Missile Approach Warning (MAW) Systems Market Size, Share & Industry Analysis, By Platform (Fighter Aircraft, Transport/Tanker Aircraft, Special Mission & ISR Aircraft, Helicopters, UAS/UCAV, and Other), By Technology (Passive UV (solar-blind) MAWS, Imaging IR/dual-color IR, RF/radar-based (incl. compact pulse-Doppler), and Multispectral fused (UV+IR/IR+RF)), By Wavelength Band (Solar-blind UV (≈240–280 nm), MWIR (3–5 µm) imaging, and LWIR (8–12 µm) imaging), By Coverage, By Integration with Countermeasures, By Installation Type, By Component, By End user, and Regional Forecast, 2026-2034

Missile Approach Warning (MAW) Systems Market Size and Future Outlook

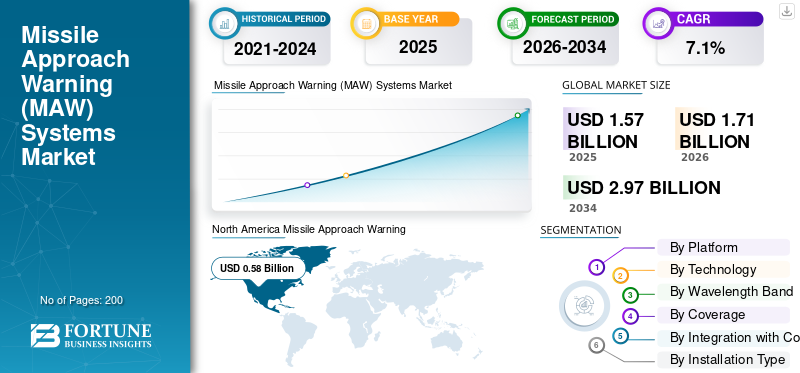

The global Missile Approach Warning (MAW) systems market size was valued at USD 1.57 billion in 2025. The market is projected to grow from USD 1.71 billion in 2026 to USD 2.97 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period. North America dominated the global market with a share of 36.94% in 2025.

Missile approach warning (MAW) systems are self-protecting systems designed to detect incoming missiles, warn platform operators, and cue the deployment of countermeasures. These systems are integrated on platforms such as fighter aircraft, transport aircraft, helicopters, UAVs, ground vehicles, and naval vessels to self-protect from missile attacks, particularly from man-portable air-defense systems (MANPADS). Increasing defense budgets and growing threats from MANPADS and SHORD make the integration of these systems mandatory in aerial platforms and ground and naval platforms, driving market growth.

Key players in the market include Northrop Grumman, BAE Systems, Elbit Systems, Leonardo, Thales, Saab AB, Hensoldt, and RTX. These companies supply MAW systems as part of wider self-protection suits. Elbit’s PAWS-2 HR and Leonardo’s MAIR systems both use high-resolution, multi-aperture imaging sensors to provide 360-degree coverage around the aircraft and, through real-time processing, detect and track missile attacks, automatically cueing countermeasures.

Download Free sample to learn more about this report.

MISSILE APPROACH WARNING SYSTEMS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.57 billion

- 2026 Market Size: USD 1.71 billion

- 2034 Forecast Market Size: USD 2.97 billion

- CAGR: 7.10% from 2026–2034

- North America dominated the market with a 36.94% share in 2025.

- The Helicopters segment is expected to dominate the market in 2026.

- The Air Forces segment is expected to dominate the market in 2026.

North America

The market reached USD 0.58 billion in 2025, driven by large U.S. defense aircraft fleets, increasing investments in aircraft survivability systems, and continuous modernization of missile warning capabilities.

Europe

The market reached USD 0.42 billion in 2025 and is projected to witness steady growth by 2026, supported by rising defense spending, military modernization programs, and increased procurement following the Russia–Ukraine conflict.

Asia Pacific

The market is projected to witness strong growth by 2026, driven by rising defense budgets, geopolitical tensions, expanding military aircraft fleets, and increasing investments in advanced electronic warfare systems.

U.S.

The market is projected to witness steady growth by 2026, supported by extensive deployment of MAW systems across fighter, transport, tanker, and special mission aircraft, along with continued defense modernization initiatives.

