Military Transport Aircraft Market Size, Share & Industry Analysis, By Type (Fixed-Wing and Rotary Wing), By Application (Troop Transport, Equipment & Cargo Transport, Medical Evacuation, Multi-Role, and Surveillance & Reconnaissance), By Systems (Systems Airframe, Engine, Avionics, Landing Gear System, and Weapon System), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

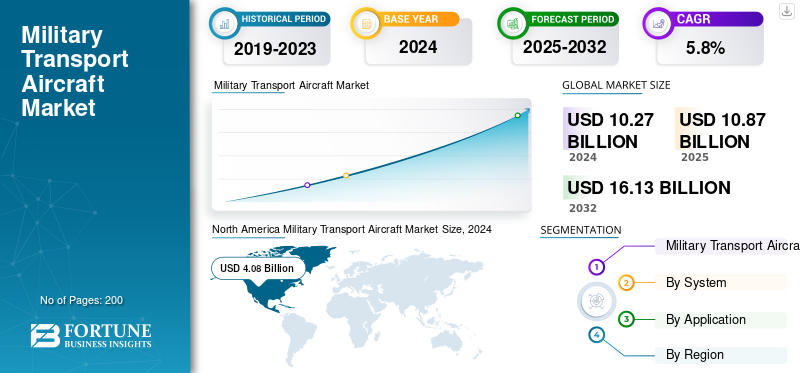

The global military transport aircraft market size was valued at USD 10.27 billion in 2024 and is projected to grow from USD 10.87 billion in 2025 to USD 16.13 billion by 2032, exhibiting a CAGR of 5.8% during the forecast period. North America dominated the global market with a share of 39.73% in 2024.

Military transport aircraft are specialized aircraft owned by the military, designed to carry troops, equipment, and supplies. They play a crucial role in military operations and humanitarian aid. These aircraft can be used for both strategic and tactical missions, enabling the movement of personnel and materials to various locations, including areas with limited ground or water access. The modernization of aging strategic airlift fleets, increased demand for multi-role capabilities, and rising defense spending, particularly in the Asia Pacific region, are driving the market growth.

Major market players are Airbus, Lockheed Martin, and Dassault Aviation, among others. Each offering specialized military transport aircraft designed for efficient carrying of troops, equipment, and supplies during military operations. These companies emphasize reliability, innovation, and environmental sustainability in their products to meet the evolving needs of the military sector. The market is experiencing growth due to factors such as the need to replace aging fleets, the rise in global defense spending, and the expansion of military operations in challenging environments.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Need for Strategic Mobility and Rapid Deployment of Troops and Equipment by Armed Forces Drives Market Growth

Military transport aircraft are essential for moving troops, equipment, and supplies quickly to operational areas, providing a crucial advantage in responding to crises and conflicts. The need for rapid force projection is a major factor driving demand for advanced transport aircraft with long-range capabilities. Additionally, increasing geopolitical tensions and conflicts globally are leading to increased military spending and the modernization of armed forces, further fueling military transport aircraft market growth.

- For instance, in December 2021, Ukrainian aircraft manufacturer Antonov State Enterprise (part of Ukroboronprom) introduced the country’s An-178-100R military aircraft to transport weapons, personnel, and light military equipment.

Increasing Global Defense Expenditure and Rising Geopolitical Tensions, Leading to a Surge in Demand for Advanced Military Platforms

Global military expenditure reached a record high in 2022, with the U.S., China, Russia, India, and Saudi Arabia accounting for the majority of the spending. This increase is driven by factors such as the Russia-Ukraine conflict, the Israel-Hamas conflict, and escalating tensions in the South China Sea.

- For instance, Germany plans to spend USD 761 billion on the military over the coming five years, in response to the Ukraine conflict. Similarly, countries in the Asia Pacific region are also increasing defense allocations due to China's growing assertiveness.

Market Restraints

High Development and Procurement Costs Restrain Market Growth

The development of advanced military transport aircraft requires substantial investment in research, development, and cutting-edge technologies. This leads to high procurement costs, which can be a barrier for many nations, especially emerging economies with budget limitations.

- For Instance, the new Airbus A400M Atlas has a unit cost of around USD 145 million, while a Boeing C-17 Globemaster III can cost around USD 218 million. The Lockheed Martin C-130J Super Hercules has a price of around USD 75.5 million.

Additionally, while initial acquisition costs are significant, the long-term operational, maintenance, and upgrade costs over the aircraft's lifecycle can be even more burdensome. These costs can strain defense budgets, especially for smaller or developing nations.

