Military 3D Printing Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Services), By Material Type (Metals & Alloys, Polymers & Plastics, Ceramics, Composites, & Others), By Technology (Stereolithography, Selective Laser Sintering, Fused Deposition Modeling, Direct Metal Laser Sintering, Electron Beam Melting, & Binder Jetting), By Application (Prototyping, Tooling, End-use Part Production, Research & Development, and Maintenance, Repair, & Overhaul), By Platform (Armored Vehicles, Ground Equipment, & Others), By End User, and Regional Forecast 2026-2034

KEY MARKET INSIGHTS

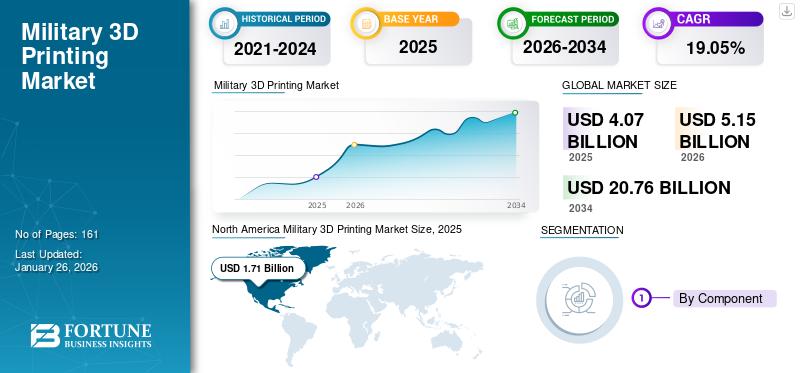

The global military 3D printing market size was valued at USD 4.07 billion in 2025. The market is projected to grow from USD 5.15 billion in 2026 to USD 20.76 billion by 2034, exhibiting a CAGR of 19.05% during the forecast period. North America dominated the global market with a share of 42.02% in 2025.

Military 3D printing, or additive manufacturing (AM) for defense purposes, is the application of layer-by-layer manufacture technologies to make three-dimensional structures, spare components, weapons systems add-ons, medical devices, and infrastructure directly from digital models. This revolutionary production methodology allows for armed forces to make complex, tailored components in situ on demand, reduces costs and lead times, saving, leading to a marked reduction of reliance on conventional supply chains and facilitating immediate response in peacetime and combat settings alike.

The technology encompasses the entire product life cycle in military operations, from original design and quick prototyping to field sustainment and battle damage repair. More than 90% of current military users intend to increase their additive manufacturing capabilities, demonstrating the strategic significance this technology provides for defense organizations across the globe.

The global military 3D printing market development stage, exhibiting strong growth fueled by an underlying transformation in defense procurement and operational strategy. Defense modernization initiatives are the key driver of market growth. Governments globally are making significant investments in additive manufacturing to decrease reliance on time-consuming procurement cycles and improve operational responsiveness.

The competitive landscape in the military 3D printing space includes a heterogeneous set of mature additive manufacturing OEMs, defense contractors with specialized capabilities, and technology disruptors. The key players of major size include the likes of Stratasys Ltd.(Israel), 3D Systems Corporation (U.S.), EOS GmbH (Germany), GE Additive (U.S.), Renishaw plc (U.K.), and so forth, among others.

Download Free sample to learn more about this report.

MILITARY 3D PRINTING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 4.07 billion

- 2026 Market Size: USD 5.15 billion

- 2034 Forecast Market Size: USD 20.76 billion

- CAGR: 19.05% from 2026–2034

- North America dominated the market with a 42.02% share in 2025.

- The Metals & Alloys segment is expected to hold the largest market share of 51.95% in 2026.

- The Stereolithography (SLA) segment is expected to hold the largest market share of 32.64% in 2026.

North America

The market reached USD 1.71 billion in 2025 and is projected to grow to USD 2.20 billion in 2026.

Europe

The market reached USD 1.01 billion in 2025 and is projected to grow to USD 1.28 billion in 2026.

Asia Pacific

The market reached USD 0.75 billion in 2025 and is projected to grow to USD 0.94 billion in 2026.

U.S.

The market is projected to reach USD 1.97 billion by 2026.

Japan

The market is projected to reach USD 0.15 billion by 2026.

