Transformer Market Size, Share & Industry Analysis, By Type (Power Transformer, Distribution Transformer, Isolation Transformer, Instrument Transformer) By Phase (Single Phase Transformer, Three Phase Transformer), By Application (Industrial, Commercial, and Utility) Regional Forecast, 2026-2034

Transformer Market Size & Share Analysis

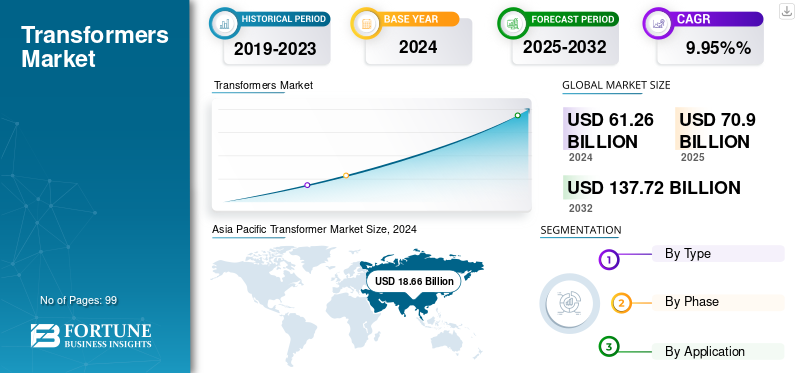

The global transformer market size was valued at USD 70.9 billion in 2025 and is projected to grow from USD 80.8 billion in 2026 to USD 158.47 billion by 2034, at an 8.78% CAGR during the forecast period. Asia Pacific dominated the global transformer market, accounting for 30.43% of the market share in 2025. Industry growth is driven by grid modernization, renewable energy integration, electrification expansion, transmission infrastructure upgrades, and growth in industrial power demand across global electricity networks.

The global transformer market represents a foundational component of electricity transmission and distribution infrastructure. Transformers enable efficient voltage conversion across power networks, supporting large-scale electricity transport from generation sources to end-use consumption points. As electricity demand expands and energy systems transition toward cleaner generation sources, the transformer market is experiencing sustained structural demand.

The transformer market size is strongly influenced by grid modernization initiatives, renewable energy integration, urban electrification, and industrial infrastructure development. Governments and utilities are investing heavily in upgrading aging transmission and distribution networks to improve reliability, energy efficiency, and grid resilience. These investments are driving long-term procurement of power and distribution transformers.

Large-scale renewable projects require high-capacity transformers capable of handling fluctuating loads from wind and solar installations. At the same time, growing electricity consumption in urban centers increases demand for distribution transformers that support localized grid networks. Utilities remain the largest buyers within the transformer industry, though industrial and commercial sectors also contribute to market expansion. Manufacturing facilities, data centers, and transport infrastructure projects require reliable voltage management solutions to ensure operational stability.

Regional dynamics play a significant role in shaping the transformer market share. Asia-Pacific dominates global demand due to rapid power infrastructure development and expanding electricity networks. North America and Europe focus on replacing aging transmission assets and improving grid efficiency. Emerging economies in Latin America, the Middle East, and Africa are investing in new electricity infrastructure to support economic development.

As electricity systems become more complex and decentralized, transformer technologies are evolving to support higher efficiency, digital monitoring capabilities, and improved operational reliability. These developments are expected to sustain transformer market growth throughout the forecast period.

The transformer market is undergoing rapid growth as global electricity use increases, industrialization accelerates, and investments in power infrastructure expand. Countries are expanding and modernizing their transmission and distribution networks, resulting in a growing demand for transformers. Additionally, ongoing urbanization, smart city development, and the electrification of transportation are increasing electricity consumption, further fueling market growth. Governments and utilities are replacing aging grid assets with energy-efficient and smart transformers to reduce losses and enhance reliability.

Transformer market vendors are expanding their manufacturing facilities to meet growing global demand for electricity, grid modernization, and renewable integration. This expansion trend reflects the need for localized production, shorter lead times, and advanced manufacturing capabilities. In September 2025, Siemens Energy plans to expand its transformer manufacturing facility in Nuremberg, Germany, in anticipation of continued global demand for larger transformers needed for grid expansion. The company will invest approximately EURO 220m (USD 256.2m) in its expansion, creating 350 new jobs and enhancing production capabilities in Nuremberg.

