Military Wearables Market Growth, Size, Share & Industry Analysis, By Wearable Type (Headwear, Eyewear, Wristwear, Hearables, and Bodywear), By Technology (Smart Textiles, Network and Connectivity Management, Exoskeleton, Vision & Surveillance, Communication & Computing Monitoring, Power and Energy Source, and Navigation), By End User (Land Forces, Naval Forces, and Air Forces), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

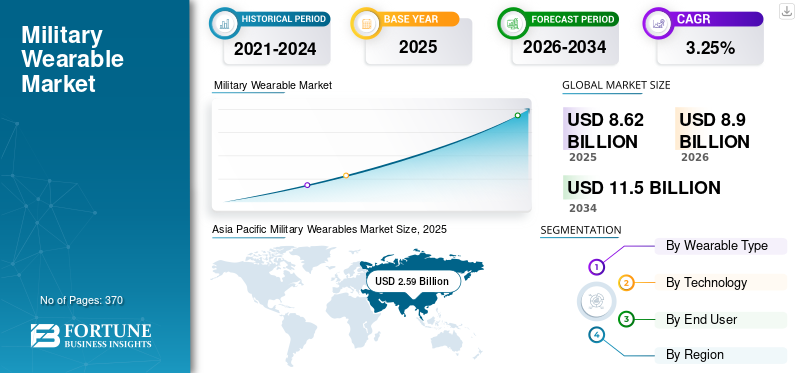

The global military wearable market size was valued at USD 8.62 billion in 2025. The market is projected to grow from USD 8.90 billion in 2026 to USD 11.50 billion by 2034, exhibiting a CAGR of 3.25% during the forecast period. Asia Pacific dominated the military wearable market with a market share of 29.99% in 2025.

Military wearables technology refers to electronic devices and equipment worn by soldiers or other military personnel as part of their uniforms or gear. These devices can include communication systems, navigation systems, various types of sensor systems, and different types of technology that can enhance soldiers' ability to perform their duties, boosting the military wearables market growth. Additionally, military wearables include smart watches, smart eyewear, heads-up displays, and exoskeletons. These devices can be connected to the internet, allowing soldiers to share information and coordinate with other unit members. Moreover, the increasing adoption of technology in wearables that incorporate advanced solutions can include a wide range of devices and systems such as Augmented Reality (AR), powered exoskeletons, biometric monitoring systems, smart clothing, and intelligent tactical systems, which aid the market growth in the forecast period.

Download Free sample to learn more about this report.

Military Wearables Market Overview & Key Metrics

Market Size & Forecast:

- 2025 Market Size: USD 8.62 billion

- 2026 Market Size: USD 8.9 billion

- 2034 Forecast Market Size: USD 11.5 billion

- CAGR: 3.25% from 2026–2034

Market Share:

- Asia Pacific dominated with 29.99% share in 2025 due to large armed forces and rapid adoption of advanced wearable technologies in China and India.

- By Wearable Type, bodywear held the largest market share; headwear is the fastest-growing segment due to AR/VR integrations and night vision systems.

- By Technology, communication & computing leads the market owing to battlefield connectivity demands, while vision & surveillance is the fastest-growing segment.

- By End User, land forces dominate due to heavy adoption of next-gen armor and wearable devices; air forces segment shows fastest growth with advanced helmets for fighter aircraft pilots.

Key Regional Highlights:

- Asia Pacific: Largest market; demand driven by China, India, and ongoing modernization programs.

- North America: Moderate CAGR supported by highest defense budgets (U.S.) and strong R&D ecosystem.

- Europe: Second-largest market; fastest-growing region due to wearable adoption across armed, naval, and air forces.

- Middle East: Countries like Iran, Turkey, Israel, UAE investing in Future Soldier Programs.

- Latin America & Africa: Moderate growth driven by rising military spending on armor protection and basic wearables.

Military Wearables Market TRENDS

Download Free sample to learn more about this report.

