Mobile Clinics Market Size, Share & Industry Analysis, By Clinic Type (Primary Care Mobile Clinics, Dental Mobile Clinics, Diagnostic & Screening Mobile Clinics, Maternal & Child Health Mobile Clinics, Specialty Care Mobile Clinics, and Others), By Application (Primary Healthcare, Dental Care, Chronic Disease Management, Infectious Disease Screening & Vaccination, and Others), By End-user (Hospitals & Health Systems, Government & Public Health Agencies, Academic & Research Institutions, Non-governmental Organizations (NGOs) / Non-profits, and Others), and Regional Forecast, 2026-2034

Mobile Clinics Market Size and Future Outlook

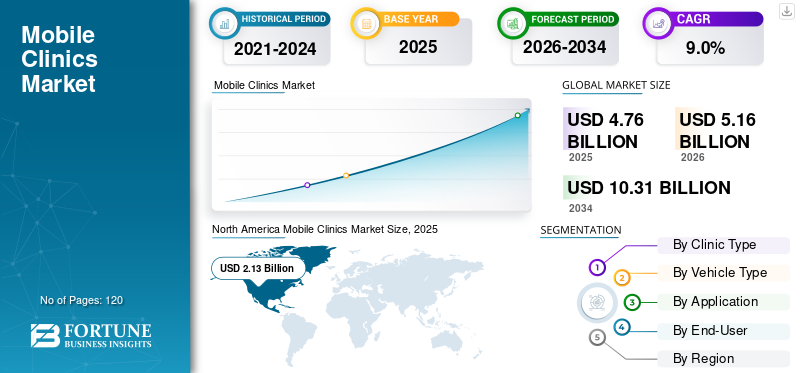

The global mobile clinics market size was valued at USD 4.76 billion in 2025 and is projected to grow from USD 5.16 billion in 2026 to USD 10.31 billion by 2034, exhibiting a CAGR of 9.0% during the forecast period. North America dominated the mobile clinics market with a market share of 41.38% in 2025.

Mobile clinics are healthcare units built into vans, buses, trucks, or similar vehicles that travel to communities and deliver medical services where people live or work. They are used for primary care, screening, maternal and child health, vaccination, diagnostics, and health education. The market growth is attributed to the rising emphasis on expanding healthcare access, and extensive investments for consolidation of healthcare services. In addition, mobile clinics help reduce travel barriers, reach people earlier, and support preventive care. They are also useful for hospitals and health systems that want to expand outreach without building a full permanent facility.

- For instance, in February 2024, the Indian Ministry of Health & Family Welfare announced the launch of mobile health services in the state of Gujarat and Maharashtra.

Furthermore, key industry players operating in the market are Mobile Health, Mission Mobile Medical, TELUS Health for Good, InHealth Group, and UK Screening Solutions. These companies are focusing on developing various innovative technologies to offer better products with improved accuracy and efficiency.

Download Free sample to learn more about this report.

MOBILE CLINICS MARKET TRENDS

Institutionalization of Mobile Clinics Within Formal Healthcare Systems

Mobile medical units are gradually shifting from being temporary or charity-based initiatives to becoming structured parts of healthcare delivery systems. Moreover, hospitals, health systems, and government programs are integrating mobile units into their regular operations for outreach, screening, and follow-up care. Instead of standalone services, these clinics are increasingly linked with hospital networks, electronic records, and referral pathways. This makes them more reliable and scalable. The focus is moving toward continuity of care rather than one-time visits. This shift indicates that mobile clinical units are no longer just access tools, but are becoming embedded within mainstream healthcare infrastructure.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Outreach-Based Healthcare Models to Accelerate Market Growth

Healthcare delivery is gradually moving beyond hospital walls, especially for preventive care and early diagnosis. In addition, mobile clinics are becoming a practical extension of hospital and public health systems to reach populations that are either geographically remote or economically underserved. Moreover, governments and private healthcare providers are actively investing in outreach programs to improve the coverage of primary care, maternal health, and chronic disease screening. This is improving access and also reducing patient load at tertiary hospitals, eventually impacting positively on the global mobile clinics market growth.

MARKET RESTRAINTS

Dependence on Funding Models and Limited Reimbursement to Deter Market Growth

Mobile clinic programs often depend on government funding, CSR initiatives, or nonprofit support rather than stable reimbursement models. Unlike hospital-based care, many mobile services are not fully covered under insurance systems, especially in developing markets. This makes long-term sustainability a concern, even when demand is high. Healthcare providers may hesitate to scale operations without clear revenue visibility. In addition, funding cycles can be inconsistent, which affects the continuity of services. Due to this, mobile clinics are sometimes run as outreach or support programs rather than core revenue-generating units, limiting faster and wider market expansion.

