Non-Dairy Butter Market Size, Share & Industry Analysis By Source (Soy, Peanut, Pistachio, Cashew, Almond, and Others), By Distribution Channel (B2B and B2C [Hypermarkets/Supermarkets, Convenience Stores, Grocery Stores, and Online Sales Channels]), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

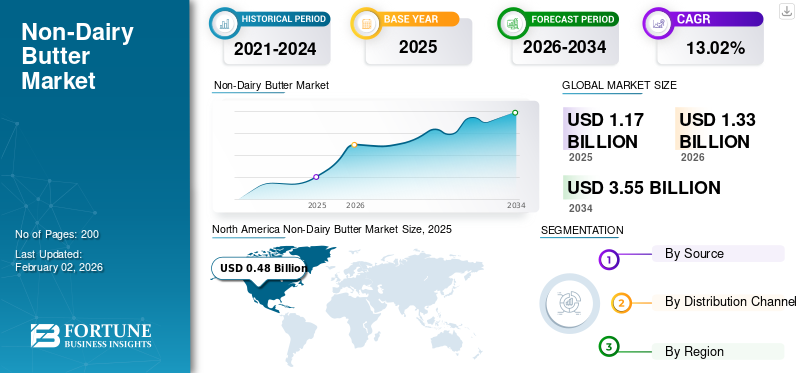

The global non-dairy butter market size was valued at USD 1.17 billion in 2025 and is projected to grow from USD 1.33 billion in 2026 to USD 3.55 billion by 2034, exhibiting a CAGR of 13.02% during the forecast period. North America dominated the non-dairy butter market with a market share of 41.24% in 2025.

The market is advancing steadily due to changing consumer patterns and increased awareness of health benefits and environmental sustainability. The increasing inclination toward dairy alternatives is being boosted by the growing rates of lactose intolerance, ethical drivers concerning animal welfare, and growing alignment with plant-centric diets. The brands are enhancing their product offerings by introducing clean-label products, differentiated tastes, and improved nutritional content to address changing consumer needs, reinforcing their competitive positions. Regulatory support for plant-based food innovation and the burgeoning growth of retail shelf space for vegan foods are anticipated to drive momentum. Conagra Brands Inc., Flora Food Group B.V., Miyoko’s Creamery, The Leavitt Corporation, and Pintola are a few established players operating in the market.

Download Free sample to learn more about this report.

Non-Dairy Butter Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 1.17 billion

- 2026 Market Size: USD 1.33 billion

- 2034 Forecast Market Size: USD 3.55 billion

- CAGR: 13.02% from 2026–2034

Market Share:

- North America dominated the non-dairy butter market with a 41.24% share in 2025, driven by rising consumer health consciousness, a strong trend toward plant-based foods, and expanding retail availability.

- By source, the soy segment is expected to retain the largest market share in 2025, supported by its high-quality protein content, widespread consumer acceptance, and appeal to those with peanut allergies.

Key Country Highlights:

- United States: Holds a major market share due to strong consumer interest in plant-based, sustainable, and healthy lifestyle products.

- Germany: High demand is driven by the country's leading rates of vegetarianism and veganism within Europe.

- China: A key market due to the traditional popularity of soy products and a consumer shift toward dairy-free foods driven by changing lifestyles.

- Brazil: Market growth is fueled by a rising millennial interest in plant proteins and growing health concerns among the population.

MARKET DYNAMICS

MARKET DRIVERS

Growing Focus on Plant-based Protein Foods to Drive Market Growth

Over the past decade, there has been a growing consumer focus on health and a rising interest in proactive nutrition. The COVID-19 pandemic also accelerated interest in functional foods, which helped deliver health and wellness benefits. With increasing health consciousness among consumers prioritizing their health, the appeal for protein-based foods and beverages is expected to grow over the forecast period. In addition, consumers associate proteins in their diet with various health benefits, including muscle health and tone, weight management, increased energy, and overall health and wellness.

