Metalized Flexible Packaging Market Size, Share & Industry Analysis, By Material (Plastic, Paper, and Aluminum Foil), By Product Type (Pouches, Bags & Sacks, Wraps & Films, Labels, and Others), By Metallization Technology (Vacuum Metallization, Sputter Coating, Evaporation Metallization, and Others), By End-use Industry (Food & Beverage , Pharmaceuticals , Cosmetics & Personal Care, Electronics & Electricals, Agriculture & Pet Food, and Other), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

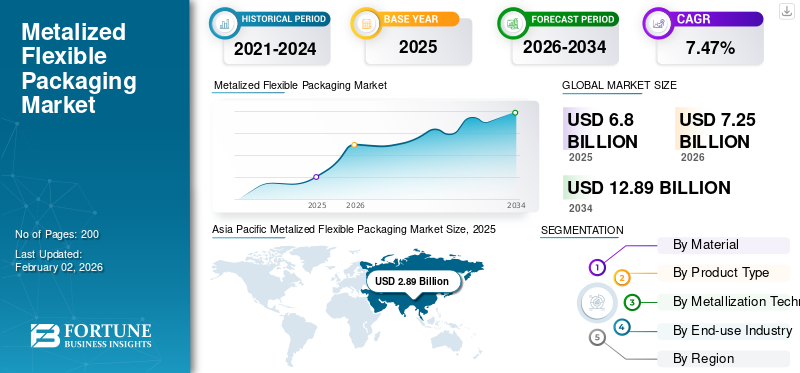

The global metalized flexible packaging market size was valued at USD 6.80 billion in 2025. The market is projected to grow from USD 7.25 billion in 2026 to USD 12.89 billion by 2034, exhibiting a CAGR of 7.47% during the forecast period. Asia Pacific dominated the metalized flexible packaging market with a market share of 42.43% in 2025.

Metalized flexible packaging refers to high-tech packaging materials created by coating flexible films, such as plastic or paper, with a thin metallic layer, usually aluminum. This coating improves resistance to moisture, oxygen, light, and impurities. These materials serve many purposes in modern packaging, including food and drinks, medicines, personal care items, and industrial goods. They extend shelf life, maintain product quality, and provide excellent printability for branding. The market for metalized flexible packaging is growing rapidly due to the increasing demand for lightweight, sustainable, and affordable packaging options. There is also a rise in usage within e-commerce and convenience food sectors. Furthermore, the push toward recyclable and eco-friendly barrier films is sparking innovation and driving market growth.

Furthermore, the market encompasses several major players, with companies such as Amcor Plc, Sealed Air Corporation, Mondi Group, Sonoco Products Company, and Huhtamaki at the forefront. A broad product portfolio, continuous innovation in film technologies, and strong regional expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Sustainable and High-Barrier Packaging to Propel Market Growth

The main factor driving the market is the growing demand for packaging solutions that combine sustainability with strong barrier performance. Metalized flexible packaging offers excellent protection against moisture, oxygen, and light. This protection is crucial for extending shelf life and maintaining quality in food, beverages, pharmaceuticals, and personal care products. At the same time, manufacturers are creating recyclable and lightweight metalized films that reduce material use and carbon emissions, aligning with global sustainability goals and regulations.

Furthermore, the rapid increase in convenience food consumption, along with the growth of e-commerce and ready-to-sell packaging formats, is boosting demand.

- For instance, Amcor introduced a recyclable metalized film solution in 2024. This solution maintains its high barrier properties while supporting circular economy goals, demonstrating the industry's shift toward sustainable and effective packaging.

MARKET RESTRAINTS

Challenges in Recycling and Material Recovery to Restrict Market Expansion

A major limitation for the market is the difficulty of recycling and recovering materials due to the multi-layer design of metalized films. These laminates often combine plastic substrates, such as PET or BOPP, with a thin aluminum layer. This makes separating the layers for recycling technically difficult and costly. As a result, a large amount of metalized flexible packaging ends up in landfills or gets incinerated. This situation raises concerns among regulators and consumers demands about environmental sustainability.

