Missile Propulsion Systems Market Size, Share, Industry Analysis and Russia-Ukraine War Impact Analysis, By End-User (Government and Military, Defense Contractors, and Research Institutions & Universities), By Range (Short Range (Below 2 km), Medium Range (2 - 4 km), Long Range (4-8 km), and Extended Range (Above 8 km)), By Propulsion Type (Solid Propulsion, Liquid Propulsion, Hybrid Propulsion, Cryogenic, and Ramjet/Scramjet), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

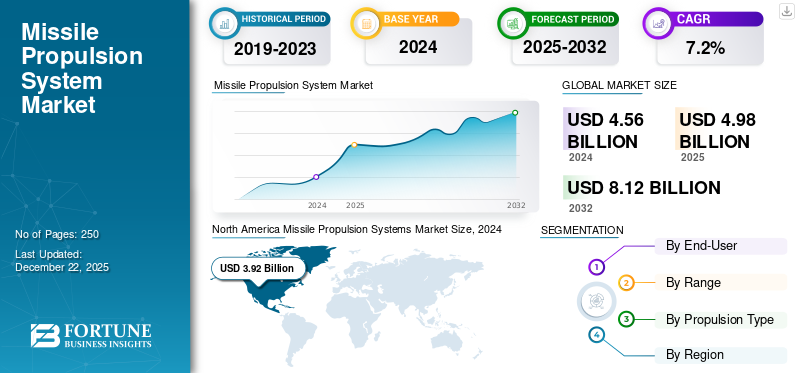

The global missile propulsion systems market size was valued at USD 4.99 billion in 2025. The market is projected to grow from USD 5.23 billion in 2026 to USD 9.3 billion by 2034, exhibiting a CAGR of 7.45% during the forecast period. North America dominated the missile propulsion systems market with a market share of 39.19% in 2025.

Missile propulsion systems are a critical segment within the defense industry, encompassing the development and production of propulsion technologies used in various missile platforms, including ballistic, cruise, and hypersonic missiles. The global market has experienced significant growth driven by increasing defense budgets, technological advancements, and geopolitical tensions.

The COVID-19 pandemic initially disrupted global supply chains, delaying manufacturing and procurement of missile components, including propulsion systems. Lockdowns and restrictions hampered factory operations, leading to delays in R&D, production, and deployment schedules. Budget reallocations in many countries toward healthcare and economic recovery also temporarily slowed defense spending. Despite these setbacks, the pandemic underscored the importance of missile defense capabilities, prompting governments to prioritize modernization efforts once the situation stabilized, reinforcing demand for advanced missile propulsion technologies.

The market is characterized by the participation of several prominent defense contractors and technology providers, including Raytheon Technologies, Northrop Grumman, and MBDA.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

RUSSIA-UKRAINE WAR IMPACT

Technological Innovations to Amplify Missile Propulsion System Demand

The Russia-Ukraine war has profoundly influenced the global missile propulsion systems market growth, reshaping defense priorities, accelerating technological innovation, and prompting strategic shifts among nations. As the conflict continues, its repercussions extend beyond the battlefield, affecting procurement patterns, supply chains, and geopolitical alliances, ultimately driving the evolution of missile technology across the globe.

Increased Defense Spending and Modernization Initiatives - One of the most immediate effects of the war has been a surge in defense budgets across numerous countries. Nations, particularly those in Europe and North America, are reallocating resources to bolster their missile arsenals, emphasizing the development and procurement of advanced missile systems. These systems depend heavily on sophisticated propulsion technologies, ranging from solid and liquid engines to emerging hypersonic propulsion. As threats evolve, countries are prioritizing investments in propulsion systems that offer longer ranges, higher speeds, and greater maneuverability, thereby fueling growth in the market.

Focus on Hypersonic and Advanced Missile Technologies - The conflict has underscored the strategic importance of hypersonic weapons, which can travel at speeds exceeding Mach 5 and evade traditional missile defenses. Russia’s demonstrated capabilities with hypersonic missiles such as the Kinzhal have prompted nations, including the U.S., China, and European countries, to intensify their hypersonic research. Developing hypersonic propulsion, such as scramjets and advanced rocket engines, presents a complex technological challenge. However, the war has accelerated efforts to transition these systems from development to deployment. This has led to increased R&D investments and the formation of strategic alliances aimed at mastering hypersonic propulsion technologies.

