Menopause Drugs Market Size, Share & Industry Analysis, By Therapy Type (Hormonal Therapies {Estrogen-based therapies, Progestogen-based therapies, Combination therapies, and Others} and Non-Hormonal Therapies {Neurokinin receptor antagonists, SSRI/SNRI therapies Gabapentinoids, GSM therapies, and Others}), By Disease Indication (Vasomotor Symptoms (VMS), Genitourinary Syndrome of Menopause (GSM), Sleep Disturbances, Mood Disorders, Postmenopausal Osteoporosis, Sexual Dysfunction, and Others), By Route of Administration, By Distribution Channel, and Regional Forecast, 2026-2034

Menopause Drugs Market Size and Future Outlook

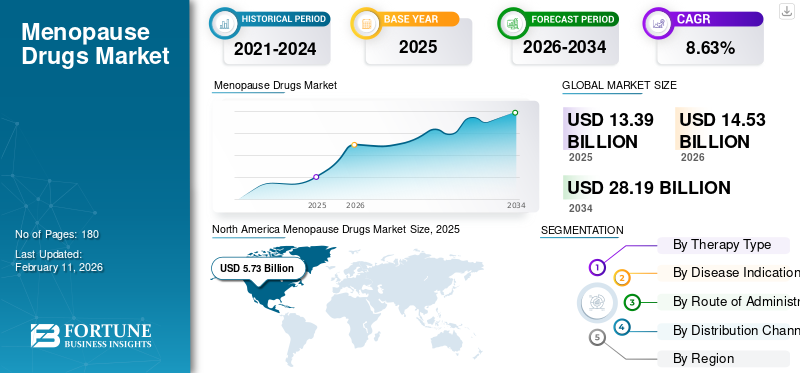

The global menopause drugs market size was valued at USD 13.39 billion in 2025. The market is projected to grow from USD 14.53 billion in 2026 to USD 28.19 billion by 2034, exhibiting a CAGR of 8.63% during the forecast period. North America dominated the global menopause drugs market with a market share of 42.79% in 2025.

The global menopause drugs market is experiencing steady and substantial growth, driven by the increasing mid-aged female population and awareness and prevalence of menopausal symptoms. These drugs are used to alleviate menopause symptoms such as hot flashes, mood swings, and osteoporosis risk, thereby fueling demand for effective menopause management options. Moreover, market players are investing in innovative therapies to improve safety profiles and address unmet needs, which is expected to continue boosting global market growth.

- For instance, in January 2026, AbCellera announced dosing its first patients in the Phase 2 portion of its ongoing Phase 1/2 clinical trial for ABCL635. ABCL635 is a potential non-hormonal treatment for moderate-to-severe vasomotor symptoms (VMS) associated with menopause.

Many key industry players, such as Bayer, Pfizer Inc., and Astellas, operating in the market, have expanded product portfolios and research and development activities to launch innovative drugs.

Download Free sample to learn more about this report.

MENOPAUSE DRUGS MARKET TRENDS

Shift Toward Development and Approval of Biosimilars is a Key Trend

The significant shift toward the development and approval of biosimilars is a key trend in the global menopause drugs market. The need for cost-effective and accessible treatment options further drives the expansion of the market. Biosimilars offer similar efficacy and safety profiles to original biologic therapies, making them attractive alternatives for hormone replacement therapies HRT used in menopause management.

Additionally, the adoption of biosimilars is expected to enhance patient access, reduce treatment costs, and foster innovation within the market.

- For instance, in January 2026, Hikma Pharmaceuticals PLC announced the launch of Enoby (denosumab-qbde) and Xtrenbo (denosumab-qbde), biosimilar products referencing Prolia and Xgeva, respectively.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Diagnosis and Treatment of Moderate-To-Severe VMS to Drive Market Growth

The increasing diagnosis and treatment of moderate-to-severe vasomotor symptoms (VMS) are driving market growth. The increasing awareness of menopause-related health issues leads to more women seeking effective management options for symptoms such as hot flashes and night sweats. Additionally, the rising prevalence of menopause-related discomfort and the availability of innovative, safer treatment options further boost market growth.