Siemens, ABB, and GE dominate the transformer market because they combine decades of engineering experience with cutting-edge digital and sustainable technologies. Their global operations, strong brand trust, and alignment with energy transition goals position them as key suppliers in modernizing power grids, integrating renewable energy sources, and enhancing energy efficiency worldwide.

Download Free sample to learn more about this report.

Transformer Market Key Takeaways

- 2025 Market Size: USD 70.90 Billion

- 2026 Market Size: USD 80.80 Billion

- 2034 Forecast Market Size: USD 158.47 Billion

- CAGR: 8.78% from 2026–2034

- Asia Pacific dominated the transformer market with a 30.43% share in 2025.

- The distribution transformer segment is projected to account for a 46.15% share in 2026.

- The three-phase transformer segment is projected to hold a 76.80% share in 2026.

Asia Pacific

Asia Pacific generated USD 21.57 billion in 2025 and is projected to reach USD 24.70 billion in 2026.

North America

North America accounted for USD 19.44 billion in 2025 and is expected to reach USD 22.35 billion in 2026.

Europe

Europe reached USD 15.63 billion in 2025 and is projected to grow to USD 17.69 billion in 2026.

U.S.

The transformer market is projected to reach USD 19.01 billion in 2026.

Japan

The transformer market is projected to reach USD 2.55 billion in 2026.

Read More

MARKET DYNAMICS

Market Drivers

Growing Urbanization and Infrastructure Development to Propel Market Growth

One of the primary factors driving the global transformer market's growth is the rapid pace of urbanization and infrastructure development. The fast-growing population of cities, smart urban infrastructure development, and the development of commercial and residential projects are continuously increasing the need for reliable electricity. Governments and utilities are investing heavily in expanding and upgrading power transmission and distribution networks to meet growing energy needs, thereby driving the installation of power transformers and distribution transformers.

The transformer market is primarily driven by rising global electricity demand and expanding power infrastructure. Electricity consumption continues to increase across residential, commercial, and industrial sectors. As economies grow and urban populations expand, power networks must scale accordingly. Transformers remain essential for managing voltage levels throughout transmission and distribution systems.

Grid modernization initiatives are another major driver of transformer market growth. Many countries operate electricity infrastructure installed several decades ago. Aging grid components require replacement to improve reliability and energy efficiency. Utilities are therefore investing in modern transformer systems designed for improved performance and reduced power losses.

Renewable energy integration is reshaping power network architecture. Wind farms and solar plants often generate electricity far from consumption centers. Transformers enable efficient voltage conversion and long-distance transmission from renewable energy facilities to grid networks. Increasing renewable capacity, therefore, stimulates additional demand for high-capacity power transformers.

Electrification of transportation and industrial processes further strengthens transformer market demand. Electric vehicle charging infrastructure, railway electrification systems, and large industrial operations require advanced transformer installations to manage high electricity loads.

In September 2025, Hitachi Energy, the largest electrification company globally, announced an additional investment of USD 270 million (approximately USD 195 million) to expand its manufacturing facility for large power transformers in Montreal, Canada. This major investment builds upon a previously announced expansion in 2024, which will nearly triple the annual production capacity at the site, further enhancing Canada's reputation as a leading supplier of clean energy manufacturing to the world.

Market Restraints

High Initial Investment and Installation Costs to Restrict Market Expansion

A significant constraint on the transformer market is the high initial investment and installation costs, which can inhibit widespread adoption of transformers, particularly in underdeveloped regions. The costs of manufacturing a transformer, especially high-voltage or smart transformers, depend on expensive raw materials such as copper, aluminum, and electrical steel, as well as the need for considerable precision engineering and sophisticated manufacturing facilities. Similarly, the costs of installing transformer assets include logistics, highly skilled labor, testing, and site preparation expenses. The high upfront costs often extend the timeline for modernization projects and delay the replacement of aging assets for utilities and industries with limited budgets.

Despite favorable long-term demand conditions, the transformer market faces several structural constraints that influence procurement cycles and production capacity. One of the most significant challenges involves supply chain complexity. Transformer manufacturing requires specialized raw materials, including electrical steel, copper windings, and insulation materials. Price volatility in these materials can affect production costs and project budgets. Manufacturing lead times also present a constraint within the transformer industry. Large power transformers require extensive engineering design, manufacturing processes, and testing procedures before deployment. Lead times can extend for many months, which may delay infrastructure projects or grid expansion programs.