MISSILE PROPULSION SYSTEMS MARKET TRENDS

Increasing Defense Budgets to Support Market Expansion

The missile propulsion systems market is experiencing rapid evolution, driven by technological advancements, geopolitical developments, and increasing defense budgets globally. One prominent trend is the rising focus on hypersonic missile propulsion technology, which offers unprecedented speeds (Mach 5 and above) and maneuverability, making missile defense increasingly challenging. Countries such as Russia, China, and the U.S. are investing heavily in developing scramjet engines and other advanced propulsion systems to support hypersonic weapons, indicating a significant shift toward high-speed, long-range missile capabilities.

Another key trend is the push for indigenous and self-reliant missile propulsion solutions. In response to geopolitical tensions and sanctions, many nations are prioritizing domestic R&D efforts to reduce reliance on foreign suppliers. This shift has led to increased collaborations between government agencies and defense contractors to develop advanced propulsion technologies tailored to specific strategic needs. Additionally, the market is also witnessing a move toward greener and more efficient propulsion systems. Innovations in solid and liquid propellants aim to improve fuel efficiency, reduce environmental impact, and enhance missile performance. Electric propulsion and hybrid systems are emerging as areas of interest, especially for smaller tactical missiles and future missile platforms that require greater flexibility and operational efficiency.

MARKET DYNAMICS

MARKET DRIVERS

Geopolitical Instability and Increased Defense Spending to Boost Market Growth

Rising geopolitical tensions, territorial disputes, and the proliferation of advanced weapon systems are significantly driving demand for sophisticated missile technologies. In response, nations are increasingly prioritizing defense capabilities to deter potential threats and maintain strategic advantage. This has led to substantial investment in advanced missile systems and, consequently, the propulsion technologies that power them. Specifically, solid propellant and air-breathing propulsion are being favored for their storage and operational advantages. As continued global unrest persists and the need for long-range, high-precision strike capabilities intensifies, the demand for the product will grow steadily.

Technological Advancements in Missile Propulsion Technologies to Drive Market Growth

Ongoing innovations in missile propulsion technologies are crucial catalysts for market growth. This includes the development of hypersonic propulsion, advanced solid rocket motors with improved performance, and efficient ramjet/scramjet systems. These advancements enable missiles to achieve higher speeds, longer ranges, and greater maneuverability, making them more effective against evolving threats. Furthermore, the push for more efficient and environmentally friendly propellants is spurring intensive research and development efforts. This push is leading to the emergence of innovative solutions that can propel the market forward in the coming years. The race to develop and deploy cutting-edge propulsion systems continues to fuel significant investment and growth.

MARKET RESTRAINTS

High Development Costs & Technological Complexity to Hamper Market Growth

Developing advanced missile propulsion systems is an incredibly expensive and complex undertaking. The R&D phase alone requires significant investment in specialized facilities, equipment, and highly skilled engineers. Overcoming the numerous technological challenges associated with achieving desired performance parameters, such as high thrust-to-weight ratios, extended range, and reliability under extreme conditions, demands extensive testing and iterative design processes.

This high barrier to entry limits the number of players capable of competing in the market, potentially stifling innovation and hindering market growth. Furthermore, the risk of project failure or delays due to unforeseen technical hurdles can deter public and private sector investment and slow down the adoption of new technologies. Developing hypersonic propulsion faces immense material science and engineering challenges, further obstructing market expansion.

MARKET OPPORTUNITIES

Development and Deployment of Hypersonic Missile Propulsion Systems is Boosting Market Growth

The market presents substantial growth opportunities, driven by technological innovation, geopolitical shifts, and increasing defense spending globally. As nations seek to modernize their military arsenals, the demand for advanced missile propulsion solutions is expected to surge, creating a lucrative landscape for manufacturers and developers.

One of the primary opportunities lies in the development and deployment of hypersonic missile propulsion systems. Hypersonic weapons, capable of traveling at speeds exceeding Mach 5, offer strategic advantages such as rapid response times and high maneuverability. Countries such as the U.S., China, and Russia are investing heavily in scramjet engines and other propulsion technologies to gain a technological edge, opening avenues for innovative research, development, and commercialization.

