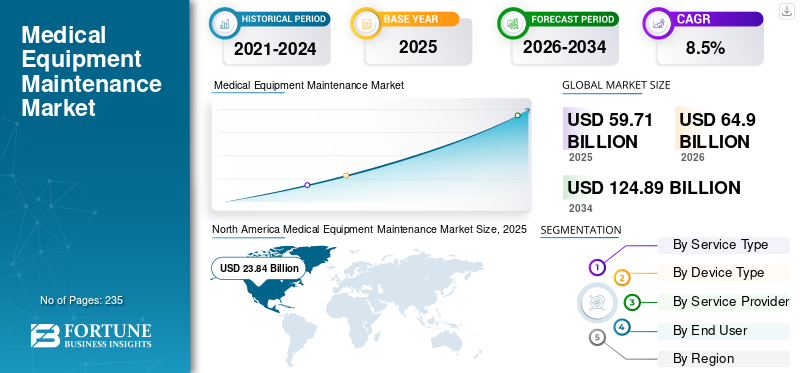

The global medical equipment maintenance market size was valued at USD 59.71 billion in 2025 and is projected to grow from USD 64.90 billion in 2026 to USD 124.89 billion by 2034, exhibiting a CAGR of 8.5% during the forecast period. North America dominated the global medical equipment maintenance market with a market share of 39.93% in 2025.

Medical equipment maintenance is a systematic process that ensures medical equipment functions properly, safely, and reliably through activities such as inspections, cleaning, calibration, and repairs. The goal is to extend the equipment's lifespan, guarantee patient and operator safety, and ensure accurate diagnostic results, thereby reducing costs and improving operational efficiency.

The growing number of patients, coupled with the development and expansion of healthcare infrastructure, as well as technological advancements that enhance safety, reliability, and stability, are further boosting demand for these products, thereby contributing to their adoption rate in the market. The increasing strategic partnerships among prominent players, such as GE HealthCare, Siemens Healthineers AG, Koninklijke Philips N.V., CANON MEDICAL SYSTEMS CORPORATION, and others, are anticipated to contribute to the global market growth.

- For instance, in September 2022, Siemens Healthineers AG and Drägerwerk AG & Co. KGaA entered into a ten-year technology & service partnership with ANregiomed Klinikum GmbH (Allied group of hospitals and clinics). Siemens and Dräger will supply, service, and maintain all technical medical devices over the contract term.

Download Free sample to learn more about this report.

MEDICAL EQUIPMENT MAINTENANCE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 59.71 billion

- 2026 Market Size: USD 64.90 billion

- 2034 Forecast Market Size: USD 124.89 billion

- CAGR: 8.5% from 2026–2034

- North America dominated the market with a 39.93% share in 2025.

- The Preventive Maintenance segment held the largest market share in 2025.

- Original Equipment Manufacturers (OEMs) accounted for 53.4% of the market in 2025.

North America

North America led the market with USD 23.84 billion in 2025 and is projected to reach USD 25.46 billion in 2026.

Europe

Europe is expected to reach USD 16.08 billion by 2026, supported by healthcare infrastructure expansion.

Asia Pacific

Asia Pacific is projected to reach USD 15.52 billion by 2026, driven by growing healthcare investments.

U.S.

The market is projected to reach USD 22.41 billion by 2026, supported by rising chronic disease cases.

Japan

The country is expected to witness steady market growth due to the increasing adoption of advanced medical equipment maintenance services.

Read More

Market Dynamics:

Market Drivers

Rising Demand for Advanced Medical Devices Across Healthcare Facilities to Drive Market Growth

The global market is experiencing robust growth, driven by several compelling factors that underscore the critical role of maintenance services in modern healthcare delivery. The surging prevalence of chronic diseases worldwide has emerged as a primary catalyst, with approximately 43% of the U.S. population suffering from one or more chronic conditions as of 2022, collectively representing 133 million Americans. This expanding patient base necessitates greater utilization of sophisticated diagnostic and therapeutic equipment, directly amplifying maintenance demands across healthcare facilities.