Read More

Market Dynamics

Market Driver

Growing On-Demand Manufacturing Capability, Defense Modernization, and Strategic Capability Enhancement Fuel Product Demand

Defense modernization initiatives are the main driver behind additive manufacturing uptake in military organizations worldwide. World defense expenditures remain on an upward curve as the great game of geopolitics and localized unrest drives the need for superior manufacturing capabilities. European NATO member states are fast boosting defense spending to counter local security issues, and defense investment in technology and regional innovation is experiencing record growth rates as venture capital finds its way into low-cost air defense systems and improved system development, thereby driving military 3D printing market growth.

The fiscal year 2024 US Air Force budget request came to around USD 215.1 billion, an increase of USD 9.3 billion compared to fiscal year 2023, with large parts dedicated to technologies such as additive manufacturing for aircraft upgrade and retrofit programs. Computer-based inventory models substitute for physical inventories with parts fabricated on demand from secure digital data sent electronically to local, district, or on-location additive manufacturing systems.

- For instance, in February of 2024, the U.S. Navy launched the Naval Aviation School for Additive Manufacturing program, a six-week training initiative offering active-duty Navy and Marine Corps maintenance personnel additive manufacturing basics, with the Institute for Advanced Learning and Research hosting training to prepare deployed technology users and maximize operational capability.

Market Restraint

Quality Assurance, Cybersecurity Vulnerabilities, and Intellectual Property Protection Can Hamper the Market

Quality control and standardization shortcomings account for the most important challenge limiting extensive military three-dimensional printing use. Ascertaining that additively produced parts made on austere desert forward operating bases exhibit the same performance traits as laboratory-manufactured analogues necessitates stringent test protocols and thorough validating processes currently devoid of international harmonization.

Digital file dependency intrinsic to additive manufacturing processes poses serious cybersecurity risks to military operational security. All print-ready components start as a digital design file, making the entire additive manufacturing process vulnerable to cyber-attacks, including unauthorized alteration, introducing structural flaws, intellectual property theft via file exfiltration, or intentional corruption, debilitating critical equipment performance.

Regulatory compliance issues add to the complexities of cybersecurity issues, especially related to International Traffic in Arms Regulations and Department of Defense Instruction mandates for defense contractors dealing with sensitive technical information. Customers seeking certified secure manufacturing offerings have providers such as Stratasys Direct available to supply Cybersecurity Maturity Model Certification-compliant, International Traffic in Arms Regulations-registered processes specifically tailored for defense and aerospace uses.

Market Opportunity

Increasing Adoption of Artificial Intelligence and Autonomous Manufacturing To Drive New Market Opportunities

Artificial intelligence convergence with additive manufacturing technologies brings transformative potential to military applications throughout the entire cycle of production. Generative artificial intelligence algorithms will fast-track huge design possibility spaces, heavily compressing development timelines by automatically determining best geometries for weight savings, structural performance, and material efficiency. Real-time quality control systems infused with artificial intelligence will track manufacturing processes with unprecedented complexity, facilitating instant defect detection and correction of process parameters during build and not post-production inspection.

Over the next five years, completely autonomous manufacturing cells that can endure production in remote or contested zones without human operation will become a reality, revolutionizing forward-deployed manufacturing capabilities. For instance, in October 2025, research highlighted that artificial intelligence enhances military three-dimensional printing capability by allowing more intelligent design optimization, predictive scheduling of maintenance, and production process improvement, with artificial intelligence-driven algorithms simulating combat scenarios to improve prototypes prior to actual manufacture, while machine learning models optimize supply chain planning by predicting spare part requirements accurately.

Moreover, predictive maintenance software is an especially strong prospect, with machine fault forecasts generated by artificial intelligence software and enabling prescriptive three-dimensional printing of replacement parts in advance of disastrous breakdowns. Sustained artificial intelligence-based quality control systems identify production defects in real time during production operations, minimizing material losses and guaranteeing mission-relevant reliability for combat components.

Military 3D Printing Market Trend

Increasing Multi-Material and Composite Additive Manufacturing Are Fueling New Emerging Trends

Multi-material and composite three-dimensional printing technologies are key technological frontiers that extend military additive manufacturing capabilities beyond single-material limitations. Composite materials that contain carbon fiber, aramid, and glass fiber reinforcement in thermoplastic matrices provide better mechanical properties, such as increased resistance, minimum weight, and metal replacement capability for use in defense. Swiss producer 9T Labs created Additive Fusion Technology for depositing continuous carbon fibers into polymer matrices with automated, controlled processes using the Red Series, including the Build Module print unit and Fusion Module post-processing machine, wherein the three-dimensional printer is able to deposit continuous fibers as per operator-defined orientations and routes to minimize component weight, cost, and solidity.