Several factors contribute to the rising demand. First, geopolitical tensions and the perceived need for rapid response capabilities are pushing countries to invest heavily in hypersonic weapons programs. Second, advancements in propulsion technologies, particularly scramjets and ramjets, are making hypersonic flight more achievable and reliable. These advancements are enabling the development of more sophisticated and effective missile systems.

MARKET CHALLENGES

Maintaining Technological Superiority Amid Rapid Innovation to Challenge Market Growth

The market faces the constant challenge of maintaining technological superiority in a rapidly evolving landscape. Competitors are continuously striving to develop more advanced systems with enhanced performance characteristics, such as higher speed, greater range, and improved maneuverability. This necessitates sustained investment in research and development to stay ahead of the curve and avoid technological obsolescence. Moreover, the emergence of new technologies, such as directed energy weapons and advanced air defense systems, poses a challenge to the traditional role of missiles. In response, propulsion systems must evolve to become stealthier, more resistant to countermeasures, and capable of engaging a wider range of targets. Failing to innovate can lead to a loss of market share and diminished competitiveness, with the global race for hypersonic technology being a prime example of this challenge.

Another significant challenge lies in balancing high-performance requirements with cost-effectiveness. While advanced propulsion systems offer superior capabilities, they often come with a high price tag. Military budgets are under constant pressure, forcing manufacturers to find ways to reduce costs without compromising performance. This requires innovative approaches to design, manufacturing, and materials selection. Moreover, the life cycle cost of propulsion systems, including maintenance, repair, and overhaul, must be considered. Developing more reliable and durable systems can reduce these costs, however, it often requires trade-offs in performance or higher upfront investment. As a result, the industry is engaged in a balancing act: delivering affordable yet high-performance propulsion systems that meet evolving defense requirements.

SEGMENTATION ANALYSIS

By End-User

Government and Military Segment Led Due to Rising Geopolitical Conflicts

By end-user, the market is classified into government and military, defense contractors, and research institutions & universities.

The government and military segment led the market accounting for 66.87% market share in 2026. This dominance is primarily driven by rising regional tensions and geopolitical conflicts, prompting governments globally to increase defense budgets to modernize and expand their missile arsenals. Military forces require advanced propulsion systems to develop long-range, high-speed, and maneuverable missile platforms for strategic and tactical applications.

The emphasis on indigenous production and technological self-reliance further boosts demand for domestically developed propulsion solutions. As the largest consumers, the government and military sectors are fueling innovation and growth in missile propulsion technologies to enhance national security and military capabilities.

By Range

Long-Range (4-8 km) Segment Led Market Due to Its Ability to Maintain High Accuracy

By range, the market is classified into short range (below 2 km), medium range (2 - 4 km), long range (4 - 8 km), and extended range (above 8 km).

The long range (4 - 8 km) segment will account for 37.45% market share in 2026. The long-range (4-8 km) segment leads as it strikes the balance between effective engagement distances and manageable missile size and launch platform compatibility, making it suitable for a wide range of military operations. It provides sufficient stand-off distance to minimize risk to operators while maintaining high accuracy.

The extended range (above 8 km) segment is projected to experience the highest CAGR during the forecast period. The growth is driven by advancements in missile technology, increased emphasis on standoff capabilities, and the need for forces to engage targets from safer distances. Growing demand for strategic, long-distance precision strikes in modern warfare is driving the rapid growth of the extended-range segment.

By Propulsion Type

To know how our report can help streamline your business, Speak to Analyst

Solid Propulsion Systems Dominated, Driven by Their Quick Launch Capabilities

Based on propulsion type, the market is divided into solid propulsion, liquid propulsion, hybrid propulsion, cryogenic, and ramjet/scramjet.

The solid propulsion segment is expected to account for 42.91% of the market in 2026. Solid propulsion systems are highly favored in the missile market due to their simplicity, reliability, and quick launch capabilities. They require less maintenance and offer a longer shelf life, making them ideal for military applications, including tactical missiles and ballistic missiles. Governments and defense agencies prefer solid-fuel rockets for their ease of storage, rapid deployment, and lower cost. As geopolitical tensions rise and the need for rapid response systems increases, the demand for solid propulsion continues to grow, driving innovation in composite materials and advanced manufacturing techniques to enhance performance and safety.

