Industrial Coatings Market Size, Share & Industry Analysis, By Resin (Acrylic, Alkyd, Polyurethane, Epoxy, Polyester, and Others), By Technology (Solvent-borne, Water-borne, Powder, and Others), By End-use (General Industrial, Powder, Automotive OEM, Automotive Refinish, Protective, Wood, Marine, Coil, Packaging, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

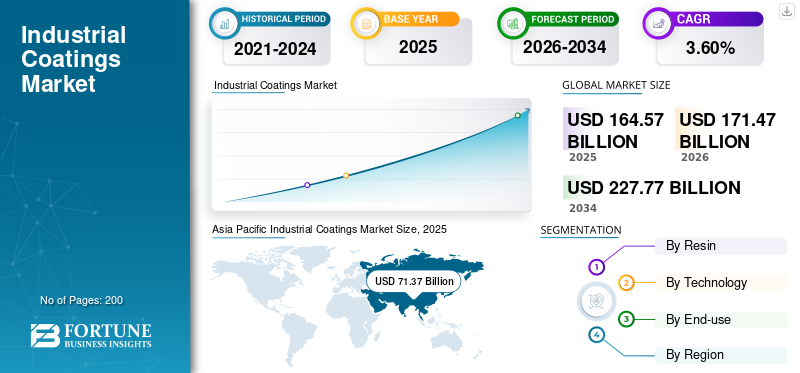

The global industrial coatings market size was USD 164.57 billion in 2024 and is projected to grow from USD 171.47 billion in 2025 to USD 227.77 billion by 2034 at a CAGR of 3.60% during the forecast period (2026-2034). Asia Pacific dominated the industrial coatings market with a market share of 43.40% in 2025. Moreover, the industrial coatings market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 40.90 billion by 2032, driven by increasing car sales, increased building activity, and other factors that are expected to drive the market size growth.

Industrial coatings are used for different applications to ensure resistance to anti-corrosion, surge durability, prevent wear & tear, and increase operational efficiency. The growing demand for environmentally friendly coatings, as well as the need for efficient processes and durable coatings with better aesthetics, is the major factor driving the industrial coatings market growth. In addition to that, the rapid urbanization, development of the middle-class, increased infrastructure, rising disposable incomes, increased propensity to spend extravagantly, and others would aid growth. The high demand for these products is mainly attributable to the global GDP, growth of the infrastructure, industrial development, and the rising number of building & construction activities.

The impact of COVID-19 pandemic has a negative impact on the coatings industry as the sales are mostly impacted by the GDP movement. Most of the production units were shut because of low labor force and lockdown situations which has resulted in the uncertainty among various producers and supply chain constraints. The automotive industry showed sluggish sales, structural slowdown, and sputtering economy in 2019-2023. During the second peak of COVID-19 in India the sales of new vehicles were shrunken as most of the auto plants and dealers were forced to close down. However, easing of lockdowns in many European countries along with incentive packages to support economic revival seems to benefit the regional automotive industry. Whereas, the automotive industry in the U.S. remains fragile due to limited inventories and fewer incentives.

Download Free sample to learn more about this report.

Global Industrial Coatings Market Key Takeaways

Market Size & Forecast:

- 2025 Market Size: USD 164.57 billion

- 2026 Market Size: USD 171.47 billion

- 2034 Forecast Market Size: USD 227.77 billion

- CAGR: 3.60% from 2026–2034

Market Share:

- Asia Pacific dominated the industrial coatings market with a 43.40% share in 2025, supported by government subsidies, rising automobile production, infrastructure development, industrial output, and high consumer spending.

- By resin type, acrylic held a significant share due to its glossy, durable surface and chemical/weather resistance.

- By technology, water-borne coatings led the market owing to their low VOC emissions, ease of application, and environmental benefits.

- By end-use, the general industrial segment led due to high demand for corrosion protection, chemical resistance, and cost reduction in infrastructure and manufacturing applications.

Key Country Highlights:

- United States: Projected to reach USD 40.90 billion by 2032, driven by increasing car sales, construction activities, and demand for energy-efficient, sustainable coatings.

- China: Leading automotive and industrial hub with rising disposable incomes and infrastructure development driving demand for coatings.

