Operating Room Equipment Market Size, Share & Industry Analysis, By Product Type (OR Tables, Surgical Lights, Anesthesia Workstations & Ventilators, Patient Monitoring Systems, Surgical Visualization Systems, and Others), By Application (Cardiovascular, Orthopedic, Gynecology & Urology, Neurosurgery, and Others), By End-user (Hospitals, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Operating Room Equipment Market Size and Future Outlook

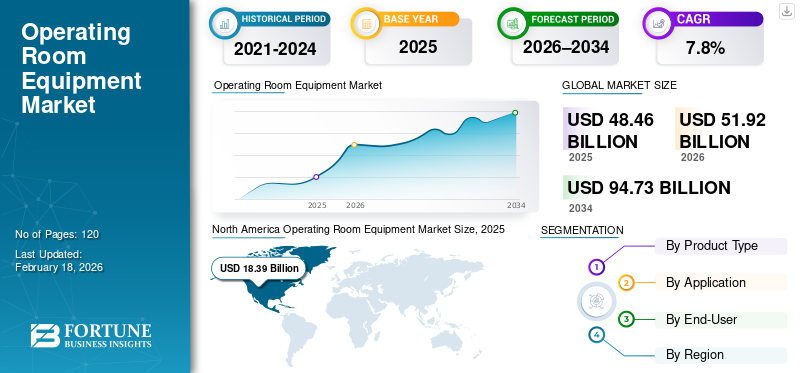

The global operating room equipment market size was valued at USD 48.46 billion in 2025. The market is projected to grow from USD 51.92 billion in 2026 to USD 94.73 billion by 2034, exhibiting a CAGR of 7.8% during the forecast period. North America dominated the operating room equipment market with a market share of 37.95% in 2025.

Operating room equipment includes the tools and systems used inside an operation theatre to help doctors perform surgeries smoothly. The equipment covers products such as surgical lights, surgical tables, anesthesia-related setup, surgical displays/visualization systems, and OR integration tools amongst others. The market growth is attributed to the rising number of surgical procedures, surging demand for advanced operating room equipment, increasing investments for cutting-edge operating room infrastructure, and focus on infection prevention. In addition, consolidation of healthcare infrastructure, especially in emerging countries, coupled with technological developments is also projected to augment market growth during the forecast period.

- For instance, in November 2024, Stryker announced the launch of its new Oculan lighting system to enhance surgical illumination and visualization.

Furthermore, many key industry players, such as Stryker, Zimmer Biomet, Medtronic, B. Braun Melsungen AG, and Getinge operating in the market, are focusing on the development of numerous innovative technologies to introduce better products with enhanced efficiency and accuracy.

Download Free sample to learn more about this report.

OPERATING ROOM EQUIPMENT MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 48.46 Billion

- 2026 Market Size: USD 51.92 Billion

- 2034 Forecast Market Size: USD 94.73 Billion

- CAGR: 7.8% from 2026–2034

- North America dominated the operating room equipment market with a 37.95% share in 2025.

- The patient monitoring systems segment is anticipated to grow at a CAGR of 7.9% during the forecast period.

- The cardiovascular segment is projected to expand at a CAGR of 9.6% during the forecast period.

North America

North America held the dominant share in 2024, valuing at USD 17.22 billion, and also maintained the leading share in 2025, with a value of USD 18.39 billion.

Europe

The Europe market is projected to record a growth rate of 7.3% over the forecast period, which is the second highest among all regions, and reach a valuation of USD 13.52 billion by 2026.

Asia Pacific

Asia Pacific is estimated to reach USD 13.41 billion in 2026 and secure the position of the third-largest region in the market.

U.S.

The U.S. operating room equipment market is estimated to reach USD 16.76 billion in 2026, accounting for approximately 32.3% of global market revenue.

Japan

Japan’s operating room equipment market is estimated at USD 2.33 billion in 2026, representing roughly 4.5% of global revenues.

Read More

OPERATING ROOM EQUIPMENT MARKET TRENDS

Rapid Growth of Surgical Visualization and Advanced Displays

The market is witnessing a substantial rise in the demand for surgical visualization and advanced displays for better surgical outcomes and clearer imaging. Moreover, hospitals are upgrading visualization platforms as surgeons want more clarity and smoother viewing for complex procedures. In addition, the healthcare facilities across the globe are also focusing on hassle-free surgery and infection prevention, which is further expected to support this market trend during the forecast period.

