Molded Pulp Packaging Market Size, Share & Industry Analysis, By Source (Wood Pulp and Non-Wood Pulp), By Molded Type (Thick-wall molding, Transfer molding, Thermoformed pulp, and Processed pulp), By Product Type (Trays, Clamshells, Plates, Bowls & Cups, End Caps & Inserts, and Others), By End-use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Consumer Durables & Electronics, Industrial & Automotive, Personal Care & Cosmetics, and Others), and Regional Forecast, 2026-2034

Molded Pulp Packaging Market Size and Future Outlook

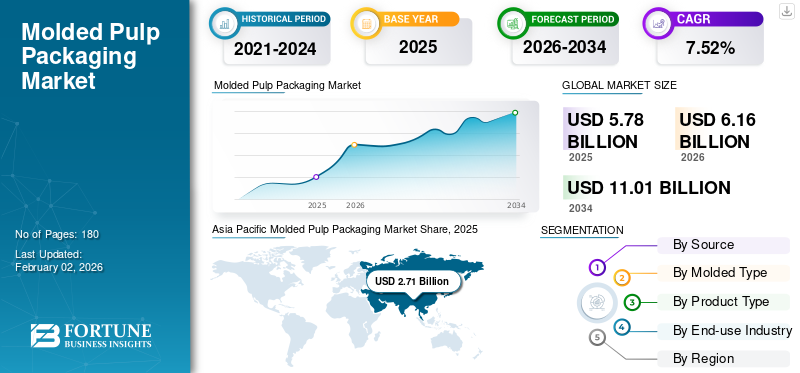

The global molded pulp packaging market size was valued at USD 5.78 billion in 2025 and is projected to grow from USD 6.16 billion in 2026 to USD 11.01 billion by 2034, exhibiting a CAGR of 7.52% during the forecast period. Asia Pacific dominated the global market with a share of 46.79% in 2025.

Molded pulp packaging refers to eco-friendly packaging materials made primarily from recycled paper, cardboard, and other natural fibers. These materials are molded into various shapes to protect and cushion products during storage and transportation. Unlike plastic-based alternatives, molded pulp offers biodegradability and compostability, aligning with global sustainability goals. The packaging is widely used for food service items, electronics, healthcare products, and consumer goods due to its durability, cost-effectiveness, and recyclability.

The market is experiencing steady expansion driven by the surging emphasis on circular economy practices, government regulations against single-use plastics, and rising consumer preference for sustainable packaging. Advancements in molding technology and material innovation, such as the development of water-resistant and high-strength pulp formulations, are further enhancing product performance. Growth in e-commerce and the increasing need for protective transit packaging are also propelling adoption.

Leading manufacturers, such as Huhtamaki, UFP Technologies, Sonoco Products Company, Sabert Corporation, and Brodrene Hartmann A/S, are focusing on automation, capacity expansion, and material optimization to strengthen their market growth presence. Collaborations with food chains and electronics brands for customized molded pulp solutions are also emerging as key strategic trends. Overall, the industry is transitioning from traditional protective packaging toward a sustainable, high-performance, and design-driven approach.

Download Free sample to learn more about this report.

Molded Pulp Packaging Market Key Takeaways

- 2025 Market Size: USD 5.78 billion

- 2026 Market Size: USD 6.16 billion

- 2034 Forecast Market Size: USD 11.01 billion

- CAGR: 7.52% from 2026–2034

- Asia Pacific dominated the molded pulp packaging market with a 46.79% share in 2025.

- The wood pulp segment is expected to account for 79.7% of the market in 2026.

- The thick-wall molding segment is projected to hold a 38.8% market share in 2026.

Asia Pacific

Asia Pacific led the global market with USD 2.71 billion in revenue in 2025 and is projected to reach USD 2.91 billion in 2026.

North America

North America accounted for 22.63% of global revenue in 2025 and is estimated to reach USD 1.38 billion in 2026.

Europe

Europe represented 20.10% of the global market in 2025 and is projected to grow to USD 1.24 billion in 2026.