Furthermore, the Recommended Dietary Allowance (RDA) for protein in the human body is 0.8 grams per kilogram of body weight. Therefore, broader awareness of the various benefits of protein drives the market for protein-based products. The manufacturers have been using this opportunity to develop an array of protein products with a "health halo" positioning. For instance, in March 2021, Pintola, an Indian brand of peanut butter and other healthy food products, launched India’s first USFDA-certified High Protein Peanut Butter. The new product is designed especially for people who are concerned about their health and perform physically strenuous activities.

MARKET RESTRAINTS

High Production Costs and Supply Chain Complexities to Hinder Market Growth

The rising cost of plant-based ingredients, processing, and loopholes in the supply chain hampers the global plant-based butter market growth. The ingredients, such as coconut oil, olive oil, almond butter, and cashew-based fats, which have superior quality and purity, substantially increase production costs. Additionally, transporting and storing such ingredients can be expensive and complicated and impact the pricing strategy and go-to-market initiatives. Firms must apply cost-effective sourcing and advanced manufacturing processes to boost their profitability and the cost efficiency of their products.

MARKET OPPORTUNITIES

Increasing Vegan Food Consumers to Offer Opportunities for Market Expansion

Veganism has grown in popularity in recent years and is expected to rise over the forecast period. According to the Vegetarian International Voice for Animals Organization, in 2022, the U.K. had the highest number of vegans in the country, with 3.2% of the population. Vegan diets tend to have rich nutrients and low saturated fats, which help people reduce their risks of diabetes and heart disease. According to the American Heart Association (AHA), consuming foods that contain high fat, such as meat, cheese, and butter, may lead to rising cholesterol levels. Therefore, the growing perception of veganism as a more sustainable option and the ever-increasing millennial population adopting western snacking habits propel the product demand.

NON-DAIRY BUTTER MARKET TRENDS

Rising Inclination toward Clean Label Products to Fuel Industry Growth

In recent years, there has been a rise in the consumer demand for food products that are perceived as wholesome, natural, and minimally processed. This shift in consumer preferences has led to the emergence of the “clean label” trend, which has also been reflected in the non-dairy butter market. Consumers are increasingly looking for foods with sustainable and natural ingredients. Non-dairy butter fits the trend by providing a plant-based substitute with perhaps fewer artificial ingredients, a lesser impact on the environment, and an emphasis on transparency. The consumer preference is fueled by factors such as health awareness, ethical and sustainable eating, and transparency issues, which further push the global non-dairy butter market growth.

Segmentation Analysis

By Source

High Protein Source and Popularity to Boost Soy Segment Expansion

Based on source, the market is divided into soy, peanut, pistachio, cashew, almond, and others.

The soy segment dominates the global market. Soybeans are known to be an excellent source of high-quality protein with all the essential amino acids. The acceptability and popularity of food products derived from soy are increasing owing to various nutritional and health benefits. In addition, soy butter is gaining traction, presenting a healthy option to peanut butter for consumers with peanut butter allergies, further driving segment growth.

The peanut butter segment will significantly expand, driven by its rich flavor and nutritional values. The creamy texture and nutty flavor of the product are a household favorite and a crucial ingredient for different food preparations. As the demand for convenient and healthy foods keeps increasing, peanut butter has made its way into different markets, where it is faster becoming a popular food option.

By Distribution Channel Type

Ease of Shopping and Accessibility to Boost B2C Segment Growth

Based on distribution channel, the market is bifurcated into B2B and B2C.

The B2C segment dominates the global non-dairy butter market share. The B2C segment includes supermarkets/hypermarkets, convenience stores, online retail, and others. As plant-based foods become mainstream around the globe, they are gradually occupying the shelf spaces in supermarkets and hypermarkets, replacing dairy products. The growing consumer interest in non-dairy butter is influencing brands and major players to develop new products to fill the supply and demand gap. This has led to more plant-based butter options occupying more shelf space in the supermarkets. Along with this, the supermarkets and hypermarkets offer the ease of shopping for other grocery items all under a single roof, thereby luring consumers toward them.

