Medical Exoskeleton Market Size, Share & Industry Analysis, By Product Type (Lower Body Exoskeletons, Upper Body Exoskeletons, and Full Body Exoskeletons), By Technology (Powered (Active) Exoskeletons and Passive Exoskeletons), By Indication (Spinal Cord Injury (SCI), Stroke, Multiple Sclerosis (MS), Cerebral Palsy, Parkinson’s Disease, and Others), By End User (Hospitals & Specialty Clinics, Rehabilitation Centers, Homecare Settings, and Others), and Regional Forecast, 2026-2034

Medical Exoskeleton Market Future Outlook

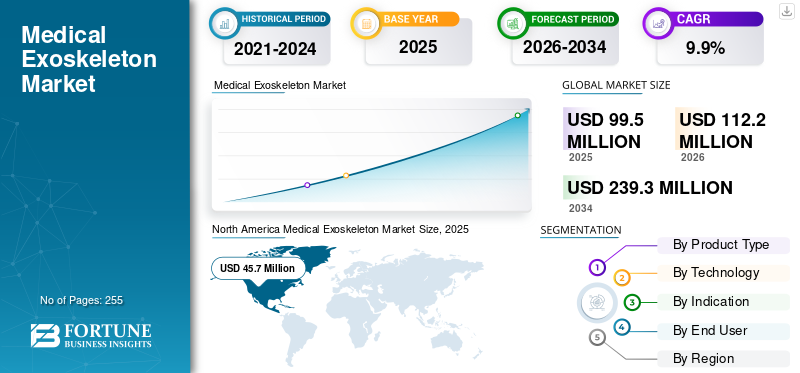

The global medical exoskeleton market size was valued at USD 99.5 million in 2025. The market is projected to grow from USD 112.2 million in 2026 to USD 239.3 million by 2034, exhibiting a CAGR of 9.9% during the forecast period. North America dominated the medical exoskeleton market with a market share of 46.16% in 2025.

Medical exoskeleton solutions comprise wearable robotic systems designed to assist or restore human movement in patients with neurological, musculoskeletal, or age-related mobility impairments. These systems are increasingly utilized across rehabilitation centers, hospitals, and homecare settings to support gait training, posture correction, and mobility assistance. The market growth is being fueled by the rising prevalence of spinal cord injuries, stroke, and neurodegenerative disorders, coupled with increasing investments in rehabilitation technologies.

- According to global health estimates, over 15 million people suffer a stroke annually, while 250,000–500,000 spinal cord injuries are reported each year worldwide, creating sustained demand for advanced mobility solutions.

Additionally, technological advancements in lightweight actuators, AI-driven gait algorithms, and battery efficiency are improving clinical outcomes and usability. The growing acceptance of robotic-assisted rehabilitation among clinicians, along with supportive reimbursement progress in countries such as the U.S. and Japan, is further accelerating market expansion. This, coupled with the increasing focus on new product launches among key players, is driving the focus of major companies, including Ekso Bionics Holdings, Inc., CYBERDYNE Inc., Lifeward, Inc., Hocoma AG, and Ottobock SE & Co. KGaA, and is expected to support the growth of the global market.

Download Free sample to learn more about this report.

Medical Exoskeleton Market Key Takeaways

- 2025 Market Size: USD 99.5 Million

- 2026 Market Size: USD 112.2 Million

- 2034 Forecast Market Size: USD 239.3 Million

- CAGR: 9.9% from 2026–2034

- North America dominated the medical exoskeleton market with a 46.16% share in 2025.

- The powered (active) exoskeletons segment held the largest market share of 81.8% in 2025.

- The spinal cord injury (SCI) segment accounted for the highest market share of 39.6% in 2025.

North America

North America led in 2025, driven by rehab infrastructure and assistive technology adoption.

Europe

Europe’s growth is supported by rehab technology investments and mobility solutions.

Asia Pacific

Asia Pacific growth is driven by healthcare expansion and rehab device demand.

U.S.

Reimbursement support, clinical adoption, and rehab centers drive market growth.

Japan

Robotic rehabilitation adoption and elderly mobility support are driving growth.

Read More

Medical Exoskeleton Market Trends

Technological Advancements in Medical Exoskeleton Enhancing Clinical Acceptance

Rapid innovation is shaping the evolution of medical exoskeletons, making them more adaptable and clinically effective. Advances in sensor integration, AI-driven gait optimization, and cloud-based analytics are enabling the development of personalized rehabilitation programs. Modern systems now offer real-time feedback, adaptive resistance, and data tracking, which improve therapy outcomes and clinician confidence. Battery improvements and lightweight materials are also enhancing patient comfort and session duration. Industry collaborations are accelerating this trend; for instance, partnerships between robotics firms and research institutes are focused on enhancing human–machine interaction and reducing the learning curve for therapists. As clinical evidence supporting robotic-assisted rehabilitation continues to grow, exoskeletons are increasingly viewed as complementary tools rather than experimental devices, supporting wider adoption.