- For instance, in July 2024, in a BMC Public Health systematic review study, in around 482,067 middle-aged women, hot flashes (a core VMS symptom) were among the most common menopausal complaints, with a pooled global prevalence of 52.65% globally.

MARKET RESTRAINTS

Stringent Regulatory and Evidence Requirements to Restrict Market Growth

Stringent regulatory and evidence requirements are significantly restraining market growth. These rigorous standards often lead to prolonged approval processes, increasing time and costs for product development. Additionally, the need for extensive clinical evidence can delay market entry and limit innovation. Such restrictions may discourage companies from investing in new menopause treatments, ultimately constraining availability and accessibility for women. As a result, regulatory hurdles can act as a barrier to the development and adoption of advanced menopause therapies.

- For instance, in November 2023, Mithra Pharmaceuticals SA disclosed the FDA feedback indicating the need for additional requirements to support its DONESTA U.S. filing, illustrating how regulatory steps can extend timelines and constrain near-term market expansion.

MARKET OPPORTUNITIES

Rising Focus on Research and Development Activities to Boost Market Growth

The increasing focus of key pharmaceutical companies on research and development to launch innovative menopause drugs is offering a lucrative growth opportunity in the market. To address menopause-related health issues, there is a development of targeted therapies with improved efficacy and fewer side effects.

For instance, in October 2025, Bayer received approval for Lynkuet (elinzanetant) 60mg capsules from the U.S. Food and Drug Administration (FDA). It is the first and only dual neurokinin (NK) targeted therapy, a neurokinin 1 (NK1) and neurokinin 3 (NK3) receptor antagonist, for the treatment of moderate to severe hot flashes due to menopause.

MARKET CHALLENGES

Side Effects Associated with Hormonal Therapies to Challenge Market Growth

Hormonal therapies lead to side effects such as increased risk of blood clots, stroke, and certain types of cancer. Such side effects can deter patient acceptance and physician prescription.

Additionally, hormonal treatments may cause weight gain, mood swings, and breast tenderness, further impacting patient compliance, thus contributing to the decline in the growth of the menopause drugs market.

Segmentation Analysis

By Therapy Type

Hormonal Therapies Segment to Lead due to Increasing Demand For Menopause Drugs

Based on therapy type, the market is segmented into hormonal therapies and non-hormonal therapies.

The hormonal therapies segment is expected to account for the largest share of the menopause drugs market. The hormonal therapies segment held a 53.7% market share in 2025, driven by increasing demand for these drugs, as they offer an effective, fast-acting option for moderate-to-severe vasomotor symptoms. Additionally, the launch of the drug with improved packaging further boost the segment’s growth.

- For instance, in June 2023, Pfizer Inc. announced the availability of DUAVEE (conjugated estrogens/bazedoxifene), an estrogen-based menopause hormone therapy, in the U.S. with improved packaging, following a voluntary recall.

The non-hormonal therapies segment is expected to grow at a CAGR of 11.12% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Rising Vasomotor Symptoms (VMS) in Menopausal Women to Lead the Segment’s Growth

Based on disease indication, the market is segmented into vasomotor symptoms (VMS), genitourinary syndrome of menopause (GSM), sleep disturbances, mood disorders, postmenopausal osteoporosis, sexual dysfunction, and others.

The vasomotor symptoms (VMS) segment is anticipated to witness a dominant market share over the forecast period. The segment held a 51.9% market share in 2025, driven by the rising prevalence of the VMS in women going through menopause, which is contributing to the increased demand for drugs.

- For instance, in November 2024, Elsevier published a study based on an online survey of Brazilian women aged 40-65 years. The findings indicated that 36.2% of postmenopausal women, among the 1,244 respondents, experienced moderate-to-severe vasomotor symptoms (VMS).