Logistical challenges further complicate transformer deployment. High-capacity transformers are extremely large and heavy, requiring specialized transportation and installation procedures. Infrastructure limitations and regulatory requirements can slow project implementation. Environmental regulations also influence transformer production. Manufacturers must comply with increasingly strict efficiency and insulation standards. Transitioning toward environmentally safer insulation fluids and improved energy efficiency designs may increase manufacturing costs.

Market Opportunities

Growing Adoption of Smart and Digital Transformers to Create Lucrative Growth Opportunities

The growing usage of smart and digital transformers is creating considerable new growth segments in the global transformer market. As power grids become increasingly complex and the electricity demand continues to rise, utilities and industries are transitioning to intelligent transformer platforms that enable them to monitor connections, automate operations, and perform predictive maintenance more easily and efficiently. Digital transformers incorporate IoT sensors, O&M communication modules, and analytics to enable continuous monitoring of the performance of connected elements, allowing operators to detect faults sooner and resulting in reduced downtime and improved energy efficiency.

In October 2024, Hammond Power Solutions introduced HPS Smart Transformers for medium- and low-voltage transformers. This innovative solution incorporates IIoT-enabled power monitors, enabling users to obtain critical data and proactively review and identify concerns before experiencing costly downtime events.

HPS Smart Transformers offer users unparalleled visibility into their electrical systems. By consistently monitoring key metrics and providing real-time analytics, users are better able to translate the data to identify early warning signs of equipment stress or failure. This proactive process is crucial for maintaining efficient operations while minimizing expensive downtime.

The transformer market presents substantial long-term opportunities as global energy systems undergo structural transformation. One of the most significant opportunities lies in renewable energy grid integration. Large-scale solar and wind power installations require extensive transmission infrastructure capable of delivering electricity from remote generation sites to population centers.

Developing economies offer additional growth potential for the transformer industry. Many countries across Asia, Africa, and Latin America continue to expand electricity access and build new power networks. These initiatives require large volumes of distribution transformers and supporting grid infrastructure.

Electrification initiatives create another opportunity for transformer market growth. Electric vehicles, high-speed rail networks, and industrial electrification projects require substantial upgrades to power distribution systems. Transformers are critical components enabling these infrastructure developments. Urbanization also drives demand for advanced transformer systems. Expanding metropolitan regions require resilient electricity distribution networks capable of supporting residential buildings, transportation infrastructure, and digital industries such as data centers.

Transformers Market Trends

Increased Integration of Renewable Energy Systems to Drive Market Growth

The increased integration of renewable energy systems such as solar, wind, and hydroelectric power is a significant contributor to the growth of the global transformer market. As countries accelerate their transition to clean and sustainable energy, the demand for efficient transformers that connect renewable energy sources to the power grid has increased significantly. Step-up transformers are needed to increase the voltage levels at generation sites for renewable generating facilities to transmit energy over long distances. Distribution transformers can accurately deliver the power generated at renewable generation sites to end users.

In August 2025, Hitachi Energy India Ltd. announced an investment of approximately USD 33.83 million (rupees 300 crore) to upgrade the manufacturing capability of high-performance insulation materials for transformers, aiming to meet the growing demand.

In transformer applications, high-quality insulation material serves as the primary defense against electrical flow, protecting against internal short circuits. Hitachi Energy India’s investment guarantees support the country's and the world's energy transition goals. These transformers will tackle the technical challenges of integrating renewable power.

Several structural trends are reshaping the transformer market as electricity networks evolve toward greater digitalization, efficiency, and renewable integration. One of the most significant transformer market trends involves the deployment of smart transformers equipped with monitoring sensors and digital control systems. These technologies allow utilities to track load conditions, detect faults, and optimize grid performance.

Digital transformer technologies enable predictive maintenance by monitoring operational parameters such as temperature, load cycles, and insulation performance. Utilities increasingly adopt these solutions to reduce outages and improve asset management strategies. Renewable energy expansion also influences transformer design requirements. Variable generation from wind and solar installations creates fluctuating power flows across electricity networks. Transformers must therefore accommodate dynamic voltage conditions while maintaining grid stability.

Another emerging trend is the growing use of environmentally friendly insulation fluids. Traditional mineral oil insulation systems are gradually being replaced by biodegradable or synthetic alternatives. These materials reduce environmental risks and improve fire safety in urban transformer installations.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Fluctuating Raw Material Prices to Hamper Market Growth

Price fluctuations of significant raw materials, such as copper, aluminum, and electrical steel, are a key challenge to the global transformer market. Copper and aluminum are used in windings, and electrical steel is critical for magnetic cores. Changes in prices for these materials affect the costs of transformer manufacturers in producing the product, the price of transformers, and ultimately their profitability. Global influences, such as supply chain disruptions, geopolitical conflicts, trade restrictions, and variability in demand for industrial sectors, can all lead to unpredictable material costs.