Market Opportunities

Increasing Demand for Multi-Role Capable Market to Provide Opportunity to Market Players

The need for multipurpose platforms that can handle various critical missions, including troop and cargo transport, medical evacuation (medevac), and other essential functions, is increasing demand for multi-role military transport aircraft. The evolving nature of modern warfare and peacekeeping operations, where adaptability is crucial, necessitates that nations strengthen their air force capabilities.

Demand for Heavy Lift Transport Aircraft is Increasing, Which Plays a Crucial Role During Conflicts and War

The increasing demand for transporting heavy military equipment such as battle tanks, aerial vehicles, UAV, and other vehicles necessitates aircraft with significantly higher payload capacities. This is particularly crucial for operations in challenging terrains where ground transport is difficult or impossible. Future conflicts are anticipated to require rapid deployment and supply chain of forces, emphasizing the need for robust airlifters.

- For instance, in November 2024, the Indian Air Force (IAF) contracted Airbus Defense and Space for the acquisition of 56 C-295MW transport aircraft.

Military Transport Aircraft Market Trends

Modernization of Military Fleets and Technological Advances in Aircraft Capabilities Fuels Market Growth

Modernization efforts include upgrades to existing aircraft and the development of new, more capable transport aircraft. Advanced features such as enhanced avionics, communication systems, and cargo handling capabilities are being incorporated into new aircraft. Moreover, increased defense budgets in various countries are fueling investments in military transport aircraft. Countries are also seeking to modernize their military fleets, replacing older aircraft with newer and more advanced models.

- For instance, in June 2025, the U.S. DOD awarded Lockheed Martin to support the avionics modernization program of the U.S. Air Force's C-5M Super Galaxy transport aircraft fleet.

Impact of Russia-Ukraine War

Russia-Ukraine War-Driven Surge in Strategic and Tactical Airlift Is Reshaping Market

The Russia-Ukraine war has turned strategic airlifts into a constant logistics backbone for NATO and its partners, and this change is reshaping the market. Large amounts of ammunition, armor, air-defense systems, and humanitarian aid have pushed C-17, C-130J, A400M, and chartered fleets into heavy use. This has revealed long-standing gaps in European and allied airlift capacity. The pressure is speeding up fleet renewal, retiring older C-130Hs, Transalls, and An-series platforms. It also expands multinational airlift cooperation and increases interest in newer aircraft such as the A400M and C-390. At the same time, sanctions and battlefield losses have disrupted the Russian-Ukrainian aerospace supply chain. The result is a market where procurement timelines are becoming shorter. Airlift, especially strategic airlifts, is now witnessed as a vital capability instead of a secondary support function.

- For instance, at ILA 2024, Janes reported that the increased use of Lockheed Martin C-130 Hercules for Ukrainian resupply missions has directly sped up European C-130 renewal plans. Several operators are fast-tracking upgrades or replacements in response to the operational surge caused by the war.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Fixed Wing Segment Ruled Global Market Due to Significant Deliveries in Recent Years

The market is divided by type into fixed wing and rotary wing.

Fixed-wing aircraft type, including both jet-powered and propeller-driven types, hold a large share of the market due to their capability for long-distance travel and the ongoing technological advances in their design and modernization. Additionally, increased defense spending and the modernization of air force fleets also drive fixed-wing aircraft demand.

- For instance, in July 2024, Australia plans to buy 20 new Lockheed Martin C-130J Hercules transport aircraft from the U.S. The deal is valued at approximately USD 6.6 billion, with the first delivery scheduled for 2027.

While fixed-wing aircraft type currently dominate the global military transport market due to large-scale deliveries, the rotary-wing segment is expected to experience the fastest growth. This growth is fueled by increasing demand for helicopters, particularly in Asia, the Middle East & Africa, and Eastern Europe, along with advancements in rotary-wing technology.

- For instance, the U.S. Initiatives such as Future Long-Range Assault Aircraft (FLRAA) and Future Attack Reconnaissance Aircraft (FARA) demonstrate the U.S. Army's focus on modernizing its rotary-wing capabilities.

By Application

Surveillance & Reconnaissance Dominate Market due to Critical Role in Border Security and Monitoring Illegal Activities

The application segment categorizes the market into troop transport, equipment & cargo transport, medical evacuation, multi-role, and surveillance & reconnaissance.

The multi-role segment holds the largest market share, and is anticipated to be the fastest growing segment during the forecast period with troop and cargo transport being significant contributors within that category. These aircraft, such as the C-17 Globemaster III, can handle a wide range of missions, including troop transport, cargo transport, medical evacuation, and even surveillance & reconnaissance. This adaptability makes them the first choice for militaries, driving their dominance in the market.

