Micro Server IC Market Size, Share & Industry Analysis, By Component (Hardware, Software), By Processor (Intel, Arm), By Application (Web Hosting & Enterprises, Analytics & Cloud Computing), and Regional Forecast, 2026–2034

Micro Server IC Market Overview

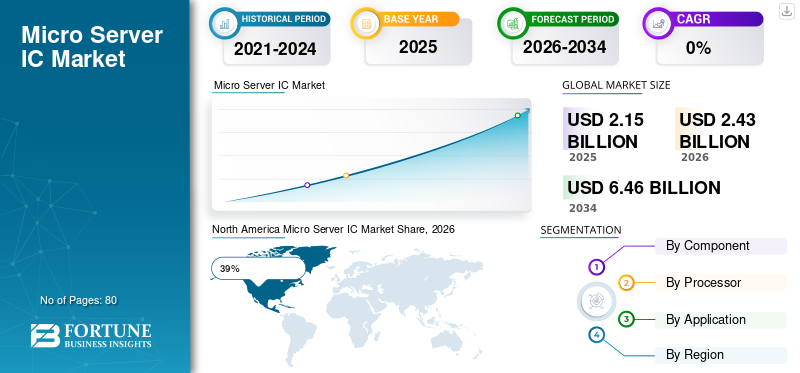

The global micro server IC market size was valued at USD 2.14 billion in 2025. The market is projected to grow from USD 2.42 billion in 2026 to USD 6.45 billion by 2034, exhibiting a CAGR of 13.00% during the forecast period.

The global micro server IC market is expanding steadily due to increasing demand for energy-efficient data center infrastructure, edge computing systems, and cloud-based server architectures. Micro server integrated circuits are widely used in compact server environments that require low power consumption, high-density processing, and scalable computing performance. The micro server IC market Report highlights rising adoption across hyperscale data centers, telecom infrastructure, enterprise cloud platforms, and AI-driven computing applications. Growing workloads associated with IoT devices, real-time analytics, and distributed computing are accelerating demand for advanced micro server processors and chipsets. Technological advancements in semiconductor design and server virtualization continue to strengthen micro server IC market growth globally.

The United States micro server IC market is witnessing strong expansion driven by rapid growth in cloud computing infrastructure, hyperscale data centers, and artificial intelligence applications. Major technology companies are investing heavily in advanced server processors and energy-efficient computing platforms to support increasing digital workloads. The Micro Server IC Industry Analysis indicates rising deployment of edge computing systems, enterprise storage servers, and AI-enabled cloud platforms throughout the United States. Demand for high-performance semiconductor solutions is also increasing across telecom networks and enterprise IT infrastructure. Expanding investments in next-generation semiconductor manufacturing and data center modernization continue to strengthen the long-term outlook of the USA micro server IC market.

Download Free sample to learn more about this report.

Key Takeaways

Market Size & Growth

- Global market size 2025: USD 2.14 billion

- Global market size 2034: USD 6.45 billion

- CAGR (2026–2034): 13.00%

Market Share – Regionals

- North America: 39%

- Europe: 25%

- Asia-Pacific: 29%

- Rest of World: 7%

Country-Level Shares

- Germany: 34% of Europe’s market

- United Kingdom: 22% of Europe’s market

- Japan: 25% of Asia-Pacific market

- China: 41% of Asia-Pacific market

Micro Server IC Market Latest Trends

The micro server IC market is evolving rapidly with increasing focus on energy efficiency, AI acceleration, and scalable edge computing infrastructure. One of the most significant micro server IC market trends is the growing adoption of ARM-based processors in hyperscale data centers due to their lower power consumption and improved workload efficiency. Cloud service providers are increasingly integrating micro server ICs optimized for AI inference, machine learning workloads, and real-time analytics applications. Another important trend in the micro server IC market Research Report is the rising deployment of edge computing systems designed to support low-latency data processing closer to end users.

Telecom operators and industrial automation providers are investing in compact server platforms powered by advanced micro server chipsets for IoT connectivity and 5G network expansion. The market is also witnessing increasing demand for heterogeneous computing architectures integrating CPUs, GPUs, and AI accelerators within server environments. Semiconductor manufacturers are focusing on advanced fabrication nodes, thermal optimization technologies, and high-bandwidth memory integration to improve server efficiency.

