Medical Polymers Market Size, Share & Industry Analysis, By Type (Fibers & Resins, Medical Elastomers, and Others), By Manufacturing Technology (Injection Molding, Extrusion Tubing, Compression Molding, and Others), By Application (Medical Devices & Equipment, Medical Packaging, and Others), and Regional Forecast, 2026-2034

(Offer valid till 31st Jul 2026)

KEY MARKET INSIGHTS

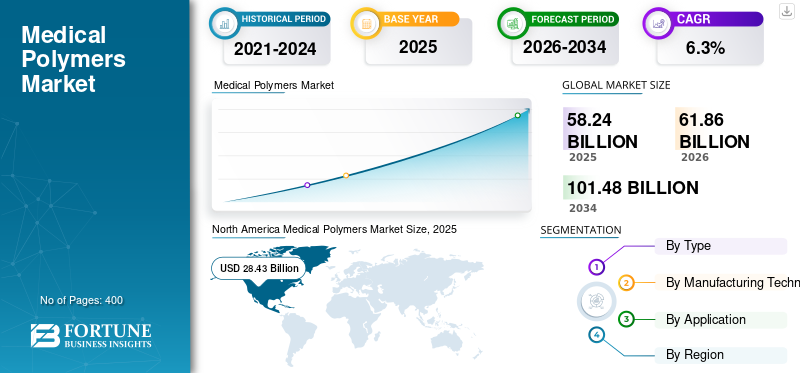

The global medical polymers market size was valued at USD 58.24 billion in 2025. The market is projected to grow from USD 61.86 billion in 2026 to USD 101.48 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period. North America dominated the global market with a share of 48.8% in 2025.

Medical polymers are polymeric materials used in the manufacturing of products for the medical and healthcare industries. These polymers are broadly categorized as fibers & resins, medical elastomers, and other types. Fibers and resins used in medical applications include PP, PE, PVC, PS, ABS, and other such polymers. Medical elastomers used in medical applications include silicone, thermoplastic elastomers, TPU, TPV, and SBS. Different types of medical polymers are used in a wide range of medical applications, including medical packaging, medical devices & equipment such as catheters, syringes, medical tubes, diagnostic instruments & tools, surgical instruments, and implants.

The outbreak of the COVID-19 pandemic had a mixed impact on the global medical polymers market growth. During the initial days of the outbreak, the manufacturing of medical products was negatively impacted due to disruptions in supply chains. However, in the later period of the pandemic, there was a significant rise in the demand for medical grade polymers due to the increasing adoption in medical devices and protective equipment. With the gradual control of the spread of the virus, manufacturing companies operating at their full capacity to meet the market demand.

Download Free sample to learn more about this report.

GLOBAL MEDICAL POLYMERS MARKET Key Takeaways

- 2025 Market Size: USD 58.24 billion

- 2026 Market Size: USD 61.86 billion

- 2034 Forecast Market Size: USD 101.48 billion

- CAGR: 6.3% from 2026–2034

- North America dominated the medical polymers market with a 48.80% share in 2025.

- The fibers and resins segment led the market accounting for 57.4% market share in 2026.

- The injection molding segment dominated the market accounting for 41.16% market share in 2026.

North America

North America market capturing 48.80% of the global market share, and is projected to reach USD 30.11 billion in 2026 and maintained its leading position due to a well-established healthcare infrastructure, strong R&D activities.

Europe

Europe accounting for 23.30% of the worldwide market, and is projected to grow to USD 14.37 billion in 2026, supported by expanding healthcare investments, an aging population, and increasing adoption of sustainable medical materials.

Asia Pacific

Asia Pacific stood at USD 13.02 billion in 2025, driven by rapid urbanization, rising healthcare expenditure, and growing demand for advanced medical technologies across emerging economies.

U.S.

The market is projected to reach USD 25.68 billion in 2026, supported by strong demand for medical packaging, advanced healthcare technologies, and continuous innovation in medical devices.

Japan

The market is projected to reach USD 1.70 billion in 2026, driven by increasing healthcare needs, an aging population, and rising adoption of high-performance medical materials.