- For instance, in December 2023, South Korea selected the Embraer C-390 Millennium, a multi-role military transport aircraft as its new military transport aircraft, marking the first Asian customer for the aircraft. The contract includes the delivery of an undisclosed number of C-390s, along with comprehensive support and services.

The surveillance & reconnaissance segment holds the second largest share in the market. This category plays a vital role in maritime patrol, border security, and the monitoring of illegal activities. The growing demand for real-time data collection and analysis to support decision-making, along with increased government investments in maritime situational awareness, is further driving the growth of this segment.

To know how our report can help streamline your business, Speak to Analyst

By System

Ongoing Research and Development Efforts of Engine Systems drive Segment Growth

The market is segmented by systems airframe, engine, avionics, landing gear system, and weapon system.

The engine segment holds the largest market share. Segment dominance is attributed to the ongoing research and development efforts focused on enhancing engine efficiency and developing advanced propulsion systems such as hybrid engines. Furthermore, rising fuel prices are driving demand for more fuel-efficient engines, including those with hybrid technology.

- For instance, in October 2023, Honeywell announced it had received an order for 41 T55-GA-714A engines to support South Korea’s procurement of new CH-47F aircraft as part of an effort to replace its older CH-47D aircraft. The order and supply of the T55 engines is managed through the office of the U.S. Army Foreign Military Sales.

The avionics systems segment is anticipated to be the fastest-growing segment during the forecast period. Increasing complexity and functionality of the aircraft heavily depend upon the advanced avionics for critical missions such as surveillance and communication, resulting in segment fastest growth. Moreover, advancements in sensor technology, flight control systems, and advanced navigation & monitoring systems further drive the growth of the avionics segment.

Military Transport Aircraft Regional Outlook

Regionally, the market is studied across North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Military Transport Aircraft Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America holds the largest military transport aircraft market share. The U.S. military aviation market is heavily influenced by the country's substantial defense budget, which reached USD 849.8 billion in 2025. This robust spending fuels research, development, and procurement of new aircraft and technologies. Moreover, the U.S. is home to several major manufacturing companies specializing in military transport aircraft, such as Boeing and Lockheed Martin, among others.

Europe

The European market is projected to account for the second-largest share in the military transport aircraft sector throughout the forecast period. This growth is attributed to Europe’s strict regulatory standards, increasing defense spending, and modernization efforts across the region. Within the region, key players such as Germany, France, and the U.K. significantly drive this market forward. Meanwhile, Europe showcases a technological advances landscape that fosters new developments in military transport aircraft, all contributing to the overall momentum of the market.

Asia Pacific

The Asia Pacific region is anticipated to show the fastest growth, with the highest CAGR during the forecast period. Countries such as China and India are continuously modernizing their military capabilities. In addition, private players in the region are significantly investing in the defense sector, including military transport aircraft, equipment manufacturing, and assembly.

The Asia Pacific military aircraft modernization and retrofit market is also experiencing growth due to the need for interoperability, evolving mission requirements, and the obsolescence of older aircraft.

Rest of the World

The Middle East & Africa is anticipated to witness significant growth during the forecast period. Countries such as the UAE, Egypt, Saudi Arabia, Qatar, Israel, and other countries in the region's growth are driven by regional security concerns and modernization efforts. Countries are investing in new aircraft acquisitions and fleet upgrades to enhance their military transport capabilities.

Latin America is expected to experience noticeable growth during the forecast period. With Brazil being the dominant player in the region. While other countries are also actively involved in modernization and infrastructure development.

Competitive Landscape

Key Industry Players

Increasing Competition Leads to Evolution of Market in Aviation

The market is primarily characterized by a consolidated structure, dominated by a few key original equipment manufacturers (OEMs) that have a strong global presence. These OEMs are actively engaged in continuous product innovation, strategic expansion, and partnerships to address evolving military requirements. The market is driven by factors such as increasing defense budgets, geopolitical tensions, and the growing need for strategic airlift capabilities.

The market is also showing an increased demand for high-lift military transport aircraft solutions to enhance both efficiency and safety. The market faces challenges of volatile raw material prices and the requirement for ongoing compliance with the aviation industry. Key players such as Airbus, Boeing, and Lockheed Martin, among others, are continuously focused on research and development to improve various aspects of their aircraft, including avionics, propulsion systems, and stealth technology. This focus is driven by the need to enhance capabilities, operational agility, and mission flexibility in response to evolving military requirements.

