MRO Distribution Market Size, Share & Industry Analysis, By Product Type (Engine Material & Components, Airframe & Component Spares, Hardware & Connectors, Cabin & Interior Components, Others), By Sourcing Type (OEM New Parts, USM (Used Serviceable Material), PMA (Parts Manufacturer Approval)), By Distribution Type (Traditional Distribution, E-Commerce & Marketplaces, Pooling/Exchange Programs, Vendor-Managed Inventory, and PBH/Material-by-the-Hour), By Platform (Narrow-body Jets, Wide-body Jets, Regional Jets, Business Jets, & Helicopters), By End User, and Regional Forecast, 2026-2034

MRO Distribution Market Size and Industry Overview

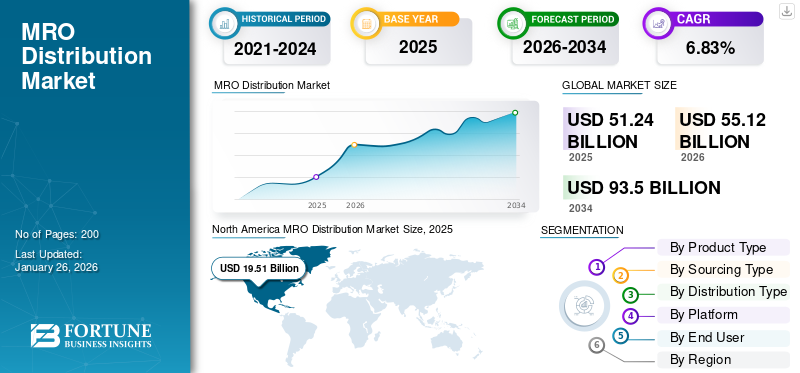

The global MRO distribution market size was valued at USD 51.24 billion in 2025 and is projected to grow from USD 55.12 billion in 2026 to USD 93.50 billion by 2034, exhibiting a CAGR of 6.83% during the forecast period. North America dominated the MRO Distribution Market with a market share of 38.07% in 2025.

The Maintenance, Repair, and Operations (MRO) distribution market forms the backbone of the aviation maintenance ecosystem. It involves the sourcing, stocking, and delivery of aircraft parts, machine consumables, and materials needed for maintenance, repair, and overhaul operations. Distributors act as the bridge between manufacturers, MRO providers, and airlines, ensuring the right parts reach the right place, on time, with full certification and traceability. This includes everything from engine components and avionics to fasteners, chemicals, and lubricants. The process combines deep technical knowledge with logistics precision, inventory forecasting, vendor-managed stock, AOG (Aircraft on Ground) response, and digital platforms for real-time part availability.

Key players such as Boeing Distribution, Satair, Proponent, AAR, and Wesco increasingly focus on reducing downtime, expanding e-commerce channels, and offering value-added services such as kitting or pooling. In essence, MRO distribution keeps fleets flying safely and efficiently by ensuring the global supply chain for aircraft parts never stops moving.

Download Free sample to learn more about this report.

MRO DISTRIBUTION MARKET KEY TAKEAWAYS

Market Size & Forecast

Market Size & Forecast

- 2025 Market Size: USD 51.24 billion

- 2026 Market Size: USD 55.12 billion

- 2034 Forecast Market Size: USD 93.50 billion

- CAGR: 6.83% from 2026–2034

Market Share

Market Share

- North America dominated the MRO Distribution Market with a market share of 38.07% in 2025.

- The OEM new parts segment is projected to lead the market with a 50.16% share in 2026.

- The segment of Wide-body Jets will witness a growth rate of 7.13% over the forecast period.

Key Regional Highlights

Key Regional Highlights

North America

North America remained the leading regional market, generating USD 19.51 billion in revenue and accounting for 38.07% of the global market in 2025.

Asia Pacific

Asia Pacific represented 30.22% of global market revenue in 2025 and is expected to maintain steady growth through the forecast period.

Europe

Europe contributed 20.13% of global revenue in 2025 and continues to strengthen its position through ongoing industrial and aviation maintenance activities.

U.S.

The country remains a major contributor to North American market growth, supported by a mature aerospace sector and extensive MRO infrastructure.

