Mineral Wool Market Size, Share, and Industry Analysis By Type (Glass, Rock, Slag, and Others) By End-use Industry (Building and Construction, Transportation, Industrial Equipment, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

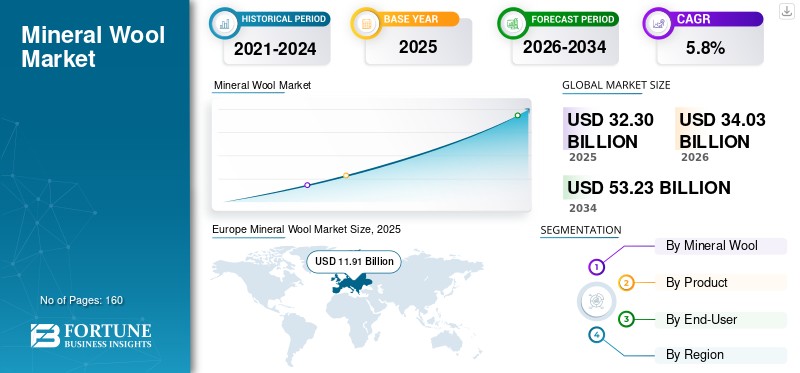

The global mineral wool market size was valued at USD 32.30 billion in 2025. The market is projected to grow from USD 34.03 billion in 2026 to USD 53.23 billion by 2034, exhibiting a CAGR of 5.8% during the forecast period. Europe dominated the global mineral wool market with a share of 36.87% in 2025.

Mineral wool is a man-made fibrous insulation material produced by melting inorganic raw materials such as natural stone (for example, basalt or diabase), blast-furnace slag, or recycled glass, and then spinning or drawing the molten material into fine fibers. It is non-combustible, dimensionally stable at high temperatures, and chemically inert, making it suitable for use in building envelopes, industrial insulation systems, HVAC ducts, appliances, and transportation applications.

The growth of the mineral wool market is driven by stricter energy-efficiency regulations and building codes that mandate improved thermal insulation to reduce energy consumption for heating and cooling. Rising emphasis on fire safety in residential, commercial, and industrial construction further supports demand, as it is non-combustible and performs reliably under high temperatures. Moreover, ongoing growth in construction and infrastructure development, combined with urbanization in emerging economies, continues to expand its application base across buildings, transport, and industrial facilities.

Furthermore, the market is comprised of several major players, including Johns Manville, Saint-Gobain, USG, Rhino, and URSA UK. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Mineral Wool Market KEY TAKEAWAYS

- 2025 Market Size: USD 32.30 billion

- 2026 Market Size: USD 34.03 billion

- 2034 Forecast Market Size: USD 53.23 billion

- CAGR: 5.8% from 2026–2034

- Europe dominated the mineral wool market with a 36.87% share in 2025.

- The glass wool segment led the market with a 63.5% share in 2025.

- The board segment accounted for the largest product form share at 50.0% in 2025.

Europe

Europe held the leading market position, supported by energy-efficiency regulations and building renovation programs.

North America

North America witnessed steady demand driven by stricter fire safety and thermal performance standards.

Asia Pacific

Asia Pacific is expected to record significant growth due to rapid urbanization and infrastructure development.

U.S.

U.S. Growing adoption of mineral wool is supported by increasing focus on energy-efficient and fire-resistant buildings.

Japan

Japan Demand is supported by stringent building standards and the need for advanced thermal and acoustic insulation solutions.

Read More

MINERAL WOOL MARKET TRENDS

Rapid Urbanization and Infrastructure Development Are One of the Significant Market Trends

Urban population growth necessitates large-scale construction of residential buildings, commercial complexes, transportation hubs, and social infrastructure. Insulation materials are integral to these projects, ensuring thermal comfort, energy efficiency, and safety, and positioning mineral wool as a core input in the construction process. Large infrastructure projects increasingly adopt standardized building specifications that favor durable, high-performance insulation materials. Mineral wool’s dimensional stability, acoustic insulation capability, and resistance to moisture and pests make it suitable for long-life infrastructure assets such as metro stations, airports, and public buildings.

- Mass transit infrastructure projects often use mineral wool insulation for station buildings and service areas due to its combined fire resistance, acoustic performance, and durability. High-density residential developments similarly adopt mineral wool to meet both thermal and noise control requirements.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Energy Efficiency Regulations and Building Codes Drive the Market Growth

Governments worldwide are increasingly mandating higher thermal performance standards to reduce energy consumption, lower carbon emissions, and enhance national energy security. Mineral wool, with its low thermal conductivity and stable insulation performance over time, is well-positioned to meet these regulatory requirements. Unlike some organic insulation materials, mineral wool retains its insulating properties even under high temperatures, moisture exposure, or aging, making it compliant with long-term building performance standards.

