Microspheres Market Size, Share & Industry Analysis, By Type (Hollow and Solid), By Materials (Polymer, Glass, Ceramic, Metallic, Fly Ash, and Others), By Application (Construction Materials & Composite, Oil & Gas, Paints & Coatings, Automotive, Healthcare & Biotechnology, Cosmetics & Personal Care, and Others), and Regional Forecast, 2026-2034

Microspheres Market Size and Future Outlook

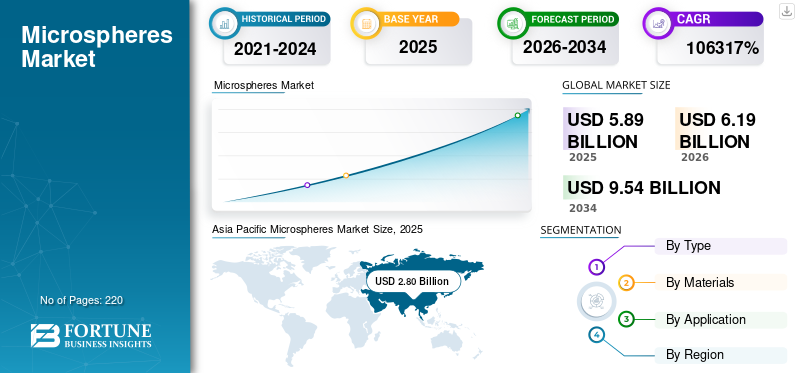

The global microspheres market size was valued at USD 5.89 billion in 2025. The market is projected to grow from USD 6.19 billion in 2026 to USD 9.54 billion by 2034, exhibiting a CAGR of 5.6% during the forecast period. Asia Pacific dominated the microspheres market with a market share of 47.54% in 2025.

Microspheres are engineered spherical particles, typically in the micron-size range, produced from materials such as glass, ceramics, polymers, and fly-ash-derived cenospheres. They are supplied as hollow or solid spheres to deliver density reduction, rheology control, improved surface finish, thermal insulation, and buoyancy in formulated systems and composites.

The market growth is driven by lightweighting and performance optimization across paints and coatings, construction materials, polymer composites, and oil and gas applications. Producers are also expanding differentiated grades to meet tighter performance windows in automotive and industrial coatings. At the same time, cenosphere recovery and processing continue to improve the accessible supply of low-density fillers.

Furthermore, the market comprises several major players, including 3M, Nouryon, Cospheric LLC, Momentive, and Omya AG. Competitive positioning is shaped by product consistency, application engineering support, and the ability to supply multiple grades at scale across regional manufacturing hubs.

Download Free sample to learn more about this report.

Microspheres Market Takeaways

- 2025 Market Size: USD 5.89 Billion

- 2026 Market Size: USD 6.19 Billion

- 2034 Forecast Market Size: USD 9.54 Billion

- CAGR: 5.6% from 2026–2034

- Asia Pacific dominated the microspheres market with a 47.54% share in 2025.

- The hollow segment accounted for the largest market share of 54.2% in 2025.

- The polymer segment held a leading share of 31.9% in 2025.

North America

North America remains a significant market and is estimated to reach USD 1.50 billion by 2026.

Europe

Europe is projected to reach USD 1.39 billion by 2026, expanding at a CAGR of 5.2% during the forecast period.

Asia Pacific

Asia Pacific led the global market with USD 2.80 billion in 2025 and is projected to reach USD 2.96 billion in 2026.

U.S.

The U.S. microspheres market was valued at USD 1.25 billion in 2025, supported by strong demand across construction, coatings, and industrial applications.

Japan

Japan is expected to witness steady market growth, driven by increasing adoption of advanced lightweight materials in manufacturing and construction sectors.

Read More

MICROSPHERES MARKET TRENDS

Lightweighting in High-Volume Manufacturing, Low-Carbon Construction Formulations, and High-Performance Coatings Are the Significant Market Trends

Microspheres demand continues to rise, where formulators and converters need to reduce density while maintaining mechanical performance and surface quality. In paints and coatings, suppliers are promoting grades that enable higher film build, matting control, and improved sanding without a proportional increase in formulation viscosity. In construction materials and composites, microspheres support low-density putties, sealants, panels, and syntactic foams, thereby improving handling and insulation performance. At the same time, the availability of fly-ash-derived cenospheres in Asia continues to influence regional economics, supporting wider adoption in cost-sensitive lightweighting applications.

- For instance, product suppliers continue to release application calculators and formulation guides (density, loading, and property trade-offs) to shorten qualification cycles and reduce performance risk for coatings and composite customers.