Japan

The market is projected to witness steady growth by 2026, driven by rising defense expenditures, regional security concerns, and increasing adoption of advanced aircraft self-protection systems.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing MANPADS and SHORAD Threats Are Forcing Nations to Rapidly Adopt Missile Approach Warning Systems

Active and increasing use of man-portable air defense systems and short-range air defense (SHORAD) in conflict zones and in the hands of non-state users has made low-altitude operation more dangerous for helicopters, transports, and special mission aircraft. National operators now treat missile approach warning systems as a core survivability capability instead of an optional upgrade, integrating MAW sensors with countermeasures dispensers and DIRCM in new and retrofit self-protection suits. This threat environment is pushing fleets to accelerate missile attack warning upgrades across both old and new platforms.

MARKET RESTRAINTS

Complex Integration, Safety, and Airworthiness Requirements Hinder the MAWs' Deployment

Missile approach warning systems are not simple to integrate on any platform. These systems bring lasers, flares, new wiring, extra power draw, and complex software logic into already complex airframes. They have to follow every weight/Power/space limit, prove safe flare trajectories, laser eye-skin safety, and ensure full airworthiness and flight-test campaigns. This results in additional time, engineering efforts, and certification risks, which slow Missile Approach Warning (MAW) systems market growth.

- For instance, in December 2023, the U.S. Government Accountability Office reported that upgrading of the F-35’s onboard systems (the Block 4 hardware/software upgrade set) led to development costs growing from USD 10.6 billion to USD 16.5 billion and the completion date slipping from 2026 to 2029, highlighting how integrating new advanced electronic capabilities on combat aircraft drives cost and schedule overruns.

MARKET OPPORTUNITIES

Strategic Transports, Tankers, and VIP Wide bodies are emerging as a High-Growth Warning Upgrades Segments

Apart from fighter and attack helicopters, the next major opportunity for Missile Approach Warning (MAW) systems lies in large transports, tankers, and VIP/civil wide-body aircraft that routinely operate into or over volatile regions. Governments are focusing on hardening strategic airlift programs and head-of-state fleets against MANPADS, and certification progress for podded MAW and DIRCM solutions on commercial airframes has removed many historical regulatory barriers. As more air forces and government operators modernize A330 MRTTs, A400Ms, C-17, and others with VIP A330/A350/Boeing fleets, they effectively open a multi-platform retrofit pipeline for integrated missile warning and laser jamming suites.

- For instance, in July 2025, Elbit Systems announced a USD 260 million contract from Airbus Defence and Space to supply its J-MUSIC DIRCM self-protection systems for the German Air Force A400M transport fleet, explicitly aimed at protecting these strategic airlift aircraft against IR-guided missile threats.

Missile Approach Warning (MAW) SystemsMARKET TRENDS

Imaging, Multi-Spectral, and Distributed-Aperture Threat Warning is Redefining Missile Approach Warning Systems

The market is transitioning from simple UV-only detectors to imaging, multispectral, distributed-aperture threat warning suites that also function as hostile-fire sensors and situational awareness cameras. New systems fuse multiple IR/UV sensors around the airframe, run high-speed digital embedded AI/ML, and feed precise tracks to DIRCM and expendable countermeasures, turning MAW from a single-function box into the core sensor of the defensive aids suite.

- For instance, in October 2024, BAE Systems completed delivery of 400 2-Color Advanced Warning Systems (2CAWS) to the U.S. Army under the LIMWS quick-reaction program. The system uses modern multispectral sensors, a high-speed digital backbone, and machine-learning algorithms to detect threats and cue laser/expendable countermeasures on utility, heavy-lift, and attack helicopters.

MARKET CHALLENGES

Strict Export Rules to Hinder Market Growth

Missile approach warning systems and DIRCM suits are two main layers of electronic warfare, resulting there’s tight control around this technology (ITAR, AECA, and national munitions lists). Every export or technology transfer deal has to clear tight licensing, limits on third-country nationals, and re-export restrictions, and many air-forces insist on self-governing source code, local integration rights, and ITAR Free or ITAR light options, restraining market growth.