For instance, in September 2025 analysis pointed out that Impossible Objects, an American company, created CBAM 25, a three-dimensional printing technology specifically for composite materials, being the latest in the composite additive manufacturing field. Additionally, in February 2025, research was able to successfully achieve formulation and manufacturing of gun propellants through Fused Deposition Modeling technology with high energetic content thermoplastic composites, which adds new applications to defense-specific material development.

Multi-material printing technology allows a single build session to include diverse material types with different properties, allowing for the formation of parts with spatially optimized properties such as rigid structural areas blended with flexible interfaces or conductive tracks embedded within insulating matrices.

High-performance composite three-dimensional printer systems by companies such as Continuous Composites utilize Continuous Fiber 3D technology, with the U.S. Air Force issuing multi-year, multi-million-dollar contracts in July of 2025 to support development of high-performance composite materials for aerospace use under two-phase programs showing potential for defense industry deployment.

Download Free sample to learn more about this report.

Market Challenges

The Workforce Development and Skills Gap Can Hinder the Market Growth

Workforce development shortfalls are a key challenge that limits military additive manufacturing adoption speed and operational capabilities. Design for Additive Manufacturing capabilities necessitate advanced knowledge to maximize component geometries for layer-by-layer manufacturing, taking advantage of special capabilities such as topology optimization, lattice structure integration, and conformal cooling channels that traditional manufacturing cannot provide.

Running metal additive manufacturing equipment requires technical proficiency involving process parameter choice, material science background, powder handling protocol, inert atmosphere control, and quality control protocol application capabilities far removed from traditional machining or fabrication skills. Advanced system maintenance and troubleshooting require continued training investments as hardware improves and new capabilities become available, with worker development issues remaining across design, operation, and maintenance areas.

For instance, in May 2024, analysis highlighted that as additive manufacturing technology is still progressing, there is a growing gap between sophisticated solutions and qualified professionals who can work with them, with uneven workforce development and shortages in industry-endorsed evidence of workforce-ready additive manufacturing capabilities generating increased demands for very skilled labor in key roles within the defense sector.

Segmentation Analysis

By Component

Growing Need for Seamless Software for Various Component Applications Catalyzes the Segmental Growth

The market is segmented by component is further divided into hardware, software, and services.

The software sub-segment is estimated to be the fastest-growing during the forecast period of 2026-2034 with the highest CAGR of 25.2%, due to mounting demand for sophisticated digital workflows, artificial intelligence-based design optimization, topology optimization capabilities, layers of cybersecurity, and built-in manufacturing execution systems. Software provides the digital bedrock for defense additive processes, transforming computer-aided design outputs into printable form while maintaining strict military standards through print path optimization, performance analysis incorporated in structural simulation, and topology optimization algorithms that progressively minimize component weight without compromising functional integrity.

- For instance, in September 2025 witnessed 3D Systems witnessed a strategic software emphasis on its in-house 3D Sprint polymer solution with the use of artificial intelligence and machine learning models based on insights from the industry's biggest installed base of production printers, as it sold its Oqton Manufacturing Operating System and 3DXpert metal printing platforms intended for printer-agnostic industry adoption.

In 2026, the hardware segment is projected to lead the market with a 50.34% share. The hardware sub-segment holds the largest military 3D printing market share, generating the highest market revenue of USD 1.69 billion during 2024, and is expected to maintain leadership status throughout the forecast period. Hardware in military additive manufacturing includes three-dimensional printers from field-deployable compact fused deposition modeling systems that are mounted in protective transport cases to large industrial powder bed fusion systems and directed energy deposition systems that can fabricate functional metal parts weighing several tonnes.

By Material Type

Increasing Adoption of Ceramics for Different Uses Catalyzes the Segmental Growth

The market is segmented by material type into metals & alloys, polymers & plastics, ceramics, composites, and others.