Download Free sample to learn more about this report.

Micro Server IC Market Dynamics

DRIVER

Rising Demand for Cloud Computing and Energy-Efficient Data Center Infrastructure.

The increasing expansion of cloud computing services and hyperscale data centers is a major factor driving micro server IC market growth worldwide. Enterprises are rapidly adopting cloud-based platforms, AI-driven analytics, and virtualized computing environments that require scalable and energy-efficient server architectures. Micro server integrated circuits provide lower power consumption, compact form factors, and improved workload optimization compared to conventional server processors. The micro server IC market Analysis highlights strong demand from telecom providers, enterprise IT infrastructure, and edge computing applications where high-density computing performance is essential. Increasing deployment of IoT devices and connected systems is also generating substantial demand for low-latency processing capabilities supported by micro server architectures. Semiconductor manufacturers are developing advanced processors with improved thermal efficiency, AI acceleration capabilities, and high-speed networking integration. Growing investments in 5G infrastructure and distributed cloud environments continue to strengthen long-term micro server IC market opportunities. \

RESTRAINT

High Semiconductor Development Costs and Supply Chain Complexity.

Despite strong market growth, the micro server IC market faces restraints associated with high semiconductor research and manufacturing costs. Developing advanced server processors requires significant investment in chip design, fabrication technologies, and performance optimization systems. Smaller semiconductor companies may struggle to compete with major industry players possessing large-scale manufacturing capabilities and advanced fabrication resources. The micro server IC market Research Report highlights supply chain challenges related to semiconductor wafer shortages, geopolitical trade restrictions, and dependency on advanced fabrication facilities. Fluctuations in raw material availability and packaging technologies can also affect production timelines and operational costs. Another restraint involves compatibility concerns between different server architectures and enterprise IT systems. Some organizations remain hesitant to transition from traditional server infrastructure due to integration complexity and software optimization requirements. High power-density management challenges in large-scale data centers may further limit deployment efficiency.

OPPORTUNITY

Expansion of Ai Workloads and Edge Computing Infrastructure.

The growing adoption of artificial intelligence, machine learning, and edge computing systems presents substantial opportunities for the micro server IC market. AI-powered applications require high-performance yet energy-efficient processors capable of handling massive real-time data processing workloads. Micro server integrated circuits optimized for AI inference and distributed computing environments are becoming increasingly important across cloud platforms and enterprise networks. The micro server IC market Forecast indicates rising demand for compact server architectures in autonomous systems, smart factories, connected healthcare, and intelligent transportation infrastructure. Telecom operators are also expanding deployment of edge computing nodes powered by advanced micro server chipsets to support 5G connectivity and low-latency applications. Semiconductor companies are investing heavily in ARM-based architectures, high-bandwidth memory integration, and heterogeneous computing technologies to improve server performance efficiency.

CHALLENGE

Intense Competition and Rapid Technology Evolution.

One of the major challenges in the micro server IC market is the rapid pace of semiconductor innovation and intense competition among leading technology companies. Server processor manufacturers must continuously improve computing performance, thermal efficiency, and AI acceleration capabilities to remain competitive in evolving cloud and enterprise computing environments. The Micro Server IC Industry Report identifies increasing pressure from hyperscale cloud providers demanding customized processors optimized for specific workloads. This creates challenges related to product differentiation, scalability, and development timelines. Smaller market participants may face difficulties competing against large semiconductor companies with extensive R&D budgets and advanced manufacturing ecosystems. Another challenge involves balancing performance efficiency with power consumption and heat management in dense server deployments. Maintaining compatibility across multiple software ecosystems and cloud platforms also increases technical complexity.

Micro Server IC Market Segmentation

By Component

Hardware components account for approximately 67% of the global micro server IC market share and remain the dominant segment due to increasing deployment of advanced processors, networking chipsets, memory controllers, and storage ICs in data center infrastructure. Cloud service providers and enterprise IT organizations are investing heavily in high-performance server hardware optimized for virtualization, AI processing, and distributed computing workloads. The micro server IC market Report highlights strong demand for energy-efficient server processors capable of supporting hyperscale cloud environments and edge computing systems. Semiconductor manufacturers are developing advanced multi-core architectures, integrated AI accelerators, and high-speed connectivity solutions to improve server performance efficiency.

