Mineral Processing Equipment Market Size, Share & Industry Analysis, By Equipment Type (Grinding Equipment, Crushing Equipment, Separation Equipment, Screening & Classification Equipment, Dewatering & Filtration Equipment, and Others), By Mineral Type (Copper, Iron Ore, Gold, Lithium, Nickel, Coal & Mineral Sands, and Others), By Installation (Stationary Processing Equipment, Semi-Mobile Systems, Mobile Processing Units, and Others), By Application (Comminution, Separation & Concentration, Dewatering & Tailings, Material Transport, and Others), and Regional Forecast, 2026-2034

Mineral Processing Equipment Market Size and Future Outlook

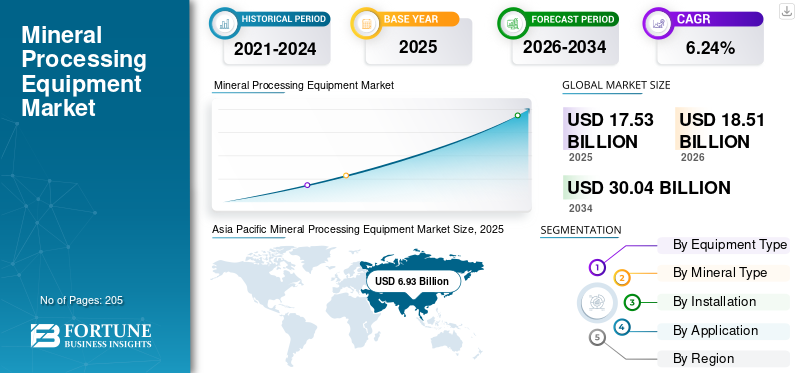

The global mineral processing equipment market size was valued at USD 17.53 billion in 2025. The market is projected to grow from USD 18.51 billion in 2026 to USD 30.04 billion by 2034, exhibiting a CAGR of 6.24% during the forecast period. Asia Pacific dominated the mineral processing equipment market with a market share of 39.53% in 2025.

Mineral processing equipment refers to machinery and systems used to crush, grind, screen, separate, concentrate, dewater, and refine ores and industrial minerals after extraction from mines. The equipment plays a critical role in improving mineral recovery rates, increasing processing efficiency, and reducing operational costs across mining operations. Key equipment categories include crushers, grinding mills, flotation systems, magnetic separators, hydrocyclones, screens, thickeners, filtration systems, and process automation technologies. These systems are widely used in the processing of copper, iron ore, gold, lithium, nickel, phosphate, rare earth elements, and industrial minerals.

The market share is experiencing steady growth due to increasing global demand for critical minerals required in electric vehicles, renewable energy infrastructure, batteries, and power transmission systems. Declining ore grades across major mining regions are also driving the need for advanced beneficiation technologies capable of efficiently handling larger ore volumes. In addition, mining companies are investing heavily in energy-efficient grinding systems, water recovery technologies, tailings management solutions, and digital process optimization systems to improve sustainability and comply with stricter environmental regulations. Growing investments in lithium, copper, and nickel processing projects are expected to accelerate global market expansion further.

- For instance, in March 2025, Metso secured a major order for mineral ore processing equipment for a large copper concentrator expansion project in South America. The project included the supply of energy-efficient grinding mills, flotation systems, slurry pumps, and advanced process automation technologies designed to improve ore recovery and reduce energy consumption. The investment reflects the growing global focus on expanding copper beneficiation capacity, driven by demand from electric vehicles, renewable energy infrastructure, and power transmission networks.

Some of the leading companies operating in the global mineral processing equipment industry include Metso, FLSmidth, Weir Group, and others. Metso is a global leader in material processing equipment and technologies, providing solutions for crushing and screening equipment, grinding, flotation, screening, filtration, and process automation across mining operations worldwide. The company serves major industries, including copper, iron ore, gold, lithium, and aggregates, with a strong focus on energy-efficient, sustainable beneficiation technologies.

Download Free sample to learn more about this report.