The genitourinary syndrome of menopause (GSM) segment is projected to grow at a CAGR of 7.77% over the forecast period.

By Route of Administration

Ease of Administration and Availability Bolstered the Oral Segment’s Growth

Based on route of administration, the market is segmented into oral, transdermal, vaginal,

intrauterine, and others.

The oral segment held a dominant share, with a 64.9% market share in 2025. The segment's growth is attributed to ease of administration and improved bioavailability. Additionally, patient preference for oral medication and new product launches associated with it are driving the segment’s growth.

- For instance, in December 2023, Astellas Pharma Inc. announced that the European Commission (EC) had approved VEOZATM (fezolinetant) 45 mg once daily for the treatment of moderate to severe vasomotor symptoms (VMS) associated with menopause.

The transdermal segment is projected to grow at a CAGR of 6.49% over the forecast period.

By Distribution Channel

Drug Stores & Retail Pharmacies Segment Dominated due to Ease of Availability

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

In 2025, the drug stores & retail pharmacies sector accounted for a 69.7% share of the market. The segment's dominant share is attributed to patients' preference, ease of availability, and the fact that pharmacist consultation improves trust and the distribution of drugs through these channels. Along with that, rising strategic initiatives by key players to promote their products are boosting the segment’s growth.

- For instance, in January 2026, Bayer partnered with actress and advocate Gabrielle Union-Wade as the official face of Lynkuet (elinzanetant), a newly launched hormone-free menopausal medication.

The online pharmacies segment is growing at a compound annual growth rate of 16.37% over the forecast period.

Menopause Drugs Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Menopause Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 5.26 billion and maintained its leading position in 2025 at USD 5.73 billion. The market in North America is expected to grow due to the rising prevalence and regulatory approval for the new and advanced hormone-free drugs.

U.S. Menopause Drugs Market

Given North America’s substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 5.27 million in 2025, accounting for roughly 39.3% of global menopause drug sales.

Europe

Europe is projected to grow at 7.33% over the coming years and reach a valuation of USD 3.61 billion in 2025. The region’s market growth is driven by the rising number of menopausal women, the increasing demand for adequate therapy, and the presence of key players with advanced product offerings.

U.K. Menopause Drugs Market

The U.K. menopause drugs market in 2025 reached around USD 0.67 billion, representing approximately 5.0% of revenues.

Germany Menopause Drugs Market

Germany’s menopause drugs market is projected to reach approximately USD 0.87 billion in 2025, equivalent to around 6.5% of the global sales.

Asia Pacific

Asia Pacific stood at USD 2.76 billion in 2025 and secured the position of the third-largest region in the market. In the region, India and China are both estimated to reach USD 0.36 billion and USD 0.88 billion, respectively, in 2025. The increasing demand for the product, driven by a larger patient pool, is expected to boost the region’s market growth.

Japan Menopause Drugs Market

The Japan market in 2025 is estimated at around USD 0.46 billion, accounting for roughly 3.5% of global revenues.

China Menopause Drugs Market

China’s menopause drugs market is projected to be one of the largest worldwide, with 2025 revenues reaching around USD 0.88 billion, representing roughly 6.6% of global sales.

India Menopause Drugs Market

The Indian menopause drugs market in 2025 is estimated at around USD 0.36 billion, accounting for roughly 2.7% of global menopause drugs revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in the market during the forecast period. The Latin American market reached a valuation of USD 0.68 billion in 2025. The region's growth is attributed to product launches, drug approvals, and an increased patient population. In the Middle East & Africa, the GCC is set to reach USD 0.31 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Emphasis on Obtaining Approvals to Boost their Market Position

The global menopause drugs market is semi-consolidated. Bayer and Astellas Pharma hold prominent positions in the fast-growing non-hormonal VMS space, supported by strong clinical evidence. Additionally, these players are focused on obtaining approvals across different countries to boost their market position.