Transformers Market Segmentation Analysis

By Type

Growing Urbanization and Industrial Development Lead to Distribution Transformers’ Growth

Based on type, the market is classified into power transformers, distribution transformers, isolation transformers, and instrument transformers.

Distribution Transformer

The distribution transformer led the segment in the market with a share of 46.15% in 2026. The growing trend of urbanization, coupled with industrial development and population growth, is contributing to a rise in global electricity consumption. To deliver electricity efficiently, utilities are also building local grids; each new substation or neighborhood network will require distribution transformers to reduce the voltage for end-users.

Distribution transformers form the backbone of electricity distribution systems and represent the largest volume segment of the transformer market. These transformers operate at lower voltage levels than power transformers and deliver electricity directly to residential, commercial, and industrial users. Distribution transformers are typically installed on utility poles, within ground-mounted substations, or inside industrial facilities. Their role is to step down voltage levels from regional transmission networks to safe levels suitable for end-use electricity consumption.

The distribution transformer segment is heavily influenced by urbanization and infrastructure expansion. Rapid urban development in emerging economies requires extensive distribution networks capable of supplying electricity to new residential communities, commercial complexes, and industrial zones.

Key factors supporting the distribution transformer market growth include:

- Expansion of urban electricity networks

- Electrification programs in developing countries

- Infrastructure upgrades in aging power distribution systems

- Rising electricity demand from residential and commercial sectors

Smart grid technologies are also transforming distribution transformer systems. Utilities increasingly deploy smart transformers equipped with digital monitoring systems that provide real-time operational data. These technologies help utilities optimize electricity distribution, detect faults quickly, and improve grid reliability.

Another major development in this segment is the shift toward energy-efficient transformer designs. Regulatory agencies in many countries require utilities to install transformers that minimize energy losses during voltage conversion. Due to the large number of installations required across electricity distribution networks, distribution transformers contribute a substantial share of overall transformer market revenue and represent the largest installed base of transformer equipment globally.

Power Transformer

The power transformer segment is the second-dominant segment in the market. The power transformer segment is growing due to the rapid expansion and modernization of high-voltage, high-capacity transmission system infrastructure, accelerating electricity demand, and the integration and rollout of large-scale renewable energy projects.

Power transformers represent the highest-capacity equipment segment within the transformer market and play a critical role in long-distance electricity transmission networks. These transformers operate primarily in high-voltage transmission systems that transport electricity from power generation facilities to regional substations. As electricity generation becomes more geographically distributed due to renewable energy development, power transformers have become increasingly essential for maintaining grid stability and transmission efficiency.

Large-scale power transformers are commonly deployed in transmission substations, renewable energy interconnection points, and high-capacity industrial installations. Their primary function is to step up voltage levels for efficient long-distance transmission or step down voltage before electricity enters regional distribution networks.

Several structural drivers support a strong demand for power transformers:

- Expansion of high-voltage transmission infrastructure

- Integration of large renewable generation facilities

- Cross-border electricity interconnection projects

- Grid reliability and capacity upgrades

Renewable energy expansion is particularly influential in this segment. Wind farms and solar installations often generate electricity far from consumption centers, requiring high-capacity transformers capable of handling fluctuating load conditions and large power flows. Technological innovation also influences power transformer development. Manufacturers are introducing designs with improved insulation systems, lower energy losses, and advanced monitoring capabilities. Digital sensors and predictive maintenance technologies are increasingly integrated into high-voltage transformers to improve operational reliability.

Because these transformers are expensive and engineered to highly specific grid requirements, they contribute significantly to the transformer market size even though production volumes are relatively limited. Utilities remain the dominant purchasers of power transformers worldwide. As national electricity networks expand and renewable generation capacity grows, the power transformer segment will continue to represent a major contributor to overall transformer market growth.

Isolation Transformer

Isolation transformers serve specialized applications where electrical isolation between circuits is required for safety, noise reduction, or system protection. These transformers separate electrical circuits while allowing power transfer through electromagnetic induction. Isolation transformers are widely used in industrial systems, healthcare equipment, sensitive electronics, and laboratory environments. They prevent electrical disturbances, voltage spikes, and ground loops from affecting connected devices.