- For instance, in January 2025, the U.S. State Department’s Bureau of Political-Military Affairs emphasized that, under the Arms Export Control Act (AECA) and International Traffic in Arms Regulations (ITAR), defense export controls are an important tool to protect technologies that offer a vital military or intelligence advantage. They specifically framed strict controls as a deliberate policy instead of just an administrative burden.

Russia-Ukraine War Impact

Modernization Cycles and NATO Rearmament Boost Demand for Missile Approach Warning (WAW) Systems

Conflict has made nations believe the battlefield is saturated with MANPADS and layered SHORAD, where any aircraft flying low to medium altitude becomes a target. Both sides have faced heavy helicopter and fixed-wing losses to ground-based air defense, and analysts now treat dense, mobile SAM/MANPADS belts as the new normal rather than the niche threat. As a result, air forces and army aviation branches, especially in Europe and along NATO’s eastern flank, are rethinking survivability, accelerating funding for aircraft self-protection, and pushing for more capable missile approach warning, DIRCM, and integrated EW suits on everything from attack helicopters to transports and ISR platforms.

- For instance, in August 2023, Newsweek reported that Dutch open-source intelligence outlet Oryx had visually confirmed over 100 Russian helicopter losses (at least 101 helicopters) since the start of the full-scale invasion of Ukraine, illustrating the scale of rotary-wing attrition in a MANPADS- and SHORAD-saturated environment.

- For instance, in April 2025, the Stockholm International Peace Research Institute (SIPRI) reported that world military expenditure reached a record USD 2.72 trillion in 2024, with European defense budgets rising sharply as governments reacted to Russia’s invasion of Ukraine by rearming and hardening their forces against the Russian threat.

Download Free sample to learn more about this report.

Segmentation Analysis

By Platform

High-Risk Low-Altitude Missions Make Helicopters the Dominant Segment

In terms of platform, the market is categorized into fighter aircraft, transport/tanker aircraft, helicopters, special mission & ISR aircraft, UAS/UCAV, and others.

The helicopters segment held the largest market share in 2025. Helicopters spend most of their time in MANPADS/SHORAD engagement envelop flying low, slow, and close to the fight. Attack, utility, and heavy-lift rotorcraft have to perform missions such as troop lift, CAS, MEDEVAC, and SOF missions over challenging terrain, making them prime targets for IR-guided missiles. As a result, army aviation units across the globe have prioritized MAW integration across all frontline helicopter fleets, driving higher system counts and retrofit demand than in any other platform category.

The others segment consists of ground vehicles, naval vessels, and business/vvip & commercial derivatives.

The UAS/UCAV is expected to grow at a CAGR of 13.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Passive Solar-Blind UV MAWS Segment Leads owing to its Popularity

On the basis of technology, the market is classified into Passive UV (solar-blind) MAWS, imaging IR/dual-color IR, RF/radar-based (incl. compact pulse-Doppler), and multispectral fused (UV+IR / IR+RF).

The Passive UV (solar-blind) MAWS holds the largest market share. The dominance of this segment is attributed to the fact that these systems have been fielded at scale for the longest time. Systems such as older UV-based missile warning and common missile warning suites have been installed on 1000+ of helicopters, transports, and fixed-wing combat aircraft across the U.S., NATO, and allied fleets. Although newer imaging IR and multispectral solutions are becoming more popular, the large number of already-deployed systems and ongoing retrofit programs based on established UV detectors keep this segment in the lead for now.

For instance, in June 2023, BAE Systems stated that its AN/AAR-57 Common Missile Warning System (CMWS), a passive missile warning and hostile fire detection suite based on solar-blind UV sensors, has been installed on more than 40 different aircraft types and over 2,500 platforms worldwide.

The Multispectral fused (UV+IR / IR+RF) is the fastest-growing segment in the market and is expected to grow at a CAGR of 12.0% over the forecast period.

By Wavelength Band

Solar-Blind UV (≈240–280 nm) Segment Leads due to its Ability to detect Rocket Motor Plumes

Based on wavelength Band, the market is segmented into Solar-blind UV (≈240–280 nm), MWIR (3–5 µm) imaging, and LWIR (8–12 µm) imaging.

