Mining Robotics Market Size, Share & Industry Analysis, By Equipment Type (Autonomous Haulage Systems, Robotic Drilling Systems, Load-Haul-Dump (LHD) Robots, Robotic Excavators, Underground Mining Robots, and Others), By Operation Mode (Fully Autonomous, Semi-autonomous, and Remote controlled), By Application (Drilling & Blasting, Material Handling, Excavation & Loading, Underground Mining Operations, Exploration & Surveying, Inspection & Monitoring, and Others), and Regional Forecast, 2026 – 2034

Mining Robotics Market Size and Future Outlook

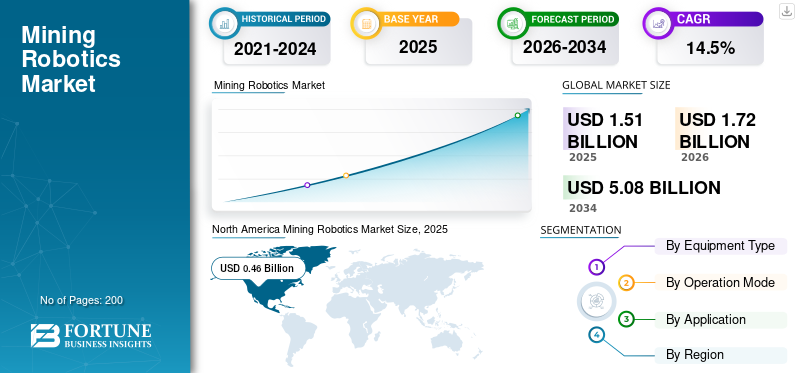

The global mining robotics market size was valued at USD 1.51 billion in 2025. The market is projected to grow from USD 1.72 billion in 2026 to USD 5.08 billion by 2034, exhibiting a CAGR of 14.5% during the forecast period. North America dominated the mining robotics market with a market share of 30.46% in 2025.

Mining activities include underground collapses, extreme temperatures, toxic gases, etc. They are few of the hazardous industries that reduce human exposure to dangerous environments, driving the market demand for remote and autonomous operations. Several companies are adopting industry 4.0 technologies along with AI integration to increase productivity. Similar trends are being witnessed in electric equipment owing to sustainability pressures, driving the adoption of cleaner and efficient technologies. Robotics enable energy-efficient operations and reduced emissions in alignment with ESG goals driving the market growth.

- For instance, in August 2025, Komatsu partnered with Nevada Gold Mines to deploy its FrontRunner autonomous haulage system in the U.S. The initiative focuses on improving mine-site safety and operational efficiency through driverless trucks.

Caterpillar Inc., Komatsu Ltd., and Sandvik AB are a few of the key players in the market. They are integrating robotics with AI and advanced analytics and investing in underground mining robotic solutions to align with ESG goals and minimize emissions which is boosting the market growth.

Download Free sample to learn more about this report.

Mining Robotics Market Key Takeaways

- 2025 Market Size: USD 1.51 Billion

- 2026 Market Size: USD 1.72 Billion

- 2034 Forecast Market Size: USD 5.08 Billion

- CAGR: 14.5% from 2026–2034

- North America dominated the mining robotics market with a 30.46% share in 2025.

- Autonomous haulage systems dominated the market due to their extensive deployment in large-scale surface mining operations.

- Semi-autonomous systems held the leading share by automation level, supported by their cost-effective and phased adoption approach.

North America

North America Led the market with strong adoption of AI, autonomous haulage systems, and advanced mining technologies.

Europe

Europe Growth is supported by sustainability initiatives, electrified underground mining, and innovation in autonomous solutions.

Asia Pacific

Asia Pacific Fastest-growing region, driven by expanding mining activities, smart mining investments, and increasing automation adoption.

U.S.

U.S. Strong investment in AI-powered mining equipment and autonomous operations continues to support market growth.

Japan

Japan Japan is advancing robotics, automation technologies, and smart industrial solutions that support innovation in mining applications.