Japan

The market is supported by strong aerospace manufacturing capabilities and increasing demand for advanced maintenance and replacement solutions.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Aircraft Fleet Age and Utilization Drive Market Growth

Airlines face growing demand for replacement parts and consumables as global fleets age and flight utilization increases. Older aircraft need constant inspections, line maintenance, and component changes, boosting material throughput. Combined with record traffic recovery and restricted OEM production slots, operators are extending aircraft lifespans, pushing more business toward independent MROs and distributors. This surge in maintenance intensity, along with higher dependence on used serviceable materials and PMA parts, fuels sustained growth in MRO distribution. The industry is evolving from reactive parts supply to predictive, data-driven provisioning that keeps maintenance lines continuously supplied and aircraft flying.

MARKET RESTRAINTS

OEM Control and Certification Complexities Restrain Market Expansion

Original equipment manufacturers maintain strong control over parts licensing, technical data, and certification pathways, restricting independent distributors’ access. Strict airworthiness and traceability rules demand dual-release forms and compliance audits that limit smaller players’ scalability. Meanwhile, airlines’ preference for OEM-backed maintenance programs and long-term contracts often sidelines third-party distributors. Regulatory differences between the FAA, EASA, and CAAC further complicate cross-border parts trade. These barriers slow market fluidity, increase operational costs, and keep profit margins under pressure. The combination of tight OEM monopolies and compliance-driven red tape remains the single biggest brake on open competition in MRO distribution.

MARKET OPPORTUNITIES

Digitalization and Predictive Supply Offer New Opportunities

Increased preference for digitalization and predictive maintenance is paving the way for MRO distributors. Platforms that integrate real-time part demand, aircraft health data, and automated replenishment are revolutionizing inventory management. Distributors using AI-driven forecasting, e-commerce channels, and blockchain traceability are gaining a competitive edge. Predictive analytics enables materials to be pre-positioned before failures occur, lessening AOG events and freight costs. Digital transparency and sustainability goals generate a more agile, value-added ecosystem where distributors evolve into trusted partners in maintenance reliability.

MRO DISTRIBUTION MARKET TRENDS

Emergence of E-Commerce and USM Adoption Shape Market Trends

The MRO distribution market is undergoing a quiet revolution through digitization and sustainability. E-commerce portals and API-based procurement are replacing manual RFQs, allowing instant price comparison and real-time availability checks. Simultaneously, the adoption of used serviceable materials (USM) and PMA parts is expanding as airlines seek cost-efficient, traceable alternatives. This shift is changing inventory composition less about stock volume, more about trace quality and data visibility. ESG and REACH compliance are influencing product ranges, specifically in chemicals and coatings. Overall, the trend points toward a faster, greener, and more data-driven distribution ecosystem powering global aviation maintenance.

MARKET CHALLENGES

Supply Chain Volatility and Logistics Disruptions Challenge Operations

Global supply chain instability continues to test MRO distributors. Delays in raw materials, shipping constraints, and geopolitical trade restrictions have made inventory planning unpredictable. With limited visibility into OEM lead times and repair shop turnaround, distributors often face stock imbalances too much of one part, none of another. The result is higher carrying costs and occasional AOG crises. Additionally, workforce shortages in warehousing and logistics add complexity to meeting service-level agreements. Distributors must balance agility with compliance while mitigating risk through diversified sourcing, localized inventory hubs, and stronger digital coordination across the aviation aftermarket network.

U.S. Tariff Impact

U.S. tariffs on imported aerospace components, metals, and specialty chemicals have quietly reshaped the MRO distribution landscape. Distributors that once relied on low-cost parts from Europe or Asia now face higher landed costs and longer lead times due to customs friction. Many have shifted to domestic suppliers or increased local stocking, which raises inventory expenses but ensures continuity. Smaller distributors struggle to absorb tariff-related price swings, while larger players pass costs downstream to MROs and airlines. The ripple effect is a tighter margin environment and growing urgency to diversify sourcing strategies beyond traditional trade lanes.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Expanding Engine Overhauls and Aging Fleets Boosted Engine Material & Components Segment Growth

On the basis of the product type, the market is classified into engine material & components, airframe & component spares, hardware & connectors, cabin & interior components, and others.

The engine material & components segment is accounted for the largest market with a share of 37.52% in 2026. The growing number of engine shop visits, coupled with aging narrow-body and regional aircraft, fuels the need for certified replacement parts. Distributors benefit as operators seek faster, traceable sourcing for critical engine components to offset OEM lead times and control maintenance costs.

The airframe & Component Spares segment is expected to rise at a CAGR of 7.09% over the forecast period.