The ceramics sub-segment is projected to be the fastest growing during the forecast period, with the highest CAGR of 25.6% during 2026-2034. The growth is driven by the aerospace and defense industry market demand owing to the growing requirement for high-performance, lightweight, and high-temperature-resistant components with the ability to withstand severe operating conditions. Ceramic materials possess high thermal stability in excess of 3000 degrees Celsius, superior corrosion resistance, and structural strength that makes them ideal for engineering applications such as thermal barrier coatings, turbine components, nozzles, radomes, and insulating components used in aircraft and space vehicles.

- For instance, in February 2025 saw Purdue Applied Research Institute scientists pushed the boundary in hypersonic production by creating new additive manufacturing process techniques for three-dimensionally printing dark ceramics into intricate structures for components of hypersonic vehicles, with materials strong enough to withstand extreme conditions of hypersonic flight while allowing scaled production to enhance efficiency and performance.

The metals and alloys segment is projected to dominate the market with a share of 51.95% in 2026. The metals and alloys segment holds a leading position in the global military 3D printing market with valued at USD 1.63 billion in 2024, and registering the highest revenue share, and is expected to maintain market dominance throughout the forecast period. Defense applications that are significant demand drivers are seeking cost-effective, high-performance production methods for complex geometries, lightweight structures, and customized components that traditional manufacturing cannot easily deliver. Alpha plus beta titanium alloys offer maximum balance of toughness, fatigue life, and strength, with the aerospace sector being one of the biggest consumers, thereby driving the market. Growth is fueled by increasing demand for thermal protection systems for hypersonic vehicles, ballistic armor uses, and high-temperature aerospace parts with capabilities to resist harsh operating conditions.

By Technology

Increasing Printing Speed and Widespread Material Capability Fuels Binder Jetting Segmental Growth

The market is segmented by technology into stereolithography (SLA), fused deposition modeling (FDM), direct metal laser sintering (DMLS), electron beam melting (EBM), binder jetting, and others.

The binder jetting sub-segment is accelerated with the highest compound annual growth rate of 27.0% during the forecast period of 2026-2034. The growth is attributed to the unparalleled printing speed, widespread material capability from metals to ceramics, and mitigation of thermal stresses, allowing complex geometries without support. The market for binder jetting three-dimensional printing technology is shown to exhibit significant growth. Binder jetting works by selectively depositing liquid binding agents onto layers of powder beds to fabricate three-dimensional products at room temperature, being fundamentally distinct from powder bed fusion processes that utilize high-energy lasers with considerable thermal stresses and material waste.

- For instance, in October 2025 witnessed Continuum Powders and HP jointly announced a partnership to qualify M247LC, a low-carbon nickel-based super alloy designed for high-temperature strength, as well as corrosion resistance specifically for aerospace and defense applications using metal binder jetting, placing binder jetting in the role of a production-capable solution for applications where performance and reliability become non-negotiable.

The Stereolithography segment is expected to lead the market, contributing 32.64% globally in 2026. Stereolithography retains a dominating market share with a value of USD 1.03 billion in the military 3D printing market, holding the highest market share due to its unrivaled precision capability, high quality of surface finish, and widespread use in aerospace and defense rapid prototyping processes. Military institutions find stereolithography essential for manufacturing complex designs that need absolute precision, such as functional prototypes, tooling, jigs, fixtures, mission-specific equipment enclosures, and specialized parts for unmanned aerial vehicles, where shape, fit, and assembly verification are vital prior to investing in costly metal production runs.

By Application

Escalating the On-Demand for Logistics Resilience Fueling the MRO Segmental Growth

The market is segmented by application into tooling, end-use part production, research & development, and maintenance, repair, & overhaul (MRO).

The maintenance, repair, & overhaul (MRO) sub-segment is estimated to be the fastest growing during the forecast period with the highest CAGR of 25.6%. The growth is driven by its key function in maintaining fleet readiness and supply chain responsiveness. Units forward-deployed are now utilizing additive manufacturing to create critical spare parts—including hydraulic fittings, sensor enclosures, and structural brackets—in hours instead of months waiting for the traditional procurement method, cutting aircraft and ship downtime by a considerable margin.

- For instance, in August 2025, San Diego-area defense contractors proved this capability during exercise Trident Mauka by 3D printing spare parts for CH-53E helicopters on board the USS Essex, producing airworthy parts in less than 48 hours and confirming at-sea maintenance feasibility.