Read More

MINING ROBOTICS MARKET TRENDS

Fully Autonomous Vehicles to Gain Market Momentum Owing to Worker Safety and Enhanced Productivity

Shift towards fully autonomous robotics is fully driven by the need to enhance worker safety, as mining environments. By deploying autonomous haul trucks, drilling rigs, and robotic loaders, companies can operate continuously without exposing personnel to these dangers. By deploying autonomous haul trucks, drilling rigs, and robotic loaders, companies can operate continuously without exposing personnel to these dangers. Zero-entry mines offer substantial productivity and efficiency gains, as autonomous systems can function continuously with optimized routes, minimal downtime, and reduced human error. These systems are increasingly integrated into connected ecosystems, where multiple robotic units communicate and coordinate tasks with real-time data.

- For example, in November 2024, ADR secured USD 2 million funding to scale production of autonomous mine-monitoring robots. These robots collect real-time data in hazardous environments without interrupting operations.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Continuous and High-Productivity Operations to Accelerate the Market Growth

The rising demand for continuous and high-productivity operations is a key driver accelerating the adoption across global mining sites. Mining companies are increasingly shifting toward continuous operational models to maximize output and meet the growing global demand for minerals such as copper, lithium, and iron ore.

In traditional mining setups, productivity is often limited by human limitations, including safety-related issues, shift changes, health hazards, etc. Robotics helps overcome these challenges by enabling uninterrupted operations with consistent performance levels.

As commodity demand rises and margins become increasingly competitive, mining companies face further pressure to produce more with fewer resources, making high-productivity robotic solutions a strategic necessity.

- For instance, in 2024, Sandvik acquired Australia-based Universal Field Robots to expand interoperability of its AutoMine platform. The acquisition enhances the integration of diverse robotic systems across mining fleets.

MARKET RESTRAINTS

Long Lead Times in Investment Casting Process and High Volume of Manufacturing Environments to Limit the Market Growth

The investment casting process is inherently time-intensive due to its multi-stage and sequential production workflow. Industries requiring rapid turnaround or mass production often find investment casting less suitable compared to faster alternatives. As a result, long lead times act as a significant barrier, particularly in time-sensitive and high-volume manufacturing environments.

MARKET OPPORTUNITIES

AI-Driven Predictive and Self-Optimizing Systems Target to Accelerate the Market Growth

The emergence of AI-driven predictive and self-optimizing system acts as a significant market opportunity for the mining robotics market growth, as companies seek to move towards intelligent and data driven operations. Traditional mining equipment operates on predefined instructions, whereas AI-enabled systems can analyze real-time data, predict failures, and optimize performance autonomously, unlocking substantial efficiency gains.

The integration of AI with digital twins and advanced analytics platforms allows mining companies to simulate operations, test scenarios, and optimize mine planning before execution. This creates new revenue streams for technology providers offering software, analytics, and AI-as-a-service solutions.

MARKET CHALLENGES

Workforce and Knowledge Skill Gaps to Act as Market Challenges

Traditional mining roles are largely focused on humanly equipment handling, whereas robotic mining requires expertise in areas such as AI, machine learning, sensor integration, and remote operations. Knowledge and skill gap among the traditional workforce might pose a gap between existing workforce capabilities and the skills needed to operate and maintain autonomous systems.

Segmentation Analysis

By Equipment Type

Autonomous Haulage Systems Takes the Lead in the Market Owing to their Large-Scale Extensive Application

Based on the equipment type, the market is divided into autonomous haulage systems, robotic drilling systems, Load-Haul-Dump (LHD) robots, robotic excavators, underground mining robots, and others.

Autonomous haulage systems to dominated the mining robotics market share in 2025 and they are also set to dominate market revenue due to their large-scale deployment in surface mining operations, particularly in iron ore, copper, and coal mines. These systems involve high-value capital equipment such as autonomous haul trucks integrated with advanced fleet management software, significantly increasing their revenue contribution. As mining companies increasingly prioritize safety and cost optimization, AHS continues to remain the largest revenue-generating segment in the market.

Underground mining robots are projected to witness the highest growth rate of about 16.5% due to increasing safety concerns and the complexity of underground environments. These robots are designed to operate in hazardous conditions such as confined spaces, unstable terrain, and low-visibility zones, where human intervention poses significant risks. Technological advancements in AI, LiDAR, and autonomous navigation and improved communication infrastructure are set to support real-time control and data transmission.