By Sourcing Type

Increasing OEM Control and Fleet Modernization Fostered Demand for OEM New Parts

In terms of sourcing type, the market is categorized into OEM new parts, USM (Used Serviceable Material), and PMA (Parts Manufacturer Approval).

The OEM new parts segment projected to capture the largest MRO Distribution market with a share of 50.16% in 2026. The segment is witnessing significant growth as airlines continue to favor OEM-certified parts to ensure compliance, warranty protection, and seamless integration with new-generation aircraft.

The USM (Used Serviceable Material) segment is expected to rise at the highest CAGR of 7.30% over the forecast period.

By Distribution Type

Traditional Distribution Segment Led Due to Established Supplier Relationships and Certified Handling

Based on distribution type, the market is segmented into traditional distribution, e-commerce & marketplaces, pooling/exchange programs, vendor-managed inventory (VMI), and PBH/material-by-the-hour.

The traditional distribution segment is anticipated to hold the dominating position with a share of 42.24% in 2026. Traditional distribution remains vital as customers prioritize reliability, technical expertise, and traceable logistics. Growth is strengthened by hybrid models that blend human-led service with digital tools, ensuring rapid AOG response and consistent fill rates.

The Vendor-Managed Inventory (VMI) segment is set to rise at a CAGR of 7.03% over the forecast period.

By Platform

Rising Flight Cycles and Fleet Expansions Propelled Narrow-body Jets Segment Growth

Based on platform, the market is segmented into narrow-body jets, wide-body jets, regional jets, business jets, helicopters, and others.

The narrow-body jets segment is anticipated to hold the dominating position with a share of 32.43% in 2026. Narrow-body aircraft dominate airline operations worldwide, creating consistent demand for consumables, rotables, and engine spares.

The segment of Wide-body Jets will witness a growth rate of 7.13% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Competitive Sourcing Flexibility and Regional Repair Growth Drive Independent MROs Segment Expansion

Based on end user, the market is segmented into independent MROs, OEM-Affiliated MROs

Airlines/operators, LCCs /charter operators, and defense & military depots.

The Independent MROs segment held the dominating position in 2024. Independent MROs depend heavily on distributors for affordable and readily available parts, making them central to aftermarket growth.

The OEM-Affiliated MROs segment is set to flourish with a growth rate of 7.12% over the forecast period.

MRO Distribution Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America MRO Distribution Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America maintained a strong presence in the global market, reaching USD 19.51 billion in 2025, accounting for 38.07% share, and is expected to reach USD 20.99 billion in 2026. North America leads the global MRO Distribution market, supported by a vast fleet base, a strong USM ecosystem, and deep-rooted distributor networks. Growth is steady as airlines focus on maintaining older aircraft, engine shop visits rise, and digital logistics streamline AOG parts delivery across major hubs.

In 2025, the U.S. market is estimated to reach USD 14.52 billion. In the U.S., safety and airworthiness regulations are enforced by the Federal Aviation Administration (FAA) and other regulatory agencies. Consistent MRO is required to comply with these complex and changing rules, which leads to market growth.

Asia Pacific

The Asia Pacific market accounted for USD 15.48 billion in 2025, representing 30.22% of the global industry, and is expected to reach USD 16.76 billion in 2026. The market in Asia Pacific is projected to record a growth rate of 7.63% during the forecast period. Asia Pacific is the fastest-growing region, fueled by rapid fleet expansion, rising domestic travel, and a surge in local MRO capabilities. Distributors are scaling up regional warehouses and e-commerce platforms to meet escalating demand from low-cost carriers and newly established maintenance centers. Countries such as China, India, and Japan are advancing their orbital capabilities, launching new constellations for communications, navigation, and remote sensing. Backed by these factors, countries including China is anticipates to record the valuation of USD 5.38 billion, Japan to record USD 3.12 billion, and India to record USD 4.63 billion in 2026.

Europe

In 2025, Europe generated USD 10.31 billion, contributing 20.13% to global market revenue, and is projected to grow to USD 11.09 billion in 2026. In the region, the U.K. and Germany both are estimated to reach USD 3.46 billion and 2.96 billion each in 2026.