The Prototyping segment will account for 24.45% market share in 2026. The Prototyping sub-segment holds the largest share in the military 3D printing market by utilizing additive manufacturing's ability to speed up design-iterate-test cycles of weapons systems, unmanned platforms, and support gear. Rapid prototyping allows defense engineers to confirm form, fit, and function of new parts, everything from unmanned aerial vehicle fairings to turret mounts, within days compared to months needed with conventional tooling. Stereolithography accuracy and surface finish make it the go-to prototyping technique for complex assemblies that need minimal post-processing, humming along behind 45 percent of all military-sourced prototyping applications worldwide.

By Platform

Growing Defense Forces’ Strategic Shift to Unmanned and Manned Systems Fuels UAVs/UGVs/UUVs Segment Growth

The market is segmented by platform into armored vehicles, ground equipment, fighter jets, helicopters, UAVs/UGVs/UUVs, warships, and military satellites.

The UAVs/UGVs/UUVs sub-segment is projected to be the fastest growing during the forecast period for 2026-2034, with the highest CAGR of 25.6%. The segment holds the value of USD 0.53 billion in 2024. The growth is driven by defense forces' strategic transition to unmanned and optionally manned systems demanding rapid, lightweight, and mission-specific components. Additive manufacturing allows the on-demand manufacture of complex airframes, sensor enclosures, and propulsion ducting for unmanned aerial vehicles, with support for ground and underwater variants through customized chassis components and pressure-resistant housings.

- For instance, in July 2025, Stratasys showcased a forward-deployed stereolithography supply chain for printing UAV fuselage sections during Exercise Falcon Eye, cutting prototype cycle times from eight weeks to less than five days and allowing real-time design iterations at remote air bases.

The armored vehicles sub-segment commands the military 3D printing market, as there is high investment in maintaining and modernizing ground combat platforms. Additive manufacturing delivers essential spare and upgrade components such as turret parts, drive sprockets, and hull reinforcement for main battle tanks and infantry fighting vehicles, lowering depot turnaround time and minimizing operational downtime. For instance, in October 2024, the U.S. Army showcased 3D printing of a key M1 Abrams track idler guard at the Joint Readiness Training Center, printing and installing the component successfully in 72 hours in combat rotation conditions, emphasizing additive manufacturing's potential for sustaining armored vehicle fleets at the tactical forefront.

To know how our report can help streamline your business, Speak to Analyst

By End User

Rising Embedding Additive Manufacturing Capabilities Led to Defense OEMs Segmental Growth

The market is segmented by end user into the army, navy, air force, defense OEMs, and research & testing institutions.

The defense OEMs sub-segment is projected to be the fastest growing, with the highest compounding rate of 24.1% during the forecast period. The growth is accelerated by closely embedding additive manufacturing capabilities within fundamental design and manufacturing processes, allowing original equipment manufacturers to simplify part qualification, minimize supply chain dependencies, and speed technology maturation. Lockheed Martin's November 2024 expansion of its Grand Prairie, Texas, additive manufacturing facility added 16,000 square feet of cutting-edge production space featuring large-format laser powder bed fusion systems and rapid heat-treatment ovens to support digital design-to-production pipelines that reduce lead times for key missile and fire-control components by as much as 60 percent. This investment supports the company's Model-Based Enterprise program, which infuses three-dimensional digital thread artifacts across the product lifecycle to provide traceability, increase quality control, and streamline supplier integration, delivering uniform AM outputs across geographically dispersed production locations.

- For instance, in May 2025, BAE Systems also entered into a Memorandum of Understanding with Renishaw to co-develop next-generation metal additive manufacturing process technology for use in future combat aircraft, a demonstration of OEMs' support for co-funded research and development, materials qualification, and full-rate production readiness.

Air for sub-segment is accounted for the largest market share in the global market, and the dominance is driven by ambitious depot modernization initiatives and strategic investments in internal sustainment capabilities. The Air Force Sustainment Center's "Complex of the Future" program combines predictive maintenance, data analysis, and forward repair nodes with fused deposition modeling and selective laser sintering equipment that allows maintainers to print on demand mission-critical electronic housings, harsh-environment engine seals, and flight-control linkages. For instance, in September 2025, Tinker AFB reported successful printing of a TF33 engine anti-ice gasket via metal laser powder bed fusion, the first additively manufactured metal engine part qualified for Air Force service and reflecting depot-level AM's strategic importance to turbine sustainment.