Market Dynamics

Market Drivers

Rising Neurological Disease Burden to Drive Product Adoption

The increasing incidence of neurological and mobility-impairing conditions remains the primary driver of the medical exoskeleton market growth. Spinal cord injuries, stroke, multiple sclerosis, and Parkinson’s disease collectively account for millions of patients requiring long-term rehabilitation and mobility support.

- In the U.S. alone, nearly 18,000 new spinal cord injury cases are recorded annually, while stroke remains a leading cause of long-term disability.

Medical exoskeletons facilitate repetitive and intensive gait training, which has been shown to enhance neuroplasticity and improve functional recovery outcomes. On the industry front, companies are actively expanding their portfolios to address this demand.

- For instance, Ekso Bionics continues to broaden the clinical adoption of its EksoNR platform across rehabilitation hospitals. At the same time, Lifeward (ReWalk Robotics) has benefited from the expansion of reimbursement for personal exoskeletons in the U.S. Furthermore, CYBERDYNE’s HAL exoskeleton has seen increased deployment in Japanese hospitals, supported by the country’s aging population and robotics-friendly healthcare policies. These factors collectively underpin strong demand momentum.

Market Restraints

High Device Cost and Limited Reimbursement to Hamper the Market Growth

Despite strong clinical potential, the high cost of medical exoskeleton systems remains a major restraint. Powered exoskeletons can cost USD 70,000–150,000 per unit, making adoption challenging for smaller hospitals and rehabilitation centers, particularly in emerging markets. Limited or inconsistent reimbursement further compounds this issue. While the U.S. has made progress in covering personal exoskeletons for spinal cord injury patients, reimbursement in Europe, Latin America, and parts of Asia remains fragmented and slow-moving.

Additionally, the use of exoskeletons often requires trained therapists, infrastructure upgrades, and ongoing maintenance, which increases the total cost of ownership. Smaller healthcare facilities often struggle to justify these investments without guaranteed patient throughput. From an industry perspective, delayed procurement cycles in public healthcare systems, especially in Europe, continue to restrict rapid scale-up. These economic and structural barriers limit broader penetration, particularly outside high-income regions.

Market Opportunities

Homecare Expansion and Aging Population to Create New Growth Avenues

The growing shift toward home-based rehabilitation presents a significant opportunity for the medical exoskeleton market. Aging populations in countries such as Japan, Germany, and Italy are driving the demand for long-term mobility support solutions that reduce the dependence on institutional care.

- By 2030, one in six people globally is expected to be aged 60 or above, significantly increasing the addressable patient pool.

Companies are responding by developing lighter, more user-friendly exoskeletons suitable for supervised home use. For example, ReWalk’s personal exoskeleton systems are increasingly positioned for home and community ambulation, while several startups are working on modular, lower-cost designs.

Additionally, partnerships between device manufacturers and rehabilitation networks are expanding access to these devices. These trends open new revenue streams beyond hospitals and create opportunities for subscription-based and service-led business models.

Market Challenges

Training, Healthcare Infrastructure, and Clinical Integration of Medical Exoskeletons Creates Challenges for Industry Expansion

Integrating medical exoskeletons into routine clinical practice remains a significant challenge. The effective use requires trained therapists, standardized protocols, and patient screening, all of which vary across regions and facilities. Many healthcare providers report a learning curve associated with device setup, calibration, and patient handling.

Additionally, space constraints in older rehabilitation centers can limit deployment. Safety concerns, particularly for elderly or severely impaired patients, also necessitate careful supervision, which can reduce throughput in busy facilities. From a regulatory standpoint, navigating approval pathways and post-market surveillance requirements adds complexity for manufacturers. These challenges, while not insurmountable, slow adoption and require sustained investment in training, education, and the generation of clinical evidence.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Large Application of Lower Body Exoskeletons to Drive Segmental Dominance

Based on product type, the market is classified into lower body exoskeletons, upper body exoskeletons, and full body exoskeletons.

To know how our report can help streamline your business, Speak to Analyst

The lower body exoskeleton segment held the largest global medical exoskeleton market share in 2025. This is due to their broad applicability in gait rehabilitation and mobility assistance. Conditions such as spinal cord injury, stroke, and cerebral palsy primarily affect lower-limb function, making these systems clinically essential. Hospitals and rehabilitation centers often favor lower-body devices, as they address key goals of neurorehabilitation, including walking, standing, and balance.

