On-Board Diagnostics (OBD) Aftermarket Size By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles (LCV), and Heavy Commercial Vehicles (HCV)), By Component (Hardware [OBD Scanners, OBD Dongles], Software [PC-based Software, Apps), and Service [Training & Consulting, Integration & Maintenance, Managed Service]), By Application (Consumer Telematics, Fleet Management, Car Sharing, Usage Based Insurance (UBI)), and Regional Forecast, 2026-2034

On-Board Diagnostics (OBD) Aftermarket Size and Future Outlook

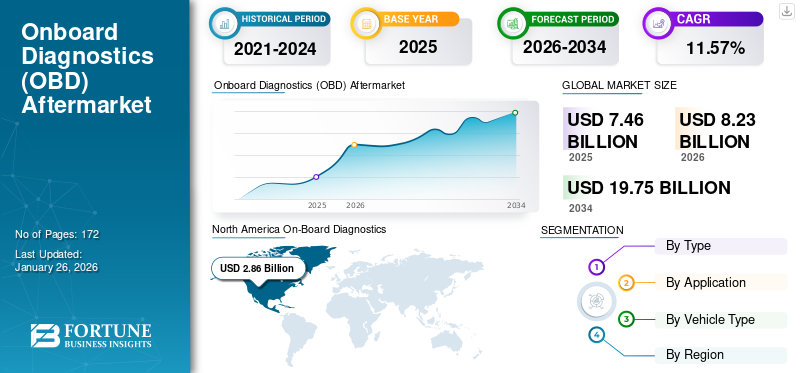

The global On-Board Diagnostics (OBD) aftermarket size was valued at USD 7.46 billion in 2025. The market is projected to grow from USD 8.23 billion in 2026 to USD 19.75 billion by 2034, exhibiting a CAGR of 11.57%. North America dominated the global market with a share of 41.70% in 2025.

The on-board diagnostics (OBD) system is designed to perform self-diagnostics and provide technicians with access to advanced information regarding various vehicle subsystems. To help reduce high mobile emissions from cars and trucks, manufacturers must build vehicles that meet strict emission standards and maintain these standards over time. Therefore, OBD systems is a part of the vehicle and it must offer universal inspection and diagnostic methods to ensure that vehicles are performing according to the required standards. Additionally, the OBD II systems enable real time monitoring of vehicle health without any help of external hand support of device.

The global on-board diagnostics (OBD) aftermarket is anticipated to grow significantly in the upcoming years owing to the integration of advanced technologies in modern vehicles. These innovations continue to improve the functionality of OBD systems, making them indispensable tools for vehicle maintenance and emissions compliance. A 2024 report by the International Association of Automotive Engineers indicates that the adoption of AI and machine learning in diagnostics significantly enhances vehicle performance and safety, propelling market growth.

The global on-board diagnostics (OBD) aftermarket is fragmented, with several global and regional players operating in this industry. Leading companies such as Robert Bosch GmbH, Continental AG, and ZF Friedrichshafen AG dominate due to their extensive product portfolios, strong regional presence, and significant industry experience.

Download Free sample to learn more about this report.

Onboard Diagnostics (OBD) Aftermarket Takeaways

- 2025 Market Size: USD 7.46 billion

- 2026 Market Size: USD 8.23 billion

- 2034 Forecast Market Size: USD 19.75 billion

- CAGR: 11.57% from 2026–2034

- North America dominated the global OBD aftermarket with a 41.70% share in 2025.

- The basic segment accounted for the largest market share of 62.61% in 2026.

- The engine segment held a leading market share of 49.48% in 2026.

North America

North America led the global market with USD 3.11 billion in 2025 and is projected to reach USD 3.42 billion in 2026, driven by strong adoption of vehicle diagnostics solutions.

Europe

Europe accounted for USD 2.58 billion in 2025, representing 34.51% of global demand, and is expected to grow to USD 2.85 billion in 2026.

Asia Pacific

Asia Pacific reached USD 1.12 billion in 2025 and is projected to expand to USD 1.26 billion in 2026, supported by increasing vehicle ownership and aftermarket activities.

U.S.

The OBD aftermarket is projected to reach USD 2.02 billion in 2026, driven by rising demand for advanced vehicle diagnostics and maintenance solutions.

Japan

The market is expected to reach USD 0.24 billion in 2026, supported by a mature automotive sector and increasing adoption of connected vehicle technologies.