Software solutions represent nearly 33% of the micro server IC market share and continue to expand due to increasing adoption of server virtualization, workload orchestration, and cloud infrastructure management platforms. Software plays a critical role in optimizing micro server performance, managing distributed computing workloads, and improving data center resource efficiency. The Micro Server IC Industry Analysis identifies growing demand for AI-enabled server management systems, virtualization software, and automated orchestration platforms across enterprise cloud environments. Organizations are increasingly utilizing software-defined infrastructure to improve scalability, security, and operational flexibility within modern data centers.

To know how our report can help streamline your business, Speak to Analyst

By Processor

Intel-based architectures account for approximately 58% of the global micro server IC market share due to their strong enterprise presence, mature ecosystem support, and extensive deployment across hyperscale data centers and cloud infrastructure platforms. Enterprise IT organizations continue to rely heavily on Intel-compatible server processors because of their compatibility with existing software environments and virtualization technologies. Semiconductor innovation in advanced packaging, AI acceleration, and integrated networking technologies continues to improve performance capabilities of Intel-based micro server systems. Cloud operators are also deploying Intel-compatible architectures for scalable computing workloads requiring high reliability and security integration.

ARM-based architectures represent approximately 42% of the micro server IC market share and are experiencing rapid adoption due to their superior energy efficiency, scalable processing capabilities, and suitability for cloud-native environments. Hyperscale cloud providers are increasingly integrating ARM-based micro server processors into data centers to reduce power consumption and optimize workload efficiency. Semiconductor manufacturers are focusing on advanced ARM server chipsets with integrated AI acceleration, high-bandwidth memory support, and improved thermal efficiency. Increasing demand for sustainable data center infrastructure and modular cloud computing systems continues to strengthen ARM adoption across enterprise and hyperscale environments.

By Application

Web hosting and enterprise applications account for a major share of the micro server IC market because organizations are increasingly adopting compact, energy-efficient server infrastructures to support websites, enterprise applications, and business-critical workloads. Enterprises are deploying micro server IC platforms to improve operational scalability, reduce power consumption, and optimize data center space utilization. The micro server IC market Analysis indicates rising demand for lightweight server architectures capable of supporting virtualization, database management, web hosting, and enterprise collaboration systems. Cloud service providers and hosting companies are integrating multicore micro server processors to manage increasing internet traffic and digital business operations efficiently. Businesses are also investing in advanced server management software and AI-based workload optimization systems to improve infrastructure performance. The growing adoption of hybrid cloud environments, remote working systems, and enterprise digital transformation strategies continues to strengthen the demand for micro server ICs within the web hosting and enterprise segment globally.

Analytics and cloud computing represent one of the fastest-growing application segments in the micro server IC market due to increasing adoption of big data processing, artificial intelligence, and distributed cloud infrastructure. Cloud providers and hyperscale data center operators are deploying advanced micro server ICs to support real-time analytics, machine learning workloads, and scalable cloud-native applications. The micro server IC market Trends highlight growing investments in edge analytics platforms and AI-accelerated computing environments capable of handling massive data volumes with lower energy consumption. Enterprises are increasingly integrating micro server architectures into hybrid cloud ecosystems to improve computing flexibility and operational efficiency. Semiconductor manufacturers are developing high-performance server processors optimized for predictive analytics, automation, and low-latency cloud services. Rising adoption of IoT-connected devices, 5G infrastructure, and real-time business intelligence systems is further driving demand for analytics and cloud computing applications across the global Micro Server IC industry.

By End Use

The micro server IC market is witnessing strong adoption across multiple end-use industries due to rising demand for energy-efficient computing infrastructure, edge processing, and scalable cloud environments. Data centers remain the leading end-use sector because hyperscale cloud providers and enterprise operators require compact server architectures capable of supporting high-density workloads with optimized power consumption. Telecommunications companies are increasingly integrating micro server ICs into 5G infrastructure and edge computing networks to improve low-latency data processing and connected device management. Healthcare organizations are adopting advanced micro server platforms for medical data analytics, telemedicine systems, AI-driven diagnostics, and secure patient information management. Government and defense institutions are also investing in micro server technologies for cybersecurity operations, surveillance systems, autonomous applications, and mission-critical communication infrastructure. The micro server IC market Analysis highlights growing adoption of AI-enabled server architectures, virtualization technologies, and cloud-native platforms across all end-use industries. Enterprises are focusing on scalable, modular, and energy-efficient server systems to reduce operational costs and improve infrastructure flexibility.