- Germany: Focus on environmentally friendly coatings, increased adoption of water-borne technologies, and sustainability in manufacturing.

- India: Rapid urbanization, expanding middle class, and infrastructure growth supporting increased demand for industrial coatings.

- Brazil: Growth fueled by rising vehicle ownership, poor road conditions, and growing demand for automotive refinish coatings.

- South Africa: Rising awareness of high-performance coatings for white goods, automotive, and packaging sectors.

- Saudi Arabia: Increased infrastructure investment and industrial output driving demand across marine, coil, and protective coating applications.

Industrial Coatings Market Trends

Manufacturers are Focusing on Sustainability Which Will Bolster Market Trend

Within the coatings sector, sustainability is becoming increasingly important. Additives, pigments, resins, and final coating formulation manufacturers have increased their attention on producing greener techniques that consume less energy, produce less waste, and emit fewer pollutants. Few of the organizations have created formal efforts to raise awareness, inspire innovation, and support the continual growth and upgrading of sustainable operations. Green manufacturing has a large and demonstrable impact on productivity and profitability, in addition to helping the environment. As a means of building sustainable processes, green chemistry principles emphasize effectiveness and hazard avoidance. Because energy use is linked to carbon dioxide emissions, reducing energy consumption is a top priority. Also, manufacturers are improving the overall resource usage. For instance, companies in the coatings sector are focusing on reducing the energy usage which is an important process for development and introducing greener manufacturing techniques. This will create new opportunities in the industry growth. Asia Pacific witnessed a growth from USD 60.76 billion in 2022 to USD 64.23 billion in 2023.

Adoption of Green Chemistry to Promote Sustainability in the Market

The concerns related to the impact on human health and the environment have led to the need for the adoption of green chemistry in industrial coating. However, the transition to green chemistry faces several challenges related to achieving regulatory compliance, low costs, and better functionality. The growing stringent government norms or rules and consumer awareness may create a wider adoption of "green chemistry" or "sustainable chemistry" in coatings.

Green chemistry is extensively used in industrial and consumer end-user industries such as automotive, aerospace, marine, electronics, consumer goods, and construction & buildings in the industrial coatings industry. Thus, green chemistry aims to reduce the volatile organic compounds (VOCs), enable process efficiency, use feedstock, and minimize waste. However, owing to increasing concerns, key players are adopting green chemistry, efficiently promoting sustainable product development.

Download Free sample to learn more about this report.

Industrial Coatings Market Growth Factors

Rising Usage of Environmentally Friendly Coatings to Drive Growth

There are several manufacturing methods for producing finished products, solvents, and alcohols. Volatile organic compounds (VOCs) are introduced in the environment as a result of the manufacturing process and they must be removed effectively. They are organic chemicals that turn into gases at room temperature and are the main cause of ground-level air pollution. According to several reports, VOCs are known to be harmful to human health and often impact the environment greatly. Coatings are a major source of human-generated VOCs.

- For example, in automotive coating processes, VOC emissions are produced during the spraying processes via the use of solvent-borne coatings. Industrial coating manufacturers, in particular anti-corrosion and heavy-duty protective coatings, are under pressure to reduce their products' VOC emissions.

But various industries are gradually turning towards water-borne and powder-based coatings due to economic factors, as well as foreign legislation and environmental concerns. Low VOC and air pollution issues remain a huge driving force for industrial coatings mostly driven by customer preferences, tightening regulations around the world, and "green" certification programs such as LEED v4, EU-Ecolabel, and AgBB. Low-VOC coatings are considered to be an alternative because regulatory agencies are raising concerns regarding the possible harmful effects of VOC spreads and limitations.

Adopting new products is followed by rising preference for water-borne coating. The popularity of powder-based coatings is also increasing where water-borne paints are undesirable, as they do not produce VOCs while also optimizing the critical properties for demanding end-uses. The push towards sustainability, lower VOCs, and stronger controls on substances are likely to drive the market, especially because of environmental awareness.