Several industries rely heavily on isolation transformer systems:

- Medical facilities using sensitive diagnostic equipment

- Industrial automation systems requiring electrical noise protection

- Data centers and telecommunications infrastructure

- Manufacturing facilities operating precision electronic machinery

The increasing complexity of industrial equipment and digital infrastructure supports demand for isolation transformers. Data centers, semiconductor manufacturing plants, and advanced automation systems require stable and interference-free power supply systems. Healthcare infrastructure expansion also contributes to market demand. Hospitals and medical laboratories deploy isolation transformers to protect critical medical devices from electrical disturbances that could compromise operational reliability.

Technological improvements in insulation materials and electromagnetic shielding are improving the performance of isolation transformers. These advancements enhance safety standards while supporting sensitive electronic systems. Although isolation transformers represent a smaller portion of the total transformer market size compared with distribution transformers, they remain strategically important within specialized industrial and medical applications.

Instrument Transformer

Instrument transformers are designed to measure and monitor electrical parameters within power systems. These transformers convert high voltage or current levels into lower values that can be safely measured by meters and protective relay systems. Instrument transformers enable accurate monitoring of electrical networks, ensuring safe and efficient system operation. They are widely used in substations, power plants, industrial facilities, and electricity distribution networks.

The growth of modern grid monitoring systems strongly influences the demand for instrument transformers. Utilities increasingly rely on real-time monitoring technologies to maintain grid stability and detect operational anomalies.

Several structural drivers support instrument transformer demand:

- Expansion of high-voltage transmission infrastructure

- Increasing grid monitoring requirements

- Deployment of smart substations and automated power systems

- Integration of digital protective relay systems

- As electricity networks become more complex, utilities require advanced monitoring capabilities to maintain reliability. Instrument transformers, therefore, remain essential components of modern power infrastructure.

By Phase

Higher Efficiency, Lower Losses, and Increased Power Capabilities Lead to Three-Phase Transformers Segmental Growth

In terms of phase, the market is categorized into single-phase transformers and three-phase transformers.

Three-Phase Transformer

The three-phase transformer segment dominates the transformer market with a share of 76.80% in 2026, due to its higher efficiency, lower losses, and increased power capabilities, making it suitable for industrial, commercial, and utility-scale power distribution and transmission applications.

Three-phase transformers represent the dominant configuration within large-scale electricity infrastructure and industrial power systems. These transformers are capable of handling higher power loads and are therefore widely used in commercial, industrial, and utility applications. Three-phase transformers support high-efficiency power transmission and distribution. Industrial facilities, commercial complexes, and large infrastructure projects require these systems to maintain a stable electricity supply.

Three-phase transformers are commonly installed in substations, manufacturing plants, large buildings, and transport infrastructure systems. The rapid expansion of industrial infrastructure across emerging economies is significantly increasing demand for three-phase transformer installations. Because of their high power handling capacity and widespread use in industrial and utility networks, three-phase transformers account for a substantial share of transformer market revenue.

Single-Phase Transformer

The single-phase transformer is the dominant segment in the market. The single-phase transformer segment holds a significant market share, particularly in parts of the transformer market that supply electrical power to residential, rural, and light commercial buildings, as it offers a low-cost, simple, and reliable option for low-load conditions.

Single-phase transformers are commonly used in low-power electrical systems and residential distribution networks. These transformers support localized electricity distribution, particularly in rural areas and small-scale commercial applications. Single-phase systems are typically deployed where electricity demand remains relatively modest. Residential buildings, small retail outlets, and agricultural operations often rely on single-phase transformer installations.

Developing economies remain major adopters of single-phase transformers due to ongoing rural electrification programs. Governments in many regions continue investing in electricity access initiatives that extend grid infrastructure to remote communities. Although these transformers handle smaller power loads compared with three-phase systems, their widespread installation contributes significantly to overall transformer market volume. Technological improvements in energy efficiency and compact transformer designs are further supporting this segment.

By Application

Power Generation, Transmission, and Distribution Fuels Utility Segment’s Growth

In terms of application, the market is categorized into industrial, commercial, and utility.

Utility

The utility segment dominates the transformer market in 2026 with a share of 50.34%. The utility segment dominates the transformer market because utilities are responsible for power generation, transmission, and distribution, which require transformers at every voltage level to deliver electricity safely and efficiently.

Utility applications represent the largest segment within the transformer market. Electric utilities operate large transmission and distribution networks that require extensive transformer infrastructure. Utility transformers support voltage regulation across entire electricity grids, enabling efficient transmission of electricity from generation sources to end users. Utilities remain the largest buyers within the transformer industry and play a central role in shaping global transformer market growth.

