Office Chairs Market Size, Share & Industry Analysis, By Type (Task/Operational, Ergonomic/Performance, Executive, and Others), By Material (Mesh, Fabric, Leather & PU Leather, and Others), By End-user (Commercial Offices/Corporate, Home Offices, Institutional, and Others), By Distribution Channel (Offline Contract Dealers/Direct B2B, Retail Stores (Physical), Online/E-Commerce, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

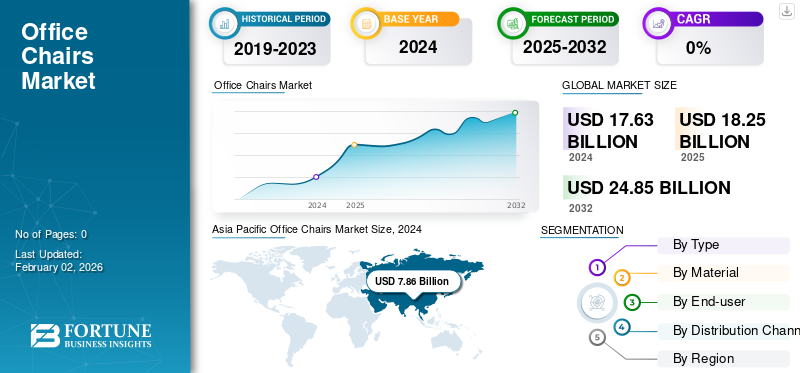

Office Chairs Market Size and Future Outlook

The global office chairs market size was valued at USD 18.25 billion in 2025. The market is projected to grow from USD 18.95 billion in 2026 to USD 28.49 billion by 2034, exhibiting a CAGR of 5.23% during the forecast period. Asia Pacific dominated the global office chairs market with a market share of 44.89% in 2025.

The office chairs have gained prominence in recent years as businesses and workers place greater emphasis on productivity, ergonomics, and hybrid work environments. Public data from BIFMA indicates that post pandemic-driven decline in 2020, the North American office and institutional furniture industry, rebounded abruptly, growing 18.4% in 2022. This reflects renewed investment in workplace infrastructure and seating upgrades as offices reopened. Growing awareness of workplace ergonomics, supplemented by increasing recognition of musculoskeletal risks and occupational health guidelines, is encouraging businesses to substitute basic seating with advanced ergonomic chairs. Moreover, office reopening and corporate workspace refurbishments are boosting large-scale procurement as businesses redesign offices for hot-desking, collaboration, and activity-based working driving market growth.

Few well established players in the market include Steelcase, MillerKnoll (Herman Miller + Knoll), HNI Corporation (HON, Allsteel), Haworth, Okamura, and Kokuyo. These key companies are mainly expanding product offering by diverting into hybrid-work and home-office segments, with online retail setup and direct-to-consumer (D2C) channels. In addition, players also emphasize upon chairs ergonomics and novel characteristics, represented by chairs such as the Steelcase Gesture and Herman Miller Aeron, highlighting cutting-edge posture-support technologies.

Download Free sample to learn more about this report.

Office Chairs Market Key Takeaways

- 2025 Market Size: USD 18.25 billion

- 2026 Market Size: USD 18.95 billion

- 2034 Forecast Market Size: USD 28.49 billion

- CAGR: 5.23% from 2026–2034

- Asia Pacific dominated the office chairs market with a 44.89% share in 2025.

- The task/operational chair segment is projected to lead the market with a 53.19% share in 2026.

- The mesh material segment accounted for the largest market share of 37.68% in 2026.

Asia Pacific

Asia Pacific generated USD 8.19 billion in 2025 and is expected to reach USD 8.56 billion in 2026, supported by expanding office infrastructure, growing IT and service industries, and rising demand for workplace seating solutions.

North America

North America reached USD 4.58 billion in 2025 and is projected to grow to USD 4.74 billion in 2026, driven by strong adoption of ergonomic office furniture and workplace modernization initiatives.

Europe

Europe accounted for USD 4.09 billion in 2025 and is expected to reach USD 4.21 billion in 2026, supported by stringent workplace standards, sustainability initiatives, and steady demand from corporate and institutional sectors.

U.S.

The U.S. market is projected to reach USD 4.11 billion in 2026, supported by increasing ergonomic awareness, hybrid work trends, and continuous replacement demand across commercial workplaces.