LIST OF KEY MILITARY TRANSPORT AIRCRAFT COMPANIES PROFILED

- Lockheed Martin (U.S.)

- Boeing Defense, Space & Security (U.S.)

- Airbus Defense and Space (Germany)

- Embraer Defense & Security (Brazil)

- AVIC/Xi’an Aircraft Industrial Corporation (China)

- United Aircraft Corporation/Ilyushin (Russia)

- Leonardo S.p.A. (Italy)

- Kawasaki Heavy Industries (Japan)

- Antonov Company (Ukraine)

- Hindustan Aeronautics Limited (India)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Elbit Systems announced a USD 260 million contract from Airbus Defense and Space to supply J-MUSIC DIRCM self-protection systems for the German Air Force’s A400M fleet, to be installed over six years and aligned with a wider German A400M protection upgrade.

- December 2024: Embraer signed a contract to sell two C-390 Millennium multi-mission transports to an undisclosed customer, including training, support and spares, making that buyer the 10th country to select the C-390.

- July 2024: Austria and the Netherlands formalized the purchase of nine Embraer C-390 Millennium aircraft (four for Austria, five for the Netherlands), with deliveries scheduled from 2027–2030, representing the largest C-390 export deal to date.

- February 2024: Embraer Defense & Security and Mahindra signed a Memorandum of Understanding to jointly pursue the C-390 Millennium for the Indian Air Force’s Medium Transport Aircraft (MTA) programme, including localization and “Make in India” industrial plans.

- November 2022: The U.S. State Department approved a Foreign Military Sale to Australia of up to 24 C-130J-30 aircraft and related equipment, with an estimated cost of USD 6.35 billion, to recapitalize the RAAF tactical transport fleet.

- March 2022: Italy’s defense ministry and Slovenia signed a government-to-government contract for one C-27J Spartan tactical transport (plus support), giving Slovenia its first modern tactical airlifter under the bilateral G2G framework.

- November 2021: The Indonesian Ministry of Defense ordered two Airbus A400M multirole tanker/transport aircraft and signed a Letter of Intent for four additional A400Ms, expanding its heavy-lift and HADR capacity.

REPORT COVERAGE

The research report delivers a detailed analysis of the market and emphasizes key aspects such as key players, offerings, objects, and end-users of military transport aircrafts. Moreover, it deals with insights into market trends, competitive landscape, market competition, product pricing, regional analysis, market players, competition landscape, and the market status, and highlights key industry growth. In addition to the factors stated above, it encompasses several direct and indirect influences that have subsidized the sizing of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 5.8% from 2025 to 2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type · Fixed-Wing · Rotary Wing |

|

By Application · Troop Transport · Equipment & Cargo Transport · Medical Evacuation · Multi-Role · Surveillance & Reconnaissance |

|

|

By System · Airframe · Engine · Avionics · Landing Gear System · Weapon System |

|

|

By Region · North America (By Type, Application, Systems, and Country) o U.S. (By Type, By Application, By Systems) o Canada (By Type, By Application, By Systems) · Europe (By Type, Application, Systems, and Country) o U.K. (By Type, By Application, By Systems) o Germany (By Type, By Application, By Systems) o France (By Type, By Application, By Systems) o Italy (By Type, By Application, By Systems) o Russia (By Type, By Application, By Systems) o Rest of Europe (By Type, By Application, By Systems) · Asia Pacific (By Type, Application, Systems, and Country) o China (By Type, By Application, By Systems) o India (By Type, By Application, By Systems) o Japan (By Type, By Application, By Systems) o South Korea (By Type, By Application, By Systems) o Australia (By Type, By Application, By Systems) o Rest of the Asia Pacific (By Type, By Application, By Systems) · Rest of the World (By Type, Application, Systems, and Country) o Middle East & Africa (By Type, By Application, By Systems) o Latin America (By Type, By Application, By Systems) |

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 10.27 billion in 2024 and is anticipated to record a valuation of USD 16.13 billion by 2032.

The market will likely grow at a CAGR of 5.8% during the forecast period.

The top ten players in the industry are Airbus, Boeing, Lockheed Martin Corp., Embraer S.A., Antonov, HAL, Lockheed Martin, Rheinmetall AG, Ilyushin, and Kawasaki Heavy Industries, based on parameters such as services portfolio, regional presence, and industry experience.

Rotary-wing is the fastest-growing segment by type in the global market report for the period 2025-2032.

The need for strategic mobility and rapid deployment of troops and equipment by armed forces drives the market growth.

- 2019-2032

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us