Mineral Processing Equipment Market Key Takeaways

- 2025 Market Size: USD 17.53 Billion

- 2026 Market Size: USD 18.51 Billion

- 2034 Forecast Market Size: USD 30.04 Billion

- CAGR: 6.24% from 2026–2034

- Asia Pacific dominated the mineral processing equipment market with a 39.53% share in 2025.

- Grinding equipment accounted for 27.20% of the global market in 2025.

- Stationary processing equipment held 73.44% of the global market share in 2025.

Asia Pacific

Asia Pacific led the market with USD 6.93 billion in 2025, accounting for 39.53% of global revenue.

North America

North America reached USD 3.43 billion in 2025 and is projected to grow to USD 3.58 billion in 2026.

Europe

Europe was valued at USD 2.13 billion in 2025 and is projected to grow at a 4.03% CAGR during the forecast period.

U.S.

The U.S. mineral processing equipment market was valued at approximately USD 2.58 billion in 2025, representing 14.73% of global revenue.

Japan

Japan market data was not specified, while Asia Pacific continued to benefit from strong mining and mineral processing investments.

Read More

MINERAL PROCESSING EQUIPMENT MARKET TRENDS

Rising Adoption of Energy-Efficient Grinding and Dry Processing Technologies is a Key Market Trend

A major trend shaping the mineral extraction systems is the rapid adoption of energy-efficient grinding systems and dry processing technologies across large-scale mining automation solutions. Grinding circuits account for a significant share of total energy consumption in mineral beneficiation technologies, particularly in copper, iron ore, and gold processing. As mining companies face increasing pressure to reduce operational costs, carbon emissions, and water consumption, investments are shifting toward technologies such as High-Pressure Grinding Rolls (HPGR), vertical grinding mills, and advanced ore sorting systems.

In addition, dry processing and dry-stack tailings technologies are gaining strong momentum in water-stressed mining regions, including Chile, Peru, Australia, and South Africa. Mining operators are increasingly replacing conventional wet beneficiation systems with filtration and dewatering solutions that improve water recovery and reduce tailings risks. Another notable trend is the integration of AI-based process optimization and digital monitoring systems within concentrators to improve throughput efficiency and recovery rates. These developments are particularly prominent in lithium, copper, and nickel projects, where processing efficiency and sustainability performance are becoming critical investment priorities for mining companies globally.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Critical Mineral Beneficiation Capacity is Key Market Driver

A key driver accelerating the mineral processing equipment market growth is the global expansion of critical mineral beneficiation capacity, particularly for copper, lithium, nickel, graphite, and rare earth elements. Governments and mining companies are increasingly investing in domestic mineral processing infrastructure to reduce dependence on raw-ore exports and strengthen regional battery and clean-energy supply chains. Countries such as Indonesia, Canada, Australia, India, and several African nations are implementing beneficiation-focused mining policies that require minerals to be processed locally before export. This shift is generating substantial demand for advanced crushing, grinding, flotation, filtration, and separation equipment.

Large mining companies are expanding concentrator capacities to support rising long-term demand from electric vehicles, grid infrastructure, semiconductors, and renewable energy systems. New copper and lithium projects are being designed with higher throughput capacities and more complex processing circuits, increasing equipment intensity per project.

MARKET RESTRAINTS

High Capital Intensity and Long Equipment Replacement Cycles to Hamper Market Growth

One of the major restraints on the mineral processing equipment industry is the high capital intensity of beneficiation plant development and large-scale processing equipment installations. Equipment such as SAG mills, HPGR systems, flotation circuits, filtration units, and thickening systems requires substantial upfront investment, making procurement decisions highly dependent on commodity price cycles and mining company cash flows.

During periods of weak metal prices or mining investment slowdowns, several processing plant expansion projects are postponed or scaled down, directly impacting equipment demand. In addition, mineral processing equipment typically has long replacement cycles due to its heavy-duty industrial design and extended operational lifespan. Many mining companies continue refurbishing existing grinding and flotation systems instead of purchasing new equipment to reduce capital expenditure.