Most of the leading manufacturers of paints & coatings in North America now report near zero VOC. This is a voluntary move by the industry, provided that even in the strictest product categories and regions, such as the Southern California Air Quality Management District (SCAQMD), up to 50 g/L VOC is permissible. There is a gradual but very important change in Asia Pacific and China towards the removal of solvents and other additives that are considered to have a harmful impact on human health.

Improved Appearance and Energy Efficiency in Automotive OEM to Propel Growth

Industrial coatings are mostly used on passenger cars and light commercial vehicles (LCVs). Asia Pacific was the leading consumer of automotive OEM coatings. China is a leading country for vehicle sales due to the rising personal disposable income that grew at a double-digit pace. Europe is also a significant consumer of automotive OEM coatings. It manufactured nearly 27.5 million passenger cars and 3.2 million LCVs in 2019, based on The Organization Internationale des Constructeurs d'Automobiles (OICA) data. Growing automotive production and sales is likely to create lucrative opportunities for the market. Overall, the demand is affected by demographic trends where older people drive less and younger people worry about the effect of auto emissions on the environment.

The U.S. was a major consumer of automotive OEM coatings for LCVs. OEMs use their current equipment and processes to explore new ways to attain premium appearances. Energy consumption not only affects prices but also sustainability. Thus, reducing the energy consumption lowers costs and decreases emissions of greenhouse gases. The coatings industry is aiming to reduce energy consumption in several ways. Manufacturers are creating more efficient processes for the production of coating ingredients and formulated paints. Resin manufacturers are innovating their products that would be able to work at lower temperatures. Equipment manufacturers, on the other hand, are improving the efficiency of healing equipment to extend the applicability of alternative healing methods that are more energy efficient.

- For instance, In January 2020, Royal DSM launched a bio-based self-matting resin that has been successfully incorporated by coating formulators.

The product contains novel resins and pigment chemistries which improves the energy efficiency of structures such as vehicles. The reduction in energy consumption during the automotive coatings process is anticipated to boost the global market.

RESTRAINING FACTORS

Effect of Humidity on Drying Time to Hinder Market Growth

Many factors contribute to the rapid drying of coatings. Apart from the structure, the thickness of the coating plays a key role in environmental conditions. Issues related are mainly due to environmental conditions, humidity, and temperature. For their products, each coating manufacturing industry issues different guidelines. For the applicator, it is often advisable to read the requirements before beginning the coating job. There are certain conditions that are specified for perfect application. The air temperature needs to be above 700C for oil-based coatings. The temperature should be above 1cc for acrylic and latex coatings. At 2 cc, some creative compositions quickly dry out.

The drying time of acrylic and latex coatings and oil-based coatings, get seriously affected in humid regions. To deal with this issue, the oxidation process treats oil-based coatings. But, water-borne coatings have a tough time. As water-borne coatings are dried through the natural drying process, it takes less drying time than solvent-borne coatings. The method becomes more complicated when used on wooden surfaces since wood appears to absorb moisture from the air. This further affects its substrate adhesive properties. This may cause the surface to peel or bubble. Many coatings manufacturing companies are investing a great deal in test chambers for humidity.

Industrial Coatings Market Segmentation Analysis

By Resin Analysis

Acrylic Segment to Control a Significant Global Market Share Due to Rising Adoption

Based on resin, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and others.

The Acrylic segment is anticipated to hold a dominant market share of 33.08% in 2026. Acrylics provide a glossy, durable surface that is resistant to chemicals and weather. Due to the general increased usage of ceramics in the biomedical sector, the acrylic segment held the majority of the industrial coatings market share. Resins, or binders, are polymers that are chosen based on the physical and chemical qualities desired in the finished product to keep all components of the product together. Naturally, solvent-borne coatings are the most common application for solution polymerized acrylic resins.

Alkyd resins are employed in many solvent-based coating systems. Polyols, acids, and vegetable oils are used to create this form of polyester. Alkyds are generally more affordable and are referred to as "general purpose" coatings due to their versatility. Epoxies are very water resistant, chemically resistant, and abrasion resistant. It does, however, lose its shine when exposed to UV radiation. Polyurethanes have a high gloss and flexibility, as well as chemical stain resistance and water resistance.