Micro Server IC Market Regional Outlook

North America

North America Micro Server IC Market Share, 2026 (%)

To get more information on the regional analysis of this market, Download Free sample

North America accounts for approximately 39% of the global micro server IC market share and remains the leading regional market for cloud infrastructure, semiconductor innovation, and hyperscale data center deployment. The region benefits from the strong presence of major cloud service providers, semiconductor manufacturers, and enterprise technology companies investing heavily in advanced server architectures. The United States dominates regional demand due to rapid expansion of AI workloads, edge computing systems, and enterprise virtualization platforms. The micro server IC market Report highlights increasing adoption of energy-efficient processors and high-density server platforms across hyperscale data centers. Telecom providers are also investing in edge infrastructure powered by micro server integrated circuits to support 5G deployment and low-latency applications. Advanced semiconductor fabrication technologies and strong R&D capabilities continue to strengthen the region’s competitive position. Data center operators are emphasizing sustainable infrastructure and reduced power consumption through next-generation server processors. Increasing integration of AI accelerators, GPUs, and high-bandwidth memory systems into server environments is driving market growth. Cloud computing demand from healthcare, financial services, retail, and industrial sectors further supports expansion. The Micro Server IC Industry Analysis identifies rising investments in hybrid cloud infrastructure and software-defined networking technologies throughout North America.

Europe

Europe holds nearly 25% of the global micro server IC market share and continues to witness stable growth driven by enterprise cloud adoption, industrial automation, and digital transformation initiatives. Countries including Germany, the United Kingdom, France, and the Netherlands are investing significantly in advanced data center infrastructure and energy-efficient computing technologies. The micro server IC market Research Report highlights rising demand for scalable server architectures across manufacturing, automotive, telecommunications, and financial services industries. European enterprises are increasingly modernizing IT infrastructure through virtualization, edge computing deployment, and AI-enabled cloud platforms. Data center operators throughout Europe are focusing heavily on sustainability and low-power server technologies to comply with strict environmental regulations. Semiconductor companies are developing advanced server chipsets optimized for AI processing, real-time analytics, and industrial IoT applications. Telecom providers are expanding edge computing infrastructure to support smart city development and next-generation communication networks. Government initiatives promoting digital infrastructure modernization and cloud computing adoption continue to support regional market growth. The Micro Server IC Industry Report also highlights increasing investment in cybersecurity-focused server solutions and secure enterprise computing platforms.

Germany Micro Server IC Market

Germany accounts for approximately 34% share within the European micro server IC market and remains one of the region’s strongest industrial technology and semiconductor innovation hubs. The country’s advanced manufacturing sector, industrial automation ecosystem, and enterprise cloud adoption are driving strong demand for micro server integrated circuits. German enterprises are increasingly deploying scalable server platforms for AI workloads, industrial IoT systems, and real-time analytics applications. The micro server IC market Analysis highlights rising investment in edge computing infrastructure and data center modernization projects throughout Germany. Automotive manufacturers and industrial companies are integrating advanced server architectures into smart factory operations and autonomous system development programs. Telecom providers are also expanding edge infrastructure to support low-latency applications and 5G deployment. Government support for semiconductor innovation and digital infrastructure expansion continues to strengthen market growth.

United Kingdom Micro Server IC Market

The United Kingdom represents approximately 22% share of the European micro server IC market and continues to expand due to rising cloud computing adoption, enterprise digital transformation, and AI infrastructure investment. Businesses across the country are increasingly implementing micro server platforms to support virtualization, data analytics, and distributed cloud applications. The micro server IC market Forecast highlights growing deployment of edge computing systems across telecommunications, financial services, and healthcare industries throughout the United Kingdom. Data center operators are emphasizing energy-efficient server architectures to improve operational performance and reduce infrastructure costs. Semiconductor and technology companies are investing in AI-enabled server solutions and scalable cloud infrastructure platforms. Government initiatives promoting digital innovation and advanced connectivity continue to accelerate market development. Telecom providers are also expanding low-latency edge networks powered by micro server processors to support smart infrastructure and IoT applications. Increasing enterprise demand for hybrid cloud solutions and secure data management systems continues to strengthen the United Kingdom micro server IC market.