MARKET OPPORTUNITIES

Growing Demand for Modular and Mobile Mineral Processing Plants Creating New Revenue Opportunities

A significant market opportunity is the increasing adoption of modular and mobile beneficiation plants across remote and small- to mid-scale mining projects. Mining companies are increasingly seeking flexible processing solutions that can be deployed quickly, relocated efficiently, and operated with lower infrastructure requirements, particularly in lithium, gold, rare earth, and industrial mineral projects.

Modular mineral processing systems reduce construction timelines, minimize on-site engineering complexity, and lower initial capital commitments compared to conventional large-scale concentrators. This trend is especially prominent in Africa, Latin America, and parts of Asia Pacific, where new mining developments are located in remote regions with limited infrastructure. Equipment manufacturers are therefore expanding their offerings to include skid-mounted crushers, containerized flotation systems, mobile screening plants, compact filtration units, and prefabricated concentrator modules.

MARKET CHALLENGES

Supply Chain Disruptions and Long Manufacturing Lead Times Creating Operational Challenges

One of the major challenges facing the market is the increasing pressure on global manufacturing and supply chains for heavy industrial processing machinery and specialized components. Equipment such as grinding mills, flotation cells, high-capacity crushers, filtration systems, and large slurry pumps requires complex fabrication processes, heavy engineering capabilities, and specialized wear-resistant materials.

Rising demand for mining equipment solutions globally has significantly extended manufacturing lead times for critical systems, particularly for large grinding mills and energy-efficient processing technologies. In several cases, delivery timelines for major concentrator equipment have stretched to more than a year, affecting project execution schedules and mine commissioning plans.

Segmentation Analysis

By Equipment Type

Grinding Equipment Dominated Due to High Energy Usage in Ore Processing

Based on the equipment type, the market is classified into grinding equipment, crushing equipment, separation equipment, screening & classification equipment, dewatering & filtration equipment, material handling equipment, process automation & digital systems, and others.

In 2025, grinding equipment systems held the 27.20% of the market share due to their critical role in reducing ore size before mineral separation and concentration processes. Grinding circuits, including SAG mills, ball mills, and vertical grinding mills, are essential components in copper, iron ore, gold, lithium, and nickel beneficiation plants. These systems typically account for the largest share of mineral processing plant capital expenditure and energy consumption, making them central to overall plant productivity and recovery efficiency. Growing investments in large-scale concentrators and declining ore grades are increasing the need for high-capacity grinding systems capable of efficiently processing larger ore volumes.

The separation equipment segment is experiencing the highest growth and is expected to grow at a CAGR of 8.24% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Mineral Type

Copper Dominated Due to Extensive Global Copper Beneficiation Investments

Based on the mineral type, the market is classified into copper, iron ore, gold, lithium, nickel, coal & mineral sands, phosphate & fertilizer minerals, industrial minerals, and others.

In 2025, the copper segment accounted for approximately 25.64% of the global market share due to the large-scale global copper mining and concentrator expansion projects. Copper ores require extensive crushing, grinding, flotation, thickening, and filtration processes, resulting in a higher equipment intensity than for many other minerals. Major copper-producing countries, including Chile, Peru, China, the U.S., Zambia, and the Democratic Republic of Congo, are continuously investing in concentrator modernization and throughput expansion to address rising global copper demand.

The lithium segment is expected to grow at a CAGR of 8.75% over the forecast period.

By Installation

Stationary Processing Equipment Led Market as It Allows Better Integration of Automation

On the basis of the installation, the market is classified into stationary processing equipment, semi-mobile systems, mobile processing units, and others.

In 2025, the stationary processing equipment held 73.44% share of the global market. Stationary systems enable better integration of automation, process optimization, and energy-efficient technologies than mobile alternatives. In addition, large concentrators handling low-grade ores require highly durable, customized stationary equipment capable of continuously processing massive ore volumes. Ongoing investments in mega concentrator expansions and long-life mining projects continue to strengthen demand for stationary mineral processing systems globally.

The mobile processing units segment is expected to grow at a CAGR of 8.80% over the forecast period.

By Application

Comminution Commanded Market as It is the Essential Stage in Ore Liberation

On the basis of the application, the market is classified into comminution, separation & concentration, dewatering & tailings, material transport, plant automation & monitoring, and others.

