Network as a Service Market Size, Share & Industry Analysis, By Type (WAN as a Service and LAN as a Service), By Enterprise Type (Small and Medium Enterprises and Large Enterprises), By Application (Wide Area Network, Virtual Private Network, Cloud Based Services, Bandwidth on Demand, and Others), By End User (Corporate Customers and Individual Customers), By Industry (Corporate Customers) (BFSI, IT & Telecom, Manufacturing, Healthcare, Retail, and Others), and Regional Forecast, 2026 – 2034

(Offer valid till 15th Aug 2026)

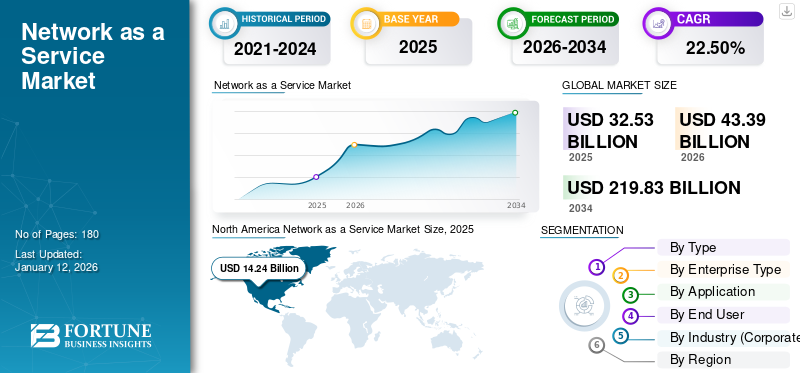

NETWORK AS A SERVICE MARKET SIZE AND FUTURE OUTLOOK

The global network as a service market size was valued at USD 28.25 billion in 2025. The market is projected to grow from USD 34.58 billion in 2026 to USD 187.18 billion by 2034, exhibiting a CAGR of 23.5% during the forecast period. North America dominated the network as a service market with a market share of 39.68% in 2025.

Network as a Service (NaaS) is a cloud-based service where you can provision, manage and consume networking capabilities as needed, either paying for them monthly or by volume. With this, an organization can obtain a number of networking services, such as connection, bandwidth, and security, when they are needed, without having to purchase physical networking infrastructures or operate complex hardware. The NaaS market is growing rapidly due to digital transformation, increased adoption of cloud applications, and the need for lower-cost, more flexible networking solutions. Organizations benefit from reduced operational overhead by having a fully managed network and receiving better visibility, improved performance, and integrated security across their entire digital landscape.

Furthermore, many key market players, such as Verizon Communications Inc., AT&T Inc., Lumen Technologies, Inc., BT Group plc, and Vodafone Group Plc, operating in the market, are increasingly integrating AI into network platforms to improve performance, reduce downtime, and simplify operations. AI helps automate network monitoring, detect issues early, and optimize traffic flow across distributed environments.

Download Free sample to learn more about this report.

NETWORK AS A SERVICE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 28.25 billion

- 2026 Market Size: USD 34.58 billion

- 2034 Forecast Market Size: USD 187.18 billion

- CAGR: 23.5% from 2026–2034

- North America dominated the network as a service market with a market share of 39.68% in 2025.

- Small and medium sized enterprises segment is anticipated to grow at the highest CAGR of 25.8% over the forecast period.

- Cloud based services segment is anticipated to grow at the highest CAGR of 25.5% over the forecast period.

North America

North America held the largest network as a service market share in 2024, valuing at USD 9.06 billion, and also maintained the leading share in 2025, with USD 11.21 billion.

Europe

Europe is projected to record a growth rate of 20.3% in the coming years and reach a valuation of USD 8.29 billion in 2026.

Asia Pacific

Asia Pacific region is estimated to reach USD 8.45 billion in 2026 and is expected to grow at the highest CAGR of 26.5% during the forecast period.

U.S.

The U.S. market can be analytically approximated at around USD 9.82 billion in 2026, accounting for roughly 28.4% of global sales.

Japan

The Japanese market is estimated at around USD 1.30 billion in 2026, accounting for roughly 3.8% of global sales.

Read More

IMPACT OF GENERATIVE AI

Surge in Integration of Generative AI Strengthening Next-Generation NaaS Platforms

NaaS is being accelerated by generative AI as it automates, predicts, and self-optimizes network operations, eliminating the need for manual troubleshooting and improving the uptime of services for enterprises. For instance,

- In March 2024, HPE integrated multiple Gen AI large language models into HPE Aruba Networking Central to improve AI Search, operator experience, network performance, and security across cloud-native network management.