Read More

Medical Polymers Market Trends

Technological Innovations and Rising Demand for Sustainable Producst to Present Lucrative Opportunities

In recent years, there have been outstanding technological innovations in the medical industry, ranging from consumable drugs to implantable medical devices. For instance, the development of smart polymers that respond to physiological changes, such as temperature and pH, can enable advanced drug delivery systems and enhance the effectiveness of medical devices. The rising budget allocation to research and development and the overall medical and healthcare sector is anticipated to further propel the growth of technological innovations and novel products.

Rising environmental regulations and concerns over the use and disposal of medical waste are resulting in the rising demand for sustainable and eco-friendly products. This trend is leading to rising investment in the development of bio-based and bio-degradable polymers, reducing the environmental hazards of medical waste and creating long-term market growth opportunities. North America witnessed a medical polymers market growth from USD 28.43 billion in 2025 and USD 30.11 billion in 2026.

Download Free sample to learn more about this report.

Medical Polymers Market Growth Factors

Increasing Adoption of Minimally Invasive Surgical Procedures to Drive Market Growth

The increasing adoption of minimally invasive surgical procedures is significantly driving the medical polymers market growth. These procedures, which involve smaller incisions and reduced tissue damage, rely heavily on advanced medical devices and components made from polymers. Medical polymers offer flexibility, durability, and biocompatibility, making them ideal for crafting catheters, stents, and other intricate devices required for these surgeries, thereby driving the market growth.

The demand for minimally invasive techniques is rising due to benefits, including shorter recovery time, less pain, and lower infection risks. This surge in demand boosts the need for high-performance, reliable medical polymers. Moreover, ongoing technological advancements in polymer science are enhancing the properties of these materials, ensuring they meet the stringent requirements of the minimally invasive procedure. As healthcare providers continue to prioritize patient comfort and outcomes, the reliance on such products is expected to grow, driving market growth.

RESTRAINING FACTORS

Stringent Regulatory Requirements and Approval Processes to Limit the Market Growth

The medical industry is highly regulated to ensure patient safety. Materials used in medical devices, packaging, and other applications must meet rigorous standards set by regulatory bodies such as the European Medicines Agency and the U.S. Food and Drug Administration. These regulatory hurdles can slow down the introduction of new medical polymer products to the market, increase development costs, and require extensive testing and documentation. This can make companies hesitant to invest in new medical polymers, thereby limiting market growth.

Medical Polymers Market Segmentation Analysis

By Type Analysis

Fibers And Resins Segment Held a largest Market Share Owing to its Wide Range Of Applications

Based on type, the market is segmented into fibers and resins, medical elastomers, and others.

The fibers and resins segment held the largest medical polymer market share in 2026 and is expected to retain its dominant position till 2034. The fibers and resins used in the medical industry include PP, PVS, PS, PE, and other similar resins and fibers. These fibers and resins are used in a wide range of medical applications, which has led to their higher market demand. The fibers and resins segment led the market accounting for 57.4% market share in 2026.

Medical elastomers used in the medical industry include silicones, thermoplastic elastomers, TPU, TPV, and other similar elastomers. This segment is expected to gain considerable growth prospects in the near future. The elastomers have relatively higher prices than the other polymers and are used in different medical applications, including medical devices & equipment, and packaging.

Other types of medical polymers mainly include biodegradable and environmentally friendly polymers such as polylactic acid and polyhydroxyalkanoate. These polymers are anticipated to witness a higher demand in the near future owing to rising demand for sustainable medical products.

By Manufacturing Technology Analysis

Injection Molding Segment Held the Largest Share Owing to High-volume Production of Medical Devices

Based on manufacturing technology, the market is segmented into injection molding, extrusion tubing, compression molding, and others.

The injection molding segment held the largest share of the market in 2026 and is anticipated to register the highest CAGR during the forecast period. Injection molding is widely used in the production of medical devices such as syringes, surgical instruments, and implantable devices. It allows high-volume production, precise control over product dimensions, and enables the creation of complex shapes with a high degree of repeatability. The injection molding segment dominated the market accounting for 41.16% market share in 2026.

The extrusion tubing segment is anticipated to grow at a considerable rate during the forecast period. Extrusion tubing involves forcing medical-grade polymers through a die to create tubes used in catheters, IV lines, and other medical devices.

The compression molding segment holds a considerable share of the global market. This technology placing the polymer in a heated mold cavity and compressed to form desired shapes. It is widely used to produce durable and complex medical components, including orthopedic implants and prosthetics.