Asia-Pacific

Asia-Pacific represents approximately 29% of the global micro server IC market share and remains one of the fastest-growing regions due to expanding semiconductor manufacturing, hyperscale data center deployment, and digital infrastructure investment. Countries such as China, Japan, South Korea, Taiwan, and India are significantly increasing adoption of advanced server architectures across cloud computing and telecom sectors. The micro server IC market Report highlights strong regional demand for energy-efficient processors, AI acceleration platforms, and edge computing systems designed for low-latency applications. Semiconductor manufacturers throughout Asia-Pacific are investing heavily in advanced fabrication technologies, heterogeneous computing architectures, and ARM-based server processors. Telecom operators are deploying micro server infrastructure to support 5G connectivity, smart city development, and industrial IoT ecosystems. Cloud service providers are expanding hyperscale data centers to manage growing digital workloads generated by e-commerce, AI analytics, and streaming services. Government initiatives supporting semiconductor self-sufficiency and domestic chip manufacturing continue to accelerate regional market expansion. Enterprise adoption of virtualization technologies and hybrid cloud systems is also increasing rapidly throughout Asia-Pacific. The Micro Server IC Industry Analysis identifies strong growth opportunities in AI computing, autonomous systems, and real-time industrial automation applications.

Japan Micro Server IC Market

Japan holds approximately 25% share within the Asia-Pacific micro server IC market and remains a leading center for semiconductor innovation, enterprise computing, and AI-enabled infrastructure development. Japanese enterprises are increasingly deploying advanced server processors to support industrial automation, robotics, cloud computing, and real-time analytics applications. The micro server IC market Research Report highlights rising demand for energy-efficient server architectures and edge computing systems throughout Japan’s manufacturing and telecom sectors. Semiconductor companies are investing heavily in AI accelerators, thermal optimization technologies, and high-performance server chipsets. Government initiatives supporting digital transformation and smart infrastructure modernization continue to strengthen market growth. Japanese cloud providers are expanding data center infrastructure to support increasing demand for enterprise virtualization and cloud-native services. Increasing focus on sustainable data center technologies and intelligent industrial automation further enhances Japan’s long-term micro server IC market opportunities.

China Micro Server IC Market

China accounts for approximately 41% share within the Asia-Pacific micro server IC market and continues to dominate regional growth through large-scale semiconductor manufacturing and rapid expansion of cloud computing infrastructure. The country’s strong digital economy and increasing AI adoption are generating substantial demand for high-performance server processors and scalable computing platforms. The micro server IC market Outlook highlights rising investment in hyperscale data centers, telecom infrastructure, and AI-enabled cloud services throughout China. Semiconductor companies are expanding production capacity for advanced server processors, ARM-based architectures, and networking chipsets. Government initiatives supporting semiconductor self-sufficiency and domestic chip development are accelerating innovation across the industry. Telecom providers are also deploying edge computing infrastructure powered by micro server ICs to support 5G applications and industrial IoT systems. Increasing enterprise adoption of hybrid cloud environments and AI analytics platforms continues to strengthen China’s leadership position within the Asia-Pacific micro server IC market.

Rest of World

The Rest of World region contributes approximately 7% of the global micro server IC market share and includes Latin America, the Middle East, and Africa. These regions are gradually increasing investment in cloud infrastructure, enterprise virtualization, and telecom network modernization to support growing digital transformation initiatives. The micro server IC market Report highlights rising demand for compact and energy-efficient server platforms across financial services, healthcare, telecommunications, and public sector organizations. Middle Eastern countries are investing heavily in hyperscale data centers and smart city projects requiring scalable computing infrastructure and low-latency edge processing systems. Latin American enterprises are increasingly adopting hybrid cloud environments and virtualization technologies to improve operational flexibility and digital service delivery. African telecom operators are also expanding edge infrastructure and data center capabilities to support growing internet penetration and mobile connectivity. Semiconductor and technology companies are collaborating with regional cloud providers to expand access to scalable server architectures. Government initiatives promoting digital infrastructure development and cloud adoption continue to support market expansion. Increasing use of AI analytics, IoT applications, and enterprise data management platforms is strengthening demand for advanced micro server integrated circuits. Improvements in connectivity infrastructure and enterprise IT modernization are expected to create long-term growth opportunities across the Rest of World micro server IC market.