Emerging economies are also strengthening building efficiency norms as urbanization accelerates and electricity demand rises. In the Asia-Pacific region, government-led affordable housing programs and green building frameworks increasingly specify mineral wool-based insulation systems to achieve compliance with energy benchmarks. Mineral wool’s adaptability across cold, temperate, and hot climates enhances its suitability for standardized adoption in large-scale housing and infrastructure projects.

- Public-sector building programs in Europe increasingly require mineral wool insulation in schools, hospitals, and public housing due to its compliance with both thermal and fire safety standards. Similarly, commercial office developments targeting high energy performance ratings often rely on mineral wool façade systems to meet envelope efficiency requirements.

MARKET RESTRAINTS

High Energy Intensity and Cost Volatility in Manufacturing to Restrict Market Expansion

Mineral wool production involves melting raw materials, such as basalt, diabase, limestone, or recycled slag, at temperatures typically exceeding 1,400°C. This process is heavily dependent on natural gas, electricity, or coke, making production costs highly sensitive to fluctuations in energy prices. As global energy markets experience frequent disruptions due to geopolitical tensions, supply constraints, and decarbonization policies, mineral wool manufacturers face persistent cost pressures.

Unlike polymer-based insulation materials that can be produced at comparatively lower temperatures, mineral wool’s melting and fiberizing stages impose a structural cost disadvantage. When energy prices spike, manufacturers often struggle to fully pass these increases on to their customers, especially in price-sensitive construction markets. This can compress margins or delay capacity utilization decisions in regions where energy subsidies are limited or being phased out, leading to restriction in the mineral wool market growth.

MARKET OPPORTUNITIES

Sustainability and Circular Economy Alignment to Restrict Market Expansion

Mineral wool is manufactured from abundant natural minerals and recycled materials such as slag, contributing to resource efficiency. Its long lifespan reduces replacement frequency, lowering lifecycle environmental impact. Green building certifications and sustainability frameworks are increasingly recognizing mineral wool for its contributions to energy efficiency, indoor comfort, and fire safety, all without relying on hazardous additives. Additionally, mineral wool products can often be recycled at the end of their life, supporting waste reduction objectives.

- Green-certified commercial buildings often specify mineral wool insulation to meet energy performance and fire safety criteria, while also supporting sustainability targets. Industrial facilities pursuing emissions reduction strategies similarly adopt mineral wool to improve energy efficiency without compromising safety.

MARKET CHALLENGES

Competition from Lower-Cost and Lightweight Insulation Alternatives to Hamper Growth

The market faces sustained restraint from competition with alternative insulation materials, particularly polymer-based products such as expanded polystyrene (EPS), extruded polystyrene (XPS), polyurethane (PU), and polyisocyanurate (PIR). These materials often offer lower upfront costs, lighter weight, and easier installation, making them attractive in cost-driven construction projects. In many residential and low-rise commercial buildings, developers prioritize short-term capital cost savings over long-term performance attributes such as fire resistance or acoustic insulation. As a result, mineral wool may be overlooked despite its superior non-combustibility and durability. Lightweight insulation materials also reduce structural load requirements and transportation costs, further strengthening their competitive position.

Segmentation Analysis

By Type

Glass Wool Segment Held a Dominant Share Due to its Preference in High-Volume Applications

Based on type, the market is segmented into glass wool, stone wool, and others.

The glass wool segment accounted for the largest mineral wool market share in 2025. Due to its cost efficiency, lightweight nature, and strong thermal and acoustic insulation performance, it is a preferred material for high-volume applications. The material’s relatively lower melting temperature compared to stone wool enables energy-efficient manufacturing, supporting large-scale production and competitive pricing. This cost advantage is important in residential and commercial construction, where insulation budgets are tightly managed. Furthermore, the segment held a 63.5% market share in 2025.

The growth of the stone wool segment is driven by its superior fire resistance, mechanical strength, and high-temperature stability, which make it essential in safety-critical and industrial applications. The material’s non-combustibility and ability to withstand temperatures above 1,000°C support strong adoption in high-rise buildings, industrial facilities, power plants, and petrochemical complexes. In addition, stone wool is projected to grow at a CAGR of 5.3% during the study period.

By Product

Board Mineral Wools Held the Largest Market Share Due to Increasing Demand for Rigid and High-Density Insulation Solutions

In terms of Product, the market is categorized into board, blanket, loose wool, and others.

The board segment accounted for the largest share in 2025. The segment is driven by demand for rigid, high-density insulation solutions that offer dimensional stability and load-bearing capability. Boards are widely used in façades, flat roofs, industrial walls, and fire-rated assemblies where structural integrity and consistent thickness are critical. Their ability to provide combined thermal, acoustic, and fire performance in a single product supports adoption in commercial and institutional buildings. Growth is reinforced by increasing use of external insulation finishing systems and ventilated façade designs in energy-efficient building projects. In addition, the segment held 50% market share in 2025.