Other technology mainly includes blow molding for creating hollow medical parts, 3D printing for custom implants and prototypes, and thermoforming for creating packaging solutions. This segment is anticipated to grow at a significant rate in the near future, owing to higher product customization offered by these techniques.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Medical Devices and Equipment Segment Held the Largest Market Share Owing to Increasing Investment in the Healthcare Industry

Depending on the applications, the market is segmented into medical devices & equipment, medical packaging, and others.

The medical devices & equipment segment held the largest share of the global market in 2026. The segment is anticipated to retain its majority share by the end of the forecast period, owing to the continuously rising demand for medical devices and equipment, including wearable, standalone, and implantable medical devices across the world. Increasing investment in the healthcare industry in emerging economies including China, India, Brazil, and South Africa, is anticipated to further drive the demand for the product as it is used in the manufacturing of medical devices and equipment. The medical devices & equipment segment is projected to dominate the market with a share of 64.29% in 2026.

The medical packaging segment is also anticipated to grow at a significant rate during the forecast period. The versatility, durability, and compatibility of medical polymers make them suitable for in several packaging applications, including sterile packaging, containers for medical devices, and protective films. Some of the medical-grade polymers are emerging as effective solutions for packaging different drug formulations, thereby driving market growth. This segment is likely to grow with a significant CAGR of 5.35% during the forecast period (2024-2032).

Other applications of medical polymer include cardio and tissue culture. The rising geriatric population in developed countries and increasing investment in tissue culture technology are anticipated to drive market growth in the near future.

REGIONAL INSIGHTS

By geography, the global medical polymer market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Medical Polymers Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America recorded a market size of USD 28.43 billion in 2025, capturing 48.80% of the global market share, and is projected to reach USD 30.11 billion in 2026 and accounted for the largest medical polymers market share. The well-developed healthcare industry, coupled with significant medical research and development, is fostering the growth of the medical polymer market in the region. Additionally, favorable regulatory frameworks and standards are enhancing the adoption of advanced medical polymers. The rising geriatric population in the region is driving the demand for medical devices and other healthcare products. The U.S. market is projected to reach USD 25.68 billion by 2026.

- In the U.S., the medical packaging segment is estimated to hold a 28.55% market share in 2023.

To know how our report can help streamline your business, Speak to Analyst

Euope

In 2025, Europe represented USD 13.56 billion, accounting for 23.30% of the worldwide market, and is projected to grow to USD 14.37 billion in 2026. Europe holds a considerable share of the global market owing to the rapidly developing healthcare industry in the region. The rising geriatric population in the region is continuously driving the demand for medical devices and equipment, propelling market growth. The U.K. market continues to expand, forecasted to reach a market value of USD 1.50 billion in 2025. Furthermore, robust healthcare funding, infrastructure support and a strong emphasis on bio-degradable and eco-friendly products are anticipated to fuel market growth during the forecast period. The UK market is projected to reach USD 1.6 billion by 2026, while the Germany market is projected to reach USD 3.03 billion by 2026. while France is set to hold USD 1.69 billion in the 2025.

Asia Pacific

The Asia Pacific market generated USD 13.02 billion in 2025, representing 22.40% of the global market landscape, and is expected to reach USD 13.98 billion in 2026. Rapid urbanization and industrialization in the Asia Pacific region have resulted in a significant rise in consumer expenditure, leading to increased demand for better healthcare and advanced medical technologies. The larger population of the region, coupled with increasing cases of chronic diseases, are anticipated to significantly drive the demand for medical products during the forecast period. Moreover, the rising healthcare expenditure by the governments of the emerging economies in the region, including China and India, is fueling market growth. The Japan market is projected to reach USD 1.7 billion by 2026, the China market is projected to reach USD 7.03 billion by 2026, and the India market is projected to reach USD 2.2 billion by 2026.

Latin America

In 2025, Latin America held 3.60% of the global market, reaching a valuation of USD 2.12 billion, and is projected to grow to USD 2.23 billion in 2026. The market in Latin America and the Middle East & Africa is expected to witness considerable growth during the forecast period. Increasing healthcare expenditure by governments and considerable financial aid for the healthcare sector from international organizations such as WHO and the World Bank are expected to play a crucial role in driving market growth. Economic development due to rising industrialization and increased access to medical services are significantly driving the demand for medical polymers. The higher number of chronic diseases in these regions further necessitates the use of advanced medical devices, driving market growth. Saudi Arabia is anticipated to stand at USD 0.40 billion in 2025.