The rapid proliferation of advanced medical technologies is driving the medical equipment maintenance market growth, as hospitals increasingly invest in cutting-edge imaging systems, surgical instruments, and patient monitoring devices to enhance diagnostic accuracy and treatment outcomes. These sophisticated devices require specialized, regular maintenance to ensure optimal functionality and patient safety. Concurrently, stringent regulatory compliance requirements mandate rigorous equipment maintenance protocols to meet safety standards set by authorities such as the FDA, compelling healthcare providers to prioritize comprehensive maintenance programs.

Additionally, healthcare infrastructure investments, particularly in emerging economies such as China and India, are leading to the establishment of new hospitals and diagnostic centers, which significantly increase equipment maintenance requirements. The medical equipment market itself reached approximately USD 570 billion in 2025, with this expanding asset base directly translating into greater demand for maintenance services, positioning the maintenance market for sustained long-term growth.

Market Restraints

High Cost Associated with Maintenance and Shortage of Qualified Technicians to Hamper Market Growth

The market faces considerable constraints that moderate its growth trajectory, with financial pressures representing the most significant impediment. High initial costs associated with acquiring advanced maintenance technologies, coupled with substantial ongoing expenditure for specialized spare parts and skilled technicians, create formidable budget challenges for healthcare facilities. These financial constraints are particularly acute in price-sensitive regions and among small to medium-sized healthcare providers operating under tight budget allocations.

The critical shortage of qualified biomedical equipment technicians (BMETs) has emerged as a structural restraint significantly impacting market dynamics. According to industry surveys, approximately 40% of currently employed BMETs are age 55 or older, with 22% over 60 and approaching retirement. Compounding this demographic challenge, more than 30 schools with biomedical-related programs have closed in recent years, leaving just 22 colleges nationwide graduating around 400 BMETs annually. The U.S. Bureau of Labor Statistics projects over 7,300 annual job openings for BMETs, creating a substantial talent gap that extends maintenance turnaround times and increases labor costs.

The complexity of modern medical equipment presents additional restraints, as technicians require extensive specialized training to service increasingly sophisticated devices that incorporate artificial intelligence, robotics, and advanced imaging technologies. This technological complexity extends the learning curve and necessitates continuous education programs, which healthcare facilities find to be costly and resource-intensive. Furthermore, delays caused by original equipment manufacturers (OEMs) in providing maintenance services and the unavailability of original spare parts often result in extended equipment downtime, which frustrates healthcare providers and negatively impacts patient care delivery. The rise of duplicate or counterfeit spare parts, which affect equipment lifespan and reliability, adds another dimension to these operational challenges.

Market Opportunities

Several Services Expansion of Independent Service Organizations (ISOs) to Create Lucrative Opportunities

The medical equipment maintenance market presents substantial growth opportunities driven by technological innovation and evolving service delivery models. The emergence and rapid expansion of Independent Service Organizations (ISOs) represent a transformative opportunity, with these specialized providers typically charging 30-50% less than OEMs for equivalent maintenance services. ISOs offer faster turnaround times, multi-vendor capabilities, and personalized service approaches that address the cost-efficiency needs of healthcare facilities while maintaining quality standards.

The integration of Internet of Things (IoT) and artificial intelligence (AI) technologies into maintenance operations creates unprecedented opportunities for delivering predictive and proactive services. IoT-enabled continuous monitoring enables real-time tracking of equipment performance, while AI-powered predictive analytics identify potential equipment failures before they occur, allowing for timely interventions that minimize downtime and reduce costs.

Additionally, the shift toward subscription-based and outcome-oriented service contracts presents opportunities for long-term partnerships that align incentives between service providers and healthcare organizations, ensuring cost predictability and sustained equipment uptime. Remote diagnostic capabilities and digital twin technologies enable service providers to deliver faster, more efficient maintenance while reducing operational costs.