The ramjet/scramjet segment is projected to experience the highest CAGR during the forecast period. Ramjet and scramjet propulsion systems are increasingly sought after for their ability to achieve hypersonic speeds, offering strategic advantages in missile technology. These air-breathing engines enable missiles to sustain high velocities over long distances, making them suitable for advanced long-range and tactical applications. Governments are investing in next-generation missile systems, seeing ramjets and scramjets as a key component to maintain technological superiority. As countries focus on hypersonic weapon development, demand for ramjet and scramjet propulsion is expected to rise, driven by the need for faster, more maneuverable, and stealthier missile platforms.

MISSILE PROPULSION SYSTEMS MARKET REGIONAL OUTLOOK

By geography, the market is segmented into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Missile Propulsion Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America held 39.19% of the global market share, reaching a valuation of USD 1.95 billion, and is projected to grow to USD 2.04 billion in 2026, driven by advanced military modernization, technological innovation, and high defense spending, primarily in the U.S. The region's focus on developing next-generation missile technologies, including hypersonic and long-range systems, is a key driver of market growth. Key defense contractors across the U.S. are investing heavily in R&D to enhance propulsion efficiency and reliability. Additionally, ongoing military conflicts and strategic defense initiatives support demand for upgraded missile systems. The region’s strong aerospace infrastructure, government funding, and collaboration between defense and private sectors position North America as a leading hub for missile propulsion technology, with continued growth expected in the coming years. The U.S. market is projected to reach USD 1.88 billion by 2026.

The market in the U.S. is driven by advanced defense research, modernization of existing missile fleets, and strategic military priorities. Leading manufacturers focus on developing high-performance, reliable propulsion technologies for ballistic, cruise, and hypersonic missiles, supported by substantial government defense budgets and innovation initiatives.

Europe

The market in Europe reached USD 1.08 billion in 2025, representing 21.57% of total market revenue, and is projected to reach USD 1.13 billion in 2026. In Europe, the market is experiencing steady growth, supported by NATO defense commitments and ongoing modernization efforts. Countries such as France, the U.K., and Germany are investing in advanced missile technologies, including cruise and ballistic missiles, to enhance national security. The region emphasizes innovation, sustainability, and integration of cutting-edge propulsion systems. European governments often collaborate with private aerospace firms and research institutions to accelerate development and deployment. European defense budgets and strategic partnerships further bolster the region’s commitment to enforcing its missile capabilities. Additionally, government initiatives to develop indigenous missile technologies and adapt to evolving threats contribute to sustained growth. Overall, Europe remains a key player in the global market, focusing on technological advancement and regional security needs. The UK market is projected to reach USD 0.24 billion by 2026, while the Germany market is projected to reach USD 0.18 billion by 2026.

Asia Pacific

Asia Pacific contributed approximately USD 1.36 billion to the global market in 2025, accounting for 27.23% share, and is expected to reach USD 1.44 billion in 2026. In Asia Pacific, the market is experiencing rapid growth, driven by increasing military modernization and geopolitical tensions across countries such as China, India, and South Korea. These nations are investing heavily in advanced missile technologies, including long-range, hypersonic, and ballistic missile systems. Growing defense budgets, regional security concerns, and strategic alliances further boost demand. Local defense manufacturers are expanding capabilities through technology transfer and collaborations. In addition, the region's expanding aerospace industry and proactive government initiatives aimed at bolstering a self-reliant national security ecosystem are key growth drivers. As a result, Asia Pacific is emerging as a significant market for missile propulsion systems, with substantial future growth prospects. The Japan market is projected to reach USD 0.2 billion by 2026, the China market is projected to reach USD 0.49 billion by 2026, and the India market is projected to reach USD 0.3 billion by 2026.