Development of Advanced Technologies and their Increasing Adoption to Aid Market Proliferation

The personnel who protect the country deserve the best technology available equipment for self-protection and self-monitoring. Wearable equipment for military soldiers, such as biometric sensors and printed heaters, can help give personnel an edge. Additionally, more new technologies in wearables are providing sustainability, mobility, and safety for personnel in hazardous situations. Technologies such as thin and flexible heaters in military clothing provide warmth in terrible weather conditions by adding a thin layer of the printed heater under the gloves, boots, helmets, and jackets. Biometric sensors give solutions for remote health monitoring in soldiers. Further, smart clothing with biometric sensors can help with performance monitoring at the individual level. Implementing biometric sensors into military personnel's clothing makes it easy to monitor muscle activity, fatigue, and symmetry.

- Asia Pacific witnessed military wearables market growth from USD 2.29 Billion in 2021 to USD 2.35 Billion in 2022.

DRIVING FACTORS

Adoption of Advanced Wearable Technology to Boost Market Growth

Military wearables are revolutionary products that could impact the armed forces in the coming years. Many pieces of equipment and gadgets can become integral to a soldier's wearable or uniform, freeing him from carrying additional payloads. Moreover, the soldier-mounted wired microsensors could be integrated into a captive wireless network and connected to a cloud-based centralized server. This will help in monitoring soldiers' health performance and provide better connectivity with the crew members. Devoted applications can be industrialized to monitor and control the soldiers deployed in hazardous missions or areas.

Furthermore, communication networks can be the next in line. Implantable sensor technology, including Wireless Body Area Networks (WBANs), tied with technologies such as the Internet of Battlefield Things (IoBT), would make battlefield management fully digital. These advanced technologies are driving market growth during the forecast period.

Embedding More Capabilities in Wearable Military Technologies to Aid Market Augmentation

In the military arena, all gear has to be carefully considered in terms of size, weight, and power (SWaP). Adding more weight will make soldiers less mobile, agile, responsive, and effective. Wearables eliminate the need to carry gear in a pack or by hand, and by embedding more capabilities into those wearables, the overall technology load is streamlined. More abilities are being integrated into personal equipment, enabling military personnel to carry fewer devices, thus driving market growth. Further, military wearables include communications devices, heated clothing, health and performance monitors, and tracking devices. Battlefield communications go beyond exchanging voice messages. Military technologies must be multifunctional and portable. Instead of adding more widgets and bulking out the soldier, new wearable technologies are creating small and multifunctional devices to connect humans and be more reliable for soldiers on the battlefield.

RESTRAINING FACTORS

Adoption of Conventional Equipment by Developing Nations to Hinder Market Proliferation

However, it is anticipated that market development would be hampered by emerging economies purchasing conventional combat equipment rather than cutting-edge military wearables. On the other hand, the exoskeleton, smart textiles, power and energy management, and communication systems have more cost than conventional equipment. Financial instability is becoming more prevalent in emerging economies, a significant issue restricting market expansion. Countries like Sudan, the Philippines, and South Africa, among others, are forced to procure conventional weapon systems rather than invest in advanced technology military equipment due to a high inflation rate, low GDP, and low military expenditure.

SEGMENTATION Analysis

By Wearable Type Analysis

Based on wearable type, the market is divided into headwear, eyewear, wristwear, hearables, and bodywear.

In wearable type, the bodywear segment held the largest market share during the forecast period. The increasing adoption of advanced technologies in bodywear is boosting segmental growth in the coming years. The key players have been undertaking extensive research and engineering to help the consumer withstand harsh conditions, provide maximum mobility and comfort, and provide tactical advantages, creating lucrative growth during the forecast period.

Further, headwear accounted for the fastest growing segment during the forecast period due to huge demand and integration of headwear with different advanced technologies such as Virtual Reality (VR) and Argument Reality (AR). Further, the modernization in military headwear, such as integrated cameras and displays for enhanced low capabilities, boosted segmental growth.

The increasing research & development in eyewear to enhance soldiers' abilities in the field boosts the market growth. For instance, in October 2021, the U.S. army and Microsoft contracted AR Glasses to the U.S. army. These glasses, called the Integrated Visual Augmentation System (IVAS), are integrated with various technologies, such as night and thermal vision and augmented reality, that allows the soldier to fight, rehearse, and train.