U.S.

The market is projected to reach USD 1.06 billion by 2026.

Japan

The market is projected to reach USD 1.06 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Government Regulations and Extended Producer Responsibility Policies Drives Market Growth

A significant driver for the adoption of molded pulp packaging in India is the implementation of stringent government regulations aimed at reducing plastic waste and promoting sustainable packaging solutions.

- In May 2025, the Indian Ministry of Environment, Forest and Climate Change (MoEF&CC) introduced a draft notification proposing Extended Producer Responsibility (EPR) for packaging made from paper, glass, and metal, effective from April 1, 2026. This policy mandates that producers take responsibility for the collection, recycling, and environmentally sound disposal of packaging materials, thereby incentivizing the use of eco-friendly alternatives such as molded pulp

Additionally, the Indian government has previously enacted regulations to phase out certain single-use plastic products, further encouraging industries to explore sustainable packaging options. These regulatory measures not only align with global environmental goals but also create a favorable market environment for molded-pulp packaging, which is biodegradable, recyclable, and derived from renewable resources.

The combination of regulatory pressure and consumer demand for sustainable products is propelling the molded pulp packaging market growth in India. Companies are increasingly investing in research and development to innovate and meet these new standards, ensuring compliance while catering to the eco-conscious consumer base.

MARKET RESTRAINTS

High Production Costs and Economic Sensitivity Hinder Market Growth

A significant restraint for molded pulp packaging is its higher production costs compared to conventional plastic alternatives, which can deter adoption, especially during economic downturns. This challenge is evident in the experience of Great Wrap, an Australian sustainable packaging company.

- In October 2025, Great Wrap entered voluntary administration with debts totaling USD 39 million. Despite receiving over USD 28 million in investment and being celebrated for its compostable stretch wrap, the company faced financial strain due to declining sales and shifting market trends toward recycled plastics. The business reportedly never turned a profit, accumulating losses of USD 26.2 million, with revenue declining 32% between FY23 and FY25. Cash flow constraints and unmet demand undermined the company's efforts to scale production, leading to its downfall.

These instances highlight that while molded-pulp packaging offers environmental benefits, its higher production costs and economic sensitivity can impede its widespread adoption. Addressing these challenges requires innovations in cost reduction, economies of scale, and supportive policies to make sustainable packaging more competitive with traditional plastic options.

MARKET OPPORTUNITIES

Expansion into Emerging Markets and New Applications to Create Growth Opportunities

A significant opportunity for molded-pulp packaging lies in its expansion into emerging markets and the adoption of new applications beyond traditional uses. This trend is driven by increasing consumer demand for eco-friendly packaging solutions and the need for cost-effective alternatives to plastic.

Furthermore, advancements in molding technology and material science are enhancing the performance and versatility of molded-pulp packaging. The integration of automation and smart systems is improving production efficiency and reducing costs, making molded pulp packaging more competitive with traditional materials.

The expansion of molded-pulp packaging into emerging markets and new applications presents a significant opportunity for growth. By leveraging technological advancements and responding to consumer demand for sustainable solutions, molded-pulp packaging manufacturers can capitalize on this trend to drive business success.

MARKET CHALLENGES

Limited Design Flexibility and Consumer Perception Propel Market Challenges

A notable challenge for molded pulp packaging is its perceived lack of design flexibility compared to plastic alternatives. While molded pulp is celebrated for its sustainability, some businesses and consumers anticipate its aesthetic and functional limitations as drawbacks. This perception can hinder broader adoption, especially among brands aiming for distinctive, high-end packaging.

- In June 2025, packaging company Lianpack highlighted that while molded pulp can be customized to some extent, it often falls short in offering the intricate designs achievable with plastics or cardboard. This limitation is particularly evident in applications requiring complex shapes or vibrant colors. Such constraints can be a deterrent for businesses seeking to create unique and eye-catching packaging for their products.