Japan

The Japan market is projected to reach USD 0.71 billion in 2026, driven by demand for ergonomic seating solutions, workplace modernization, and growing focus on employee comfort and productivity.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growing Emphasis on Workplace Ergonomics to Drive Market Growth

Increasing global focus on workplace comfort, productivity, and people's efficiency in their working environment, supported by both growing regulatory and health awareness and employer priorities drive the office chairs market growth. As businesses identify the direct correlation between employee’s well-being and their increased work output, they are enhancing from simple seating arrangements to advanced ergonomics spaces including conference chairs that offer adjustable lumbar support mechanism and posture-correcting designs. This trend is strengthened by studies and occupational health guidelines suggesting that poor seating arrangements is contributing to MSDs (musculoskeletal disorders), which is one of the major workplace related concerns. To overcome this, employers are increasingly focusing on offering ergonomically certified seating to reduce fatigue, improve long-duration comfort for desk-based workers, and avoid injuries. Moreover, the growing inclination towards flexible and hybrid work culture has widened this scope to home offices, where employees are investing in high-performance chairs to support extended working hours, further consolidating market growth.

MARKET RESTRAINTS

Higher Price Range of Premium Ergonomic Chairs to Restrict Market Expansion

Hefty pricing associated with advanced ergonomic seating is one of the major aspects, limiting its adoption amongst consumers, particularly budget-sensitive buyers, restraining market growth. Cutting-edge technology incorporated within seating systems that feature adjustable lumbar support, mesh engineering, multi-pivot mechanisms, and certified ergonomic designs often carry expensive pricing over standard task chairs. Several organizations, especially small and medium sized businesses or institutions run on tight budgets. Substantial ergonomic seating upgrades can put large strain on their finances and expenditure ability, slowing adoption as well as replacement rate. Consumers of home-office environments also hesitate to spend on advanced chairs owing to less awareness of its long-term benefits compared to short-term cost considerations. Thus, high upfront cost of the product continues to stand as a barrier to large-scale adoption, hampering overall market growth.

MARKET OPPORTUNITIES

Post-Pandemic Expansion of Hybrid and Flexible Workplaces Boost Market Opportunities

Continued global expansion of hybrid and flexible work environments has offered several growth opportunities for key players in the market, which is reforming how firms design and furnish their workplaces. With businesses undertaking hybrid work culture, offices are being reconfigured to support hot-desking, activity-based work zones, touchdown areas, and collaborative zones, each demanding new sets of seating arrangements beyond conventional fixed workstations. This transition leads to demand for ergonomic, comfortable, versatile, lightweight, and easy to configure chairs that can serve multiple purposes across dynamic layouts. Simultaneously, the work-from-home culture has gained momentum since the COVID-19 with individuals investing in superior-quality advanced chairs. This trend has created a sustained growth opportunity for key market players to innovate and launch custom chair designs to suit best to one’s requirement, expanding both commercial and consumer demand.

OFFICE CHAIRS MARKET TRENDS

Incorporation of Recycled and Sustainable Materials Pose as Market Trends

One of the major influential trends shaping the market is the blending and integration of low-impact, sustainable, and recyclable materials into the making of high-end ergonomic chairs. Manufacturers of furniture and chairs are responding better to corporate environmental, social, and governance (ESG) priorities and regulatory pressures by unveiling chairs designed with bio-based foams, recycled plastics, low-VOC finishes, and easy-to-dissemble components that uplift and support circular manufacturing. For instance, many well-recognized global office-furniture brands have assimilated post-consumer and ocean-bound recycled plastic into their signature chair portfolio, highlighting a notable move towards eco-friendly responsible production. This sustainability trend not only resonates with eco-conscious consumers but also aligns with the corporate procurement policies who increasingly mandate eco-certified furniture.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Large-Scale Procurement and Higher Affordability Aspect Driving Growth of Task/Operational Chair Segment

On the basis of type, the market is segmented into task/operational, ergonomic/performance, executive, and others.

The task/operational chair segment is projecteed to dominate the market with a share of 53.19% in 2026. These chair types form the backbone of seating arrangements across large corporate workspaces, call centers, shared workplaces, and institutional environments where the highest chunk of employees use standard workstation seating. Moreover, their affordability over high-performance and executive chairs, combined with their functionality and versatility, sets them as ideal choices for large-scale procurement.

The ergonomic/performance chair type segment is projected to expand at a fastest CAGR of 5.20% over the projected years. Growing awareness regarding the benefits of ergonomically designed chairs, a transition towards health-focused, premium seating, and increased hybrid and home-office usage are some of the factors likely to drive the segmental growth.

To know how our report can help streamline your business, Speak to Analyst

By Material

Lightweight, Minimalist Design, and Adaptation to Dynamic Sitting Drive Mesh Material Dominance

By material, the market is segmented into mesh, fabric, leather & PU leather, and others.

The mesh material captured the largest share 37.68% of the market in 2026. Mesh stands as the preferred material for office chairs due to properties such as breathability, temperature regulation, and comfort provided for extended periods. All of these factors contribute to today’s ergonomic-driven workspace standards and therefore have high demand in both offices and work-from-home environments.