In recent years, the increasing development in wristwear for military use is creating lucrative opportunities in the forecast period. The various technologies are integrated into a single device with multiple functions, such as communication, health monitoring system, and navigation, which boost the market growth.

By Technology Analysis

Rising Adoption of Communication & Computing Equipment in the Modern Battlefield for Better Connectivity, Protection, and Situational Awareness to Boost the Market

Based on technology, the market is classified into smart textiles, network and connectivity management, exoskeleton, vision & surveillance, communication & computing, monitoring, power and energy source, and navigation.

Communication & computing is the largest segment during the forecast period. The rising adoption of communication technology in wearable devices will aid market growth. These devices allow soldiers to be more connected and efficient on the battlefield, as they can easily communicate with each other and access important information.

With rising technological-based equipment for military personnel to protect and give them real-time situational awareness in the field, the vision & surveillance segment is the fastest-growing segment during the forecast period. Leading players are introducing technologies such as artificial intelligence in the devices, sensors in smart textiles for personnel body measures, advanced eyewear, communication, and navigation systems, thereby gaining attraction from military forces.

For instance, in October 2020, BAE Systems introduced the illuminated Hawkeye HWK1411, the ultra-low-light image sensor with night vision capabilities with reduced size, weight, and power. The 1.6-megapixel sensor provides high-performance imaging capabilities in all light conditions and is optimal for battery-powered soldier systems, unmanned platforms, and targeting and surveillance applications.

By End User Analysis

To know how our report can help streamline your business, Speak to Analyst

Increasing Adoption of Various Wearables Equipment by Land Forces for Special Operation Application Aids the Market Growth

The Land Forces segment led the market accounting for 41.36% market share in 2026. By end user, the market is divided into land forces, naval forces, and air forces. The land forces segment held most of the worldwide market share in 2021. Increasing adoption of next-generation body armor, lightweight military wearables, eyewear and helmets, and other equipment by land forces is a key factor driving the segment's growth. For instance, in October 2020, U.S. Army awarded a contract to Elbit Systems to supply next-level Enhanced Night Vision Goggle – Binocular Systems for personnel in the war field. Moreover, in October 2020, Elbit Systems provided Soldier Systems to the Armed Forces of the Netherlands.

- The land forces segment is expected to hold a 41.36% share in 2022.

The air forces segment is the fastest growing segment during the forecast period due to the rising adoption of technologically based advanced systems by aircraft pilots, which drives segmental growth. For instance, Elbit Systems and Rockwell Collins introduced a Helmet Mounted Display System (HMDS) for F-35 Gen III fighter aircraft. The helmet is made of carbon fiber to overcome weight and reinforced with a checkerboard pattern and Kevlar to stay rigid. Additionally, it provides pilots with real-time information such as airspeed, heading, altitude, targeting, and warnings. According to both companies, these helmets cost around USD 400,000.

REGIONAL Analysis

Asia Pacific Military Wearables Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The global market is divided into North America, Europe, Asia Pacific, South East Asia, the Balkans, the Middle East, and the Rest of the World.

Asia Pacific

Asia Pacific dominated the market with a valuation of USD 2.59 billion in 2025 and is projected to reach USD 2.67 billion in 2026. Asia Pacific is the dominating region in the military wearables market in 2022. Countries like China and India have the most armed forces in land, naval, and airborne platforms. So it needs more wearable equipment for its application in various situations. Moreover, the adoption of advanced wearables in this region is boosting the demand for wearables during the forecast period.

North America

The market in North America is predicted to grow at a moderate CAGR during the estimated period. The U.S. had the highest defense budget in 2021. The rise in the adoption of next-generation advanced wearables for personnel and the presence of key manufacturers are estimated to fuel the market growth in North America. Moreover, increasing the federal budget for military procurement plans for all military platforms, such as air, sea, and land, will drive market growth during the forecast period.