The blanket segment is projected to experience significant growth in the years to come. The growth of the segment is driven by the demand from residential construction and retrofitting projects, where installers value ease of cutting and fitting around obstacles. Blankets also provide cost-effective insulation coverage over large surface areas, making them suitable for use in warehouses, factories, and agricultural buildings. The product’s lightweight nature reduces transportation and labor costs, which is critical in large-scale insulation deployments. The blanket segment is projected to grow at a CAGR of 5.4% over the forecast period.

The loose wool segment is witnessing favorable growth throughout the forecast period. This expansion is driven by its suitability for blow-in insulation applications and its effectiveness in filling hard-to-reach or irregular spaces. This format is widely used in attic insulation, cavity wall retrofits, and renovation projects where dismantling existing structures is impractical. Growth is supported by energy efficiency upgrade programs in mature markets for residential buildings constructed before modern insulation standards were introduced.

By End-User

Building and Construction Segment Dominates the Market Due to the Stringent Building Codes and Sustainability Standards

In terms of end-user, the market is categorized into automotive and transportation, building and construction, industrial and consumer appliances, others, and others.

The building and construction segment accounted for the largest share in 2025. Stringent building codes and sustainability standards continue to mandate higher insulation performance in residential, commercial, and institutional buildings. Mineral wool’s ability to deliver thermal insulation, alongside fire resistance and sound absorption, makes it a preferred material for use in walls, roofs, and façades. Urbanization, renovation of aging building stock, and growth in green building certifications directly support demand. The building and construction segment held 61.3% of the market share in 2025.

The need for thermal insulation, energy efficiency, and operational safety drives the growth of the industrial and consumer appliances segment. Mineral wool is used in ovens, boilers, water heaters, refrigerators, and industrial machinery to reduce heat loss and improve energy performance. Increasing appliance efficiency standards globally are pushing manufacturers to integrate high-performance insulation materials. The industrial and consumer appliances segment is projected to grow at a CAGR of 5.7% over the forecast period.

The automotive and transportation segment is also expected to experience favorable growth over the projected period. The growth of the segment is driven by demand for acoustic insulation, thermal management, and fire safety in vehicles and transport infrastructure. In automotive applications, mineral wool helps reduce noise in engine compartments, exhaust systems, and cabin insulation. Growth is reinforced by stricter noise and vibration regulations in electric and hybrid vehicles, where powertrain noise is lower, and road noise becomes more prominent.

The automotive and transportation segment is expected to grow at a CAGR of 5.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

Mineral Wool Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Europe

Europe Mineral Wool Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Europe held the dominant share in 2025, valued at USD 11.91 billion. Asia Pacific holds the dominant share of the market. The growth is driven by policy-led decarbonization of the building sector. Ambitious climate targets, energy efficiency mandates, and national renovation programs have made insulation a central pillar of building upgrades, particularly in residential and public buildings. Mineral wool benefits from its ability to deliver thermal insulation alongside fire resistance and acoustic performance, which are critical in dense urban environments and multi-story construction common across Europe.

- Energy efficiency regulations and building renovation activity strongly drive Germany’s market. The country has one of Europe’s most stringent building energy performance frameworks, making thermal insulation a core requirement rather than an optional upgrade. A significant portion of demand stems from the retrofitting and refurbishment of existing residential and public buildings, as Germany prioritizes reducing heating energy consumption and emissions from its building stock.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a positive contributor to the market. The demand in North America is the tightening of energy efficiency and fire safety expectations in buildings, particularly in commercial, institutional, and multi-family residential construction. Building codes and standards are increasingly emphasizing thermal performance, non-combustibility, and acoustic comfort, all of which align well with the material characteristics of mineral wool.

- In the U.S., the demand is driven by performance-based building practices rather than sheer construction volume. Energy efficiency requirements embedded in building codes, combined with growing emphasis on fire resistance and acoustic control, support the use of mineral wool in commercial buildings, multi-family housing, and institutional projects.

Asia Pacific

Asia Pacific is anticipated to witness notable growth in the coming years. The growth of the region is driven by a combination of urbanization, infrastructure expansion, and rising regulatory focus on energy efficiency, though the intensity varies significantly by country. Rapid urban growth and high-rise construction in China, India, and Southeast Asia create a strong underlying demand for thermal and acoustic insulation, particularly in commercial and residential towers. Fire safety concerns in densely populated cities have increasingly prompted developers to adopt non-combustible insulation materials, supporting the use of mineral wool in façades and partitions.

- China’s market is driven by the scale of urban construction and infrastructure development, combined with increasing attention to building energy efficiency and fire safety. Rapid urbanization and the dominance of high-rise residential and commercial buildings create strong demand for non-combustible insulation materials in façades, partition walls, and roofing systems.