Industrial

The industrial transformer segment is growing as global industries expand, electrify, and modernize, creating strong demand for efficient, high-performance transformers to ensure a stable, sustainable, and uninterrupted power supply in industrial operations. Industrial applications represent a major share of the transformer market due to the electricity-intensive nature of manufacturing operations. Industrial facilities require reliable voltage control systems to support heavy machinery, automated production lines, and high-energy equipment.

Industries such as steel production, chemical manufacturing, oil refining, and semiconductor fabrication depend on a stable electricity supply to maintain operational efficiency. Transformers deployed in industrial environments must meet strict reliability and durability standards. Equipment failures can disrupt production operations and cause significant economic losses.

Advanced monitoring technologies are increasingly integrated into industrial transformer systems to improve operational safety and maintenance planning.

Commercial

Commercial infrastructure, such as office buildings, shopping centers, hospitals, and transportation hubs, requires extensive transformer installations to manage electricity distribution across complex building systems. Commercial electricity consumption continues to increase due to expanding urban populations and the rapid growth of digital infrastructure such as data centers. Commercial transformers must accommodate fluctuating electricity loads while maintaining a stable power supply across large building complexes.

To know how our report can help streamline your business, Speak to Analyst

Regional Insights

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia-Pacific Transformer Market Analysis

Asia Pacific Transformer Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific generated USD 21.57 Billion, contributing 30.43% to global market revenue, and is projected to grow to USD 24.7 Billion in 2026. In the Asia Pacific, the transformer market is experiencing rapid growth due to surging electricity demand, industrial expansion, and the integration of large-scale renewable energy across emerging economies. In 2025, the Chinese market is estimated to reach USD 4.83 billion. The Chinese transformer market is growing as the nation modernizes its vast power grid, integrates renewable energy on a large scale, and industrializes rapidly, while also embracing smart and energy-efficient transformer technologies to support its long-term carbon and energy reduction goals.

Asia-Pacific dominates the global transformer market due to rapid electricity infrastructure expansion and industrial growth. Large-scale urbanization and increasing electricity demand require extensive transmission and distribution networks. Governments across the region are investing heavily in power infrastructure development. These initiatives support strong transformer market growth while strengthening Asia-Pacific’s leading transformer market share globally.

For instance, in May 2025, Hitachi Energy supplied rectifier transformers for a significant green hydrogen project in Songyuan, Northeast China. This project is one of the largest integrated hydrogen-ammonia-methanol projects globally, built by China Energy Engineering Corporation (CEEC). The project envisions replacing fossil fuels with hydrogen across the Chinese industry, while accelerating the production of clean ammonia and methanol.

The Japan market is projected to reach USD 2.55 billion by 2026, the China market is projected to reach USD 6.39 billion by 2026, and the India market is projected to reach USD 5.17 billion by 2026.

Japan Transformer Market

Japan’s transformer market focuses on grid reliability, energy efficiency, and advanced power management technologies. Following electricity infrastructure modernization initiatives, utilities are upgrading transformer installations to support renewable energy integration and smart grid development. Industrial electricity demand also contributes to the steady procurement of transformer equipment. These factors sustain Japan’s position within the global transformer market.

China Transformer Market

China represents the largest contributor to the global transformer market size due to extensive power infrastructure expansion. Rapid urbanization, industrial development, and renewable energy installations require significant transformer deployment. Government investment in ultra-high-voltage transmission networks is further accelerating demand. These initiatives continue to strengthen China’s transformer market share and reinforce its leadership in global electricity infrastructure development.

North America Transformer Market Analysis

Other regions, such as North America, are expected to experience notable growth in the coming years. During the forecast period, The North America region captured 27.41% of the global market in 2025, generating USD 19.44 Billion in revenue, and is projected to reach USD 22.35 Billion in 2026. The U.S. and Canada transformer market is growing due to grid modernization, renewable energy expansion, and the replacement of aging infrastructure across North America. Backed by these factors, countries such as the U.S. are expected to reach a valuation of USD 14.21 billion in 2024, and Canada is expected to reach USD 16.47 billion in 2025.

North America represents a mature yet strategically important transformer market driven by grid modernization and infrastructure replacement programs. Aging transmission networks across the United States and Canada require extensive transformer upgrades to improve reliability and energy efficiency. Renewable energy integration and electrification initiatives are accelerating transformer procurement. These factors continue to support steady transformer market growth across the region’s power infrastructure.