By Operation Mode

Semi-Autonomous Robotics Leads the Market Owing To Their Lower Upfront Investment And Usage in Complex And Variable Mining Environments

Based on operation mode, the market is segmented into fully autonomous, semi-autonomous, and remote-controlled.

Semi-autonomous systems dominate the market as they strike a balance between automation and human control. These systems allow operators to supervise and intervene when necessary, making them more practical for complex and variable mining environments. They require lower upfront investment compared to fully autonomous solutions, enabling easier adoption across mid- to large-scale mining operations. Additionally, many mining companies prefer a phased automation approach, where semi-autonomous systems act as a transitional step toward full autonomy.

Fully autonomous systems are expected to witness the highest growth rate of about 15.3% due to increasing demand for zero-human intervention in hazardous mining environments. These systems operate independently using advanced AI, sensors, and real-time analytics, significantly improving safety and productivity. Growing labor shortages and rising cost pressures are accelerating the shift toward complete automation.

By Application

To know how our report can help streamline your business, Speak to Analyst

Need for Continuous and High-Volume Material Handling Makes Material Handling the Leading Application

Based on application, the market is segmented into drilling & blasting, material handling, excavation & loading, underground mining operations, exploration & surveying, inspection & monitoring, and others.

Material handling dominates the market due to its extensive application across both surface and underground mining operations. Activities such as hauling, transportation, and ore movement are continuous and high-volume, making them ideal for automation through robotic systems like autonomous trucks and conveyor solutions. These operations directly impact productivity and cost efficiency, driving strong investment from mining companies.

Underground mining operations are expected to witness the highest growth rate of about 17.1% due to increasing focus on safety and operational efficiency in hazardous environments. Robotics are increasingly being deployed for drilling, hauling, and navigation in confined and high-risk underground settings, reducing human exposure. The growing demand for critical minerals and deeper ore extraction is further accelerating automation in underground mines.

Mining Robotics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Mining Robotics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America leads the market due to early adoption of automation, AI, and autonomous haulage systems, particularly in the U.S. and Canada. Large mining has strong capital budgets, enabling deployment of high-cost robotic fleets and retrofits. The region benefits from advanced digital infrastructure, strong OEM presence and established mining technology ecosystems. Safety regulations and labor cost pressures further accelerate automation adoption. Additionally, high penetration of autonomous drilling, hauling, and monitoring systems contributes to revenue dominance. Retrofit demand for existing fleets is also significant.

U.S. Mining Robotics Market

The U.S. dominates due to technological leadership in AI, robotics, and autonomous systems. Large mining firms are increasingly deploying autonomous haul trucks and drilling systems to improve productivity. High wages and labor shortages create strong economic justification for automation. Government support for critical minerals is accelerating investment in advanced mining technologies.

Europe

Europe’s market is driven by sustainability mandates and strict environmental regulations, particularly in Nordic countries. The region focuses heavily on electrified and autonomous underground mining, with companies investing in zero-emission robotic solutions. While mining activity is smaller compared to other regions, Europe leads in technology innovation and pilot deployments. OEMs and technology providers emphasize precision mining, remote operations, and digital twins.

U.K. Mining Robotics Market

The U.K. market in 2026 will reach a value of USD 0.05 billion, representing roughly 3.2% of global market revenues.

Germany Mining Robotics Market

Germany’s market will reach USD 0.07 billion in 2026, equivalent to around 3.9% of the global sales.

Asia Pacific

Asia Pacific is the fastest-growing region due to large-scale mining operations in China, Australia, and India. Australia is a global leader in fully autonomous mining operations, particularly in iron ore, while China is rapidly investing in AI-driven smart mining initiatives. The region benefits from high demand for commodities and increasing pressure to improve efficiency and safety in hazardous environments. Governments are actively promoting smart mining and digital transformation, accelerating robotics adoption. Lower current penetration compared to North America creates strong growth headroom.

India Mining Robotics Market

The Indian market, in 2026, will be valued at USD 0.13 billion, accounting for roughly 7.3% of the global market.

China Mining Robotics Market

China’s market is projected to remain dominant in the Asia Pacific region in 2026, with revenues reaching USD 0.18 billion, representing roughly 10.6% of global sales.

