Metal Glass Market Size, Share & Industry Analysis, By Type (Ribbons, Bulk Metallic Glass, Wires, Coatings, and Others), By Application (Transformer Cores, Inductors & Chokes, Sensors, Structural Components, Medical Devices, Aerospace Components, and Others), and Regional Forecast, 2026-2034

Metal Glass Market Size and Future Outlook

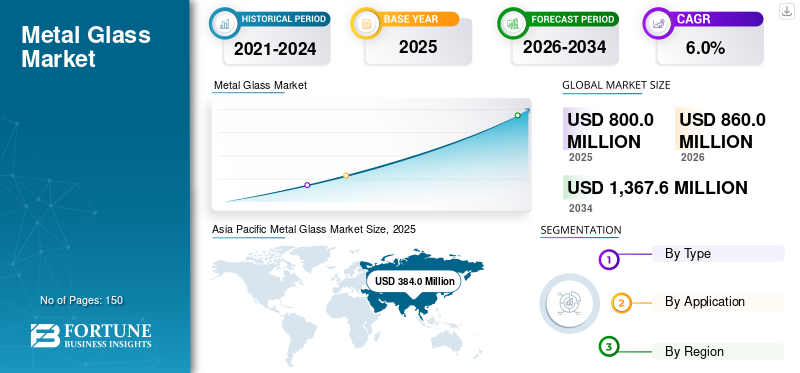

The global metal glass market size was valued at USD 800.0 million in 2025. The market is projected to grow from USD 860.0 million in 2026 to USD 1,367.6 million by 2034, exhibiting a CAGR of 6.0% during the forecast period. Asia Pacific dominated the metal glass market with a market share of 48.% in 2025.

Metal glass, also known as amorphous metal, is a class of metallic materials characterized by a non-crystalline atomic structure formed through rapid solidification. Unlike conventional metals, metal glass lacks long-range atomic order, resulting in unique properties such as high strength, superior elasticity, excellent corrosion resistance, and low magnetic losses. These properties make metal glass highly suitable for transformer cores, inductors, sensors, medical devices, and aerospace components. Among applications, transformer cores dominate due to the material’s ability to significantly reduce energy losses in power distribution systems. Growing demand for energy-efficient electrical infrastructure, miniaturized electronic components, and high-performance structural materials continues to drive market expansion. Additionally, advancements in bulk metallic glass processing and additive manufacturing are broadening the application scope. The market remains technology-driven, supported by specialized manufacturers focusing on performance-critical industries. Proterial, Ltd., Qingdao Yunlu Advanced Materials Technology Co., Ltd., Zhejiang Zhaojing Electrical Technology Co., Ltd., VACUUMSCHMELZE GmbH & Co. KG (VAC), and Metglas, Inc. are the major companies operating in the market.

Download Free sample to learn more about this report.

METAL GLASS MARKET TRENDS

Energy Efficiency Standards and Miniaturization Shaping Market Evolution

The market is evolving in response to stricter global energy efficiency standards and increasing demand for miniaturized, high-performance components. A key trend is the adoption of amorphous metal ribbons in next-generation transformer cores to reduce core losses and improve grid efficiency. Governments worldwide are implementing policies encouraging low-loss transformers, accelerating demand. Another important trend is the expansion of bulk metallic glass applications in precision structural components due to its high strength-to-weight ratio and elasticity. Miniaturization in electronics is also promoting the use of metal glass in inductors and sensors. Technological advancements in casting and thermoplastic forming techniques are enabling larger and more complex bulk metallic glass components. These trends reflect a structural shift toward high-efficiency and high-performance materials, thus shaping the long-term trajectory of the metal glass market.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Superior Magnetic Properties and Mechanical Strength Sustaining Demand

The primary driver of the market is its superior magnetic performance compared to conventional silicon steel. Amorphous metal ribbons exhibit significantly lower core losses, making them highly effective in energy-efficient transformers and inductors. Rising global electricity consumption and grid modernization initiatives directly support demand for such materials. Additionally, bulk metallic glass offers exceptional strength, hardness, and corrosion resistance, driving adoption in structural and aerospace applications. Increasing emphasis on reducing energy waste and improving system efficiency reinforces the use of metal glass in electrical infrastructure. Growing investment in renewable energy and smart grids further supports consumption. These performance advantages ensure sustained demand across the energy and high-technology sectors, thereby maintaining stable metal glass market growth.