- For instance, in January 2026, Haaglanden Medical Center became the first medical center in the Netherlands to install and utilize gyroscopic radiosurgery

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Focus on Patient Safety and Infection Control to Accelerate Market Growth

The growing focus on patient safety and infection control is one of the prominent drivers boosting the global operating room equipment market growth. Hospitals are under pressure to reduce surgical infections and improve overall surgical outcomes. As a result, they are investing in better OR equipment such as advanced surgical lights, easy-to-clean surfaces, modern tables, and controlled airflow systems. New equipment also supports the safer handling of instruments and smoother movement of staff inside the operating room.

MARKET RESTRAINTS

High Cost and Slow Approval Processes to Deter Market Growth

A key restraint is the high cost of OR equipment and the slow approval process inside hospitals. OR upgrades often require large budgets, tendering, and multiple approvals, which can delay buying decisions. Hospitals also prefer proven systems as OR downtime is expensive and risky. Even when a new solution looks good, many facilities first run trials, compare vendors, and check service support before final purchase. This slows adoption, especially for mid-sized hospitals and smaller cities where budgets are tighter.

MARKET OPPORTUNITIES

Expansion of Smart OR and Automation to Offer Favorable Market Growth Opportunities

Recently, the market is witnessing rising demand for smart operating rooms for better workflows and surgical outcomes. This demand for smart ORs is expected to offer a favorable opportunity, driving the adoption of intelligent and automated systems. Moreover, hospitals also focus on acquiring tools that reduce manual coordination such as systems that track OR status, improve turnover time, and support better teamwork. This is why companies are partnering to bring AI and automation into OR workflows.

- For instance, in January 2026, Oath Surgical announced a strategic collaboration with NVIDIA to support the OathOS platform. It is a multimodal and next generation of value-based surgery.

MARKET CHALLENGES

Limited Technical Skills and Staff Adaptation Act as Critical Challenges for Market Growth

A key challenge for market players is getting hospital staff comfortable with new equipment. Modern operating rooms use advanced systems that require training and regular practice. Surgeons, nurses, and technicians may resist change if new tools feel complicated or slow them down initially. Smaller hospitals often lack dedicated training teams, making adoption even harder. If staff are not fully confident using new equipment, hospitals delay upgrades or use only basic features, reducing the full value of the investment. This slows down adoption and creates hesitation when hospitals consider replacing existing OR setups.

Segmentation Analysis

By Product Type

Rising Focus on Better Surgical Visualization to Boost Surgical Visualization Systems Segment Growth

Based on product type, the market is divided into OR tables, surgical lights, anesthesia workstations & ventilators, patient monitoring systems, surgical visualization systems, and others.

The surgical visualization systems segment is anticipated to account for the largest operating room equipment market share. Hospitals are currently investing in better visualization to help surgeons see clearly and work confidently, especially in complex cases. In addition, these systems also support teaching, team coordination, and consistent workflow inside the OT. That is why, large companies keep upgrading visualization platforms and expanding regional launches.

- For instance, in January 2023, Olympus Corporation announced the launch of its new VISERA ELITE III surgical visualization platform.

The patient monitoring systems segment is anticipated to rise with a CAGR of 7.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

High Volume of Orthopedic Surgical Procedures to Accelerate Orthopedic Segment Growth

Based on application, the market is segmented into cardiovascular, orthopedic, gynecology & urology, neurosurgery, and others.

In 2025, the orthopedic segment dominated the global market. Orthopedic surgeries contribute a high share as they are high-volume procedures in many hospitals. Knee replacements, trauma fixation, and other bone-related surgeries happen daily in large centers. Moreover, these surgeries also benefit heavily from strong OR infrastructure, stable surgical tables, bright surgical lighting, and reliable visualization systems help teams perform efficiently.

- For instance, according to data published by the American Joint Replacement Registry in 2022, an estimated 2.8 million hip and knee surgeries are performed each year in the U.S.

The cardiovascular segment is anticipated to rise with a CAGR of 9.6% over the forecast period.

By End-User

High Number of Surgeries to Accelerate Hospitals Segment Growth

Based on segmentation by end-user, the market is subdivided into hospitals, specialty clinics, and others.

In 2025, the hospital segment held the highest market share. Hospitals lead as they record the highest number of surgeries and handle complex cases that require well-equipped operating rooms. Large hospitals also run multiple operating theaters. Hence, they buy equipment in higher volumes and invest in integrated systems to standardize workflows across ORs. They are also more likely to adopt OR automation, OR integration, and communication tools to reduce turnaround time. Furthermore, the segment is set to hold 77.4% share in 2026.