- For instance, in July 2025, Bayer announced that the Medicines and Healthcare products Regulatory Agency (MHRA) had authorized the use of elinzanetant, the first dual neurokinin (NK)-targeted therapy (NK-1 and NK-3 receptor antagonist), Lynkuet, for the treatment of moderate to severe vasomotor symptoms in menopausal women in the U.K.

Other notable players, such as Pfizer, Inc., and Novo Nordisk, remain important due to established hormonal portfolios, strong leadership, and expanded footprints, which continue to support their market presence.

LIST OF KEY MENOPAUSE DRUGS COMPANIES PROFILED

- Bayer (Germany)

- Astellas Pharma Inc. (Japan)

- Pfizer Inc. (U.S.)

- Novo Nordisk (Denmark)

- Hisamitsu Pharmaceutical (Japan)

- Teva Pharmaceuticals Company Limited (Israel)

- Viatris (U.S.)

- Amneal Pharmaceuticals (U.S.)

- AbbVie Inc. (U.S.)

- Organon (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Noema Pharma AG announced positive topline results from a Phase 2a trial for cendifensine in menopausal women experiencing moderate-to-severe vasomotor symptoms (VMS), including hot flashes and night sweats.

- December 2024: Astellas Pharma announced that Health Canada approval of VEOZAH, the first and only non-hormonal treatment indicated for the treatment of moderate to severe vasomotor symptoms (VMS) associated with menopause.

- June 2022: Organon agreed with Shanghai Henlius Biotech, Inc. to give commercialization rights for biosimilar candidates referencing Perjeta and Prolia/Xgeva, which are used for the treatment of postmenopausal osteoporosis and breast cancer.

- May 2022: Organon announced that coverage of PROMETRIUM and ESTROGEL under Régie de l’assurance maladie du Québec (RAMQ) in Québec. This helps to have access to menopause hormone therapy.

- March 2021: Theramex announced Decentralized Procedure approval in EU countries and the U.K. for Bijuva (Estradiol & Progesterone) capsules for hormone replacement therapy.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2034 |

|

Growth Rate |

CAGR of 8.63% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Therapy Type, Disease Indication, Route of Administration, Distribution Channel, and Region |

|

By Therapy Type |

· Hormonal Therapies o Estrogen-based therapies o Progestogen-based therapies o Combination therapies o Others · Non-Hormonal Therapies o Neurokinin receptor antagonists o SSRI/SNRI therapies o Gabapentinoids o GSM therapies o Others |

|

By Disease Indication |

· Vasomotor Symptoms (VMS) · Genitourinary Syndrome of Menopause (GSM) · Sleep Disturbances · Mood Disorders · Postmenopausal Osteoporosis · Sexual Dysfunction · Others |

|

By Route of Administration |

· Oral · Transdermal · Vaginal · Intrauterine · Others |

|

By Distribution Channel |

· Hospital Pharmacies · Drug Stores & Retail Pharmacies · Online Pharmacies |

|

By Region |

· North America (By Therapy Type, Disease Indication, Route of Administration, Distribution Channel, and Country) o U.S. o Canada · Europe (By Therapy Type, Disease Indication, Route of Administration, Distribution Channel and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Therapy Type, Disease Indication, Route of Administration, Distribution Channel and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Therapy Type, Disease Indication, Route of Administration, Distribution Channel and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Therapy Type, Disease Indication, Route of Administration, Distribution Channel, and Country/Sub-region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 13.39 billion in 2025 and is projected to reach USD 28.19 billion by 2034.

In 2024, the market value stood at USD 5.73 billion.

The market is expected to grow at a CAGR of 8.63% over the forecast period (2026-2034).

By therapy type, the hormonal therapies segment is expected to lead the market.

The rising cases of menopause and symptoms associated with it are the key factors driving market expansion.

Pfizer Inc. and Bayer are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us