Read More

Market Dynamics

Market Drivers

Integration of OBD Systems into Insurance Policies to Catalyze Market Growth

The inclusion of on-board diagnostics (OBD) aftermarket into insurance policies is increasingly recognized as important development, fueled by multiple essential factors. These advancements improve the value offering for both insurers and policyholders, allowing more tailored and effective insurance solutions.

The rise of Usage-Based Insurance (UBI) models is a key factor driving the global on-board diagnostics (OBD) aftermarket growth in the insurance industry. UBI allows insurers to determine premiums based on actual driving behavior rather than traditional metrics such as age or vehicle type. OBD systems collects real-time data on driving habits, such as speed, braking patterns, and mileage, which enables insurers to assess risk more accurately and customize premiums accordingly. This shift encourages safer driving practices and reward responsible drivers with lower premiums.

Moreover, OBD systems play a crucial role in enhancing risk assessment by collecting detailed data. Insurers can use information from OBD devices to analyze driver behavior and vehicle performance, resulting in more accurate underwriting decisions. This data-driven approach enables insurers to manage their risk portfolios more effectively, decreasing the likelihood of unexpected claims and ultimately improving profitability. This precise measurement enables the creation of customized premiums that reflect actual driving behavior rather than relying on generalized statistics.

The integration of on-board diagnostics (OBD) aftermarket into insurance policies marks a significant change in how premiums are calculated and managed. This shift has led to the emergence of Usage-Based Insurance (UBI) models, which provide enhanced risk assessment capabilities and encourage greater customer engagement.

By utilizing real-time data, insurers can personalize risk assessments and improve the efficiency of claims processing. OBD technology greatly impacts insurance premiums, making them more reflective of individual driving behavior and promoting safer driving practices. Additionally, this advancement offers cost-reduction opportunities for insurers while ensuring compliance with regulatory requirements.

Market Restraints

High Cost of On-Board Diagnostics (OBD) Systems Could Impede Market Expansion

One of the most significant barriers to adopting OBD systems is the high cost associated with advanced diagnostic devices. Many OBD systems, especially those with extensive features and connectivity options, come with a premium price tag. This can discourage potential users, particularly small automotive service providers and consumers from lower-income brackets, from investing in these technologies. The economic burden of purchasing and maintaining sophisticated OBD systems limits market growth, as cost-sensitive consumers may choose basic diagnostic tools instead.

The complexity of configuring OBD systems can deter many users, especially those without technical expertise. They may find it challenging to set up and effectively use these systems. This complexity often results in a greater need for troubleshooting and maintenance, which can further discourage potential users who might prefer simpler solutions.

Additionally, as the OBD market expands, increased competition among manufacturers can lead to market saturation. This saturation may trigger price wars, which could reduce profit margins for companies that produce OBD devices.

Market Opportunity

IoT Enabled Predictive Maintenenace to Enhance Market Growth

The Internet of Things (IoT) enables continuous monitoring of vehicle health through connected On-Board Diagnostics (OBD) systems. By collecting real-time data on various vehicle parameters such as check engine light and performance, emissions, and diagnostic trouble codes—IOT allows for the immediate identification of issues through electronic control unit. This capability promotes proactive maintenance, reducing the likelihood of breakdowns and enhancing vehicle reliability. As modern vehicles become increasingly complex, the demand for advanced diagnostic tools such as OBD solutions in the aftermarket continues to grow.

With IoT integration, OBD systems can utilize data analytics to predict maintenance needs based on actual usage patterns instead of relying solely on scheduled intervals. This proactive approach to helps both fleet operators and individual vehicle owners by identifying potential issues before they develop into major problems, preventing costly repairs and minimizing downtime. The capability to accurately forecast maintenance requirements positions IoT-enhanced OBD systems as essential tools in the aftermarket.

Furthermore, the increasing demand for efficient fleet management solutions is significantly driving the growth of the OBD aftermarket. The rise of Usage-Based Insurance (UBI) models is particularly benefiting from IoT-enabled OBD systems, which provide insurers with detailed insights into driving behaviors. This data allows for personalized insurance premiums based on actual risk profiles instead of traditional demographic factors. As more consumers choose telematics-based insurance solutions, the demand for OBD systems that support these applications continues to rise, further fueling market growth.

On-Board Diagnostics (OBD) Aftermarket Trend

Rising Demand for Vehicle Personalization to Amplify Product Demand

The technological trends shaping the on-board diagnostics (OBD) market illustrate a dynamic environment driven by enhanced connectivity, predictive analytics, customization options, and the need for regulatory compliance. As these trends continue to evolve, they are expected to significantly boost growth in the on-board diagnostics (OBD) aftermarket, improving vehicle performance and safety while addressing the changing needs of consumers in an increasingly complex automotive landscape.