MARKET OPPORTUNITIES

Integration with Population Health and Screening Programs to Offer Lucrative Growth Opportunities

Mobile clinics are well positioned to support large-scale screening and population health programs, especially in areas with low healthcare penetration. They allow healthcare providers to identify diseases early, such as diabetes, hypertension, and cancers, without requiring patients to visit hospitals. This creates strong opportunity for partnerships between hospitals, NGOs, and government bodies. In addition, mobile units can act as entry points for long-term care by linking patients to larger healthcare systems. As healthcare shifts toward preventive and value-based models, these clinics are expected to play a bigger role in early diagnosis and community-level health management.

MARKET CHALLENGES

Ensuring Continuity of Care and Patient Follow-Up to Pose a Critical Challenge to Market Growth

While mobile clinics are effective for initial consultation and screening, maintaining long-term patient follow-up remains a major challenge. Patients identified with chronic conditions or requiring further treatment often need to be referred to hospitals and tracking their journey can be difficult. In many cases, there is limited integration between mobile units and hospital information systems. This can lead to gaps in treatment continuity and patient monitoring. Without strong referral networks and digital tracking systems, mobile clinics risk becoming one-time service providers instead of part of an ongoing care pathway, which reduces their overall impact on health outcomes.

Segmentation Analysis

By Clinic Type

Substantial Requirement of Basic Healthcare Consultations to Boost Primary Care Mobile Clinics Segment Growth

Based on clinic type, the market is divided into primary care mobile clinics, dental mobile clinics, diagnostic & screening mobile clinics, maternal & child health mobile clinics, specialty care mobile clinics, and others.

The primary care mobile clinics segment is anticipated to account for the largest market share. These type of clinics are frequently used for basic consultations, fever and infection treatment, maternal and child health, blood pressure and glucose checks, vaccinations, and follow-up care. Moreover, these services are needed regularly and by a large number of people, especially in underserved communities. In addition, active government involvement to introduce new such clinics is also projected to accelerate segment growth during the forecast period.

- For instance, in March 2022, the state government of Karnataka, India, announced plans to open a new mobile clinic in one of the prominent cities of the state. The new clinic will cater the demand for healthcare services, especially for tribal communities.

The specialty care mobile clinics segment is anticipated to rise at a CAGR of 10.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Substantial Flexibility Offered by Van-Based Mobile Clinics to Boost Segment Growth

Based on vehicle type, the market is segmented into van-based mobile clinics, bus/truck-based mobile clinics, and trailer-based mobile clinics.

In 2025, the van-based mobile clinics segment dominated the global market. The segment holds the largest share as they offer the best balance of flexibility, cost, and practicality. They are easier to operate than large buses or trucks, can reach narrower roads and dense urban neighborhoods, and are usually less expensive to buy and maintain. For most primary care and screening services, a van provides enough space while still being easy to deploy. Moreover, van-based clinics makes it a good fit for hospitals, non-profits, and government outreach programs.

The trailer-based mobile clinics segment is anticipated to rise at a CAGR of 10.2% over the forecast period.

By Application

High Demand for First-Level Care to Boost Primary Healthcare Segment Growth

Based on application, the market is segmented into primary healthcare, dental care, chronic disease management, infectious disease screening & vaccination, and others.

In 2025, the primary healthcare segment dominated the global market. The growth of the segment is attributed to its substantial utilization as it offers first-level care. This includes general consultations, maternal care, child health, screening for chronic conditions, and preventive services. These are high-volume needs that fit well into a mobile format and create repeat demand. Moreover, mobile clinics are especially effective here as they help identify health problems early and reduce the need for patients to travel long distances for basic care.

The chronic disease management segment is anticipated to rise at a CAGR of 9.8% over the forecast period.

By End-User

Considerable Staff and Reference Network of Hospitals & Health Systems to Accelerate Segment Growth

Based on end-user, the market is segmented into hospitals & health systems, government & public health agencies, academic & research institutions, non-governmental organizations (NGOs) / non-profits, and others.

In 2025, the hospitals & health systems segment holds the largest mobile clinics market share as they have the clinical staff, referral networks, and operational systems needed to run mobile medical units effectively. A mobile clinic is often the most valuable when it is connected to a larger care network that can provide testing, referral, follow-up, and treatment. Hospitals also use mobile units to expand community outreach, preventive screening, and population health programs without building new fixed sites. Furthermore, the segment is set to hold a 37.4% share in 2026.

In addition, the government & public health agencies segment is projected to grow at a CAGR of 9.0% during the analysis period.