In addition to this overall acceleration of the NaaS market, generative AI enhances NaaS by providing the ability for AI-native platforms to model user experiences, proactively detect network problems, and recommend resolutions to those problems before users are affected.

Overall, generative AI is moving NaaS from the provision of simply managed connectivity to the provision of a more intelligent, AI-assisted approach to the orchestration of networks. As a service provider, your network will become differentiable based on automation, predictive maintenance, analytics on security, and connectiveness between AI workloads.

NETWORK AS A SERVICE MARKET TRENDS

Increasing Integration of NaaS with SASE Driving Secure and Unified Networking

Enterprises are increasingly using unified platforms to combine network & security services, which is enabling companies to accelerate the transition of Networking as a service (NaaS) into Secure Access Service Edge (SASE). This is happening owing to an increasing demand by organizations for a single cloud-based solution that can provide security for their distributed users, cloud applications, branch office locations, and/or remote devices, as opposed to multiple stand-alone products. The integration of NaaS with SASE simplifies the operational complexity of these security solutions by improving visibility across the entire network, thus creating an environment where policy enforcement is done uniformly. For instance,

- Cisco’s 2024 Global Networking Trends research, based on insights from over 2,000 IT leaders, highlights the growing enterprise focus on modern and integrated network transformation.

The transition to zero trust principles has helped accelerate this integration due to a growing desire within organizations to find networking solutions that allow secure access based on identity, device (or endpoint) as well as application contextual information. This model is becoming more relevant as enterprises modernize security strategies for cloud and hybrid work environments.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Adoption of Cloud-First and Hybrid IT Environments Driving NaaS Demand

Multiple enterprises are opting for a cloud-first or hybrid IT environment, where they have placed some of their applications and workloads in the public cloud, some in private clouds, and some are still on-premise or in data centers. As this occurs, enterprises have an ever-growing need for flexible, scalable and software-defined networking solutions that meet their changing business needs. Traditional network infrastructure is not able to manage distributed environments effectively and this has resulted in operational inefficiencies. For instance,

- According to Flexera’s 2024 State of the Cloud Report, 73% of organizations have adopted hybrid cloud strategies, highlighting the growing reliance on interconnected systems that require agile network infrastructure.

In particular, the increased use of multi-clouds has further complicated network management, as companies must now manage connectivity, performance & security across multiple platforms. Ensuring that companies have the same level of service across all these environments can be a challenge for traditional networking models, and many of these models remain heavily hardware-dependent and ill-positioned to respond quickly to the rapid pace of change. NaaS provides a solution to this problem by providing centralized control of the network, automated provisioning capabilities, and the ability to scale bandwidth based on real time needs.

MARKET RESTRAINTS

Rising Data Security and Compliance Concerns Limiting NaaS Adoption

Uncertainties stemming from issues with securing and protecting data and concerns associated with adherence to regulations have led to enterprises adopting a conservative approach toward utilizing NaaS for their organization. The third-party managed infrastructure, along with cloud-based delivery models pose a number of unauthorized access, data breaches and lack of control over key network functions challenges; in particular, these issues are especially amplified in companies whose business is primarily dependent on securing sensitive information such as organizations operating in BFSI, healthcare, and government sectors.

The complexities arising from different regulatory regimes, as well as different regional laws governing the protection of data exacerbate enterprises' ability to implement NaaS. The organization's ability to implement NaaS across geographic regions typically requires an organization to comply with numerous different and often conflicting data protection laws and evolving compliance standards. For organizations that are large and global in nature, this can create additional risks and operational burden.

MARKET OPPORTUNITIES

Expansion of 5G and Edge Computing Driving New Opportunities for NaaS

There are a lot of possibilities for network as a service (NaaS) as 5G infrastructure is rapidly expanding. NaaS is becoming more attractive owing to an increase in demand for agile, low-latency, and high-capacity network connectivity. Many enterprises are moving toward private 5G, smart operations, and data-intensive applications to create their own networks, but they need network models that can be deployed quickly at a minimal hardware investment. NaaS will meet these needs by providing software-based connectivity that can respond dynamically to changing traffic demands. For instance,

- GSMA states that global 5G connections reached 2 billion by the end of 2024, reflecting the growing scale of adoption and strengthening the demand for service-based networking models.