- For instance, according to the U.S. Environmental Protection Agency (EPA), only about 8.7% of all plastic packaging waste was recycled in the U.S. in 2021, with flexible laminates and multi-material films being among the least recovered categories. Similarly, the European Commission reported in 2023 that nearly 60% of flexible plastic packaging in Europe was not effectively recycled, largely due to material complexity. These limitations slow down the adoption of metalized flexible packaging in regions with strict sustainability targets, thereby restraining overall metalized flexible packaging market growth.

MARKET OPPORTUNITIES

Development of Recyclable and Mono-Material Metalized Films to Create Growth Opportunities

Recyclable and mono-material metalized packaging solutions designed for specific needs have become more popular in recent years. These improvements address the challenge of multi-layer recycling while maintaining strong barrier performance. They also help meet circular economy goals and upcoming regulatory standards. This trend is expected to create significant opportunities for packaging producers. International brands are committing to ambitious sustainability targets and are seeking eco-friendly packaging solutions.

- For instance, the Ellen MacArthur Foundation reported that over 500 companies and organizations, representing more than 20% of global plastic packaging volumes, have signed the New Plastics Economy Global Commitment, pledging to make all plastic packaging reusable, recyclable, or compostable by 2025. This push is creating strong demand for recyclable metalized films, positioning manufacturers that innovate in this area to capture future growth.

METALIZED FLEXIBLE PACKAGING MARKET TRENDS

Shift toward Digital Printing and Premium Aesthetics is one of the Significant Market Trends

In recent years, brand owners have been using metalized flexible packaging more to improve product visibility on shelves and help with personalization efforts. The shift to digital printing on metalized films enables high-resolution imagery, shorter production runs, and faster time-to-market. This appeals to brands in food, beverage, and personal care. This change is mainly driven by rising consumer interest in visually appealing, high-quality packaging, and the growth of e-commerce, where packaging serves as a branding tool.

- For instance, according to Smithers’ analysis of packaging printing (based on industry association data), digital printing in packaging grew at over 10% annually between 2017 and 2022, with flexible packaging being one of the fastest-growing segments due to its adaptability and branding potential. This growing adoption of digital printing is reshaping the value proposition of metalized flexible packaging.

Download Free sample to learn more about this report.

MARKET CHALLENGES

High Production and Material Costs to Hamper Market Growth

A key barrier to market growth is that metalized flexible packaging has relatively high production and raw material costs. Production techniques require vacuum metallization, specialized coatings, and multi-layered film constructions which are more expensive than traditional flexible packaging material. With the variation in aluminum prices, metalized flexible packaging has a cost structure that can lack price stability. This can create problems for manufacturers that want to be price competitive in cost-sensitive markets such as emerging economies. Slower adoption often occurs with most small to mid-sized brand owners who have limited packaging budgets.

- For instance, according to the London Metal Exchange (LME), aluminum prices averaged around USD 2,400 per metric ton in 2023, a nearly 20% increase compared to 2020 levels, driving up the cost of producing metalized films. Such volatility in raw material pricing continues to pose a challenge for sustained market growth.

Segmentation Analysis

By Material

High Demand for Metalized Flexible Plastic Packaging Contributed to Segmental Growth

On the basis of the segmentation of material, the market is classified into plastic, paper, and aluminum foil.

The plastic segment is expected to account for 59.21% of the market in 2026. This is due to strong consumer demand within food, beverages, and personal care applications due to their excellent barrier properties, lightweight, and low-cost. Furthermore, the ability to easily seal, mold, and print plastic films has also increased their use within the fast-moving consumer goods segment.

- For example, Amcor plc and Sealed Air Corporation are leading players which support innovative plastic-based metallized packaging solutions for global brand owners.

To know how our report can help streamline your business, Speak to Analyst

By Product Type

Rising Demand for Convenience Drives Growth of Pouches Segment

In terms of product type, the market is categorized into pouches, bags & sacks, wraps & films, labels, and others.

The pouches segment is anticipated to hold a dominant market share of 46.51% in 2026. In 2025, the segment is anticipated to dominate with over 45.9% share. Metalized flexible pouches are widely used across food, beverage, and personal care sectors due to their lightweight nature, superior barrier protection, and portability. The surge in single-serve packs, on-the-go consumption, and growing penetration of e-commerce channels are key factors boosting this segment’s growth.