Market Challenges

Cybersecurity Vulnerabilities in Connected Medical Devices to Hinder Market Growth

The medical equipment maintenance market confronts multifaceted challenges that test service providers' adaptability and operational capabilities. The highly fragmented and intensely competitive market structure presents substantial viability challenges, particularly for smaller players lacking the capital resources to retain skilled biomedical engineers, manage complex logistics, and navigate regulatory approvals. With service providers ranging from multinational corporations to small local entities offering similar services, price competition intensifies, compressing profit margins and forcing industry consolidation. This competitive pressure is amplified by ISOs charging 30-50% less than OEMs, compelling original manufacturers to reduce service contract prices while maintaining quality standards.

Cybersecurity vulnerabilities in medical devices represent an escalating challenge with potentially catastrophic implications for patient safety and data security. Approximately 14% of connected medical devices operate on unsupported or end-of-life operating systems, while 99% of healthcare organizations remain vulnerable to publicly available exploits. Medical device manufacturers and maintenance providers face increasing regulatory pressure to implement robust cybersecurity measures throughout the device lifecycle, with the FDA's 2023 guidance mandating comprehensive security risk management plans. The complexity of ensuring security while maintaining device functionality and conducting timely updates creates operational tensions that maintenance providers must navigate carefully.

Additionally, standardizing maintenance protocols across proprietary vendor platforms while managing the technical obsolescence of legacy equipment presents persistent operational hurdles that require continuous adaptation and investment.

Medical Equipment Maintenance Market Trends

Shifting Preference Toward Subscription-based Service Models to Fuel Demand

The medical equipment maintenance market is undergoing a significant transformation, characterized by several defining trends that are reshaping service delivery and operational paradigms. The accelerating adoption of predictive maintenance powered by IoT sensors and artificial intelligence represents the most prominent trend, enabling real-time equipment monitoring and proactive failure prevention. Healthcare providers increasingly leverage these technologies to transition from reactive repair models to data-driven preventive strategies, achieving equipment uptime improvements of 40-50% while reducing overall maintenance costs by 25%.

The proliferation of subscription-based service models and multi-vendor maintenance contracts constitutes another major trend, with healthcare facilities seeking to consolidate disparate vendor relationships into unified service agreements that reduce complexity and costs. Multi-vendor service offerings enable centralized management across different equipment brands and modalities, providing healthcare systems with streamlined operations and greater negotiating leverage. For instance, GE Healthcare's Assure Point multi-vendor service exemplifies this trend by supporting imaging equipment from various manufacturers.

Remote diagnostics and telehealth integration are revolutionizing maintenance delivery, enabling technicians to troubleshoot and resolve issues remotely without the need for physical site visits, thereby reducing response times and travel costs. Siemens Healthineers' Smart Remote Services and similar platforms demonstrate how secure remote connections enable continuous monitoring, proactive issue detection, and remote software updates. The COVID-19 pandemic accelerated the adoption of these remote capabilities, establishing them as permanent operational standards.

Additionally, environmental sustainability concerns are also influencing maintenance strategies, with healthcare providers increasingly prioritizing the extension of equipment lifecycles and refurbishment to reduce electronic waste and support circular economy principles.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Service Type

High Medical Devices Installed Base to Drive Preventive Maintenance Segment Dominance

Based on service type, the market is classified into preventive maintenance, corrective/breakdown maintenance, and operational/performance maintenance.

The preventive maintenance segment held the largest market share in 2025. The dominant share is attributed to a large portion of installed medical devices, including ultrasound machines, CT scanners, MRI scanners, tabletop analyzers, motorized beds, ventilators, infusion systems, and surgical equipment, which require regular maintenance to increase their performance and lifespan. This, along with the growing focus of key players toward research and development activities to launch innovative devices, is further anticipated to support the segmental growth.