The solar-blind UV (240 to 280 nm) segment dominates the missile approach warning systems market. Most legacy and current MAWS fleets use UV sensors designed for this range. These solar-blind detectors detect rocket motor plumes in a spectrum with low natural background noise. This feature has made them the preferred option for helicopters, transports, and tactical aircraft. Although MWIR and LWIR imaging solutions are increasing, the high number of deployed and newly ordered UV-based systems maintains this segment's dominance during the forecast period.

The LWIR (8–12 µm) imaging is the fastest-growing segment in the market and is expected to grow at a CAGR of 11.5% throughout the forecast period.

By Coverage

Distributed Aperture (Multi-sensor 360°) Segment Dominates the Market due to Accurate Threat Localization Capability

Based on coverage, the market is segmented into distributed aperture (multi-sensor 360°), Sector/single-head coverage, and Federated via central EW controller.

Distributed aperture (multi-sensor 360°) is the leading segment as modern survivability systems focus on full-sphere awareness instead of just narrow sector protection. Multiple MAWS sensors are now installed around the airframe, offering continuous 360° coverage, accurate threat localization, and strong clutter rejection. These features are crucial for effectively guiding DIRCM, smart flares, and connected EW functions. As operators move from older single-head/sector systems to integrated multi-sensor configurations on helicopters, transports, and special-mission platforms, distributed aperture configurations are capturing a larger share of new installations and mid-life retrofits.

For instance, in October 2024, the UK Royal Air Force reported live-fire trials of a new self-protection system. Thales’ Elix-IR threat warning system, which uses multiple sensors to provide full 360° missile and hostile-fire detection around the aircraft, was integrated with Leonardo’s Miysis DIRCM. This combination achieved a 100% interception rate against infrared-guided missiles during tests.

The Federated via central EW controller segment is expected to grow at a CAGR of 8.8% during the forecast period.

By Integration with Countermeasures

MAWS + CMDS (Flares/Chaff) Cueing Dominated the Segment Due to Its Large Installed Base

Based on integration with countermeasures, the market is segmented into MAWS + CMDS (flares/chaff) cueing, MAWS + DIRCM (laser jamming) cueing, and MAWS + towed decoy/ECM suite orchestration.

The MAWS and CMDS (flares/chaff) cueing segment dominates the market in 2025. It is the standard self-protection system for most helicopters, transports, and tactical aircraft worldwide. In practice, missile warning sensors provide threat data to an airborne countermeasures dispenser system (CMDS, which then automatically chooses and launches decoys against infrared (IR) and radio frequency (RF) threats. DIRCM and towed decoy/ECM orchestration are increasing at the high end. However, the large number of platforms that use MAWS-driven flare/chaff dispensers results in this system’s dominance due to its large installed base and short-term retrofit volumes.

The MAWS + DIRCM (laser jamming) cueing segment is set to grow at a CAGR of 12.2% during the forecast period.

By Installation Type

Continuous Cockpit or Avionics Upgrades Make Retrofit/MRO & Sustainment the Dominant Segment

By installation type, the market is divided into Line-fit/OEM and Retrofit/MRO & sustainment upgrades.

Retrofit/MRO & sustainment upgrades capture the key missile approach warning (MAW) systems market share. Most demand comes from operators adding MAWS-based self-protection suites to large, existing fleets of helicopters, transports, and special-mission aircraft. New-build line-fit or OEM integrations are growing, but they originate from a much smaller base. In contrast, every life-extension program, cockpit or avionics upgrade, or electronic warfare modernization efforts on older airframes naturally lead to retrofitting MAWS, countermeasure dispensers, and sometimes DIRCM. This trend keeps retrofit work ahead in both volume and contract value.

Line-fit/OEM is set to grow at a CAGR of 9.3% during the forecast period.

By Component

Sensor/Optics Segment Leads the Market due to an Increase in Geopolitical Tensions

Market is segmented by component into Sensors/Optics, processing units & software, EW integration hardware, HMI/Alerting & Recording, and lifecycle services.