Additionally, the integration of moisture-resistant coatings or additives to enhance the durability of molded-pulp packaging can further complicate the design process. These treatments may affect the material's appearance and texture, potentially altering its natural aesthetic appeal. Balancing functionality with design integrity remains a challenge for manufacturers.

MOLDED PULP PACKAGING MARKET TRENDS

Integration of Smart Features into Molded Pulp Packaging is a Market Trend

A notable trend in molded-pulp packaging is the integration of smart features, enhancing functionality beyond traditional protective roles. This evolution is driven by advancements in technology and the growing demand for interactive and informative packaging solutions.

- In January 2025, as per Cornell University, researchers introduced recyclable thin-film soft electronics designed for smart packaging applications. These innovations enable the embedding of sensors and conductive inks into packaging materials, allowing for functionalities such as monitoring the freshness of perishable goods. The integration of such technologies into molded-pulp packaging represents a significant step toward creating intelligent, eco-friendly packaging solutions.

Furthermore, the packaging industry is witnessing a shift toward incorporating digital elements into packaging design. For instance, the use of QR codes and RFID tags in molded pulp packaging allows consumers to access product information, track sustainability metrics, and engage with brands in innovative ways. This trend aligns with the broader movement toward digitalization and consumer interaction in packaging.

Download Free sample to learn more about this report.

Molded Pulp Packaging Market Segmentation Analysis

By Source

High Demand for Wood Pulp Packaging Contributed to Segmental Growth

On the basis of the segmentation of source, the market is classified into wood pulp and non-wood pulp.

The wood pulp segment held a substantial market share in 2024. This growth is primarily driven by its biodegradability, recyclability, and wide adoption in food and beverage packaging applications. Wood pulp-based molded packaging offers excellent cushioning, strength, and moisture resistance, making it suitable for products ranging from fresh produce to electronics. Furthermore, increasing consumer preference for sustainable and eco-friendly packaging solutions has further fueled the adoption of wood pulp. The wood pulp segment is expected to account for 79.7% of the market in 2026.

- For example, Huhtamaki Oyj and PulpWorks Inc. are key players actively expanding their wood pulp-based molded packaging portfolios, catering to global food and consumer goods brands.

By Molded Type

On the basis of molded type, the market is classified into thick-wall molding, transfer molding, thermoformed pulp, and processed pulp.

The thick-wall molding segment held a substantial market share in 2024. This is primarily due to its superior strength, durability, and protective properties, making it highly suitable for heavy-duty applications such as industrial equipment packaging, electronics, and fragile food items. Thick-wall molded-pulp packaging provides excellent cushioning and impact resistance while being cost-effective and environmentally friendly packaging, which has driven its adoption across multiple sectors. The thick-wall molding segments is anticipated to hold a dominant market share of 38.8% in 2026.

- For instance, in June 2025, Fripa Group launched thermoformed pulp trays for bakery and snack packaging in the European market, highlighting the increasing interest in versatile molded pulp solutions beyond thick-wall molding.

The thermoformed pulp segment is expected to grow at a CAGR of 9.32% over the forecast period.

By Product Type

On the basis of product type, the market is classified into trays, clamshells, cups, plates, bowls, end caps, and others.

The tray segment held a substantial molded pulp packaging market share in 2024. This dominance is largely attributed to their extensive use in food service, fresh produce, and electronics packaging due to their high structural integrity, recyclability, and adaptability for multiple designs. Molded pulp trays are increasingly replacing plastic trays in supermarkets and quick-service restaurants, driven by regulatory bans on single-use plastics and the growing consumer demand for sustainable packaging. In 2026, the trays segment is projected to lead the market with a 44.64% share.

- For example, in May 2025, Huhtamaki Oyj introduced a new line of molded pulp trays for ready-to-eat meals and fresh produce across Europe, enhancing its sustainable packaging portfolio.

By End-use Industry

Widespread Usage in Packaged Foods and Ready-to-Eat Products Supplemented Segment Growth

On the basis of end-use industry, the market is classified into food & beverages, pharmaceuticals & healthcare, consumer durables & electronics, industrial & automotive, personal care & cosmetics, and others.