MARKET DYNAMICS

MARKET DRIVERS

Lightweighting and Formulation Efficiency in Coatings and Construction Materials Are Driving Market Growth

Microspheres enable formulators to add volume and improve application properties while reducing mass per unit area in coatings and construction materials. This improves transport economics and can support lower material usage in certain designs. In automotive and industrial markets, microspheres also support lightweighting of composite parts and help tune stiffness-to-weight ratios, contributing to efficiency targets. These factors drive the microspheres market growth.

- For instance, lightweight fillers are increasingly specified in repair putties and texture coatings to improve sanding and handling while maintaining low density.

MARKET RESTRAINTS

Qualification Requirements, Cost-Performance Trade-offs, and Supply Variability Can Limit Adoption

Microspheres must meet tight performance requirements for crush strength, particle size distribution, and compatibility with binder systems, especially in high-end coatings, engineered composites, and oil and gas uses. Qualification cycles can be lengthy, and customers may require extensive application testing to validate processing stability and long-term performance. For cenospheres, supply quality can vary by source and processing route, increasing the need for sorting and quality control.

MARKET OPPORTUNITIES

Growth in Syntactic Foams, Thermal Management, and EV-Driven Lightweighting to Create Lucrative Growth Opportunities

Demand growth is expected for buoyancy and syntactic foam systems in offshore energy, marine, and specialized industrial applications, where low density and compressive strength are critical. In addition, thermal insulation and thermal management needs in building materials and mobility platforms support further penetration of hollow glass and ceramic microspheres. As electric vehicle platforms scale, lightweighting of non-structural components and coatings optimization can expand addressable demand in high-volume manufacturing.

MARKET CHALLENGES

End-Use Cyclicality, Regulatory Scrutiny in Some Polymer Uses, and Substitution Risk May Affect Growth

Construction and automotive demand can be cyclical, which can soften microspheres consumption during downturns. In cosmetics and other consumer uses, polymer microspheres may face regulatory scrutiny under microplastics restrictions, prompting substitution toward alternative texture agents in some regions. Moreover, customers may substitute microspheres with alternative lightweight fillers when cost or supply reliability becomes a concern, particularly in price-sensitive applications.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Hollow Segment Held the Largest Share Owing to the Preference From the Construction Industry

Based on type, the market is segmented into hollow and solid.

The hollow segment accounted for the largest microspheres market share in 2025. The growth of this segment is driven by its adoption in paints and coatings, construction materials, and oil and gas buoyancy and syntactic foam systems. Furthermore, the segment held a 54.2% share in 2025.

The growth of the solid segment is supported by rising demand in coatings and cosmetics for texture, matting, and surface feel, as well as in select industrial formulations that require controlled friction or spacing. The solid segment is projected to grow at a 5.5% CAGR during the forecast period.

By Materials

Polymer Segment is Expected to Remain Prominent Due to Broad Applicability in Various Applications

Based on materials, the market is segmented into polymer, glass, ceramic, metallic, fly ash, and others.

The polymer segment accounted for the largest share in 2025, driven by solid and expandable microspheres used to reduce density and improve surface finish in coatings and construction materials. Furthermore, the segment held a 31.9% share in 2025.

The glass segment is expected to grow favorably with a CAGR of 5.7% over the forecast period, driven by hollow grades used for lightweighting, insulation, and composite reinforcement.

By Application

To know how our report can help streamline your business, Speak to Analyst

Construction Materials & Composite Segment Dominates the Market Due to the Extensive Use of the Product

By application, the market is categorized into construction materials & composite, oil & gas, paints & coatings, automotive, healthcare & biotechnology, cosmetics & personal care, and others.

The construction materials & composite segment accounted for the largest share in 2025, driven by broad use in low-density putties, sealants, panels, and composites that offer improved handling and reduced weight. Furthermore, the segment held a 29.5% share in 2025.

The oil & gas segment is also expected to experience favorable growth over the forecast period. The segment's growth is supported by buoyancy modules and syntactic foam systems in offshore and subsea environments. The segment is expected to grow at a CAGR of 5.8% over the forecast period.

Microspheres Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Microspheres Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 2.80 billion, and is expected to maintain its leading share in 2026, valued at USD 2.96 billion. The region's growth is supported by high-volume manufacturing, construction activity, and strong demand for paints and coatings. China remains the largest consumer, while Japan and South Korea contribute through advanced coatings, electronics-adjacent materials, and precision manufacturing supply chains.

China Microspheres Market

In 2025, China’s market reached a valuation of USD 1.52 billion. Construction materials, industrial coatings, and large downstream manufacturing bases support steady microsphere consumption, including cenosphere use when supply economics are favorable.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is a significant contributor to the market, with the market estimated to reach USD 1.50 billion by 2026. The region benefits from broad coatings and construction activity, a mature composites ecosystem, and offshore and oilfield uses that support hollow microspheres in buoyancy and syntactic foam systems. The U.S. market accounts for the majority of regional consumption through scale in manufacturing and high-value industrial end uses.