By Technology Analysis

Water-borne Segment Held Majority Share Owing to its Low VOC Content

In terms of technology, the market is segmented into solvent-borne, water-borne, powder, and others.

In 2026, the Waterborne Coatings segment is projected to lead the market with a 45.20% share. The majority market share was held by the water-borne segment. These type of coatings decrease VOC emissions during application, can be easily cleaned, minimize the danger of fire, and result in lesser worker exposure to the organic vapors. Key features of these coatings, such as hardness and resistance to water and chemicals, have been enhanced to meet product demand. This coating technology not only reduces the cost of the coating process for customers, but it also benefits coating producers by offering a cost-effective and attractive payback period for any investment necessary to convert the line of application to the use of water-borne coatings.

Solvents are utilized to transfer coating solids to the painted surface. They are added to coatings to help in reducing viscosity and making the coating easier to apply. However, solvents are an important source in coating applications due to the emission of hazardous air pollutants (HAPs) and volatile organic compounds (VOCs) during curing process.

By End-use Analysis

To know how our report can help streamline your business, Speak to Analyst

General Industrial Segment Expected to Lead Due to its Ability to Provide Corrosion Protection

On the basis of end-use, the market is classified into general industrial, powder, automotive OEM, automotive refinish, protective, wood, marine, coil, packaging, and others.

The rising usage of these type of products in general industries is due to its high degrees of corrosion resistance, chemical resistance, and UV or weather protection ability which is crucial in cost reductions. A rising trend in infrastructure development activities, as well as an expanding middle-class population, are providing promising market growth prospects. Some of the primary drivers of the automobile coating industry, both in OEM and refinishing, include high durability, chemical resistance, and sustainability, as well as scratch resistance, including low VOC and water-borne systems.

Low and ultra-low VOC coatings are of particular interest to the wood furniture and flooring industry, due to tightening regulatory pressures and new sustainability initiatives. Wood product manufacturers are now turning to the high-performance water-based coatings with a variety of curing mechanisms under pressure to reduce emissions and meet the shortened lead times. To adhere to its many unique surfaces, the typical agricultural, construction, and earthmoving (ACE) machine needs a variety of different coating technologies including powder coatings for smaller metal components such as handles, pedals, and wheels. Powder coatings have an additional environmental bonus of producing near-zero waste and no VOCs. Lower VOC requirements are likely to drive the marine coating industry towards more sustainable solutions. The General Industrial segment is projected to dominate the market with a share of 27.60% in 2026.

REGIONAL INSIGHTS

Asia Pacific Industrial Coatings Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 71.37 billion in 2025, accounting for 43.40% share, and is expected to reach USD 74.76 billion in 2026. Asia Pacific dominated the industrial coatings market and is expected to hold this position during the forecast period. Government subsidies, rising automobile production, building activities, general industrial output, low interest rates, and high consumer spending, all major components of GDP, are anticipated to drive market growth. The Japan market is projected to reach USD 6.24 billion by 2026, the China market is projected to reach USD 44.6 billion by 2026, and the India market is projected to reach USD 10.1 billion by 2026.

- In China, the automotive oem segment is estimated to hold a 8.8% market share in 2023.

Europe

The Europe region captured 22.00% of the global market in 2025, generating USD 36.18 billion in revenue, and is projected to reach USD 37.52 billion in 2026. The European market is likely to be driven by advancements in the oil and gas industry as well as infrastructure initiatives. The rising usage of powder coatings is expected to expand as a consequence of technical improvements in this technology in recent years. Furthermore, an increase in environmental consciousness is projected to boost market expansion. The UK market is projected to reach USD 3.3 billion by 2026, while the Germany market is projected to reach USD 4.72 billion by 2026.

North American

In 2025, the North America market stood at USD 39.91 billion, representing 24.30% of global demand, and is projected to grow to USD 41.37 billion in 2026. The North American industrial sector is expected to recover at a moderate pace. Due to the general rising industrial production, the region is expected to generate high demand for coatings. Increasing car sales, increased building activity, and other factors are expected to drive the market growth in this region. The US market is projected to reach USD 34.51 billion by 2026.