Rest of the World

Rest of the World accounted for USD 5.94 billion in 2025, representing 11.58% of the global market share, and is projected to reach USD 6.28 billion in 2026. Middle East, Africa and Latin America regions would witness a moderate growth over the forecast period. The Middle East market is set to record USD 4.27 billion as its valuation in 2025. Latin America is set to attain the value of USD 1.67 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Digital Revolution, Strategic Partnerships, and Inventory Agility Define Competitive Landscape

The global MRO distribution market is moderately consolidated, led by a mix of OEM-backed suppliers and large independent distributors competing on reliability, reach, and responsiveness. Key companies, including Proponent, Satair (Airbus), AAR, Boeing Distribution, and Wesco, dominate core product flows, while niche specialists concentrate on PMA and USM parts to capture price-sensitive demand. Competition increasingly centers on digital enablement, real-time inventory visibility, e-commerce platforms, and predictive stocking rather than sheer warehouse size. Strategic partnerships between distributors, repair shops, and logistics providers are redefining supply efficiency, while smaller regional players survive through flexibility, localized service, and deep customer relationships.

LIST OF KEY MRO DISTRIBUTION COMPANIES PROFILED

- Boeing (U.S.)

- Satair (Denmark)

- Proponent (U.S.)

- AAR Corp. (U.S.)

- Wesco Aircraft/Incora (U.S.)

- GA Telesis (U.S.)

- AJW Group (U.K.)

- HEICO Aerospace (U.S.)

- Avtrade (U.K.)

- Kellstrom Aerospace (U.S.)

- AerFin (U.K.)

KEY INDUSTRY DEVELOPMENTS

- October 2024- Proponent and ATS Technic, the sole independent EASA-certified provider of line maintenance and logistics for a variety of aircraft in UAE, inked a Memorandum of Understanding (MOU). By combining Proponent's extensive global distribution network with ATS Technic's maintenance experience, this partnership seeks to increase the effectiveness of procuring and delivering premium aviation components.

- September 2024- HAECO and Boeing signed a new agreement to support HAECO's worldwide MRO services by covering consignment and spare parts provided by Boeing. Under the recently signed comprehensive agreement, several Boeing and HAECO business units' prior separate agreements are combined into a single deal.

- September 2024: HAECO and Proponent announced a new agreement that will reshape their cooperation and business practices. All functioning businesses under the HAECO Group will be covered by a "landmark group contract," which creates a single framework intended to simplify administration.

- April 2024: Ontic and Boeing signed an exclusive distribution deal at MRO Americas. By signing a new 10-year distribution deal, Boeing will expand its product offerings to include the thrust reverser actuation system (TRAS) and propeller electronic control unit (PECU) product lines.

- January 2024: In a new multi-year arrangement with Ontic, AR CORP., a provider of aviation services to government and commercial operators, MROs, and OEMs, grants AAR the distribution rights to supply the U.S. government with a strategic selection of military equipment, including exclusivity on some parts.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.83% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Sourcing Type, Distribution Type, Platform, End User, and Region |

|

By Product Type |

· Engine Material & Components · Airframe & Component Spares · Hardware & Connectors · Cabin & Interior Components · Others |

|

By Sourcing Type |

· OEM New Parts · USM (Used Serviceable Material) · PMA (Parts Manufacturer Approval) |

|

By Distribution Type |

· Traditional Distribution · E-Commerce & Marketplaces · Pooling/Exchange Programs · Vendor-Managed Inventory (VMI) · PBH/Material-by-the-Hour |

|

By Platform |

· Narrow-body Jets · Wide-body Jets · Regional Jets · Business Jets · Helicopters · others |

|

By End User |

· Independent MROs · OEM-Affiliated MROs · Airlines/Operators · LCCs/Charter Operators · Defense & Military Depots |

|

By Region |

· North America (By Product Type, Sourcing Type, Distribution Type, Platform, End User, and Country) o U.S. o Canada · Europe (By Product Type, Sourcing Type, Distribution Type, Platform, End User, and Country/Sub-region) o U.K. o Germany o France o Russia o Rest of the Europe · Asia Pacific (By Product Type, Sourcing Type, Distribution Type, Platform, End User, and Country/Sub-region) o China o Japan o India o South Korea o Rest of the Asia Pacific · Rest of the World (By Product Type, Sourcing Type, Distribution Type, Platform, End User, and Country/Sub-region) o Middle East & Africa o Latin America |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 55.12 billion in 2026 and is projected to reach USD 93.50 billion by 2034.

In 2025, the market value stood at USD 19.51 billion.

The market is expected to exhibit a CAGR of 6.83% during the forecast period of 2026-2034.

The engine material & components segment led the market by product type.

Rising aircraft fleet age and utilization drive market growth.

Boeing, Satair, Proponent, AAR Corp., Wesco Aircraft/Incora, and GA Telesis are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us