U.S. Microspheres Market

In 2025, the U.S. market reached a valuation of USD 1.25 billion. In the U.S., the demand is supported by large-scale coatings and construction materials consumption, strong automotive and composites manufacturing, and specialty offshore applications.

Europe

Europe is expected to experience significant growth over the coming years. The European region is projected to grow at a CAGR of 5.2% during the forecast period and reach a valuation of USD 1.39 billion in 2026. High-value industrial coatings, automotive lightweighting, and advanced construction and composites applications drive the region’s growth. Europe also benefits from strong quality and qualification standards that support consistent demand for engineered microsphere grades.

U.K. Microspheres Market

The U.K. market in 2025 was valued at USD 0.18 billion, representing approximately 4.5% of global market revenues.

Germany Microspheres Market

Germany’s market reached approximately USD 0.37 billion in 2025, equivalent to around 5.8% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2026 is expected to reach a valuation of USD 0.21 billion. The demand in the region is largely import-driven and linked to construction, general industrial coatings, and selective automotive and oil and gas projects.

Middle East & Africa

The Middle East & Africa region is gradually expanding, with a valuation of USD 0.13 billion in 2025. GCC countries account for a notable share of regional demand, driven by offshore and oilfield uses of hollow microspheres in buoyancy and syntactic foam systems, while other demand is linked to construction materials and imported specialty formulations.

GCC Microspheres Market

GCC market reached a valuation of USD 0.08 billion in 2025, accounting for approximately 2.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Adopting Business Expansion Strategies to Maintain Their Positions in the Market

Competition is shaped by access to consistent raw materials, control over particle size distribution and crush strength, support for formulation and processing qualification, and the ability to supply multiple grades globally. Diversified advanced materials producers compete with specialists focused on hollow glass microspheres, expandable polymer microspheres, and cenosphere processing. Some of the key market players include 3M, Nouryon, Cospheric LLC, Momentive, and Omya AG. Key competitive differentiators include product consistency, technical service, and supply reliability across regional manufacturing hubs.

LIST OF KEY MICROSPHERES COMPANIES PROFILED

- 3M (U.S.)

- Nouryon (Netherlands)

- Cospheric LLC (U.S.)

- Momentive (U.S.)

- Omya AG (Switzerland)

- Envirospheres (Australia)

- Trelleborg(Sweden)

- Potters Industries LLC. (U.S.)

- MO SCI, LLC (U.S.)

- Bangs Laboratories, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2024: Nouryon launched Expancel WB microspheres for white-shoe sole applications (introduced at Chinaplas 2024 in Shanghai), signalling continued application-driven product innovation beyond traditional industrial uses.

- October 2023: Nouryon started full-scale production at its new Expancel expandable microspheres plant in Green Bay, Wisconsin (U.S.), signalling execution of earlier investments to improve regional availability across packaging, construction, mining, and automotive end uses.

- June 2022: Nouryon launched Expancel HP92 microspheres designed to withstand high-pressure processing in automotive underbody coatings and sealants, signalling innovation targeted at lightweighting and durability under demanding manufacturing conditions.

- July 2021: Nouryon announced it would increase Expancel production capacity in China by relocating operations from Suzhou to Ningbo (planned completion by end-2021), signalling a push to scale regional supply closer to major Asia Pacific demand centers.

- April 2021: BASF and Omya entered a global partnership to advance and commercialize BasoSphere™ hollow glass microspheres for oil & gas cementing/drilling, signalling stronger technology–market alignment for lightweight, high-compressive-strength additives in well construction.

- August 2020: Nouryon selected Green Bay, Wisconsin (U.S.) for a new Expancel® expandable microspheres production facility, signalling a strategic capacity expansion to strengthen supply and customer service in North America.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Materials, Application, and Region |

| By Type |

|

| By Materials |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 5.89 billion in 2025 and is projected to reach USD 9.54 billion by 2034.

Recording a CAGR of 5.6%, the market is slated to exhibit steady growth during the forecast period.

The construction materials & composite application segment led the market in 2025.

Asia Pacific held the largest market share in 2025.

3M, Nouryon, Cospheric LLC, Momentive, and Omya AG are some of the prominent players in the market.

The growth driver is the lightweighting and formulation efficiency in coatings and construction materials.

The major factors expected to favor product adoption are the need for lightweighting and cost-performance optimization, plus formulation benefits such as better rheology/flow, improved surface finish, insulation/buoyancy, etc. across industrial products.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us