Latin America

In 2025, Latin America represented USD 7.99 billion, accounting for 4.90% of the worldwide market, and is projected to grow to USD 8.3 billion in 2026. The major multinational coating manufacturers have a significant presence in Latin America. These key players have been continuously investing in the region through organic expansion and strategic acquisitions. Over the last few years, the region has seen an increase in automobile ownership as a result of increased purchasing power and living standards. Additionally, the prevalence of poor road condition and frequent traffic accidents is likely to fuel the growth of automotive refinish coatings in the region.

Middle East and Africa's

The Middle East & Africa market accounted for USD 9.12 billion in 2025, representing 5.50% of the global industry, and is expected to reach USD 9.52 billion in 2026. The Middle East and Africa's markets are expected to expand due to the region's growing demand for white goods, fueled by lower interest rates on borrowing. As coatings producers raise awareness about the advantages of employing the proper coating materials for various application sectors such as automotive, marine, packaging, and others, it is also expected to generate many prospects for products such as coil coatings, which will drive the market's growth. Furthermore, developments in industrial output, building and infrastructure investment, lower energy pricing, and rising consumer spending are anticipated to benefit and fuel product demand.

To know how our report can help streamline your business, Speak to Analyst

List of Key Companies in Industrial Coatings Market

Companies to Focus on Strategic Planning to Strengthen their Market Share

Major firms are pursuing mergers and acquisitions, constructing infrastructure, expanding manufacturing facilities, investing in research and development, and seeking vertical integration possibilities across the value chain. These companies compete on the basis of the product quality they offer and the technology they employ to manufacture it. The market is fragmented, with several major competitors as well as numerous global and regional small-and-medium-sized players operating globally.

LIST OF KEY COMPANIES PROFILED

- Akzo Nobel N.V. (Netherlands)

- Axalta Coating Systems, LLC (U.S.)

- Industrial Coatings Ltd. (Finland)

- PPG Industries, Inc. (U.S.)

- The Sherwin-Williams Company (U.S.)

- Nippon Paint Holdings Co., Ltd. (Japan)

- Kansai Paint Co., Ltd. (Japan)

- RPM International Inc. (U.S.)

- BASF SE (Germany)

- PPG Asian Paints Pvt Ltd. (India)

- Hempel A/S (Denmark)

- The Chemours Company FC, LLC. (U.S.)

- Jotun A/S (Norway)

KEY INDUSTRY DEVELOPMENTS

- August 2020 –Sherwin-Williams Company Protective & Marine introduced rapid curing technology to significantly reduce the time and labor costs for the protection of structural steels. The company’s Envirolastic 2500 system can be applied as a single or multi-coat system with comparable color and gloss retention to a polyurethane topcoat, resulting in faster shop throughput, as compared to a traditional two-pack coating system.

- July 2020 – PPG Industries, Inc. announced the introduction of hydrophobic coating for PPG Surface Seal. The newly formulated product is ultraviolet (UV) light-resistant, compatible with most fluids in aerospace cleaning and maintenance, and is compliant with REACH & EPA.

REPORT COVERAGE

The market report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, products, and applications. Also, it offers insights into the key market trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors that have contributed to the growth of the market over recent years. It includes historical data & forecasts revenue growth at global, regional, and country levels, and analyzes the latest market dynamics and opportunities in the industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.60% during 2026-2034 |

|

Unit |

Value (USD Billion); Volume (Kiloton) |

|

Segmentation |

By Resin

|

|

By Technology

|

|

|

By End-Use

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market worth was USD 164.57 billion in 2025 and is projected to reach USD 227.77 billion by 2034.

In 2025, the Asia Pacific market size stood at USD 71.37 billion.

Growing at a CAGR of 3.60%, the market will exhibit steady growth during the forecast period (2026-2034).

The water-borne segment is the leading technology in the market.

Improved appearance and energy efficiency in automotive OEMs is one of the major drivers of the market.

PPG Industries, Inc., The Sherwin-Williams Company, AkzoNobel N.V., Axalta Coating Systems, LLC, and Nippon Paint Holdings Co., Ltd. are the top players in market.

Asia Pacific dominated the global market in 2025.

The robust growth of environmentally friendly coatings shall drive adoption of Industrial Coatings.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us