United States Transformer Market

The U.S. market is projected to reach USD 19.01 billion by 2026. The United States transformer market is largely driven by transmission infrastructure upgrades and renewable energy grid integration. Utilities are replacing aging transformer fleets installed decades ago to improve grid resilience and energy efficiency. The rapid expansion of electric vehicle charging networks and data center infrastructure is increasing electricity demand. These structural factors sustain strong transformer market growth across the country’s evolving electricity systems.

Europe Transformer Market Analysis

Europe maintained a strong presence in the global market, reaching USD 15.63 Billion in 2025, accounting for 22.05% share, and is expected to reach USD 17.69 Billion in 2026, securing its position as the third-largest region in the market. In the region, Germany is estimated to reach USD 3.42 billion in 2025. The European transformer market is growing steadily due to grid modernization, the integration of renewable energy, and increasing electrification across various industries and transportation sectors.

Europe’s transformer market is shaped by strong regulatory emphasis on energy efficiency and renewable energy expansion. Countries across the region are investing in transmission upgrades to integrate offshore wind projects and decentralized renewable generation. Grid modernization programs are also replacing aging electricity infrastructure. These developments are reinforcing transformer market growth while supporting Europe’s broader energy transition strategy.

The U.K. market is projected to reach USD 3.24 billion by 2026, while the Germany market is projected to reach USD 3.88 billion by 2026.

Germany Transformer Market

Germany plays a significant role within the European transformer market due to its ambitious renewable energy transition strategy. Large-scale wind and solar installations require upgraded transmission infrastructure capable of managing variable electricity flows. German utilities continue investing in grid expansion and modernization projects. These initiatives sustain demand for advanced transformer technologies and strengthen the country’s transformer market position.

United Kingdom Transformer Market

The United Kingdom transformer market is influenced by offshore wind expansion and electricity grid reinforcement programs. As renewable generation capacity increases, utilities must upgrade transmission infrastructure to support higher electricity flows. Investment in smart grid technologies is also accelerating transformer deployment. These developments contribute to steady transformer market growth within the United Kingdom’s evolving energy system.

Latin America Transformer Market Analysis

Over the forecast period, the Latin America and Middle East & Africa regions. The Latin America transformer market is expanding as the region develops and upgrades its power infrastructure to accommodate increasing electricity needs, integrate renewable energy, sustain industrialization, and electrify rural areas, supported by investments from both the government and private sectors. The Latin America market generated USD 3.13 Billion in 2025, representing 4.42% of the global market landscape, and is expected to reach USD 3.52 Billion in 2026.

Latin America’s transformer market is expanding as governments invest in electricity infrastructure modernization and renewable energy development. Countries across the region are strengthening transmission networks to support growing electricity demand and economic development. Industrial expansion and urbanization are increasing the need for reliable power distribution systems. These factors contribute to gradual transformer market growth.

Middle East & Africa Transformer Market Analysis

The Middle East and Africa transformer market is experiencing growth due to rising electricity demand, rapid urbanization, the expansion of renewable energy, and large-scale infrastructure development across the region. Middle East & Africa recorded a market size of USD 11.12 Billion in 2025, capturing 15.69% of the global market share, and is projected to reach USD 12.54 Billion in 2026.

The Middle East and Africa transformer market is supported by expanding electricity infrastructure and rising energy demand. Governments across the region are investing in grid expansion and renewable energy integration projects. Industrial development and urban population growth further increase electricity consumption. These factors are gradually strengthening transformer market growth across emerging power infrastructure networks.

Transformer Industry Competitive Landscape

Vendors Are Expanding Their Transformer Manufacturing Facilities To Support Power Infrastructure

Transformer market players are actively increasing their production capacities through facility expansions and technological upgrades. This strategy aims to ensure timely delivery, support the rising demand for energy-efficient and smart transformers, and strengthen regional economies amid the ongoing global energy transition.

The transformer market is characterized by a mix of large multinational electrical equipment manufacturers and specialized regional producers. Competition is primarily based on technological capabilities, manufacturing capacity, product reliability, and long-term service support. Transformer manufacturers operate within a highly technical environment where engineering expertise and compliance with international power standards are critical to market participation.

Large global companies dominate high-capacity transformer production, particularly in the power transformer segment. These manufacturers possess advanced engineering capabilities, extensive research and development infrastructure, and large-scale manufacturing facilities capable of producing high-voltage transformers for national electricity grids. Their global presence allows them to participate in major transmission infrastructure projects across multiple regions.