To know how our report can help streamline your business, Speak to Analyst

The food & beverages segment held the largest market share in 2024. This dominance is primarily driven by the increasing shift toward sustainable and biodegradable packaging for fresh produce, dairy, eggs, beverages, and ready-to-eat meals. Molded pulp packaging provides excellent protection, ventilation, and moisture resistance while maintaining product freshness, making it an ideal alternative to plastic. The rising number of quick-service restaurants and the expansion of organized retail chains have further fueled demand for molded pulp trays, clamshells, and cups. The food & beverages segment is forecast to represent 58.44% of total market share in 2026.

- For instance, in March 2025, Huhtamaki Oyj partnered with a European retail chain to supply molded pulp packaging for ready-to-eat meals and bakery products, reinforcing the growing integration of sustainable materials in the food service sector.

Molded Pulp Packaging Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Molded Pulp Packaging Market Share, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in Asia Pacific reached USD 2.71 billion in 2025, representing 46.79% of total market revenue, and is projected to reach USD 2.91 billion in 2026. This growth is attributed to the rapid expansion of the food delivery industry, rising urbanization, and increasing consumer preference for sustainable packaging solutions. Countries such as China, India, and Japan are major contributors, supported by large-scale manufacturing facilities and government initiatives encouraging plastic reduction. In 2026, the China market is estimated to reach USD 1.32 billion. The Japan market is forecast to attain USD 0.36 billion by 2026 and the India market is anticipated to achieve USD 0.53 billion by 2026.

- For instance, in July 2025, YFY Inc. (Taiwan) announced the expansion of its molded pulp production facility in China to cater to the growing demand from the electronics and food packaging sectors, reinforcing Asia Pacific’s leadership in the global market.

Europe and North America

Other regions such as Europe and North America are anticipated to witness notable growth in the coming years. In 2025, Europe held 20.10% of the global market, reaching a valuation of USD 1.16 billion, and is projected to grow to USD 1.24 billion in 2026. The North America market was valued at USD 1.31 billion in 2025, capturing 22.63% of global revenue, and is estimated to reach USD 1.38 billion in 2026. During the forecast period, the North America region is projected to record a growth rate of 5.50%, which is the second highest amongst all the regions, reaching a valuation of USD 1.24 billion in 2025. This is primarily driven by strong regulatory measures against single-use plastics and rising consumer awareness about compostable packaging. The U.S. and Canada are key contributors, with major players such as Sonoco Products Company and Cascades Inc. innovating in molded fiber trays, clamshells, and protective packaging for food and consumer goods. The U.S. market is assessed at USD 1.06 billion by 2026. After North America, the market in Europe is estimated to reach USD 1.24 billion in 2026 and secure the position of third-largest region in the market. In the region, France both are estimated to reach USD 0.17 billion in 2025. The UK market is expected to reach USD 0.16 billion by 2026, while the Germany market is anticipated to account for USD 0.24 billion by 2026.

Latin America and Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions would witness a moderate growth in this marketspace. Latin America maintained a strong presence in the global market, reaching USD 0.35 billion in 2025, accounting for 6.11% share, and is expected to reach USD 0.37 billion in 2026. Latin America market in 2025 is set to record USD 0.34 billion as its valuation. Driven by increasing urbanization, government-led sustainability programs, and growing exports of agricultural products are supporting the uptake of molded pulp packaging. In 2025, the Middle East & Africa market stood at USD 0.25 billion, representing 4.37% of global demand, and is projected to grow to USD 0.27 billion in 2026. In the Middle East & Africa, Saudi Arabia is set to attain the value of USD 0.07 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings coupled with Strong Distribution Network of Key Companies Supported their Leading Position

The global market shows a semi-concentrated structure with numerous small-to-mid-size companies actively operating across the globe. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Brødrene Hartmann A/S, Huhtamaki Oyj, and UFP Technologies, Inc are some of the dominating players in the market. A comprehensive portfolio of metalized films and laminates, global presence through extensive manufacturing and distribution networks, and continuous investment in sustainable flexible packaging innovations are few characteristics of these players which support their dominance.