MARKET RESTRAINTS

High Production Costs and Processing Limitations Restricting Market Penetration

Despite strong performance benefits, the market faces restraints related to production complexity and cost. Manufacturing amorphous metals requires rapid solidification processes and precise temperature control, increasing operational expenses. Bulk metallic glass components are limited in size due to cooling rate constraints, restricting broader structural applications. Additionally, specialized equipment and technical expertise are necessary for forming and shaping operations. Competition from conventional magnetic materials and advanced composites also limits penetration in cost-sensitive markets. Limited awareness among end users further restricts widespread adoption. These technical and economic barriers reduce scalability and market accessibility, hence moderating the overall growth rate of the market.

MARKET OPPORTUNITIES

Electrification and Advanced Material Demand Creating Expansion Potential

The market presents strong opportunities driven by global electrification, renewable energy integration, and demand for advanced materials. Expansion of power transmission and distribution networks increases demand for high-efficiency transformer cores made from amorphous metal ribbons. The market growth in electric vehicles and renewable energy systems further supports advanced magnetic component requirements. Another opportunity lies in aerospace and medical applications, where lightweight, corrosion-resistant, and high-strength materials are increasingly preferred. The development of additive manufacturing technologies enables complex geometries in bulk metallic glass components, opening new design possibilities. Additionally, rising focus on energy conservation and carbon reduction policies enhances demand for low-loss magnetic materials. These expanding application areas and technological innovations collectively create significant growth potential, therefore strengthening long-term prospects for the market.

MARKET CHALLENGES

Scalability Constraints and Material Handling Requirements Affecting Commercial Expansion

A major challenge in the market is scaling production while maintaining uniform amorphous structure and performance consistency. Manufacturing larger bulk components without crystallization remains technically demanding. Additionally, forming and machining require specialized thermoplastic processing techniques to prevent structural degradation. Supply chain limitations for high-purity raw materials further add complexity. Ensuring long-term reliability and quality assurance in critical infrastructure applications also poses challenges. Overcoming these barriers demands continuous R&D investment and advanced manufacturing solutions, therefore influencing commercialization pace and competitive positioning within the market.

RESEARCH AND DEVELOPMENT ACTIVITIES

R&D efforts focus on developing new alloy compositions with improved glass-forming ability and thermal stability. Advances in thermoplastic forming and additive manufacturing are enabling larger and more complex bulk metallic glass parts. These innovations enhance performance and broaden application potential.

Segmentation Analysis

By Type

Low Core Loss Characteristics Driving Dominant Market Share of Ribbons

By type, the market is segmented into ribbons, bulk metallic glass, wires, coatings, and others.

Ribbons segment held the leading metal glass market share in 2025. The growth of this segment is driven by its extensive use in transformer cores and magnetic components. Produced through rapid solidification, these thin strips exhibit excellent magnetic permeability and extremely low core losses compared to conventional electrical steels. Rising global demand for energy-efficient transformers in power transmission and distribution networks directly supports ribbon consumption. Additionally, their ease of lamination and integration into transformer designs enhances adoption. Government regulations promoting low-loss transformers further reinforce segment dominance. The combination of performance efficiency and established industrial usage ensures sustained high-volume demand, thus maintaining ribbons as the largest segment in the market.

Bulk metallic glass segment is set to grow at a CAGR of 5.6% during the forecast period. The product offers exceptional strength, elasticity, and corrosion resistance, making it suitable for structural components, medical devices, and precision engineering parts. Unlike ribbons, BMG can be formed into three-dimensional shapes through thermoplastic processing. Growth in the aerospace and medical sectors supports demand for lightweight and high-performance materials.