Edge computing also helps create new opportunities for NaaS as data processing occurs closer to devices and users, as well as to industrial systems. As this shift occurs, the demand for responsive, efficient network services that link edge sites with cloud-based platforms while providing high performance and visibility will increase. NaaS can fulfill this demand as it provides centralized management, scalable bandwidth, and faster deployment options at multiple distributed locations.

Segmentation Analysis

By Type

Growing Enterprise Shift toward SD-WAN Boosted WAN-as-a-Service Segmental Dominance

Based on type, the market is bifurcated into WAN as a service and LAN as a service.

WAN as a service segment accounted for the largest market share in 2025. This is owing to the rapid adoption of cloud and Software Defined Wide Area Network (SD-WAN) technology by large enterprises with multi-cloud networks, and hybrid work models requiring secure and scalable wide-area connectivity. As more large enterprises shift away from conventional MPLS (Multiprotocol Label Switching) to cloud-managed WANs in order to increase flexibility, decrease operational costs, and support real-time performance for applications across a distributed branch network, they are using SD-WAN to gain access to a more agile and more efficient wide-area network.

LAN as a service segment is anticipated to grow at the highest compound annual growth rate (CAGR) of 25.7% over the forecast period. This is owing to increasing adoption of cloud-managed campus networks, Wi-Fi 6/6E infrastructure, and hybrid workplace environments requiring scalable, secure, and centrally managed local area networking solutions.

To know how our report can help streamline your business, Speak to Analyst

By Enterprise Type

Expansion of Hybrid Work Infrastructure Fueled Adoption of NaaS in Large Enterprises

Based on enterprise type, the market is divided into small and medium enterprises and large enterprises.

Large enterprises segment accounted for the largest market share in 2025. This is owing to their high investment capacity in cloud networking, SD-WAN, and secure multi-site connectivity solutions to support complex and widespread operations. These organizations increasingly adopted NaaS platforms to improve network scalability, automate traffic management, strengthen cybersecurity, and efficiently manage hybrid workforce environments across global business locations.

Small and medium sized enterprises segment is anticipated to grow at the highest CAGR of 25.8% over the forecast period. This is owing to increasing demand for cost effectiveness, subscription-based, and cloud-managed networking solutions that enable scalable connectivity and secure remote operations without heavy upfront infrastructure investments.

By Application

Growing Demand for Secure Enterprise Connectivity Strengthening Wide Area Network Segment Dominance

Based on application, the market is categorized into wide area network, virtual private network, cloud based services, bandwidth on demand, and others.

Wide area network segment is anticipated to account for the largest market share. This is owing to increased enterprise demands for secure multi-site connectivity, access to cloud applications, and an overall high-performance management of networks that span geographically distributed operations. The accelerated deployment of WAN-based network-as-a-service solutions by large enterprises and telecommunications service providers continued to grow based on the rapid adoption of SD-WANs, hybrid work situations, and multi-cloud infrastructures.

Cloud based services segment is anticipated to grow at the highest CAGR of 25.5% over the forecast period. This is owing to accelerating adoption of multi-cloud environments, remote working models, and AI-driven enterprise applications requiring scalable, flexible, and on-demand network connectivity solutions.

By End User

Rising Adoption of Cloud Networking Solutions Fueling Corporate Customers Segment Growth

Based on end user, the market is divided into corporate customers and individual customers.

Corporate customers segment is anticipated to account for the largest market share. This is owing to their accelerated implementation of digital transformation through the adoption of such technologies as cloud networking, SD-WAN, and secure remote connectivity. Increased demand for centralized management of scalable network infrastructure from many sectors, including BFSI, IT & telecom, manufacturing, and healthcare, has supported corporate users in their continued acceptance of NaaS.

Individual customers segment is anticipated to grow at the highest CAGR of 24.9% over the forecast period. This is owing to increasing adoption of remote work, smart home connectivity, cloud gaming, and high-speed subscription-based networking services requiring flexible and on-demand network management solutions.

By Industry (Corporate Customers)

Expansion of Cloud and 5G Infrastructure Bolstered IT & Telecom Segment Dominance

Based on industry (corporate customers), the market is classified into BFSI, IT & telecom, manufacturing, healthcare, retail, and others.