Europe

Europe is the second-largest market in 2022 and is estimated to be the fastest-growing market during the forecast period. The increasing adoption of wearables in all platforms, such as armed forces, naval forces, and air forces, for various threat protection applications across the region. Additionally, several countries such as Germany, France, Russia, Spain, and the U.K. are investing in advanced technological products for threat/soldier protection. Increased spending in wearables for enhanced soldier capabilities aids the Europe market growth in the upcoming years.

Iran, Turkey, Israel, and the UAE in the Middle East region are increasing investment in the Future Soldier's Program to strengthen their armed personnel with more advanced wearables. Additionally, adopting technological devices for the military, which can benefit the soldiers during training, on-ground service, or war, thereby boosting the regional market growth during the forecast period.

Latin America and Africa are increasing the adoption of next-level armor protection with advanced technology-based products for personnel, which can be helpful on the battlefield. The rest of the world's market is growing moderately as rising military expenditure by various countries in both regions drives the market growth.

KEY INDUSTRY PLAYERS

The competitive landscape of the global market depicts the domination of top military wearables players such as Elbit System Ltd., Leonardo S.p.A., L3harris Technologies Inc., Lockheed Martin Corporation, and others. Key players focus on investments in research and development to diversify their product portfolio. They also focus on business expansion strategies such as agreements, mergers and acquisitions, and long-term contracts with multinational companies and governments of various countries.

LIST OF KEY COMPANIES PROFILED:

- Aselsan A.S. (Turkey)

- Elbit Systems Ltd. (Israel)

- General Dynamics Corporation (U.S.)

- Honeywell International Inc. (U.S.)

- L3harris Technologies Inc. (U.S.)

- Leonardo S.p.A. (Italy)

- Lockheed Martin Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Safariland LLC (Florida)

- TE Connectivity Ltd. (Switzerland)

- Thales Group (France)

KEY INDUSTRY DEVELOPMENT

- October 2022 – L3Harris Technologies launched a new product called Iridium Distributed Tactical Communications Systems (DTCS). This product is used for push-to-talk voice and data for fighters worldwide. The mission module connects with the L3Harris AN/PRC-163 channel and provides secure voice and data communication without having a satellite radio.

- October 2022 – The U.S. Army awarded a contract to L3Harris Technologies to provide AN/PRC-163 Leader and AN/PRC-158 Manpack radios. These products deliver multi-mission networking ability for personnel in the war field. The contract's total value was USD 235 million and included a five-year base and an additional five-year option.

- October 2022 – The Canadian Department of National Defense awarded a contract to Logistik Unicorp to provide functional clothing and footwear to equip military personnel. Under the contract, Logistik Unicorp will supply operational gear for 160,000 personnel, including regular and reserve force members. The total value of the agreement was USD 2.82 Million.

- February 2022 – The Defense Ministry representatives of three countries, Norway, Finland, and Sweden, signed a contract on the joint acquisition for soldiers from all the Nordic countries to deliver uniforms from the same manufacturers. The contract's total value was USD 435.46 million, and the first delivery will start in 2022.

- July 2022 – The U.S. Marine Corps was awarded a contract worth USD 176 million to L3Harris Technologies to provide multi-channel handheld and vehicular radio systems.

REPORT COVERAGE

The report brings a comprehensive analysis of the market and highlights key aspects such as key players, objects, offerings, and end users of military wearables. Moreover, the research report provides insights into the competitive landscape, market trends, market competition, product pricing, regional analysis, market players, competition landscape, and the market status and highlights key industry growths. In addition to the factors stated above, the report encompasses several direct and indirect influences that have subsidized the sizing of the global market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.25% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Wearable Type

|

|

By Technology

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market size was USD 8.62 billion in 2025 and is anticipated to reach USD 11.5 billion by 2034.

Registering a CAGR of 3.25% the market will exhibit steady growth in the forecast period (2026-2034).

Bodywear in the wearable type segment is likely to be the leading segment in this market.

Elbit System Ltd. is the leading player in the market.

Asia Pacific dominated the market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 370

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us