List of Top Micro Server IC Market Companies

- Intel Corporation

- Advanced Micro Devices, Inc. (AMD)

- ARM Holdings

- Applied Micro Circuits Corporation (AMCC)

- Marvell Technology Group

- Broadcom Inc.

- Cavium

- Hewlett Packard Enterprise (HPE)

- Dell Technologies

- Super Micro Computer, Inc

- Quanta Computer Inc.

- NVIDIA Corporation

- Fujitsu Limited

- Cisco Systems, Inc.

- NEC Corporation

- Samsung Electronics

- MediaTek Inc.

- Ampere Computing

- NXP Semiconductors

- Qualcomm Technologies, Inc

Top Two Companies by Market Share

- Intel Corporation – Approximately 26% market share

- Advanced Micro Devices, Inc. (AMD) – Approximately 18% market share

Investment Analysis and Opportunities

The micro server IC market is attracting substantial investment from semiconductor manufacturers, cloud service providers, telecom companies, and AI infrastructure developers. Increasing demand for energy-efficient data centers, edge computing systems, and AI-enabled cloud infrastructure is encouraging strong capital investment across advanced server processor technologies. Semiconductor firms are investing heavily in advanced fabrication nodes, ARM-based architectures, and heterogeneous computing platforms designed for hyperscale workloads.

The micro server IC market Opportunities are especially strong in AI inference acceleration, 5G edge infrastructure, enterprise virtualization, and distributed cloud computing environments. Cloud providers are expanding deployment of compact server architectures optimized for low-latency data processing and scalable computing efficiency. Telecom operators are also increasing investment in micro server infrastructure to support edge AI applications and next-generation networking systems.

New Product Development

New product development in the micro server IC market is centered around AI acceleration, low-power computing architectures, advanced thermal management, and scalable edge processing technologies. Semiconductor manufacturers are developing multi-core server processors with integrated AI engines and high-bandwidth memory systems designed for hyperscale cloud infrastructure and edge computing workloads.

Advanced packaging technologies, chiplet architectures, and integrated networking solutions are improving server scalability and operational performance. Cloud service providers are increasingly demanding customized processors tailored for machine learning, analytics, and virtualization workloads. Semiconductor companies are also focusing on sustainable server designs with improved power efficiency and reduced heat generation. Expansion of edge AI applications and autonomous systems continues to accelerate innovation across the global Micro Server IC industry.

Five Recent Developments (2023-2025)

- Intel Corporation expanded AI-enabled Xeon server processor capabilities in 2024 to improve hyperscale cloud computing performance.

- AMD introduced advanced EPYC server processors in 2025 optimized for AI inference and enterprise virtualization workloads.

- NVIDIA Corporation strengthened data center AI infrastructure solutions in 2024 through integration of high-performance server accelerators.

- Ampere Computing expanded ARM-based cloud server processor deployment partnerships during 2025 for hyperscale data center environments.

- Marvell Technology Group increased investment in edge computing chipsets and networking infrastructure solutions in 2023 to support 5G expansion.

Report Coverage of Micro Server IC Market

The micro server IC market Report provides comprehensive analysis of semiconductor innovation, cloud infrastructure expansion, AI computing adoption, and edge processing technologies influencing the global server processor ecosystem. The report evaluates key market growth factors including rising cloud computing demand, enterprise virtualization, telecom infrastructure modernization, and increasing adoption of energy-efficient server architectures.

Request for Customization to gain extensive market insights.

Regional analysis spans North America, Europe, Asia-Pacific, and Rest of World markets with country-level insights focused on semiconductor manufacturing capabilities, cloud infrastructure investment, and digital transformation initiatives. The Micro Server IC Industry Report also evaluates competitive strategies adopted by leading semiconductor and technology companies including partnerships, product launches, fabrication expansion, and AI accelerator integration. Emerging innovations such as chiplet architectures, heterogeneous computing platforms, edge AI processing systems, and sustainable data center technologies are extensively analyzed to provide strategic insights for investors, semiconductor manufacturers, enterprise IT providers, and cloud infrastructure developers.

- 2021-2034

- 2025

- 2021-2024

- 80

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us