One transformative trend is the integration of Internet of Things (IoT) technologies into OBD systems. IoT enables real-time data collection, transmission, and analysis, facilitating on-board diagnostics and proactive maintenance. The connectivity of modern vehicles enables for continuous monitoring of vehicle health, which improves operational efficiency and minimizes downtime. As the number of connected vehicles increases, the demand for IoT-enabled On-Board Diagnostics (OBD) solutions is expected to rise significantly.

Additionally, the growing interest in vehicle personalization is fueling demand for advanced OBD solutions that support customization. Car enthusiasts are actively seeking tools that allow them to optimize engine settings, monitor performance in real time, and make modifications while staying compliant with regulatory standards. In response to this demand, the OBD aftermarket is offering products that enable users to customize their vehicles to achieve specific performance objectives.

Download Free sample to learn more about this report.

Impact of COVID-19

The COVID-19 pandemic had a significant impact on the global on-board diagnostics (OBD) aftermarket, resulting in both immediate disruptions and long-term changes in the industry. Lockdowns and restrictions severely disrupted manufacturing and distribution, which affected the availability of diagnostic tools. This situation was especially notable due to the reliance on semiconductor chips, which faced shortages that slowed automotive production and impacted various features, including OBD systems.

During the lockdowns, many people stayed home, leading to a significant decrease in vehicle usage. As a result, there was a temporary decline in the demand for maintenance and repair services, which are essential for on-board diagnostics (OBD) tools. However, the pandemic accelerated the shift toward OBD and telematics solutions, as technicians started using OBD tools to diagnose and repair vehicles remotely. This trend is likely to persist as businesses adjust to new operational models.

Moreover, OBD tools became essential for DIY diagnostics and maintenance. This shift resulted in increased sales of OBD devices through a e-commerce platforms, as consumers sought convenient solutions for at-home usage. During the initial phases of the pandemic, automotive manufacturers faced several challenges, including temporary factory closures, supply chain disruptions, and reduced consumer purchasing power. These factors hindered the deployment and adoption of remote vehicle diagnostics systems, as companies prioritized immediate cost-cutting measures and focused on maintaining their core operations.

SEGMENTATION ANALYSIS

By Type

Growing Fleet of Modern and Electric Vehicles Creating Opportunity to Advance Diagnostic Systems to Monitor Vehicle Performance

The market is classified by type into basic and advance.

The advance segment is estimated to be the fastest-growing during the forecast period 2025-2032. The advance segment plays a crucial role in the automotive diagnostics market by enabling real-time data analysis and remote monitoring. With the increasing adoption of IoT and connected vehicles, advanced solutions are essential for predictive maintenance and OTA updates. Additionally, AI and machine learning advancements in diagnostic systems are catalyzing the segment’s growth.

The basic segment accounted for the largest market share of 62.61% in 2026. The evolution from OBD-I to OBD-II has transformed vehicle diagnostics, making them more standardized and accessible. The ongoing growth of the global OBD market is fueled by increasing vehicle complexity, regulatory demands, technological advancements, and a burgeoning aftermarket.

By Application

Engine Segment Led owing to Stricter Emissions Regulations

By application, the market is classified into engine, emission system, and others.

The engine segment is estimated to be the fastest-growing during the forecast period 2025-2032 and accounted for the largest market with a share of 49.48% in 2026. The application of on-board diagnostic systems for engine monitoring is growing due to stricter emissions regulations, enhanced diagnostic capabilities, real-time monitoring, integration with advanced technologies, increased consumer awareness, fleet management efficiency, and technological advancements. Moreover, as environmental concerns increase, governments globally are implementing stricter emissions testing regulations. OBD systems play a vital role in ensuring that vehicles comply with these regulations by continuously monitoring emission-related components and alerting drivers to any malfunctions that could lead to higher emissions. This regulatory pressure drives the adoption of advanced OBD systems in new vehicles, further catalyzing segment growth. The segment is estimated to attain 49% of the market share in 2025.

The emission system segment is estimated to be the second-fastest growing with a CAGR of 11.40% during the forecast period (2025-2032). Modern OBD systems are equipped with advanced sensors and software which enable comprehensive monitoring of various emission control components, such as catalytic converters and oxygen sensors. This capability enables real-time detection of issues that could cause excessive emissions, leading to quicker diagnostics and repairs. The ability to monitor these components effectively is crucial as vehicles become more complex and equipped with advanced technologies catalyze the growth of the segment.