Military 3D Printing Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Military 3D Printing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 1.71 billion in 2025, representing 42.02% of the global industry, and is expected to reach USD 2.2 billion in 2026. The region continues to dominate the market with a valued USD 2.2 billion and is projected to reach by 2032 at valued 7.91 billion. In addition, the region is projected to be the fastest growing with a compound annual growth rate of 24.5% during the forecast period of 2026-2034.

The dominance is led by the high defense expenditures of the U.S. and Canada, established industrial ecosystems, and early mover advantage in adopting additive manufacturing technologies for use across all branches of their militaries. Key OEMs such as Lockheed Martin, Boeing Defense, and Northrop Grumman have additive manufacturing facilities within the region, facilitating secure digital threads from design to production. For instance, in November 2024, the Defense Logistics Agency issued its first competitive additive manufacturing contract for F-15 pylon bumpers manufactured through binder jetting, representing a critical shift toward competitive procurement and further enhancing North America's market leadership.

The U.S. Department of Defense invested USD 800 million in additive manufacturing activities in 2024, up by a whopping 166% from the previous year, with the North American defense agencies incorporating AM into sustainment, prototyping, and on-demand spare parts manufacturing processes. Factories, namely Tinker Air Force Base's Oklahoma City Air Logistics Complex, have transformed updated depots into "Complexes of the Future," integrating laser powder bed fusion, directed energy deposition, and polymer AM technology inside repair hangars to produce mission-critical parts in-house. The U.S. market is projected to reach USD 1.97 billion by 2026.

Europe

Europe recorded a market size of USD 1.01 billion in 2025, capturing 24.84% of the global market share, and is projected to reach USD 1.28 billion in 2026. Europe is estimated to be the second fastest-growing region during the forecast period, driven by aggressive defense modernization initiatives, enhanced R&D partnerships, and localization drives across NATO nations. The U.K. Ministry of Defense unveiled a Defense Advanced 3d Manufacturing Strategy in March 2025, targeting GBP 110 million in savings through strategic adoption of AM across the supply chain and demonstrating that Spiral 1 of Project TAMPA successfully printed safety-critical components meeting NATO standards.

European defense manufacturers such as BAE Systems, Airbus, and Dassault Aviation have set up separate additive manufacturing departments, qualifying metal and polymer components for combat aircraft, naval ships, and land vehicles. BAE Systems and Renishaw collaborated in July 2025 to create future DMLS processes for the next generation of combat aircraft structures, demonstrating Europe's dedication to co-funded innovation and sovereign manufacturing capability. The UK market is projected to reach USD 0.38 billion by 2026, while the Germany market is projected to reach USD 0.29 billion by 2026.

Asia Pacific

In 2025, Asia Pacific represented USD 0.75 billion, accounting for 18.38% of the worldwide market, and is projected to grow to USD 0.94 billion in 2026. The Asia Pacific market is significantly growing, fueled by rising defense spending in India, China, South Korea, Japan, and Australia, as well as by government efforts to indigenize military industrial capacity. India's Army led high-altitude field construction with three-dimensional printing of its first defensive military facility at 11,000 feet in Leh in April 2025, demonstrating AM's capabilities for expeditionary infrastructure in hostile environments and conforming to Strategic Partnership Models under Make in India policies. China's People's Liberation Army has incorporated portable AM labs for drone repair and uncommon vehicle repair, while South Korea's Defense Acquisition Program Administration initiated its inaugural metal AM qualification program for the KF-21 fighter jet parts in June 2025. Regional OEM collaborations with technology vendors expedite material qualification and process standardization to facilitate fast fleet modernization in the Asia Pacific. The Japan market is projected to reach USD 0.15 billion by 2026, the China market is projected to reach USD 0.31 billion by 2026, and the India market is projected to reach USD 0.17 billion by 2026.

Middle East & Africa

Middle East & Africa contributed 9.88% to the global market in 2025, with a valuation of USD 0.4 billion, and is projected to reach USD 0.49 billion in 2026. Middle East & Africa and Latin America show moderate growth powered by selective defense modernization, joint ventures with international OEMs, and investments in infrastructure with a view to increasing localized manufacturing. In September 2025, Saudi Arabia's National Additive Manufacturing and Innovation Company (NAMI) entered into an agreement with Lockheed Martin to qualify and produce additively manufactured aluminum aerospace parts in the Kingdom, in accordance with Vision 2030's emphasis on localization of the defense industry and technology transfer.