Wires are used in precision magnetic sensors, inductors, and electronic components due to their soft magnetic properties and mechanical flexibility. Miniaturization in electronics supports consistent demand. While smaller in share compared to ribbons, niche electronic applications sustain moderate growth, therefore reinforcing relevance. The segment is expected to grow at a CAGR of 4.8% during the forecast period.

By Application

Energy Efficiency Regulations Driving Dominant Adoption of Transformer Cores

By application, the market is segmented into transformer cores, inductors & chokes, sensors, structural components, medical devices, aerospace components, and others.

Transformer cores represent the leading application segment in the market due to the material’s exceptionally low core loss and high magnetic permeability. Amorphous metal ribbons significantly reduce no-load losses in distribution transformers compared to conventional silicon steel. Rising global electricity consumption, grid modernization initiatives, and integration of renewable energy sources are accelerating demand for high-efficiency transformers. Government regulations mandating energy-efficient electrical equipment further reinforce adoption. Utilities increasingly prioritize long-term energy savings and carbon reduction, directly supporting metal glass usage. These structural energy efficiency requirements sustain dominant demand, thus maintaining transformer cores as the largest application segment in the market.

To know how our report can help streamline your business, Speak to Analyst

The inductors & chokes segment is anticipated to grow at a CAGR of 5.4% during the forecast period. Metallic glass is increasingly utilized in inductors and chokes due to its superior soft magnetic properties and low coercivity. These characteristics enhance efficiency in high-frequency electronic circuits and power conversion systems. Growing demand for compact power electronics in electric vehicles, renewable energy inverters, and consumer electronics supports segment growth. Additionally, miniaturization trends in electronic components require materials that deliver stable magnetic performance at reduced sizes. Metal glass enables improved energy transfer efficiency and reduced heat generation in such systems. As industries focus on enhancing power efficiency and reducing component size, demand for metal glass in inductors and chokes continues to expand, hence strengthening its application share.

In sensors, the metallic glass demand is growing due to their high permeability, low hysteresis loss, and excellent sensitivity to magnetic fields. These properties enable accurate detection in automotive systems, industrial automation, and smart devices. Growing adoption of IoT-enabled monitoring systems and industrial automation technologies is driving demand for high-precision sensors. Additionally, automotive safety systems and position-sensing applications rely on stable magnetic materials for reliable operation. Metal glass ensures durability and long-term performance stability, which are essential for sensor functionality. These performance-driven advantages support steady adoption, therefore reinforcing the role of metal glass in advanced sensing applications. The segment is expected to grow with a CAGR of 4.8% during the forecast period.

Metal Glass Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Metal Glass Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to the rapid expansion of power transmission networks and strong electrical and electronics manufacturing capacity. Countries such as China, Japan, and South Korea are major producers and consumers of amorphous metal ribbons used in energy-efficient transformer cores. Increasing electricity demand, renewable energy integration, and government mandates for low-loss transformers significantly boost adoption. Additionally, growth in electric vehicles and industrial automation supports demand for magnetic components and sensors. Competitive manufacturing costs and integrated supply chains strengthen regional competitiveness. These structural drivers ensure sustained high consumption, thus reinforcing the Asia Pacific’s leadership in the global market.

China Metal Glass Market

China’s market was valued at USD 192.0 million in 2025, accounting for approximately 24.0% of global revenues. Large-scale power infrastructure upgrades and strong domestic production of amorphous metal ribbons for energy-efficient transformers support expansion.

To know how our report can help streamline your business, Speak to Analyst

India Metal Glass Market

The Indian market in 2025 was valued at USD 44.2 million. Rising electrification, rural grid expansion, and increasing focus on reducing transmission losses are accelerating the adoption of amorphous core transformers.

North America

North America remains a significant regional market with a valuation of USD 192.0 million in 2025. The region represents a stable and technology-driven market for metal glass. The U.S. leads regional adoption due to grid modernization programs and strict transformer efficiency standards. Utilities increasingly deploy amorphous core transformers to reduce no-load energy losses. Additionally, advanced aerospace, defense, and medical industries support demand for bulk metallic glass in high-performance components. Strong R&D capabilities and material science innovation enhance product development. Although growth remains moderate compared to the Asia Pacific, policy-driven energy efficiency initiatives and high-value industrial applications sustain demand. These factors collectively support consistent regional expansion, hence maintaining North America’s strategic position in the market.