IT & telecom segment witnessed a dominating market share in 2025. This is owing to the rapid expansion of cloud infrastructure, 5G deployment, and increasing adoption of software-defined networking technologies across telecom operators and IT service providers. Additionally, the industry’s focus on network virtualization, the increasing use of edge computing, and high-speed data traffic management created momentum in the adoption of scalable, AI driven network-as-a-service solutions at an accelerated pace on a global basis.

Healthcare segment is anticipated to grow at the highest CAGR of 27.5% during the forecast period. This is owing to the increasing adoption of telemedicine, connected medical devices, cloud-based healthcare systems, and secure high-speed network infrastructure required for real-time patient data management and remote healthcare services.

Network As A Service Market Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America Network As A Service Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest network as a service market share in 2024, valuing at USD 9.06 billion, and also maintained the leading share in 2025, with USD 11.21 billion. The market is expected to increase, owing to the region’s strong enterprise adoption of cloud networking, SD-WAN, SASE, and subscription-based network infrastructure, especially across the U.S. and Canada. The region also benefits from large-scale connectivity investments, for instance,

- In March 2026, AT&T announced a USD 250 billion commitment to advance U.S. 5G, fiber, and next-generation broadband networks, strengthening the infrastructure base for NaaS adoption.

These factors play a significant role in fueling the market growth.

U.S. Network as a Service Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 9.82 billion in 2026, accounting for roughly 28.4% of global sales.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is projected to record a growth rate of 20.3% in the coming years and reach a valuation of USD 8.29 billion in 2026. The market is experiencing significant growth, owing to the rising enterprise cloud adoption, SD-WAN/SASE migration, and demand for flexible OpEx-based networking across distributed offices and cloud workloads. The market growth in the region is also supported by telecom-led network modernization and consumption-based enterprise connectivity. For instance,

- In February 2025, BT launched Global Fabric, allowing multinational enterprises to provision and manage connectivity between offices, data centers, and cloud environments through an OpEx-led model, directly supporting NaaS adoption in Europe.

U.K. Network as a Service Market

The U.K. market is estimated at around USD 1.33 billion in 2026, representing roughly 3.8% of global revenues.

Germany Network as a Service Market

Germany’s market is projected to reach approximately USD 1.58 billion in 2026, equivalent to around 4.6% of global sales.

Asia Pacific

Asia Pacific region is estimated to reach USD 8.45 billion in 2026 and is expected to grow at the highest CAGR of 26.5% during the forecast period. This is owing to the rapid adoption of multicloud, enterprise digital transformation, and the increasing need for Software-Defined Networks (SDN) to accommodate cloud, artificial intelligence, and distributed operations. For instance,

- In October 2024, IDC reported that almost 90% of Asia Pacific enterprises had meaningful workload deployments across multiple public clouds, creating strong demand for scalable, secure, and cloud-managed NaaS solutions.

Furthermore, the evolving market continues to be fueled by expanding 5G networks and increasing use of managed SD-WAN/SASE in China, India, Japan, South Korea, Australia, and ASEAN markets.

China Network as a Service Market

China’s market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 2.64 billion, representing roughly 7.6% of global revenues. This is owing to large-scale 5G deployment, expansion of hyperscale cloud infrastructure, and increasing enterprise adoption of AI-driven networking and SD-WAN solutions to support smart manufacturing, industrial IoT, and digital transformation initiatives.

Japan Network as a Service Market

The Japanese market is estimated at around USD 1.30 billion in 2026, accounting for roughly 3.8% of global sales.

India Network as a Service Market

The Indian market was estimated at around USD 1.13 billion in 2026, accounting for roughly 3.3% of global revenues.

South America

South America is expected to witness moderate growth in this market during the forecast period. The South American market is set to reach a valuation of USD 1.76 billion in 2026. This is owing to rapid growth of smart city projects across South America. Brazil and Chile are investing in urban infrastructure that integrates IoT devices, smart sensors, and networking technologies to improve public safety, energy efficiency, traffic management, and other urban services.

Brazil Network as a Service Market

Brazil’s market is set to reach a value of USD 0.97 billion in 2026.

Middle East & Africa

The Middle East & Africa is estimated to reach USD 2.35 billion in 2026 and expected to grow at a prominent growth rate in the coming years. This is owing to rapid cloud adoption, 5G rollout, smart city investments, and government-led digital transformation programs across GCC countries, Israel, Turkey, and South Africa, which are increasing demand for scalable, secure, and cloud-managed network infrastructure.