Sensors/optics dominate the missile approach warning systems market, holding around 39% of the total market share. Sensors and optics play an important role, as their high-sensitivity electro-optic heads detect and track the heat signature of incoming missiles before impact, mainly in dense man-portable air defense systems (MANPADS) environments. As geopolitical tensions rise and defense budgets increase in the Asia Pacific, the Middle East and Africa, and Latin America, air forces are prioritizing sensor updates. This move aims to strengthen defense capabilities in response to evolving missile threat environments, driving segment growth.

Processing Units & Software is set to grow at a CAGR of 9.7% during the forecast period.

By End User

Ability to Provide Protection from Missile Attacks in Challenged Airspace Boosted the Air Forces Segment Growth

By end-user, the market is segmented into air forces, army aviation & HLS/Paramilitary, naval aviation, and Government/VVIP operators.

Air Forces dominated the missile approach warning systems market in 2025. They manage the largest and most valuable mix of fighter jets, transport and tanker fleets, and special mission and ISR aircraft, all of which need protection from missile attacks in challenged airspace. These platforms are key targets for man-portable air defense systems (MANPADS) and radar-guided threats. As a result, air forces are investing significantly in missile approach warning (MAW) systems that can detect and track the heat signature of incoming missiles.

Army Aviation & HLS/Paramilitary is set to grow at a CAGR of 7.9% during the forecast period.

Missile Approach Warning (MAW) Systems Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America held the dominant share in 2024, valued at USD 0.54 billion, and maintained its lead in 2025 with USD 0.58 billion, led primarily by the U.S., which alone contributes 93.31% of the regional market. U.S. defense forces operate large fleets of valuable fighters, transports, tankers, and special-mission aircraft. These aircraft need protection from missile attacks and threats from man-portable air defense systems (MANPADS) and more complex surface-to-air missiles (SAMs).

North America Missile Approach Warning (MAW) Systems Market Size,2025,(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific and Europe

Asia Pacific and Europe are expected to witness significant growth in the Missile Approach Warning (MAW) systems market in the coming years. During the forecast period, Europe is projected to grow at a CAGR of 7.3%. The market in Europe is estimated to be USD 0.42 billion in 2025, driven directly by the Russia-Ukraine war and the resulting re-armament cycle. In this region, both the U.K. and France are expected to reach USD 0.08 billion and USD 0.07 billion, respectively, in 2026. In Asia Pacific, countries including China, India, Japan, and South Korea are witnessing rapid growth. According to SIPRI and IISS, there are sharp rises in Asia Pacific defense spending, driven by China’s military build-up, U.S. & China rivalry, Taiwan/South China Sea tensions, and spill-over from conflicts in Ukraine and the Middle East. Based on these factors, countries such as China expect to reach a valuation of USD 0.17 billion, and India is set to reach USD 0.09 billion by 2026.

Rest of the world

The rest of the world (Middle East & Africa and Latin America) contributes approximately 10.68% in 2025. Although these regions have a comparatively smaller share, they are growing at a CAGR of 6.9. SIPRI’s latest data shows fast growth in military spending in the Middle East, along with a steady increase in Africa's defense budgets. This rise is driven by regional tensions, internal security threats, and cross-border instability.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Companies Focus on Technological Advancements to Detect and Track the Heat Signature of Incoming Missiles

Major global electronic warfare companies and a range of regional specialists are pushing rapid growth in the MAWs Market. Leading companies such as Saab AB, Diehl Defence GmbH & Co KG, BAE Systems, RTX, Leonardo, Thales, Elbit Systems, and HENSOLDT provide integrated missile approach warning (MAW) systems. These systems detect and track the heat signature of incoming missiles and automatically activate countermeasures. They form the central part of larger defense aid suites for air and defense forces using fighters, transports, helicopters, UAS/UCAV, and special mission aircraft in increasingly hostile environments filled with missile threats and man-portable air defense systems (MANPADS).

Increasing defense budgets, rising geopolitical tensions, and more contested airspace are driving market growth in North America and Europe. At the same time, Asia Pacific, the Middle East & Africa, and Latin America are becoming major battlegrounds for future contracts. In these regions, governments are rapidly upgrading their defense capabilities in response to evolving threats and are looking to Western solutions as they release tenders for new or updated platforms, drawing more companies into the competitive landscape. Saab AB and Diehl Defence GmbH & Co KG are using missile approach warning systems, directed infrared countermeasures, and electronic warfare integration programs as starting points for broader market growth.