Latin America

Latin America is experiencing steady growth, driven by the selective adoption of technologies in commercial buildings, industrial facilities, and higher-end residential projects, rather than broad-based residential penetration. Rising electricity costs and concerns over energy efficiency in large commercial buildings are driving the increased use of thermal insulation, particularly in offices, shopping centers, and hospitals.

Middle East & Africa

The Middle East & Africa region is gradually expanding, driven by extreme climate conditions, energy-efficiency mandates, and industrial insulation needs. In the Middle East, high cooling loads necessitate the use of thermal insulation to reduce electricity consumption in residential and commercial buildings. Mineral wool is widely employed in roofs, walls, and HVAC systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Adopting Business Expansion Strategies to Maintain Their Positions in the Market

Manufacturers are expanding their business to gain a competitive edge in the industry and mitigate the threats posed by new entrants. Some of the key market players include Johns Manville, Saint-Gobain, USG, Rhino, and URSA UK. Market participants are fiercely competing with international and regional players that have extensive distribution networks, regulatory expertise, and established suppliers. Additionally, companies enter into contracts, acquisitions, and strategic partnerships with other market leaders to expand their reach.

LIST OF KEY MINERAL WOOL COMPANIES PROFILED

- Johns Manville (U.S.)

- Saint-Gobain (France)

- Knauf Insulation (Germany)

- K-FLEX S.p.A. (Italy)

- USG (U.S.)

- Rhino (U.S.)

- URSA UK (Spain)

- Polybond Insulation Private Limited (India)

- Minwool Rock Fibres Limited (India)

- ROCKWOOL Limited (Denmark)

KEY INDUSTRY DEVELOPMENTS

- March 2022: Saint-Gobain Isover announced investments in France to increase glass wool capacity (including upgrades and a new line), targeting an additional 70,000+ tons by 2025 to support energy renovation-driven demand.

- December 2021: Saint-Gobain signed a definitive agreement to acquire Rockwool India Pvt Ltd, expanding its insulation footprint in India by entering/strengthening stone wool for thermal, acoustic, and fire-safety applications.

- July 2021: ROCKWOOL began commercial production at its second U.S. factory in Jefferson County, West Virginia, adding post-pandemic stone wool insulation capacity for residential, commercial, and industrial demand.

- May 2021: Knauf Insulation announced the first customer shipments from its new €120 million Johor Bahru (Malaysia) site, positioning glass mineral wool supply closer to Asia-Pacific markets and emphasizing the use of recycled glass inputs and ECOSE Technology binder.

- June 2020: Owens Corning Paroc launched the REWOOL take-back/recycling system in Finland (with partners Lassila & Tikanoja and Eko-Expert), enabling construction-site stone wool offcuts to be collected and reused, an early move to formalize circularity in mineral wool value chains.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.8% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Type, Product, End-User, and Region |

|

By Type |

· Glass Wool · Stone Wool · Others |

|

By Product |

· Board · Blanket · Loose Wool · Others |

|

By End-User |

· Automotive and Transportation · Building and Construction · Industrial and Consumer Appliances · Others |

|

By Geography |

· North America (By Type, By Product, End-User, and Country) o U.S. (By End-User) o Canada (By End-User) · Europe (By Type, By Product, End-User, and Country) o Germany (By End-User) o U.K. (By End-User) o France (By End-User) o Italy (By End-User) o U.K. (By End-User) o Rest of Europe (By End-User) · Asia Pacific (By Type, By Product, End-User, and Country) o China (By End-User) o Japan (By End-User) o India (By End-User) o South Korea (By End-User) o Rest of Asia Pacific (By End-User) · Latin America (By Type, By Product, End-User, and Country) o Brazil (By End-User) o Mexico (By End-User) o Rest of Latin America (By End-User) · Middle East & Africa (By Type, By Product, End-User, and Country) o Saudi Arabia (By End-User) o South Africa (By End-User) o Rest of the Middle East & Africa (By End-User) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 32.30 billion in 2025 and is projected to reach USD 53.23 billion by 2034.

Recording a CAGR of 5.8%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The building and construction end-user segment led in 2025.

Europe held the highest market share in 2025.

Johns Manville, Saint-Gobain, USG, Rhino, and URSA UK are some of the prominent players in the market.

The primary growth driver is the tightening of building energy-efficiency and fire-safety regulations worldwide, which is accelerating demand for high-performance thermal and acoustic insulation materials. Mineral wool’s non-combustibility, thermal resistance, and recyclability align well with regulatory and sustainability mandates in construction and industrial applications.

The major factors expected to favor product adoption in the market are supported by the rising construction of green buildings, the refurbishment of aging infrastructure, and an increasing awareness of indoor comfort and noise control. Additionally, mineral wool’s durability, moisture resistance, and compatibility with circular economy goals strengthen its preference over conventional insulation materials.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us