Latin America

The Latin America market was valued at USD 0.2 billion in 2025, capturing 4.88% of global revenue, and is estimated to reach USD 0.24 billion in 2026. Latin American militaries are implementing AM pilot projects. Nigeria's military launched a polymer AM facility for producing spare parts in May 2025, and Brazil's navy deployed an AM team on Amazon patrol boats in August 2025 to produce mission-critical equipment in situ, highlighting a slow-moving trend toward distributed manufacturing capabilities. These efforts place both regions in ongoing, but modest, additive manufacturing adoption as part of more general defense modernization efforts.

COMPETITIVE LANDSCAPE

Key Market Players

Growing Innovations and Adoption of 3D Print Components by Defense OEMs Hold Intense Competitions

The military 3D printing market's competitive environment features consolidation patterns, strategic alliance creations, and hostile technology portfolio build-outs as incumbent original military equipment makers and dedicated additive manufacturing firms position themselves to gain share of growing defense procurement budgets. In December 2024, Ex-CEO Yoav Stern announced, symbolizing Nano Dimension's promise to disciplined capital management, margin enhancement through operational improvements, and prioritization of resources to revenue-generating opportunities instead of pursuing the previous administration's aggressive merger and acquisition approach, criticized by activist shareholder Murchinson Ltd. This consolidation move follows a larger industry trend where the three-dimensional printing industry saw record merger offers during 2023, including 3D Systems.

Defense original equipment manufacturers are showcasing aggressive vertical integration practices, integrating additive manufacturing capabilities into design-to-production processes in order to eliminate supply chain dependencies and shorten qualification timelines. This trend toward vertical integration goes beyond aerospace primes to include naval and ground vehicle manufacturers increasingly opening in-house additive manufacturing facilities to keep intellectual property within secure environments, preserve sovereign control over proprietary warfighter systems, and create closed-loop feedback between design engineers and production operators to permit rapid iteration on complex geometries and topology-optimized structures.

For instance, in September 2025, Saudi Arabia's National Additive Manufacturing and Innovation Company collaborated with Lockheed Martin to qualify and manufacture additively produced aluminum aerospace parts in the Kingdom, demonstrating Vision 2030's localization of the defense industry thrust while bringing diversified supply base benefits to Lockheed Martin.

In addition, BAE Systems keeps pushing additive manufacturing forward with its Factory of the Future program that includes Renishaw metal three-dimensional printing equipment to produce production-grade parts for Typhoon fighter jets while enabling fast prototyping for Tempest next-generation combat air vehicles. In May 2025, the Memorandum of Understanding with Renishaw established cooperative development of next-generation processes for future combat planes. 3D printing technology specialization strategies foster unique competitive positioning, with firms seeking specialized capabilities in a particular additive manufacturing process versus diversified portfolio strategies.

For instance, in October 2025, Velo3D revealed increased partnership with iRocket, a next-generation aerospace firm working on one hundred percent reusable launch vehicles, whereupon iRocket purchased Velo3D Sapphire printers and Rapid Production Solutions to increase U.S.-based production of space and defense propulsion and structural components, with Velo3D's support-free metal printing proving especially useful for intricate propulsion system geometries conventional approaches cannot produce.

List of Key Military 3D Printing Market Company Profiles

- 3D Systems Corporation (U.S.)

- Divergent Technologies (U.S.)

- DM3D Technologies (U.S.)

- Elimold (China)

- EOS GmbH (Germany)

- GE Additive (Colibrium Additive) (U.S.)

- Lockheed Martin Corporation (U.S.)

- Markforged Holding Corporation (U.S.)

- Materialise NV (Belgium)

- Renishaw plc (U.K.)

- Sciaky, Inc. (U.S.)

- Solid Concepts, Inc. (U.S.)

- SPEE3D (Australia)

- Stratasys Ltd. (U.S.)