In 2025, the comminution segment accounted for 44.60% share of the global market. Comminution dominated the market as it is the primary and most energy-intensive stage in mineral beneficiation operations. The process involves crushing and grinding ore to achieve adequate mineral liberation before flotation, magnetic separation, or other concentration processes. Comminution systems, including crushers, SAG mills, ball mills, and High-Pressure Grinding Rolls (HPGR), are widely deployed across copper, iron ore, gold, lithium, and nickel processing plants. These systems account for a substantial share of total concentrator capital expenditure and operating costs due to their continuous high-capacity operation requirements.

The separation & concentration segment is expected to grow at a CAGR of 7.59% over the forecast period.

Mineral Processing Equipment Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Mineral Processing Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific reached USD 6.93 billion in 2025 and is estimated to account for a dominating market share. In the region, India and China reached USD 0.97 billion and USD 2.32 billion, respectively, in 2025. Asia Pacific leads the mineral processing equipment market share due to large-scale investments in lithium concentrators, iron ore beneficiation plants, nickel processing facilities, and copper concentrator expansions across China, Australia, India, and Indonesia.

India Mineral Processing Equipment Market

The India market accounted for roughly 5.56% of global revenues. India’s market is expanding due to rising investments in iron ore beneficiation, coal washing plants, bauxite processing, and critical mineral development projects supported by domestic mineral value-addition policies.

China Mineral Processing Equipment Market

China’s market accounts for roughly 13.25% of global revenues.

Australia Mineral Processing Equipment Market

The Australian market in 2025 was valued at around USD 1.71 billion, accounting for roughly 9.76% of global revenues.

North America

The North America market in 2025 was valued at USD 3.43 billion and held a dominant share in 2026, reaching USD 3.58 billion. North America represents a technologically advanced market, supported by significant investments in concentrator modernization, autonomous processing systems, and advanced tailings management infrastructure. The region is witnessing increasing deployment of high-capacity grinding circuits, digital process control systems, and water recovery technologies, particularly across copper, gold, and critical mineral projects in the U.S. and Canada.

U.S. Mineral Processing Equipment Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at around USD 2.58 billion in 2025, accounting for roughly 14.73% of global revenues.

Europe

Europe is projected to record a growth rate of 4.03% in the coming years and was valued at USD 2.13 billion in 2025. Investments strongly influence Europe’s market in battery mineral beneficiation, sustainable concentrator technologies, and strict environmental compliance standards. Countries such as Finland, Sweden, and Germany are expanding advanced flotation, filtration, and sensor-based ore-sorting technologies to support critical raw-material processing and reduce dependence on imported refined minerals.

Germany Mineral Processing Equipment Market

The German market in 2025 was valued at around USD 0.50 billion and is estimated at around USD 0.52 billion in 2026, representing roughly 2.88% of the global revenues. Germany’s market is characterized by strong demand for high-capacity crushing systems, advanced filtration technologies, and energy-efficient grinding solutions used across industrial minerals, copper, and recycling-oriented beneficiation projects.

Latin America

Latin America is expected to see moderate growth in this market over the long term. The Latin America market was valued at USD 3.11 billion in 2025. Latin America’s market is driven by large-scale copper concentrator expansions in Chile and Peru, along with rapidly growing lithium beneficiation investments in Argentina and Brazil.

Brazil Mineral Processing Equipment Market

Brazil's market was valued at approximately USD 1.45 billion in 2025, accounting for roughly 8.27% of global revenues.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market was valued at USD 1.93 billion in 2025.

The Middle East & Africa market is witnessing rising investments in copper concentrators, phosphate beneficiation, lithium processing, and gold recovery projects across Saudi Arabia, South Africa, Zambia, and the Democratic Republic of Congo. The region is also experiencing growing demand for modular processing plants, tailings filtration systems, and high-capacity flotation technologies to support new mining developments and domestic beneficiation initiatives.