By Vehicle Type

To know how our report can help streamline your business, Speak to Analyst

Passenger Car Segment Led due to Rising Demand for Personal Mobility

By vehicle type, the market is classified into passenger cars, light commercial vehicles, and heavy commercial vehicles.

The passenger car segment accounted for the largest market with a share of 58.60% in 2026. As urban areas grow, the need for personal mobility becomes more pronounced, with longer commutes and inadequate public transport systems compel individuals toward personal vehicles ownership. In addition, the growing interest in electric vehicles (EVs) is reshaping consumer preferences within the passenger car segment. This segment is foreseen to hold 59% of the market share in 2025.

The light commercial vehicles segment is estimated to be the fastest-growing during the forecast period. The exponential growth of e-commerce has significantly increased the need for efficient last-mile delivery solutions. LCVs are particularly well-suited for urban environments due ot their agility and maneuverability, enabling them to navigate congested streets and delivering goods timely. Additionally, rise in consumer expectations for faster delivery services are further propelling demand. This segment is likely to grow with a considerable CAGR of 12.40% during the forecast period (2025-2032).

Moreover, the shift toward electric and hybrid vehicles is transforming the LCV segment. Manufacturers are investing heavily in the development of electric light trucks to meet growing environmental concerns and comply with stricter emissions regulations. This trend aligns with global efforts to reduce carbon footprints, supported by government incentives promoting sustainable transportation.

North America On-Board Diagnostics (OBD) Aftermarket Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

On-Board Diagnostics (OBD) Aftermarket Regional Outlook

By region, the market is classified into North America, Europe, Asia Pacific, and Rest of the World.

North America

The market in North America reached USD 3.11 billion in 2025, representing 41.70% of total market revenue, and is projected to reach USD 3.42 billion in 2026. The region accounted for the largest market share in global on-board diagnostics (OBD) aftermarket share in 2024 due to its advanced automotive industry and high adoption of connected technologies. Government initiatives promoting vehicle safety, emissions reduction, and the development of smart infrastructure drives market growth. Moreover, the presence of automotive manufacturers and tech firms in the U.S., Canada, and Mexico fosters innovation in remote vehicle diagnostics. These advancements lead to the development of more sophisticated diagnostic systems, driving market growth in the region.

North America, spearheaded by the U.S., holds a considerable portion of the global OBD aftermarket, propelled by strict environmental regulations and the increasing use of advanced diagnostic tools. Federal laws such as the EPA’s emission standards and state regulations like California’s CARB OBD-II standards are significant contributors to this growth. These regulations necessitate that vehicles track and report issues related to emissions, leading to a higher demand for aftermarket diagnostic tools. Additionally, the growing average age of vehicles in the U.S. heightens the necessity for aftermarket OBD solutions to enhance performance and prolong vehicle longevity. The U.S. market is projected to be worth USD 2.02 billion in 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 1.12 billion, representing 15.02% of global demand, and is projected to grow to USD 1.26 billion in 2026. The region is estimated to be the fastest-growing during the forecast period, driven by rapid vehicle production and increasing demand for advanced automotive technologies. Countries such as China, Japan, and South Korea have led the development and adoption of on-board diagnostics. China is set to gain USD 0.34 billion in 2025. Increasing focus of auto insurance providers for insurtech telematics systems for vehicle health tracking and flexible insurance plans is contributing to market growth. For instance, in November 2022, OPES announced its collaboration with IMS to offer telematics-based motor insurance in Vietnam. India is projected to be valued at USD 0.32 billion in 2026, while Japan is anticipated to stand at USD 0.24 billion in the same year.

Europe

Europe contributed approximately USD 2.58 billion to the global market in 2025, accounting for 34.51% share, and is expected to reach USD 2.85 billion in 2026. Europe is the second largest market expected to hit USD 2.58 billion in 2025, exhibiting a CAGR of 12.10% during the forecast period (2025-2032). Europe's market growth is supported by its leading automotive manufacturing industry and a strong focus on innovation. The U.K. market is anticipated to hold USD 1.23 billion in 2025. The region’s emphasis on high-quality engineering and advanced technology adoption in vehicles promotes the use of on-board diagnostics. Stringent regulatory standards regarding vehicle emissions and safety in Europe necessitate the use of advanced diagnostic systems. These regulations ensure that vehicles comply with environmental and safety standards, further driving the adoption of on-board diagnostics. Germany is poised to grow with a value of USD 0.72 billion in 2026, while France is expected to reach USD 0.51 billion in the same year.