Rest of the World

The Rest of the World market accounted for USD 0.6 billion in 2025, representing 12.01% of the global industry, and is expected to reach USD 0.62 billion in 2026. The market in the Rest of the World includes regions such as the Middle East & Africa and Latin America. These regions are experiencing increased defense spending driven by regional conflicts, security threats, and geopolitical tensions. Countries such as Saudi Arabia, UAE, Brazil, and South Africa are investing in missile modernization and indigenous propulsion technologies to bolster their military capabilities. Growing defense budgets, strategic alliances, and regional security concerns are key market drivers. While the market faces challenges such as technological gaps and budget constraints, ongoing modernization efforts and regional security priorities are expected to foster steady growth in missile propulsion systems across these regions.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Offer Advanced Missile Systems to Meet Evolving Defense Needs

The missile propulsion systems market is dominated by key players such as Raytheon Technologies Corporation, Northrop Grumman Corporation, and Lockheed Martin Corporation, which lead in innovation and technological advancements. Other significant companies include MBDA Missile Systems, MBDA Deutschland GmbH, Rafael Advanced Defense Systems Ltd., and China Academy of Launch Vehicle Technology (CALT), each offering advanced missile systems to meet evolving defense needs. These industry leaders focus on developing lightweight, highly accurate, and versatile missiles capable of defeating modern armored threats. The competitive landscape is driven by increasing defense budgets, technological innovation, and the demand for enhanced battlefield survivability, positioning these key players at the forefront of the global market.

LIST OF KEY MISSILE PROPULSION SYSTEM COMPANIES PROFILED

- Raytheon Technologies Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- MBDA Missile Systems (France)

- MBDA Deutschland GmbH (Germany)

- Rafael Advanced Defense Systems Ltd. (Israel)

- China Academy of Launch Vehicle Technology (CALT) (China)

- ISRO Propulsion Complex (IPRC) (India)

- Korea Aerospace Industries (KAI) (South Korea)

- Aerojet Rocketdyne Holdings, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025 - Kratos Defense & Security Solutions, Inc., a technology firm specializing in defense, national security, and global markets, along with GE Aerospace, declared a formal partnership aimed at enhancing propulsion technologies for the forthcoming generation of cost-effective unmanned aerial systems and Collaborative Combat Aircraft (CCA-type) aircraft.

- February 2025 - The strategic partnership between India and the U.K. made significant progress with the official initiation of the Defence Partnership–India (DP-I). This initiative marks a major step forward in bilateral collaboration, particularly focusing on the joint development of next-generation weapon systems.

- June 2024 - Vaya Space, a company specializing in space and defense, entered into a Cooperative Research and Development Agreement (CRADA) with the U.S. Army Combat Capabilities Development Command Aviation and Missile Center (DEVCOM AvMC). This agreement aims to explore the application of Vaya Space's vortex hybrid propulsion technology in a scale representative of a surface-to-surface missile, potentially enhancing future U.S. defense capabilities.

- May 2024 - Japanese technology will be utilized for the rocket engines and propulsion systems of hypersonic missiles being developed under the Glide Phase Interceptor Cooperative Development Project Arrangement, which has been signed by the U.S. Department of Defense and Japan’s Ministry of Defense.

- July 2022 - Rolls-Royce and Safran Power Units entered into a collaborative Assessment Phase contract with MBDA, as part of the Franco-British Future Cruise/Anti-Ship Weapon (FC/ASW) program. The two partners would work together to develop an advanced propulsion solution for a subsonic, low observable missile that is anticipated to be deployed by the end of 2030.

REPORT COVERAGE

This missile propulsion systems research report offers a comprehensive market analysis, identifying key players, end-users, ranges, and propulsion types. It also details market trends and significant industry developments. Moreover, the report highlights various factors that have fueled the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.45% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By End-User

|

|

By Range

|

|

|

By Propulsion Type

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 5.23 billion in 2026 and is estimated to reach USD 9.3 billion by 2034.

The market will grow at a CAGR of 7.45% during the projection period (2026-2034).

By end-user, the government and military segment led the market.

Raytheon Technologies Corporation (U.S.), Northrop Grumman Corporation (U.S.), Lockheed Martin Corporation (U.S.), MBDA Missile Systems (France), and MBDA Deutschland GmbH (Germany) are some of the major players in the market.

North America dominates the market.

Asia Pacific is the fastest-growing region in the global market.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us