- For instance, in June 2024, Amcor launched recyclable metalized pouches tailored for snacks and confectionery, enhancing both shelf life and sustainability.

Pouches segment is expected to grow at a CAGR of 7.42% over the forecast period.

By Metallization Technology

Widespread Adoption of Vacuum Metallization Process Strengthens Segment Growth

Based on metallization technology, the market is segmented into vacuum metallization, sputter coating, evaporation metallization, and others.

In 2026, the vacuum metallization segment is projected to lead the market with a 53.28% share. By metallization technology, the vacuum metallization segment accounted for 52.41% share in 2024. Its dominance is attributed to advantages such as cost-effectiveness, high production efficiency, excellent barrier protection against oxygen and moisture, and broad applicability across food, beverage, and pharmaceutical packaging. The increasing preference for lightweight packaging with extended shelf life further supplements demand for vacuum metallized films, driving the segment’s growth.

- For instance, Uflex Ltd. and Mondi Group are among the key players providing vacuum metallized flexible packaging solutions, catering to a wide range of FMCG and industrial applications.

By End User

Widespread Usage in Packaged Foods and Ready-to-Eat Products Supplemented Segment Growth

Based on end-use industry, the market is segmented into food & beverage, pharmaceuticals, cosmetics & personal care, electronics & electricals, agriculture & pet food, and others.

In 2024, the global market was dominated by the food & beverage segment in terms of end-use. The strong adoption of metalized flexible packaging for extending shelf life, improving product visibility, and ensuring barrier protection against moisture, oxygen, and light has supported the dominance of this segment. Furthermore, the segment is set to hold over 53.14% share in 2026 owing to rising demand for packaged products and convenience foods.

- For instance, Mondelez International and Nestlé have widely adopted metalized flexible pouches and wraps for chocolates, confectionery, and snack packaging, owing to their superior barrier properties and lightweight structure.

In addition, pharmaceuticals end users are projected to grow at a CAGR of 6.02% during the study period, driven by the rising need for unit-dose packaging, lidding films, and improved medicine protection.

Metalized Flexible Packaging Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Metalized Flexible Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for USD 2.89 billion in 2025, representing 42.43% of the global market share, and is projected to reach USD 3.12 billion in 2026. Factors driving the region’s dominance include rapid urbanization and population growth resulting in higher consumption of packaged food and beverages. Other factors include strong manufacturing hubs for flexible films and laminates and growing investment from international and regional companies in sustainable packaging innovations. In 2026, the China market is estimated to reach USD 1.33 billion.

- For instance, in March 2024, Amcor opened its Asia-Pacific Innovation Center in Jiangyin, China, focusing on sustainable flexible and metalized packaging solutions to cater to the fast-growing regional demand from food, beverage, and personal care industries.

Europe and North America

Other regions such as Europe and North America are anticipated to witness notable growth in the coming years. The North America market generated USD 1.66 billion in 2025, representing 24.45% of the global market landscape, and is expected to reach USD 1.76 billion in 2026. This is primarily due to strong research and innovation capabilities, rising sustainability regulations, and high demand for premium packaging solutions across food, beverage, and pharmaceutical industries. Backed by these factors, countries including India anticipate to record the valuation of USD 0.63 billion, Japan to record USD 0.46 billion in 2026, and Southeast Asia to record USD 0.31 billion in 2025. The U.S. market for metalized flexible packaging is expanding vigorously due to the higher demand for lighter, durable, and attractive packaging in food, beverage, and personal care applications. The increasing consumer preference for sustainable and recyclable packaging is encouraging manufacturers to develop eco-friendly metalized films. In addition, the growing e-commerce and ready-to-eat food markets provide an ongoing demand for high-barrier, shelf-stable packaging.

After North America, Europe contributed 20.07% to the global market in 2025, with a valuation of USD 1.37 billion, and is projected to reach USD 1.45 billion in 2026. In the region, Germany and France both are estimated to reach USD 0.37 billion in 2026 and USD 0.20 billion in 2025.