The upper body exoskeleton segment is expected to grow at a CAGR of 14.1% over the forecast period.

By Technology

Increasing Preference for Powered (Active) Exoskeletons Led to the Dominance of the Segment

Based on technology, the market is segmented into powered (active) exoskeletons and passive exoskeletons.

The powered (active) exoskeletons segment dominated the global market with a share of 81.8% in 2025. Powered exoskeletons dominate the technology landscape, providing active assistance through motors and sensors that enable controlled, repeatable movement. These systems are preferred in clinical settings due to their ability to support patients with severe mobility impairments. Powered devices also generate measurable therapy data, which supports clinical validation and reimbursement discussions, making them the technology of choice in hospitals and advanced rehab centers.

Additionally, the passive exoskeletons segment is projected to grow at a CAGR of 13.6% during the study period.

By Indication

Increasing Prevalance of Spinal Cord Injury (SCI) Led to the Dominance of the Segment

Based on indication, the market is segmented into spinal cord injury (SCI), stroke, multiple sclerosis (MS), cerebral palsy, Parkinson’s disease, and others.

The spinal cord injury (SCI) segment dominated the global market with a share of 39.6% in 2025. Spinal cord injury represents the largest indication segment owing to the clear functional benefits exoskeletons offer to this patient group. SCI patients often require long-term gait training and mobility assistance, and exoskeletons provide one of the few viable solutions for upright ambulation. Reimbursement progress for SCI-focused exoskeletons, particularly in the U.S., has further strengthened this segment’s dominance.

Additionally, the cerebral palsy segment is projected to grow at a CAGR of 11.8% during the study period.

By End-user

Growing Number of Hospitals & Specialty Clinics Led to the Segment’s Dominance

Based on end-user, the market is segmented into hospitals & specialty clinics, rehabilitation centers, homecare settings, and others.

The hospitals & specialty clinics segment dominated the market in 2025. The dominance is due to their access to trained clinicians, substantial capital budgets, and the complexity of patient cases. These settings are often early adopters of advanced rehabilitation technologies and serve as reference sites for clinical validation. As a result, most initial deployments and product launches are targeted at hospital-based rehabilitation programs. Furthermore, the segment is set to hold a 57.3% share in 2026.

Additionally, the rehabilitation centers segment is projected to grow at a CAGR of 11.6% during the study period.

Medical Exoskeleton Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Exoskeleton Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

The North America medical exoskeleton market held the dominant share in 2025, valued at USD 45.7 million, and maintained its leading position in 2026, with a value of USD 52.2 million. North America dominates, driven by its strong clinical adoption ecosystem and favorable reimbursement landscape. The region has a high prevalence of spinal cord injuries and stroke-related disabilities, creating sustained demand for advanced rehabilitation solutions.

U.S. Medical Exoskeleton Market

Based on North America’s strong contribution and the U.S. dominance within the region. The U.S. market is estimated to reach around USD 47.6 million in 2026, accounting for roughly 42.4% of the global product sales.

Europe

Europe is projected to record a growth rate of 8.7% in the coming years, which is the third highest rate among all regions, and reach a valuation of USD 31.5 million by 2026. The regional market growth is driven by a strong rehabilitation infrastructure and rising emphasis on long-term neurorehabilitation. The region faces a growing burden of stroke and age-related mobility impairments, particularly in Western and Northern Europe. Public healthcare systems increasingly recognize the clinical value of robotic-assisted rehabilitation in improving patient outcomes and reducing long-term care costs.

U.K. Medical Exoskeleton Market

The U.K. market is estimated to be around USD 4.5 million in 2025, representing approximately 4.5% of global medical exoskeleton revenues.

Germany Medical Exoskeleton Market

Germany’s market is projected to reach approximately USD 5.7 million in 2025, equivalent to around 5.7% of global medical exoskeleton sales.

Asia Pacific

Asia Pacific is estimated to reach USD 21.7 million in 2026 and secure the position of the third-largest region in terms of value in the market. Asia Pacific is emerging as a high-growth region for the medical exoskeleton market, supported by demographic shifts and strong technological acceptance. Japan plays a pivotal role due to its rapidly aging population and long-standing integration of robotics into healthcare. The country’s supportive regulatory environment and hospital-led adoption of robotic rehabilitation systems have accelerated clinical uptake.

Japan Medical Exoskeleton Market

The Japan market, in 2026, is estimated to be around USD 6.1 million, accounting for roughly 5.5% of global medical exoskeleton revenues.

China Medical Exoskeleton Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 5.3 million, representing roughly 4.8% of global medical exoskeleton sales.

India Medical Exoskeleton Market

The India market, in 2026, is estimated to be around USD 2.7 million, accounting for roughly 2.4% of global medical exoskeleton revenues.