GCC Mineral Processing Equipment Market

The GCC market was valued at around USD 0.28 billion in 2025, representing roughly 1.60% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players are Actively Expanding Their Market Share Via Partnerships, Business Expansion, and Technological Advancements

The global mineral processing equipment market is highly consolidated, with prominent players including Metso, FLSmidth, Weir Group (Weir Minerals), and others. Companies operating in the market are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in March 2025, FLSmidth announced the supply of advanced grinding and flotation equipment systems for a large copper concentrator expansion project in Chile. The order included energy-efficient SAG mills, flotation cells, hydrocyclones, and digital process optimization systems designed to improve throughput capacity and recovery efficiency. The project supports rising global copper demand from renewable energy infrastructure and electric vehicle

Other key players in the global market include Sandvik Rock Processing Solutions, Thyssenkrupp Mining Technologies, TAKRAF Group, and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY MINERAL PROCESSING EQUIPMENT COMPANIES PROFILED

- Metso (Finland)

- FLSmidth (Denmark)

- Weir Group (U.K.)

- Sandvik Rock Processing Solutions (Sweden)

- Thyssenkrupp Mining Technologies (Germany)

- TAKRAF Group (Germany)

- Eriez (U.S.)

- Multotec (South Africa)

- McLanahan Corporation (U.S.)

- Terex Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Sandvik AB Rock Processing Solutions introduced a new high-capacity cone crushing system for iron ore and copper beneficiation plants in Australia. The equipment was designed to improve crushing efficiency, reduce energy consumption, and support higher throughput operations in large concentrators. The installation included automated process monitoring and wear optimization technologies to reduce maintenance downtime and improve operational reliability. Mining operators increasingly adopted advanced crushing solutions to manage declining ore grades and rising processing volumes in large-scale mineral beneficiation projects.

- November 2024: TAKRAF Group secured a contract for a large-scale bulk material handling and conveying system at a copper processing project in Zambia. The project included in-pit crushing systems, conveyor infrastructure, and beneficiation support technologies to improve ore transport efficiency and reduce operational costs. The development supported expanding copper concentrator capacity in Central Africa, where mining companies are increasing investments in high-throughput processing operations.

- September 2024: Metso secured a contract to deliver mineral processing equipment for a lithium beneficiation project in Western Australia. The scope included crushing systems, grinding mills, screening technologies, and filtration equipment for spodumene concentrate production. The project was developed to strengthen battery mineral supply chains and increase domestic lithium processing capacity. The concentrator was designed with modular processing systems and advanced automation controls to support operational flexibility, improve recovery rates, and reduce energy consumption across the beneficiation process.

- February 2024: Eriez announced the deployment of advanced magnetic separation and fine particle flotation systems for a rare earth mineral processing facility in the U.S. The equipment was designed to improve the efficiency of rare earth recovery and support the development of the domestic critical mineral supply chain. The project reflected increasing investments in strategic mineral-processing infrastructure aimed at reducing dependence on imported refined rare-earth materials.

- January 2024: Weir Minerals introduced upgraded tailings dewatering and slurry transport systems for copper and gold processing plants in Peru. The deployment included high-capacity slurry pumps, filtration technologies, and wear-resistant cyclone systems intended to improve water recovery and reduce tailings disposal risks. Mining companies in the region are increasingly investing in advanced dewatering infrastructure to comply with stricter environmental regulations and address growing pressure to improve water efficiency.

REPORT COVERAGE

The global mineral processing equipment market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and the market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.24% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Equipment Type, Mineral Type, Installation, Application, and Region |

| By Equipment Type |

|

| By Mineral Type |

|

| By Installation |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 17.53 billion in 2025 and is projected to reach USD 30.04 billion by 2034.

In 2025, the market value in North America stood at USD 3.43 billion.

The market is expected to exhibit a CAGR of 6.24% during the forecast period of 2026-2034.

The grinding equipment segment led the market by equipment type.

Rising investments in critical mineral beneficiation, declining ore grades, and growing demand for energy-efficient, high-throughput processing technologies are key drivers of the market.

Metso, FLSmidth, Weir Group, and Sandvik Rock Processing Solutions are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Increasing mining activities, rising demand for critical minerals and metals, and growing automation in mining operations are the major factors expected to favor the adoption of mineral processing equipment.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us