- UltiMaker (Netherlands)

- Zortrax S.A. (Poland)

KEY INDUSTRY DEVELOPMENTS

- In September 2025, SOGECLAIR purchased an AddUp FormUp 350 metal 3D printing press for their Toulouse base, expanding on their 2016 PRINTSKY partnership to speed industrial adoption of metal additive manufacturing for future-generation aircraft thermal components and key aerospace systems.

- In August 2025, the Royal Australian Navy deployed its first prototype Deployable Additive Manufacturing and Repair Capability (DAMR) housed in a shipping container near Gladstone during Exercise Talisman Sabre 2025, featuring three 3D printers, including Prusa Core One, Ultimaker Factor 4, and Markforged X7, for forward-deployed fabrication support.

- In June 2025, Velo3D joined a four-year Cooperative Research and Development Agreement with Fleet Readiness Center East and Naval Air Warfare Center Aircraft Division to define advanced materials and create applications for military flight hardware using Sapphire printer capability to satisfy demanding defense qualification standards.

- In July 2025, CRG Defense was the second U.S. company to purchase the ARGO 1000 HYPERMELT large-format 3D printer from Italian robot maker Roboze, boosting the ability to create aerospace-grade polymer and composite components at high volume while assisting in a USD 2.5 million U.S. Air Force contract for development of ultra-high-temperature 3D printing systems.

- In July 2025, Synergy Additive Manufacturing was awarded a Phase I Small Business Innovation Research (SBIR) contract by the Naval Air Systems Command to develop Extremely High-Speed Laser Cladding technology for improving titanium cylinder bores in helicopter parts to extend part life, save money, and cut maintenance downtime for U.S. Navy aerospace uses.

REPORT COVERAGE

The global military 3D printing market analysis provides an in-depth study of the market size & forecast by all the market segments included in the military 3D printing market report. It includes details on the global military 3D printing market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 19.05% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Component · Hardware · Software · Services By Material Type · Metals & Alloys · Polymers & Plastics · Ceramics · Composites · Others By Technology · Stereolithography (SLA) · Selective Laser Sintering (SLS) · Fused Deposition Modeling (FDM) · Direct Metal Laser Sintering (DMLS) · Electron Beam Melting (EBM) · Binder Jetting · Others By Application · Prototyping · Tooling · End-use Part Production · Research & Development · Maintenance, Repair, & Overhaul (MRO) By Platform · Armored Vehicles · Ground Equipment · Fighter Jets · Helicopters · UAVs/UGVs/UUVs · Warships · Military Satellites By End User · Army · Navy · Air Force · Defense OEMs · Research & Testing Institutions By Regionally North America (By Component, By Material Type, By Technology, By Application, By Platform, By End User, By Country) · U.S. (By End User) · Canada (By End User) Europe (By Component, By Material Type, By Technology, By Application, By Platform, By End User, By Country) · U.K. (By End User) · Germany (By End User) · France (By End User) · Italy (By End User) · Nordic Countries (By End User) · Rest of Europe (By End User) Asia Pacific (By Component, By Material Type, By Technology, By Application, By Platform, By End User, By Country) · China (By End User) · Japan (By End User) · South Korea (By End User) · India (By End User) · Australia (By End User) · Southeast Asia (By End User) · Rest of Asia Pacific (By End User) Middle East & Africa (By Component, By Material Type, By Technology, By Application, By Platform, By End User, By Country) · Saudi Arabia (By End User) · UAE (By End User) · Israel (By End User) · Iran (By End User) · South Africa (By End User) · Rest of Middle East & Africa (By End User) Latin America (By Component, By Material Type, By Technology, By Application, By Platform, By End User, By Country) · Brazil (By End User) · Mexico (By End User) · Argentina (By End User) · Rest of Latin America (By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.15 billion in 2026 and is projected to reach USD 20.76 billion by 2034.

In 2025, the market value stood at USD 1.71 billion.

The market is expected to exhibit a CAGR of 19.05% during the forecast period of 2026-2034.

The Maintenance, Repair, & Overhaul (MRO) sub-segment is expected to hold the highest CAGR over the forecast period.

The Growing On-Demand Manufacturing Capability, Defense Modernization, and Strategic Capability Enhancement Drives the Military 3D Printing Market Growth.

Divergent Technologies (U.S.), DM3D Technologies (U.S.), Elimold (China), EOS GmbH (Germany), and others are top players in the market.

North America dominated the global market with a share of 42.02% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 161

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us