The online segment is poised to grow with a high CAGR over the forecast period. The online retail is picking up pace due to e-commerce expansion, direct-to-consumer (DTC) brand strategies, and subscription-based models. The ability to shop a wider selection of specialty and international brands at their fingertips, along with special online offers, is further attracting tech-savvy buyers.

Non-Dairy Butter Market Regional Outlook

By geography, the market is categorised into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Non-Dairy Butter Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 0.48 billion in 2025, capturing 41.24% of global revenue, and is estimated to reach USD 0.55 billion in 2026. The North America non-dairy butter market is the leading one in the global market and is primarily driven by the rising consumption of plant-based foods and expanding retail channels in the region. The growing health consciousness among consumers has nudged them to seek more healthful options. Key players have been launching innovative products to meet the rising demand. For instance, in October 2023, Wesson, a brand owned by Richardson International Ltd., launched a new plant-based butter. The new product is launched to appeal to consumers who focus on healthier lifestyles and high-quality foods.

The U.S. holds a major share in the North America market, attributed to the rising interest of consumers toward plant-based, safe, and sustainable products, along with leading a healthy lifestyle. According to a study by the Good Food Institute (GFI) and Plant-based Food Association (PBFA), consumers are turning toward plant-based foods owing to their increasing health concerns, which increased the plant-based food sales by 6.2% in 2021 compared to 2020.

Download Free sample to learn more about this report.

Europe

In 2025, Europe held 19.39% of the global market, reaching a valuation of USD 0.23 billion, and is projected to grow to USD 0.26 billion in 2026. In Europe, heightening health consciousness, sustainability concerns, and increasing adoption of plant-based diets post-COVID-19 continue to drive the non-dairy butter industry expansion. The growing incidences of lactose intolerance and the shift toward vegan butter compared to traditional dairy butter in the region have led to a larger consumer base opting for a vegan diet. The gradual inclination of consumers toward veganism is growing in various countries in the region as they want to reduce animal protein intake in their daily diets due to environmental and health factors. Germany has the highest rate of vegetarianism in comparison to its other European neighbors. According to a survey by Veganz Group AG, a food brand from Berlin, in 2020, about 2.6 million vegans in Germany represented 3.2% of the population. In addition, the growing variety of plant-based products available in the market and innovation taking over to address the changing desires of consumers is driving the region’s market growth.

Asia Pacific

The market in Asia Pacific reached USD 0.43 billion in 2025, representing 36.57% of total market revenue, and is projected to reach USD 0.49 billion in 2026. The Asia Pacific non-dairy butter market is primarily driven by the calorie concerns and higher prevalence of obesity, that made consumers shift to vegan diets and adopt dairy alternatives. The consumption of soy milk has traditionally been seen in the region, especially in countries such as Japan, Vietnam, China, and others. Along with this, the abundant availability of soybeans in the region allows easier processing and accessibility to soy and its products for manufacturers. For instance, in June 2024, Fuji Oil Group launched soy milk cream butter, a new plant-based product made from soy milk using Fuji Oil’s proprietary Ultra Soy Separation (USS process). China is among the key countries in the region, which is a major consumer of plant-based dairy alternatives, attributable to its popularity amongst consumers as a source of protein. The changing lifestyles of consumers have influenced them to shift toward dairy-free food, including butter.

South America

South America's market is driven by the rising shifts toward reducing or completely abandoning the consumption of animal-based products, such as dairy items, due to factors, including improving health, animal and environmental welfare concerns. The trend is observed mainly among millennials due to their growing interest in plant proteins. According to a survey report by DuPont Nutrition & Biosciences, in 2019, 67% and 65% consumers were interested in plant protein in Brazil and Argentina, respectively. Along with this, there is a rising health concern since the obese population has grown in recent years. Rapid urbanization and growing awareness of environmental preservation are key drivers of increased plant-based food consumption. Urbanization influences dietary shifts by changing lifestyles, income levels, and food availability, often leading to more diverse diets that can include more plant-based options. Furthermore, the rising popularity of high-quality premium vegan products, particularly among the region’s affluent class, is driving the growth of the market.

Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 0 billion, representing 0.11% of global demand, and is projected to grow to USD 0 billion in 2026. The non-dairy butter market in the Middle East and Africa is growing at a steady pace, as consumers in the region are diversifying their consumption patterns and diets and are willing to try out new plant-based alternatives to dairy products. The changes in food consumption patterns are mainly driven by urbanization as well as exposure to Western food culture. Various niche and local players are also coming up with their innovative dairy alternative products in the Middle East and African markets. This is mainly to meet the consumers’ demand as they gradually steer away from dairy products due to health conditions such as lactose intolerance, or they choose a vegan lifestyle, upon understanding the detrimental effects of animal products on the environment and the consequences faced by animals. For instance, in February 2020, Amarlane Foods, an Israeli-based company, launched a dairy alternative, Betterine, a vegan butter. The new product is non-GMO, contains no trans fats or lactose, and is certified Orthodox Union (OU) Kosher.

Latin America

Latin America maintained a strong presence in the global market, reaching USD 0.05 billion in 2025, accounting for 4.60% share, and is expected to reach USD 0.06 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Depict Growing Focus on Innovative Launch to Expand their Business

The pioneers in the global plant-based butter market emphasize expanding their product offerings and scaling up their production capacity, which helps them to meet the growing product demand.

The strongly evolving plant-based diet preference globally leads the product demand and it unlocks an opportunity for industry players to expand their consumer base across the world. Thus, the producers are emphasizing various approaches to enter the new marketplace, which also aids them in achieving a more competitive advantage while concentrating on serving new consumers. For instance, in July 2023, Naturli´ Foods A/S, a Danish plant-based food manufacturer, debuted its vegan butters in the U.S. The new product is made with cocoa butter and almond butter.

LIST OF KEY NON-DAIRY BUTTER COMPANIES PROFILED

- Conagra Brands Inc. (U.S.)

- Flora Food Group B.V. (Netherlands)

- Miyoko’s Creamery (U.S.)

- Wayfare Food (U.S.)

- Prosperity Organic Food Inc. (U.S.)

- Pintola (India)

- Alpino Health Foods (India)

- The Leavitt Corporation (U.S.)

- Vegan Way (UAE)

- Naturli Foods A/S (Denmark)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Maison Linotte, a French luxury pastry brand, launched a new generation of plant-based butter, called Purely. The new product is ideal for chefs and pastry lovers and made from organic ingredients and is free of allergens, palm oil, and additives.

- September 2024: Flora Food Group B.V., a Dutch food company, expanded its range of plant-based products with the launch of a new smoked garlic-flavored plant butter. The new product adds a versatile and rich taste to vegan recipes.

- June 2024: Miyoko’s Creamery, an American food producer, launched two new flavors of oat milk butter, including Garlic Parm and Cinnamon Brown Sugar. The product consists of organic sunflower oil, organic whole grain oat milk, herbs, and other ingredients.

- December 2023: Táche, a food and beverage company that produces pistachio milk, launched Pot de PisTÁCHE pistachio butter from pistachio milk. The new product contains a creamy, subtle, nutty, and sweet profile.

- March 2023: Apis India, one of the leaders in the organized honey trade market, launched a new peanut butter range. The product is available in two variants, including creamy and crunchy.

REPORT COVERAGE

The global non-dairy butter market report provides the market size and forecast on the basis of various segments. It includes details on the market dynamics and market trends over the forecast period. It offers information about the key regions/countries, key industry developments, new product launches, and details on partnerships, mergers, and acquisitions. The report also covers a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 13.02% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Source

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size is projected to grow from USD 1.33 billion in 2026 to USD 3.55 billion by 2034

The market is expected to exhibit a CAGR of 13.02% during the forecast period of 2026-2034.

The B2C segment leads the market by distribution channel.

The rising focus on plant-based protein foods is a key factor set to drive market growth.

Conagra Brands Inc., Flora Food Group B.V., Miyokos Creamery, The Leavitt Corporation, and Pintola are the top players in the market.

North America dominated the market in 2024.

The rising trend of clean label products is anticipated to fuel product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us