Regional manufacturers typically focus on distribution transformers and specialized industrial transformer applications. These companies compete through cost efficiency, localized supply chains, and faster delivery timelines. In many emerging economies, domestic transformer manufacturers benefit from government procurement policies that support local industrial production.

Technological innovation is increasingly shaping competitive positioning in the transformer industry. Manufacturers are developing advanced transformer systems with improved energy efficiency, digital monitoring capabilities, and environmentally sustainable insulation materials. Digital transformer technologies enable utilities to monitor operational parameters in real time, improving grid reliability and predictive maintenance.

Strategic partnerships are also becoming more common. Transformer manufacturers frequently collaborate with utility operators, grid infrastructure companies, and renewable energy developers. These collaborations support the deployment of advanced power infrastructure required for modern electricity systems.

In July 2024, Toshiba Transmission & Distribution Systems (India) Pvt. Ltd. is planning to expand its transformer manufacturing capacity. The company announced that it would increase manufacturing capacity by approximately 1.5 times from its level as of the end of FY 2023-24, over three years starting from the current FY, 2024-25. Toshiba Group has positioned its power T&D business as a focus business and will invest approximately JPY 10 billion (USD 63.5 million) in TTDI to expand its capacity.

Key competitive factors influencing transformer market share include:

- Manufacturing scale and production capacity

- Engineering expertise in high-voltage transformer systems

- Ability to deliver energy-efficient transformer designs

- Integration of digital monitoring technologies

LIST OF KEY TRANSFORMER COMPANIES PROFILED:

- Hitachi Energy Ltd (Switzerland)

- Siemens Energy (Germany)

- Eaton Corporation (U.S.)

- GE Vernova (U.S.)

- Toshiba Corporation (Japan)

- ABB Group (Switzerland)

- Schneider Electric (France)

- Fuji Electric (Japan)

- Mitsubishi Electric Corporation (Japan)

- CG Power and Industrial Solutions Ltd. (India)

- WEG S.A. (Brazil)

- Arteche Group (Spain)

- LS Electric Co., Ltd. (South Korea)

- Hubbell Incorporated (U.S.)

- Voltamp Transformers Ltd. (India)

Latest Transformer Industry Developments:

- March 2025: Hitachi Energy announced the expansion of transformer manufacturing capacity to address the rising global demand for grid infrastructure equipment. The initiative aims to support power transmission upgrades and renewable energy integration. The expansion incorporates advanced production automation and high-voltage transformer technologies designed for ultra-high-voltage electricity networks.

- January 2025: Siemens Energy introduced a new generation of digitally monitored power transformers designed to improve grid reliability and predictive maintenance capabilities. The strategic objective is to support smart grid modernization programs. The transformers integrate advanced sensors, digital diagnostics systems, and real-time performance monitoring technologies.

- October 2024: ABB launched an energy-efficient distribution transformer platform designed to reduce electricity losses in urban power networks. The development focuses on improving transformer efficiency and supporting sustainability objectives within the electricity infrastructure. The system utilizes advanced insulation materials and optimized core design technologies.

- July 2024: Toshiba Energy Systems & Solutions began construction of a new transformer manufacturing facility to increase production capacity for high-voltage power transformers. The strategic goal is to support expanding transmission infrastructure projects worldwide. The facility integrates advanced testing laboratories and automated manufacturing technologies.

- April 2024: Schneider Electric introduced a new line of eco-efficient transformers using environmentally friendly insulation fluids. The initiative supports regulatory requirements related to energy efficiency and environmental safety. These transformers incorporate biodegradable insulation technologies and advanced thermal management systems designed for modern grid infrastructure.

REPORT COVERAGE

The global transformer market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.78% from 2026-2034 |

| Unit | Value (USD Billion) |

| By Type |

|

| By Phase |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 80.8 billion in 2026 and is projected to reach USD 158.47 billion by 2034.

In 2025, the market value stood at USD 21.57 billion.

The market is expected to exhibit a CAGR of 8.78% during the forecast period (2026-2034).

The utility segment led the market in terms of application.

Growing urbanization and infrastructure development to propel market growth.

Hitachi, Siemens, ABB, and other companies are among the prominent players in the market.

Asia Pacific dominated the market and had the highest share in 2024.

Integration with renewable energy systems to drive market growth.

- 2021-2034

- 2025

- 2021-2024

- 99

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us