Apart from this, other prominent players in the market include Sabert Corporation, Henry Molded Products, Inc., Pro-Pac Packaging Limited, Fabri-Kal, Eco-Products, Inc., and Genpak, LLC. These companies are undertaking various strategic initiatives such as mergers & acquisitions, capacity expansions, and development of recyclable molded-pulp packaging structures to enhance their market presence and cater to rising demand across food, pharmaceuticals, and personal care industries.

LIST OF KEY MOLDED PULP PACKAGING COMPANIES PROFILED:

- Brødrene Hartmann A/S (Denmark)

- Huhtamaki Oyj (Finland)

- UFP Technologies, Inc. (U.S.)

- Sabert Corporation (U.S.)

- Henry Molded Products, Inc. (U.S.)

- Pro-Pac Packaging Limited (Australia)

- Fabri-Kal (U.S.)

- Eco-Products, Inc. (U.S.)

- Genpak, LLC (U.S.)

- CKF Inc. (Canada)

- Thermoform Engineered Quality LLC (U.S.)

- FiberCel Packaging (Canada)

- EnviroPAK (U.S.)

- Pacific Pulp Molding, Inc. (U.S.)

- Celluloses de la Loire (CDL) (France)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Solenis, a leading global provider of water and hygiene solutions, will be exhibiting at two key industry tradeshows, where it will highlight technology to enable paperization through chemistry for sustainable packaging.

- May 2025: Amcor, a global leader in developing and producing responsible packaging solutions, and forestry industry company Metsä Group, announced a collaboration to develop three-dimensional molded fiber packaging solutions with lidding and liner for a variety of food applications. The collaboration underscores Amcor and Metsä Group’s commitment to sustainability and innovation by creating recycle-ready packaging solutions. Combining Amcor’s advanced high-barrier film liner and lidding technology with Muoto™, a wood-based molded fiber product developed by Metsä Spring, Metsä Group’s innovation company, the partnership seeks to deliver innovative fiber-based food packaging that protects perishable food products and extends shelf life.

- May 2025: PulPac, a company specializing in Dry Molded Fiber (a variant of molded pulp technology), announced its patent portfolio now includes ~400 granted patents across 58 countries, covering innovations in its SCALA machine architecture, cutting tools, and process improvements.

- April 2025: Hartmann Packaging A/S agreed to acquire SC Dentaş Romania SRL, which specializes in molded fiber packaging, expanding Hartmann’s European footprint and capacity in molded pulp products.

- October 2024: Huhtamaki began smooth molded fiber (SMF) lid production at its existing facility in Lurgan, Northern Ireland, increasing its capacity and local supply of molded fiber lids.

REPORT COVERAGE

The global molded pulp packaging market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.52% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Source

By Molded Type

By Product Type

By End-use Industry

By Region North America (By Source, Molded Type, Product Type, End-use Industry and Country)

Europe (By Source, Molded Type, Product Type, End-use Industry , and Country)

Asia Pacific (By Source, Molded Type, Product Type, End-use Industry, and Country)

Latin America (By Source, Molded Type, Product Type, End-use Industry and Country)

Middle East & Africa (By Source, Molded Type, Product Type, End-use Industry and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.78 billion in 2025 and is projected to reach USD 11.01 billion by 2034.

In 2025, the market value stood at USD 2.71 billion.

The market is expected to exhibit a CAGR of 7.52% during the forecast period.

The food & beverages segment led the market by end-use industry.

The key factors driving the market are government regulations and extended producer responsibility (EPR) policies.

Brødrene Hartmann A/S, Huhtamaki Oyj, and UFP Technologies, Inc, are some of the prominent players in the market.

Asia Pacific dominated the market with a share of 46.79% in 2025.

Expansion into emerging markets and new applications to create growth opportunities.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us