The fabric material chairs segment is expected to grow at second-fastest CAGR of 4.63% over the forecast period. Advances in performance textiles, such as antimicrobial, stain-resistant, and recycled fabrics are magnifying their appeal amongst end-users and sustainability-focused buyers which is expected to drive segment growth.

By End-user

Regular Replacement Cycles and Large-Scale Procurements Driving Growth of Commercial Offices/Corporate Segment

Based on end-user, the market is segmented into commercial offices/corporate, home offices, institutional, and others.

Commercial offices/corporate end-user segment accounts for the largest market share 55.73% 2026 since multinationals, bigger organizations, and enterprise workspaces account for the highest volume of seating installations across floors, departments, and entire campus. Massive floor spaces in the corporations demand standardized workstations seating for hundreds of thousands of employees, leading to large-scale procurement cycles that far outpace the purchasing capacity of smaller institutions or home offices. Moreover, corporates typically follow regular replacement cycles and compliance-driven upgrades, further sustaining consistent high-volume demand.

The home office segment is projected to grow the fastest CAGR, boosted by rising individual investment in comfortable seating for long-term hybrid work adoption or remote work setups. Moreover, strong e-commerce demand and shifting consumer buying trends continue to fast-track growth of the segment.

By Distribution Channel

Wide Product Assortments and Affordable Mass-Market Options Driving Growth of Offline/Direct B2B Segment

Based on distribution channel, the market is segmented into offline contract dealers/direct B2B, retail stores (physical), online/e-commerce, and others.

The Offline Contract Dealers/Direct B2B segment is expected to lead the market, contributing 46.07% globally in 2026. These dealers fulfill the bulk orders coming from corporate end-users, institutional buyers, and government procurement. These end-use consumers usually rely on established dealer networks and direct B2B vendors for large-scale seating installations. Well-recognized and globally established manufacturers including Haworth, MillerKnoll, HNI, and Steelcase structure their business operations and sales primarily around contract dealers, consolidating the dominance of this distribution channel.

In addition, online/e-commerce is the fastest-growing channel and is projected to grow at a CAGR of 5.19% during the study period. Expansion of D2C (direct-to-consumer) brands by key players, rising home-office demand, and rising buyer comfort with one click away door-step delivery is building segmental growth.

Office Chairs Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific recorded a market size of USD 8.19 Billion in 2025, capturing 44.89% of the global market share, and is projected to reach USD 8.56 Billion in 2026. Regional market growth is majorly supplemented by large-scale commercial office expansion, growth of IT/ITeS, tech, and service sectors, massive manufacturing base and lower product cost advantage, along with rapid expansion of co-working and flexible workspaces. The region hosts some of the fastest-growing markets globally, including India, China, Indonesia, the Philippines, and Vietnam, where corporate expansion and rapid urbanization are increasing the number of office workstations directly amplifying the product demand. The Japan market is projected to reach USD 0.71 billion by 2026, the China market is projected to reach USD 2.94 billion by 2026, and the India market is projected to reach USD 2.67 billion by 2026.

Asia Pacific Office Chairs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America generated USD 4.58 Billion, contributing 25.11% to global market revenue, and is projected to grow to USD 4.74 Billion in 2026. Growth is driven by strict workplace ergonomics and occupational safety standards, along with the widespread adoption of ergonomically designed office chairs. The region is home to a large concentration of corporate offices, universities, healthcare systems, and government institutions that require continuous procurement and replacement of seating solutions. For instance, MillerKnoll reported USD 3.63 billion in FY2024 revenue, while Steelcase generated USD 3.2 billion in revenue, reflecting strong demand for office furniture. The U.S. remains the largest and most influential market in the region, supported by workplace modernization initiatives, growing ergonomic awareness, regular replacement cycles, and increasing demand for adjustable office chairs driven by hybrid and remote work trends. The U.S. market is projected to reach USD 4.11 billion by 2026.

Europe

The Europe market accounted for USD 4.09 Billion in 2025, representing 22.43% of the global industry, and is expected to reach USD 4.21 Billion in 2026. securing its position as the third-largest regional market. The market is supported by stringent workplace standards, rising awareness of ergonomics, and a growing emphasis on sustainability and circular design principles. A strong corporate and institutional presence across the region continues to generate steady demand for office seating solutions. In addition, Europe’s high broadband penetration and well-developed e-commerce infrastructure encourage ongoing consumer purchases of ergonomic office chairs, further strengthening regional market growth during the forecast period. The UK market is projected to reach USD 0.56 billion by 2026, while the Germany market is projected to reach USD 0.81 billion by 2026.