In addition, the specialty clinics segment is projected to grow at a CAGR of 8.2% during the forecast period.

Operating Room Equipment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Operating Room Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 17.22 billion, and also maintained the leading share in 2025, with a value of USD 18.39 billion. The market in North America is expected to increase due to the higher emphasis on superior surgical outcomes and rising demand for cutting-edge systems in operating rooms.

U.S. Operating Room Equipment Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 16.76 billion in 2026, accounting for roughly 32.3% of the global sales.

Europe

The Europe market is projected to record a growth rate of 7.3% over the forecast period, which is the second highest among all regions, and reach a valuation of USD 13.52 billion by 2026. The region is estimated to witness considerable market growth due to rising investments for new product development and rising number of operating rooms.

U.K. Operating Room Equipment Market

The U.K. market is estimated at around USD 2.35 billion in 2026, representing roughly 4.5% of global market revenues.

Germany Operating Room Equipment Market

The Germany market is projected to reach approximately USD 3.25 billion in 2026, equivalent to around 6.3% of the global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 13.41 billion in 2026 and secure the position of the third-largest region in the market. Massive investments by governments as well as international and regional healthcare providers are projected to expand the number of operating rooms in the region. In addition, the growing number of surgical procedures and the rising prevalence of chronic conditions are expected to boost the market growth during the forecast period.

Japan Operating Room Equipment Market

The Japan market is estimated at around USD 2.33 billion in 2026, accounting for roughly 4.5% of global revenues.

China Operating Room Equipment Market

The China market is projected to be one of the largest worldwide, with 2026 revenues estimated to touch around USD 4.45 billion, representing roughly 8.6% of global sales.

India Operating Room Equipment Market

The India market is estimated to reach around USD 2.98 billion in 2026, accounting for roughly 5.7% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 2.69 billion in 2026. In the Middle East & Africa, the GCC is set to reach a value of USD 0.63 billion in 2026.

South Africa Operating Room Equipment Market

The South Africa market is projected to reach around USD 0.26 billion in 2026, representing roughly 0.50% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Number of Product Approvals and Rising Number of Collaborations by Leading Players to Boost Market Progress

The global operating room equipment market depicts a semi-consolidated market structure, constituting key players such as Stryker, Zimmer Biomet, Medtronic, B. Braun Melsungen AG, and Getinge. The significant global market share of these companies is on account of a range of strategic activities, including the implementation of new programs and distribution collaborations.

- For instance, in October 2025, Surgical Theater announced that it surpassed 50,000 XR utilizations, reflecting the growing adoption of advanced surgical visualization methods.

Other significant participants in the global market comprise Olympus Corporation, Smith & Nephew, Johnson & Johnson MedTech, and Baxter. These players are anticipated to prioritize partnerships to enhance their global market share during the analysis period.

LIST OF KEY OPERATING ROOM EQUIPMENT COMPANIES PROFILED

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

- Medtronic (U.S.)

- Braun Melsungen AG (Germany)

- Getinge (Sweden)

- KARL STORZ (Germany)

- Olympus Corporation (Japan)

- Smith & Nephew (U.K.)

- Johnson & Johnson MedTech (U.S.)

- Hill-Rom (an Arjo company) (U.S.)

- ConMed (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Olympus announced the launch of an AI-powered surgical planning tool through a strategic partnership to support workflow efficiency.

- March 2025: Stryker launched Sync Badge, a wearable communication device aimed at improving care-team workflow and coordination.

- January 2025: KARL STORZ announced its acquisition of the medical business of T1V, expanding its collaboration and OR-focused portfolio.

- August 2024: Getinge introduced Maquet Corin OR table and Maquet Ezea surgical light for the medtech market in India.

- December 2023: Skytron introduced a new line of mobile storage carts to support better organization in healthcare environments including OTs.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.8% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Application, End-User, and Region |

|

By Product Type |

|

|

By Application |

|

|

By End-User |

|

|

By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 48.46 billion in 2025 and is projected to reach USD 94.73 billion by 2034.

In 2025, the market value stood at USD 18.39 billion.

The market is expected to exhibit a CAGR of 7.8% during the forecast period of 2026-2034.

By product type, the surgical visualization systems segment is expected to lead the market.

Rising emphasis on better surgical outcomes and technological advancements in surgical systems are driving market expansion.

Stryker, Zimmer Biomet, Medtronic, B. Braun Melsungen AG, and Getinge are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us