The operational/performance maintenance segment is expected to grow at a CAGR of 9.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Device Type

Advancements in Diagnostic and Medical Imaging Equipment Led to the Dominance of the Segment

Based on device type, the market is segmented into imaging equipment, life support equipment, patient monitoring equipment, surgical & endoscopy devices, laboratory & diagnostic equipment, dental equipment, and others.

The imaging equipment segment dominated the global market with a 46.9% share in 2025. The advancement in imaging equipment is increasing the demand for advanced medical equipment maintenance services.

- For instance, in June 2024, Siemens Healthineers launched its Biograph Trinion, an energy-efficient Positron Emission Tomography/Computed Tomography (PET/CT) scanner, aiming to strengthen its product portfolio.

The segment of surgical & endoscopy devices is poised for growth, with a forecasted rate of 10.0% across the period.

By Service Provider

Original Equipment Manufacturers (OEMs) Mostly Offer Maintenance Service to their Products, Leading to Dominance of Segment

Based on service provider, the market is segmented into original equipment manufacturers (OEMs), independent service organizations (ISOs), in-house maintenance, and hybrid maintenance models. The original equipment manufacturers (OEMs) segment dominated the global market with a 53.4% share in 2025. The dominance of the segment is due to the innovation in medical equipment maintenance services by OEMs.

- For instance, in October 2024, GE announced the “OnWatch Predict” platform, which uses IoT/AI to monitor equipment, reducing unplanned downtime by ~58% and saving ~36 hours of downtime per activation.

The segment of hybrid maintenance models is poised for growth, with a CAGR of 10.7% across the forecast period.

By End-user

Large Medical Devices Installed Base in Hospitals & ASCs Led to Segment’s Dominance

Based on end-user, the market is segmented into hospitals & ASCs, clinics, diagnostic imaging centers, clinical & research laboratories, and others.

The hospitals & ASCs settings segment dominated the market in 2025. The increasing prevalence of chronic conditions, a growing patient pool, and a rising preference for treatment in hospital settings, as well as rising research and development funding initiatives among key players, are key factors driving the growth of the segment in the market. Furthermore, the segment is set to hold a 61.1% share in 2025.

In addition, clinical & research laboratories end users are projected to grow at a CAGR of 9.8% during the study period.

Medical Equipment Maintenance Market Regional Outlook

In terms of region, the market is divided into North America, Asia Pacific, Latin America, Europe, and the Middle East & Africa.

North America Medical Equipment Maintenance Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America solidified its leadership with a market size of USD 23.84 billion and is expected to maintain its dominance with USD 25.46 billion in 2026. The stronghold is powered by escalating chronic disease cases, advanced healthcare infrastructure, supportive reimbursement frameworks, rapid digital health integration, and continual product launches from leading players. The U.S. market is poised to reach USD 22.41 billion in 2026.

- For instance, according to the U.S. Department of Health and Human Services, it is estimated that 129 million people in the U.S. have at least 1 major chronic disease, such as heart disease, cancer, diabetes, obesity, hypertension, etc.

Europe

Europe is projected to record a growth rate of 7.6% and reach a valuation of USD 16.08 billion by 2026, thereby securing its position as the second-largest region in the market. This momentum stems from rapid enhancements in healthcare infrastructure, a rising burden of diseases, and the strategic push by leading players to introduce innovative services and reinforce their regional networks. As a result, major markets are expected to expand steadily, with the U.K. projected to reach USD 2.41 billion, Germany USD 3.54 billion, and France USD 2.89 billion by 2026.

Asia Pacific

The market in Asia Pacific is projected to reach USD 15.52 billion by 2026. In the region, India is estimated to reach USD 2.33 billion while China is estimated to reach USD 4.35 billion in 2026.