ASEAN Mining Robotics Market

The ASEAN market in 2026 will reach a value of USD 0.04 billion, accounting for roughly 2.2% of revenue.

South America

South America, led by Chile, Peru, and Brazil, is a key mining hub for copper, lithium, and iron ore. The region is gradually adopting mining robotics to improve operational efficiency and worker safety, particularly in large open-pit mines. Chile is at the forefront, with strong investments in autonomous haulage and remote operation centers.

Mining companies are investing in robotics to improve efficiency in high-altitude and remote operations. Increasing global demand for energy transition minerals is accelerating modernization. Adoption is supported by partnerships with global OEMs and technology providers. However, adoption is moderated by capex constraints, infrastructure limitations, and regulatory variability. Global mining companies operating in the region are key drivers of technology deployment.

Brazil Mining Robotics Market

The Brazil market will reach USD 0.09 billion in 2026, representing roughly 5.1% of the global market

Middle East and Africa

The Middle East & Africa region, even though in early adoption phase, shows strong long-term potential. Africa hosts vast mineral reserves, but adoption of robotics is limited due to its infrastructure gaps and capital constraints. However, South Africa is increasingly adopting automation in deep mining operations for safety improvements. In the Middle East, mining diversification strategies are driving investment in modern, automated mining technologies. International mining firms are introducing robotics in large projects, especially for remote monitoring and semi-autonomous operations.

GCC Mining Robotics Market

The GCC market will reach USD 0.04 billion in 2026, representing roughly 2.4% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches and Integration Of Technology To Propel The Key Players’ Market Penetration

Key players in the mining robotics market are adopting a multi-pronged strategy focused on automation scale-up, technology integration, and ecosystem partnerships to gain competitive advantage. A primary strategy is the development and commercialization of fully autonomous mining systems, including haulage, drilling, and loading, moving beyond pilot projects to large-scale deployments. Companies are heavily investing in AI, machine learning, and computer vision to enhance real-time decision-making, predictive maintenance, and operational efficiency. Strategic partnerships with mining companies are critical, enabling co-development and faster on-site validation of robotic solutions.

- For instance, in 2025, MineSense deployed shovel-mounted sensors enabling real-time ore classification. The system integrates robotics and AI to improve ore recovery and reduce waste. It delivers measurable cost savings and efficiency gains in copper mining.

LIST OF KEY MINING ROBOTICS MARKET COMPANIES PROFILED

- Caterpillar Inc. (U.S.)

- Komatsu Ltd. (Japan)

- Hitachi Construction Machinery Co., Ltd. (Japan)

- ABB Ltd (Sweden)

- Hexagon AB (Sweden)

- Autonomous Solutions Inc. (U.S.)

- Epiroc AB (Sweden)

- Sandvik AB (Sweden)

- Built Robotics (U.S.)

- Atlas Copco (Sweden)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Schneider Electric is deploying EcoStruxure platforms, combining AI, IoT, and robotics for mining operations. The system optimizes energy use and automates decision-making across robotic fleets.

- May 2025: Hexagon is enhancing robotic mine planning and safety systems using automation and radar-based monitoring. The solution integrates robotics with real-time analytics to improve worker safety and productivity.

- April 2025: Epiroc is advancing autonomous drill rigs with precision GPS and sensor-based control systems. These robotic drills improve ore extraction accuracy and reduce manual intervention.

- February 2025: Caterpillar continues expanding its MineStar autonomous haulage and fleet management systems globally. The platform integrates AI, sensors, and robotics for real-time decision-making.

- March 2024: Sandvik acquired Australia-based Universal Field Robots to expand interoperability of its AutoMine platform. The acquisition enhances integration of diverse robotic systems across mining fleets.

REPORT COVERAGE

The global mining robotics market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Equipment Type, Operation Mode, By Application, and Region |

| By Equipment Type |

|

| By Operation Mode |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.51 billion in 2025 and is projected to reach USD 5.08 billion by 2034.

In 2025, the market value stood at USD 0.46 billion.

The market is expected to exhibit a CAGR of 14.5%during the forecast period.

By equipment type, the autonomous haulage system to dominate the market revenue.

Growing demand for continuous and high-productivity operations to accelerate the market growth.

Caterpillar Inc., Sandvik AB, and Komatsu Ltd., are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us