Rest of the World

Rest of the World recorded a market size of USD 0.65 billion in 2025, capturing 8.77% of the global market share, and is projected to reach USD 0.69 billion in 2026. The rest of the world is anticipated to reach a market value of USD 0.69 billion in 2026. The Rest of the World, including the Middle East, Africa, and Latin America, shows growing interest in automotive on-board diagnostics due to increasing vehicle ownership and the need for efficient vehicle maintenance. The adoption of connected vehicle technologies and smart transportation systems is on the rise, supporting market growth in these regions.

Competitive Landscape

Key Makret Players

Leading Players Are Focusing on Integrating Advanced Technologies to Gain Strong Foothold

The On-Board Diagnostics (OBD) aftermarket is highly fragmented, with numerous players competing on various factors, including pricing, technology, and service offerings. This fragmentation can lead to intense competition and price wars. The rapid pace of technological advancement requires companies to continuously innovate to maintain a competitive edge. Leading companies such as Robert Bosch GmbH, Continental AG, and ZF Friedrichshafen AG are well-positioned to capitalize on these trends through their extensive product portfolios and strong market presence. In addition, companies such as CalAmp Corporation, Geotab Inc., and HeLLA GmbH & Co. KGaA also rank highly, leveraging advanced technology and a global footprint. Emerging players such as Autel Intelligent Technology and Verizon are gaining traction driven by growing market presence and innovative solutions, further intensifying competition within the OBD aftermarket.

LIST OF KEY MARKET PLAYERS

- Autel Intelligent Technology Corp., Ltd. (China)

- CalAmp Corporation (U.S.)

- Continental AG (Germany)

- Geotab Inc. (Canada)

- HeLLA GmbH & Co. KGaA (Germany)

- Robert Bosch GmbH (Germany)

- TomTom Telematics (Amsterdam)

- Verizon Communications (U.S.)

- Xirgo Technologies (U.S.)

- ZF Friedrichshafen (Germany)

KEY INDUSTRY DEVELOPMENTS

- May 2024 - EVBox partnered with EVA Global to integrate an on-board diagnostic telematics device into its fast charging stations. The company has also implemented initiatives to improve its after-sales support, including the launch of a LiveChat option and a Virtual Assistant on its website. These initiatives, along with the incorporation of a diagnostic telematics technology into its rapid charging stations, aim to improve customer service.

- October 2023 - Opus IVS launched IVS Mobile, a cutting-edge mobile application that offers a thorough platform for original equipment (OE) and multiple brand diagnostics, along with remote programming and calibration services. This application provides adnanced diagnostic capabilities for automotive technicians, providing them real-time access to essential diagnostics and repair tools.

- May 2022 - TOPDON, a full-service provider of mobility diagnostic solutions, launched Phoenix Remote, a cutting-edge vehicle scanning device designed to offer extensive diagnostic capabilities. The Phoenix Remote supports both local and remote diagnostics, making it ideal for a variety of multifunctional and multi-environment diagnostic needs.

- February 2022 - Matco Tools launched RAPASSIST, a versatile tool created for on-board diagnostic and programming aid, which is part of its ongoing partnership with Opus IVS, formerly known as Drew Technologies. This cutting-edge RAPASSIST provides automotive repair shops with four primary advantages for diagnostic and programming assistance within a single multi-tool platform: IVS 360 Live Expert Support; RAP – Remote Assist Programming; DIY programming through a CarDAQ-J2534 pass-thru interface; and printable OE vehicle scan reports.

- June 2021 - Ford launched Ford Telematics Essentials, a new fleet management solution that enhances its connected commercial vehicle diagnostics system for fleet operators in Europe, aiming to boost the efficiency of connected commercial vehicles

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on important aspects, such as key players, device type, vehicle type, and applications depending on various regions and countries. Moreover, it offers deep insights into the market global on-board diagnostics (OBD) aftermarket trends, competitive landscape, market competition, comparative analysis, and market status, and highlights key industry developments. Additionally, it encompasses several direct and indirect factors that have contributed to the expansion of global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.57% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Application, Vehicle Type and Region |

|

Segmentation

|

By Type

|

|

By Application

|

|

|

By Vehicle Type

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the On-Board Diagnostics (OBD) Aftermarket size was valued at USD 8.23 billion in 2026 and is anticipated to USD 19.75 billion by 2034.

The market is likely to grow at a CAGR of 11.57% during the forecast period.

The top players in the industry are Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG., CalAmp Corporation, Geotab Inc., HeLLA GmbH & Co. KGaA, and others.

North America dominated the market.

Engine sub-segment in application segment is leading in the market

U.S. is a dominating country in North America region.

- 2021-2034

- 2025

- 2021-2024

- 172

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us