LIST OF KEY MISSILE APPROACH WARNING (MAW) SYSTEMS COMPANIES PROFILED

- BAE Systems (U.K.)

- Saab AB (Sweden)

- Diehl Defence GmbH & Co. KG (Germany)

- Leonardo S.p.A. (Italy)

- Thales Group (France)

- RTX Corporation / Raytheon (U.S.)

- Northrop Grumman (U.S.)

- Elbit Systems Ltd. (Israel)

- HENSOLDT AG (Germany)

- L3Harris Technologies, Inc. (U.S.)

- Airbus (France)

- Israel Aerospace Industries (IAI) (Israel)

- ELTA Systems (Israel)

- ASELSAN A.Ş. (Turkey)

- Bharat Electronics Limited (India)

- Terma A/S (Denmark)

KEY INDUSTRY DEVELOPMENTS

- In June 2025, BAE Systems received a USD 1.2 billion contract from the U.S. Space Systems Command to provide missile tracking satellite capabilities for the U.S. Space Force. BAE Systems would be the main contractor for the Resilient Missile Warning & Tracking (RMWT) Medium Earth Orbit (MEO) Epoch 2 program. They would design and build 10 spacecraft under this agreement. This includes a four-year timeline for delivering the space vehicles, plus an additional five years for operations and support.

- In April 2025, The Economic Times and other Indian business media reported that Bharat Electronics Ltd (BEL) signed a contract worth about approx. USD 266 million (₹2,210 crore) with India’s Ministry of Defense to supply advanced Electronic Warfare (EW) suites for the Indian Air Force’s Mi-17V5 helicopters. The DRDO-designed suites comprise a Radar Warning Receiver (RWR), Missile Approach Warning System (MAWS), and Counter Measure Dispensing System (CMDS).

- In May 2025, Space Systems Command awarded the Future Operationally Resilient Ground Evolution (FORGE) Enterprise OPIR Solution (EOS) contract through a competitive SpEC OTA prototype agreement. EOS would improve the government-owned FORGE framework. It will provide a scalable, cyber-secure ground processing capability. This aims to support the Space Force’s missile warning and tracking mission and speed up solutions for warfighters facing threats.

- In April 2022, Defense Advancement reported that BAE Systems received a USD 22 million U.S. Foreign Military Sales contract to supply its AN/AAR-57 Common Missile Warning System (CMWS) and associated equipment for a fleet of Apache helicopters, providing automatic detection of hostile fire and missile threats and cueing countermeasures.

- In March 2022, HENSOLDT announced that the German Bundeswehr decided to equip its C-130J-30 and KC-130J Hercules fleet with the MILDS Block 2 missile defence system, supplying 35 UV missile warning sensors as part of a package integrated by Terma A/S to close a critical protection gap on the new transports.

REPORT COVERAGE

The global Missile Approach Warning (MAW) Systems market analysis provides an in-depth study of market size, company profiling, and forecast by all segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attributes | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Platform, Technology, Wavelength Band, Coverage, Integration with Countermeasures, Installation Type, Component, End User, and Region |

|

By Platform

|

|

|

By Technology

|

|

|

By Wavelength Band

|

|

|

By Coverage

|

|

|

By Integration with Countermeasures

|

|

|

By Installation Type

|

|

|

By Component

|

|

|

By End User

|

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.71 billion in 2026 and is projected to reach USD 2.97 billion by 2034.

In 2025, the market value stood at USD 0.58 billion.

The market is expected to exhibit a CAGR of 7.1% during the forecast period of 2026-2034.

The helicopters segment led the market by platform.

The key factor driving the market is the increasing MANPADS and SHORAD threats.

BAE Systems (U.K.), Saab AB (Sweden), Diehl Defence GmbH & Co. KG (Germany), Leonardo S.p.A. (Italy), Thales Group (France), RTX Corporation (U.S.), and Northrop Grumman (U.S.) are the top companies in the market.

North America dominated the market in 2024.

- 2021-2034

- 2024

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us