Latin America and Middle East & Africa

Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. Latin America is expected to reach a valuation of USD 4.54 billion in 2026. The growing prevalence of chronic conditions, rising R&D funding initiatives, and adoption of advanced services are anticipated to fuel the demand for medical equipment maintenance services in the market. In the Middle East & Africa, GCC is set to attain the value of USD 1.65 billion in 2026.

Competitive Landscape

Key Industry Players

Rising Introduction of Innovative Services Among the Prominent Players to Support Their Dominance

The market leadership of major players is reinforced by their extensive service portfolios and cutting-edge product offerings, supported by a firmly established global footprint. Companies such as GE HealthCare, Siemens Healthineers AG, Koninklijke Philips N.V., and CANON MEDICAL SYSTEMS CORPORATION continue to dominate the landscape in 2024. Their growing emphasis on strategic partnerships with healthcare providers, particularly for the installation and maintenance of capital medical equipment, further fuels the medical equipment maintenance market share.

- For instance, in October 2024, Siemens Healthineers signed an imaging value partnership worth over USD 60.3 million with University Hospital Nantes. The partnership will span 12 years and focus on 13 public hospitals, with the imaging manufacturer installing new equipment, collaborating on research, and helping to pursue sustainability goals.

Meanwhile, other prominent players, including Drägerwerk AG & Co. KGaA, Medtronic, FUJIFILM Holdings Corporation, Baxter, B. Braun Melsungen AG, and Shenzhen Mindray Bio-Medical Electronics Co., Ltd., are strengthening their foothold through acquisitions, mergers, and market expansion initiatives.

List of Key Medical Equipment Maintenance Companies Profiled:

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherland)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Drägerwerk AG & Co. KGaA (Germany)

- Medtronic (Ireland)

- FUJIFILM Holdings Corporation (Japan)

- Baxter (U.S.)

- Braun Melsungen AG (Germany)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS:

- July 2025 - Safe Life AB completed the acquisition of Singapore-based HTM Medico, a distributor & service provider, to expand its equipment maintenance footprint in the Asia Pacific region.

- April 2024 – TRIMEDX announced the launch of GeoSense, a Real-Time Location System (RTLS) for health care. TRIMEDX GeoSense provides health systems with accurate and timely medical device tracking data by using next-generation, multi-modal technology that is lightweight, room-level precise, and easy to implement.

- November 2022 - Siemens Healthineers and Atrium Health, a leading nonprofit healthcare provider recognized for its top-ranked pediatric, cancer, and heart care programs, announced a multi-year Value Partnership agreement. This strategic agreement will focus on driving access to care in Atrium Health’s service region across the southeastern U.S.

- August 2022 - US Med-Equip, a leading provider of rented medical equipment and services, announced its acquisition of Freedom Medical to meet the growing equipment and service needs of hospitals and other healthcare partners throughout the country.

- June 2022 – Siemens Healthineers announced the launch of the company’s Technology Optimization Partnerships at the Association for the Advancement of Medical Instrumentation (AAMI) eXchange event in San Antonio, Texas. Technology Optimization Partnerships are a strategic approach to multivendor service that leverages connected solutions to help hospitals and health systems make data-driven decisions, improve equipment utilization, and enhance financial performance across the enterprise.

REPORT COVERAGE

The market report provides a detailed global medical equipment maintenance market analysis and focuses on key aspects such as leading companies, service type, device type, service provider, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Service Type

By Device Type

By Service Provider

By End User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 59.71 billion in 2025 and is projected to reach USD 124.89 billion by 2034.

In 2025, the North America regional market value stood at USD 23.84 billion.

Growing at a CAGR of 8.5%, the market will exhibit steady growth over the forecast period (2026-2034).

By service type, the preventive maintenance segment led the market in 2025.

Rising demand for advanced medical devices across healthcare facilities is driving the market's growth.

GE HealthCare, Siemens Healthineers AG, Koninklijke Philips N.V., and CANON MEDICAL SYSTEMS CORPORATION are the major players in the global market.

North America dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 235

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us