Latin America and Middle East & Africa

Over the forecast period, Latin America and the Middle East & Africa regions would witness a moderate growth in this marketspace. Latin America contributed approximately USD 0.5 billion to the global market in 2025, accounting for 7.40% share, and is expected to reach USD 0.52 billion in 2026. Driven by the expanding food & beverage sector, rising demand for cost-effective packaging, and increasing adoption of sustainable flexible packaging solutions in the region.

In 2025, Middle East & Africa held 5.65% of the global market, reaching a valuation of USD 0.38 billion, and is projected to grow to USD 0.4 billion in 2026. In the Middle East & Africa, Saudi Arabia is set to attain the value of USD 0.38 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings and Strong Distribution Network of Key Companies Supported Leading Position

The global market shows a semi-concentrated structure with numerous small-to-mid-size companies actively operating across the globe. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Amcor plc, Mondi Group, and Huhtamäki Oyj are some of the dominating players in the market. A comprehensive portfolio of metalized films and laminates, global presence through extensive manufacturing and distribution networks, and continuous investment in sustainable flexible packaging innovations are few characteristics of these players which support their dominance.

Apart from this, other prominent players in the market include UFlex Ltd., Constantia Flexibles, Sonoco Products Company, Berry Global Inc., Sealed Air Corporation, and ProAmpac LLC. These companies are undertaking various strategic initiatives such as mergers & acquisitions, capacity expansions, and development of recyclable metalized packaging structures to enhance their market presence and cater to rising demand across food, pharmaceuticals, and personal care industries.

LIST OF KEY METALIZED FLEXIBLE PACKAGING COMPANIES PROFILED

- Amcor plc (Switzerland)

- Sealed Air Corporation (U.S.)

- Mondi Group (U.K.)

- Huhtamäki Oyj (Finland)

- Sonoco Products Company (U.S.)

- UFlex Ltd. (India)

- Constantia Flexibles (Austria)

- Berry Global Group, Inc. (U.S.)

- Coveris Holdings S.A. (Austria)

- Toray Plastics (America), Inc. (U.S.)

- Cosmo Films Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- April 2025: TOPPAN Holdings Inc. completed the acquisition of the Thermoformed & Flexibles Packaging (TFP) business from Sonoco Products Company. This deal enhances TOPPAN’s capabilities in flexible packaging including metalized flexible structures.

- April 2025: Mondi Plc acquired the Western European assets of Schumacher Packaging, enhancing its product portfolio, production capacity, and innovation capabilities to better serve customers seeking high-performance, sustainable metalized flexible packaging solutions at scale.

- February 2025: TIPA unveiled a global launch of an advanced home-compostable metallized high-barrier film (312MET Premium) for snack packaging. The film offers enhanced protection against salt, oil, and moisture in a biodegradable solution, and when paired with cellulose or paper layers, forms one of the thinnest 2-ply home compostable solutions globally.

- June 2024: Sonoco Products announced its acquisition of Eviosys for USD 3.9 billion. While Eviosys is more in metal cans/aerosol side, the acquisition signals Sonoco’s broader strategy to bolster its metal & related packaging businesses including overlapping flex/hybrid metal-related flexible packaging capabilities.

- April 2019: Amcor launched AmLite Ultra Recyclable, a new metalized flexible packaging solution in Europe designed for full recyclability, targeting the food and pharmaceutical sectors.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.47% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Product Type, Metallization Technology, End-use Industry, and Region |

|

By Material |

|

|

By Product Type |

|

|

By Metallization Technology |

|

|

By End-use Industry |

|

|

By Region |

o U.S. o Canada

o Germany o France o U.K. o Italy o Spain o Russia o Poland o Romania o Rest of Europe

o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific

o Brazil o Mexico o Rest of Latin America

o Saudi Arabia o UAE o Oman o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.25 billion in 2026 and is projected to reach USD 12.89 billion by 2034.

In 2025, the market value stood at USD 6.80 billion.

The market is expected to exhibit a CAGR of 7.47% during the forecast period.

The plastic segment led the market by material.

The key factors driving rising demand for sustainable and high-barrier packaging to propel market growth.

Amcor plc, Mondi Group, and Huhtamäki Oyj., are some of the prominent players in the market.

Asia Pacific dominated the metalized flexible packaging market with a market share of 42.43% in 2025.

Development of recyclable and mono-material metalized films to create growth opportunities.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us