Latin America and Middle East & Africa

The growth in Latin America and the Middle East & Africa markets is driven by government-led healthcare modernization and investments in advanced rehabilitation infrastructure and technologies. Gulf Cooperation Council (GCC) countries, including Saudi Arabia and the UAE, are actively developing centers of excellence for rehabilitation and neurological care as part of broader healthcare transformation initiatives.

GCC Medical Exoskeleton Market

The GCC market is projected to reach approximately USD 1.9 million by 2026, accounting for roughly 1.7% of global market revenues.

Competitive Landscape

Key Industry Players

Increasing Focus on New Product Launches by Prominent Companies to Support their Domination

The medical exoskeleton market is moderately consolidated at the top and highly fragmented at the lower tiers, reflecting an early-to-mid commercialization stage. A small group of established players dominates global revenues through the development of clinically validated products, regulatory approvals, and expanding reimbursement coverage, while numerous regional and emerging companies operate at pilot or early deployment stages. Leading companies such as Ekso Bionics, CYBERDYNE, and Lifeward hold a strong competitive position due to their early market entry, broad clinical evidence base, and presence in major rehabilitation centers. These players continue to strengthen their portfolios through product upgrades, regulatory expansions, and strategic acquisitions.

- For instance, Ekso Bionics’ acquisition of the Indego exoskeleton line expanded its addressable patient base and strengthened its position in both clinical and personal mobility segments. Similarly, Lifeward’s FDA clearance and the U.S. commercial launch of ReWalk 7 reinforced its leadership in the spinal cord injury segment, supported by improving reimbursement acceptance.

Other key players, including Hocoma AG, Ottobock SE & Co. KGaA, Rex Bionics Ltd., and others, are also expanding in the market. This is primarily due to their increasing emphasis on R&D activities to develop advanced products and strengthen their market presence.

List of Key Medical Exoskeleton Companies Profiled

- Ekso Bionics Holdings, Inc. (U.S.)

- CYBERDYNE Inc. (Japan)

- Lifeward, Inc. (U.S.)

- Hocoma AG (Switzerland)

- Ottobock SE & Co. KGaA (Germany)

- Rex Bionics Ltd. (New Zealand)

- BIONIK Laboratories Corp. (Canada)

- Fourier Intelligence (China)

- Wandercraft (France)

- Honda Motor Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- March 2025 - Lifeward Ltd. announced that the company received 510(k) FDA clearance for the newest generation of its personal exoskeleton device, the ReWalk 7.

- March 2025 - Lifeward Ltd. and CorLife, LLC. jointly announced their finalization of an agreement for CorLife to become the exclusive distributor for the ReWalk Personal Exoskeleton for individuals with Workers’ Compensation claims.

- September 2024 – Human in Motion Robotics announced that XoMotion, the world's most advanced exoskeleton, received its first regulatory approval, for it to be marketed and sold in Canada.

- April 2023 - Harmonic Bionics, a rehabilitation robotics company, announced the registration of its flagship exoskeleton Harmony SHR with the FDA as a Class II 510(k)-exempt device.

- July 2022 - Ekso Bionics Holdings Inc. received approval from the U.S. Food and Drug Administration to market its EksoNR robotic exoskeleton for use with multiple sclerosis patients.

REPORT COVERAGE

The market report provides a detailed global medical exoskeleton market analysis and focuses on key aspects such as leading companies, product type, technology, indication, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market and advancements over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.9% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Product Type, Technology, Indication, End User, and Region |

|

By Product Type |

|

|

By Technology |

|

|

By Indication |

|

|

By End User |

|

|

By Region |

North America (By Product Type, By Technology, By Indication, By End User, and by Country)

Europe (By Product Type, By Technology, By Indication, By End User, and by Country/Sub-region)

Asia Pacific (By Product Type, By Technology, By Indication, By End User, and by Country/Sub-region)

Latin America (By Product Type, By Technology, By Indication, By End User, and by Country/Sub-region)

Middle East & Africa (By Product Type, By Technology, By Indication, By End User, and by Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 99.5 million in 2025 and is projected to reach USD 239.3 million by 2034.

In 2025, the North America market value stood at USD 45.7 million.

The market will exhibit steady growth at a CAGR of 9.9% over the forecast period (2026-2034).

By product type, the lower body exoskeletons segment was the leading segment in this market in 2025.

The rising neurological disease burden is one of the major factors driving the market's growth.

Ekso Bionics Holdings, Inc., CYBERDYNE Inc., Lifeward, Inc., Hocoma AG, and Ottobock SE & Co. KGaA are the major players in the global market.

North America dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 255

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us