Middle East & Africa

Middle East & Africa accounted for USD 1.1 billion in 2025, representing 1.90% of the global market share, and is projected to reach USD 1.16 billion in 2026.

KEY INDUSTRY PLAYERS

Manufacturing High-performance and Eco-Friendly Products can Provide the Competitive Edge to Manufacturers

Key players operating in the market include BASF SE, SABIC, Covestro, Celanese, Momentive Performance Material, and others. Established medical polymer manufacturers are investing in the development of high-performance and eco-friendly biodegradable polymers due to consumer preferences, environmental consciousness, and regulations. Prominent players in the market are also focusing on expanding their geographical footprint in different emerging markets across the world. The brand image of the established players and the technological expertise of the small and regional players in the manufacturing of specialized medical-grade polymers play a key role in industrial rivalry.

List of Top Medical Polymers Companies:

- BASF SE (Germany)

- SABIC (Saudi Arabia)

- Covestro Ag (Germany)

- Celanese (U.S.)

- Evonik (Germany)

- Arkema (France)

- Solvay (Belgium)

- Kuraray Co., Ltd. (Japan)

- Momentive Performance Material (U.S.)

- ExxonMobil (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- March 2024: SABIC announced that it has achievd successful step towards creation of the circular polymers based on advanced recyalinc of used medical plastics, The company ahs achievd this milestone in collaboration with JESSA HOSPITAL.

- October 2023 – Covestro began operations at its dedicated mechanical recycling compounding line for polycarbonates at its location in Shanghai, China. The company aimed to deliver over 25,000 tons of products annually.

- July 2023 – Evonik announced that its healthcare products manufacturing site in Ham, France, achieved carbon neutrality. The site develops and manufactures solutions for medical devices, active pharmaceutical ingredients, personal care, cosmetics, and nutrition for animals and humans.

- June 2023 – Arkem announced that it had broadened its range of high-performance polymers with the acquisition of the controlling stakes in the South Korean Company, PI Advanced Materials (PIAM).

- November 2021 – Arkema launched the new Advanced Bio-Circular polyamide 11 medical polymer. The products has high rigidity and intended to replace traditional polymers and metalas in medical applications.

REPORT COVERAGE

The market report provides detailed market analysis and focuses on crucial aspects such as leading companies, sources, applications, and products. Also, the report offers insights into market trends and dynamics and highlights vital industry developments and market outlook. In addition to the factors mentioned above, the report encompasses various factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.3% from 2026-2034 |

|

Unit |

Value (USD Billion); Volume (Kiloton) |

|

Segmentation |

By Type

|

|

By Manufacturing Technology

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global medical polymers market was valued at USD 58.24 billion in 2025 and is projected to reach USD 101.48 billion by 2034, growing at a CAGR of 6.3% during the forecast period.

In 2025, the market size in North America stood at USD 28.43 billion.

Growing at a CAGR of 6.3%, the market will exhibit steady growth during the forecast period.

The primary types include fibers and resins (such as polypropylene and polyethylene), medical elastomers (like silicone and thermoplastic elastomers), and biodegradable polymers (e.g., PLA and PHA). Fibers and resins hold the largest market share.

Increasing adoption of minimally invasive surgical procedures is the key factor driving market growth.

Common production methods include injection molding, extrusion, compression molding, blow molding, 3D printing, and thermoforming. Injection molding remains the most dominant due to its precision and scalability.

The leading application is in medical devices and equipment, including catheters, surgical tools, and implantables. Other growing applications include medical packaging and tissue engineering.

North America leads the market due to strong healthcare systems and innovation in medical technologies. Asia Pacific is the fastest-growing region, driven by expanding healthcare infrastructure and rising medical needs.

Market growth is fueled by the rising demand for minimally invasive procedures, advancements in biodegradable polymers, an aging global population, and the increased use of wearable and implantable medical devices.

BASF SE, SABIC, Covestro, Celanese, and Momentive Performance Material are some of the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 400

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us