GCC Network as a Service Market

The GCC market is set to reach a value of USD 0.91 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Cloud-Managed Networking and Strategic Partnerships by Key Players to Propel Market Growth

The global market holds a semi-consolidated market structure, with prominent players such as Verizon Communications Inc., AT&T Inc., Lumen Technologies, Inc., BT Group plc, and Vodafone Group Plc holding significant positions. These companies are driving network as a service market growth through continuous investments in cloud-managed networking, SD-WAN, SASE, private 5G, and secure enterprise connectivity solutions. Advancements in technologies such as AI-driven network automation, edge computing, network virtualization, and zero-trust security are enabling enterprises to manage distributed networks with improved scalability, reliability, and operational efficiency.

Other notable players in the global market include Hewlett Packard Enterprise Company, Cisco Systems, Inc., Tata Communications Limited, Telefónica, S.A., and Megaport Limited. These companies are increasingly focusing on expanding NaaS portfolios, improving network orchestration, strengthening cloud connectivity, and integrating security capabilities into service-based networking models. Strategic initiatives such as partnerships with cloud providers, expansion of SD-WAN and SASE offerings, investment in AI-enabled network management, and entry into new regional markets are expected to strengthen their market positioning.

LIST OF KEY NETWORK AS A SERVICE COMPANIES PROFILED IN REPORT

- Verizon Communications Inc. (U.S.)

- AT&T Inc. (U.S.)

- Lumen Technologies, Inc. (U.S.)

- BT Group plc (U.K.)

- Vodafone Group Plc (U.K.)

- Hewlett Packard Enterprise Company (U.S.)

- Tata Communications Limited (India)

- Megaport Limited (Australia)

- Telefónica, S.A. (Spain)

- Cisco Systems, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: AT&T announced a USD 250 billion long-term investment commitment to expand fiber, 5G, and next-generation broadband infrastructure across the U.S., supporting growth in cloud-managed and NaaS-based enterprise networking services. The investment aims to strengthen secure connectivity, SD-WAN deployment, and AI-driven network operations.

- June 2025: Cisco partnered with Airtel Uganda to launch a subscription-based network as a service solution that gives businesses access to scalable, secure, and fully managed network infrastructure without upfront hardware investment.

- April 2025: Hewlett Packard Enterprise expanded HPE Aruba Networking Central with new virtual private cloud and on-premises deployment options for enterprises needing stronger data sovereignty, security, and regulatory control. This strengthens HPE’s NaaS positioning by offering AI-powered network management across public SaaS, dedicated VPC, on-premises, and NaaS deployment models.

- February 2025: BT launched Global Fabric, a cloud-centric networking platform that enables enterprises to dynamically connect applications, cloud environments, and branch locations through an on-demand service model. The launch strengthens BT’s network as a service portfolio by offering automated provisioning and AI-driven network orchestration capabilities.

- January 2025: Verizon Business expanded its AI Connect portfolio to support enterprise AI workloads through integrated networking, private 5G, edge computing, and cloud connectivity services, strengthening its position in the NaaS market. The solution is designed to help enterprises manage high-bandwidth AI applications with scalable and secure network infrastructure.

- October 2024: Megaport launched its NaaS offering in Milan, Italy, establishing cloud connectivity points of presence with AtlasEdge, Data4, Equinix, and Retelit. This expansion strengthened Megaport’s European NaaS footprint by enabling enterprises to access cloud, data center, and edge connectivity through an on-demand platform.

- September 2024: Lumen Technologies partnered with Microsoft to enhance AI-enabled cloud networking and edge connectivity capabilities, helping enterprises support generative AI workloads with low-latency network services. The partnership strengthens Lumen’s NaaS offerings through integrated cloud, edge, and security solutions.

REPORT COVERAGE

The global network as a service market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021 – 2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026 – 2034 |

|

Historical Period |

2021 – 2024 |

|

Growth Rate |

CAGR of 23.5% from 2026 to 2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Type

By Enterprise Type

By Application

By End User

By Industry (Corporate Customers)

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 28.25 billion in 2025 and is projected to reach USD 187.18 billion by 2034.

In 2025, the North America’s market value stood at USD 11.21 billion.

The market is growing at a CAGR of 23.5% during the forecast period of 2026-2034.

By type, WAN as a service segment led the market.

Growing adoption of cloud-first and hybrid IT environments is driving NaaS demand.

Verizon Communications Inc., AT&T Inc., Lumen Technologies, Inc., BT Group plc, and Vodafone Group Plc are the top players in the global market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us