South America

South America is expected to witness significant growth during the forecast period. The regional market is projected to reach a valuation of USD 0.74 billion in 2025. Growth is primarily driven by the expansion of corporate workplaces and the increasing presence of IT and BPO industries across key economies such as Brazil, Argentina, Colombia, and Chile. Rising investments in commercial infrastructure and office development projects are further supporting market expansion across the region.

Middle East & Africa

The Middle East & Africa market generated USD 0.64 Billion in 2025, representing 3.52% of the global market landscape, and is expected to reach USD 0.67 Billion in 2026. The Middle East & Africa region is also anticipated to experience notable growth over the forecast period. Increasing business activity, ongoing urban development, and rising investments in commercial and institutional infrastructure are contributing to market expansion across the region. In the Middle East & Africa, the UAE market is set to attain a value of USD 0.07 billion in 2025, supported by the country’s growing corporate sector and demand for modern workplace solutions.

COMPETITIVE LANDSCAPE

Key Industry Players:

Intensifying Competition Drives Innovation and Strategic Partnerships in Market

The global market is fierce and consolidated, with the presence of global giants such as Haworth, Steelcase, Kokuyo, MillerKnoll, HNI, and Okamura competing against several regional and local manufacturers. Key players in the market distinguish themselves via sustainability-driven approach, ergonomic innovation, and wide range of product offerings custom-made to suit institutional, corporate, and home-office needs. Investment in advanced ergonomics is one of the major competitive strategies adopted by players, mainly focusing on breathable mesh technologies and posture-adaptive mechanisms to achieve an edge in the highly competitive product category. Players are also integrating circular design and recyclable materials, pursuing sustainability leadership, and thus meeting corporate ESG expectations. Moreover, digital visualization tools, strong dealer network, expansion of D2C channels, and strategic partnership or collaborations are some of the other few strategies adopted by market players.

LIST OF KEY OFFICE CHAIRS COMPANIES PROFILED

- Steelcase Inc. (U.S.)

- MillerKnoll (Herman Miller + Knoll) (U.S.)

- HNI Corporation (HON, Allsteel) (U.S.)

- Haworth Inc. (U.S.)

- Okamura Corporation (Japan)

- Kokuyo Co., Ltd. (Japan)

- Kinnarps AB (Sweden)

- Vitra International AG (Switzerland)

- Interstuhl Büromöbel GmbH & Co. KG (Germany)

- UE Furniture Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Chinese manufacturer UE Furniture, acquired a production facility in Timiș County, Western Romania, enhancing its manufacturing capacity and international supply-chain influence. With this expansion the company continues to expand OEM and ODM partnerships with global brands.

- March 2024: MillerKnoll, formed in 2021 between the merger of Herman Miller and Knoll, has expanded partnerships with e-commerce platforms and improved its direct-to-consumer ecosystems, integrating Herman Miller’s strong online presence.

- May 2022: Steelcase announced that it had signed a definitive agreement to acquire HALCON, a Minnesota-based designer and manufacturer of finely crafted wood furniture for the workplace. The acquisition valued at USD 127.5 million, with potential additional consideration based on performance metric, added HALCON’s custom wood tables, desks, and credenzas to Steelcase’s existing offerings, thereby broadening the parent company’s product portfolio across private offices, collaborative spaces, and conference settings.

- July 2021: Herman Miller, completed its acquisition of Knoll, Inc., and the combined entity was named MillerKnoll. The unified product range of both these companies together has strengthened their position in the global market.

- November 2020: In a definitive agreement, Kimball International, Inc. acquired Poppin, Inc., New York headquartered, digitally-enabled commercial-furniture design firm. With this acquisition, Kimball strategically accelerated its online business capabilities while broadening its addressable market through both work-from-home and corporate offices.

REPORT COVERAGE

The global office chairs market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses porters five forces analysis, a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attributes | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.23% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Material, End-user Distribution Channel, and Region |

| By Type |

|

| By Material |

|

| By End-user |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value reached USD 18.25 billion in 2025 and is projected to reach USD 28.49 billion by 2034.

In 2025, the market value stood at USD 8.19 billion.

The market is expected to exhibit a CAGR of 5.23% during the forecast period.

The task/operator chairs office chairs led the market by type.

Growing investments in workplace infrastructure and seating upgrades, and growing awareness of workplace ergonomics, supplemented by increasing recognition of musculoskeletal risks and occupational health guidelines are driving the global market growth.

Steelcase, MillerKnoll (Herman Miller + Knoll), HNI Corporation (HON, Allsteel), Haworth, Okamura, and Kokuyo are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

With businesses undertaking hybrid work culture or permanent work-from-home is expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 129

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us