U.S. Metal Glass Market

The U.S. market in 2025 was valued at USD 16.0 million, representing approximately 1.0% of regional revenues. In the U.S., growth is driven by grid modernization programs and federal energy-efficiency standards promoting the adoption of low-loss amorphous metal transformer cores.

Europe

Europe is projected to record modest growth in the market. The region reached a valuation of USD 176.0 million in 2025. The market in Europe is shaped by stringent energy efficiency regulations and decarbonization policies. Countries including Germany, France, and the UK are upgrading power grids to reduce transmission losses, encouraging the adoption of amorphous metal transformer cores. Additionally, advanced automotive and aerospace industries drive demand for high-performance structural components. Regional focus on sustainable manufacturing and low-carbon materials further supports gradual adoption.

Germany Metal Glass Market

Germany’s market reached around USD 52.8 million in 2025, representing approximately 6.6% of regional demand. Demand growth is fueled by stringent energy efficiency regulations and investment in sustainable, low-loss electrical distribution systems.

U.K. Metal Glass Market

The U.K. market in 2025 was valued at USD 23.8 million, accounting for roughly 3.0% of regional revenues.

Latin America, the Middle East, and Africa

Latin America represents an emerging market for metal glass, primarily driven by investments in power distribution infrastructure. Countries such as Brazil and Mexico are upgrading transmission networks to reduce energy losses and improve grid efficiency. Adoption of amorphous metal transformer cores is gradually increasing as awareness of energy savings grows. Industrial development and renewable energy installations further support incremental demand. The Middle East & Africa region is experiencing gradual growth in the market due to infrastructure modernization and expanding power networks. Countries such as Saudi Arabia and the UAE are investing in grid efficiency improvements and renewable energy integration, encouraging the adoption of low-loss transformer technologies. Industrial diversification initiatives also support niche applications in sensors and structural components. The Middle East & Africa market reached USD 16.0 million in 2025.

GCC Metal Glass Market

The GCC market accounted for around USD 8.1 million in 2025, representing approximately 1.0% of regional revenues. Growth is supported by rapid infrastructure development, smart grid deployment, and government-led initiatives to improve power transmission efficiency.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Expertise and Energy Efficiency Demand Strengthening Market Concentration

The market is moderately concentrated, with competition led by specialized manufacturers possessing advanced rapid solidification and alloy processing capabilities. Leading players focus on amorphous metal ribbons for transformer cores, where performance reliability and magnetic efficiency are critical differentiators. Technological know-how, patent portfolios, and long-term supply agreements with transformer manufacturers provide competitive advantages. Bulk metallic glass producers compete in niche, high-value applications such as aerospace, medical devices, and precision engineering. High capital investment requirements and complex production processes create significant entry barriers.

LIST OF KEY METAL GLASS COMPANIES PROFILED

- Proterial, Ltd. (Japan)

- Qingdao Yunlu Advanced Materials Technology Co., Ltd. (China)

- Zhejiang Zhaojing Electrical Technology Co., Ltd. (China)

- VACUUMSCHMELZE GmbH & Co. KG (VAC) (Germany)

- Metglas, Inc. (U.S.)

- Eutectix, LLC (U.S.)

- Orbray Co., Ltd. (Japan)

- RUBY MICA COMPANY LIMITED (India)

- Heraeus Group (Germany)

- Liquidmetal Technologies, Inc. (U.S.)

REPORT COVERAGE

The global market report provides detailed analysis of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.0% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 800.0 million in 2025 and is projected to reach USD 1,367.6 million by 2034.

Recording a CAGR of 6.0%, the market is slated to exhibit steady growth during the forecast period.

By application, the transformer cores segment is leading the market.

Asia Pacific held the highest market share in 2025.

Superior magnetic properties and mechanical strength are the key factors driving the market growth.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us