Mobile Clinics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Mobile Clinics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 1.97 billion, and also maintained the leading share in 2025, with a value of USD 2.13 billion. The market in North America is expected to expand owing to strong healthcare infrastructure and substantial healthcare spending.

U.S. Mobile Clinics Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at a value of around USD 1.97 billion in 2026. This accounts for roughly 38.2% of the global sales.

Europe

The Europe market is projected to record a CAGR of 8.6% over the forecast period, which is the second highest among all regions, and reach a valuation of USD 1.29 billion by 2026. The region is estimated to witness considerable market growth due to the considerable prevalence of chronic conditions and rising investments for better healthcare.

U.K. Mobile Clinics Market

The U.K. market is estimated to touch a value of around USD 0.21 billion in 2026, representing roughly 4.1% of the global revenues.

Germany Mobile Clinics Market

The Germany market is projected to reach approximately USD 0.29 billion in 2026, equivalent to around 5.6% of the global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.12 billion in 2026 and secure the position of the third-largest region in the market. The increasing burden of chronic diseases and surging emphasis on cost-effective care delivery are significant factors anticipated to accelerate the regional market growth.

Japan Mobile Clinics Market

The Japan market is estimated to touch around USD 0.19 billion in 2026, accounting for roughly 3.8% of the global revenues.

China Mobile Clinics Market

The China market is projected to be one of the largest worldwide, with 2026 revenues estimated to reach around USD 0.37 billion, representing roughly 7.2% of the global sales.

India Mobile Clinics Market

The India market is estimated to hit around USD 0.25 billion in 2026, accounting for roughly 4.8% of the global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regional markets are expected to witness moderate growth during the forecast period. The Latin America market is set to reach a valuation of USD 0.33 billion in 2026. In the Middle East & Africa, the GCC market is set to reach a value of USD 0.04 billion in 2026.

South Africa Mobile Clinics Market

The South Africa market is projected to reach around USD 0.02 billion in 2026, representing roughly 0.33% of the global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players’ Substantial Emphasis on Launching of New Mobile Units to Boost Market Progress

The global mobile clinics market holds a semi-consolidated structure, constituting pivotal companies such as Mobile Health, Mission Mobile Medical, TELUS Health for Good, InHealth Group, and UK Screening Solutions. The significant global market share of these participants is driven by numerous strategic activities, including the implementation of new programs collaborations focused on distribution.

- For instance, in October 2023, IHH Healthcare Malaysia announced the launch of mobile clinics with an aim to expand access to healthcare amongst industrial workforce.

Other notable companies in the global market comprise Heart of Australia, Street Side Medics, IHH Healthcare, MEDLIFE Movement, and Aster DM Healthcare. These industry participants are anticipated to prioritize partnerships focused on enhancing their global market share during the analysis period.

LIST OF KEY MOBILE CLINICS COMPANIES PROFILED

- Mobile Health (U.S.)

- Mission Mobile Medical (U.S.)

- TELUS Health for Good (Canada)

- InHealth Group (U.K.)

- UK Screening Solutions (U.K.)

- Heart of Australia (Australia)

- Street Side Medics (Australia)

- IHH Healthcare (Malaysia)

- MEDLIFE Movement (U.S.)

- Aster DM Healthcare (UAE)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Artemis Hospital announced the launch of its new mobile clinics in India to cater the demand for better healthcare services in rural areas.

- January 2024: The government of India announced the launch of its new state-of-the art telemedicine mobile clinic in Jammu Kashmir.

- April 2024: The College of Health and Human Services at Fresno State announced the deployment of new mobile health units.

- August 2023: The Department of Veterans Affairs announced the deployment of new 25 medical units across the U.S. The van will focus on primary care, audiology, and telehealth

- August 2022: Huawei India announced a partnership with Wockhardt Foundation and CanWinn Foundation with an aim to run mobile medical clinic van.

REPORT COVERAGE

The global mobile clinics market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and investments by key regions. The global market research report also provides an in-depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Clinic Type, Vehicle Type, Application, End-User, and Region |

| By Clinic Type |

|

| By Vehicle Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.76 billion in 2025 and is projected to reach USD 10.31 billion by 2034.

In 2025, the North America market value stood at USD 2.13 billion.

The market is expected to exhibit a CAGR of 9.0% during the forecast period of 2026-2034.

By clinic type, the primary care mobile clinics segment is expected to lead the market.

The rising emphasis on better patient convenience and increasing prevalence of chronic conditions are driving market expansion.

Mobile Health, Mission Mobile Medical, TELUS Health for Good, InHealth Group, and UK Screening Solutions are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us