Orthopedic Devices Market Size, Share & Industry Analysis, By Type (Joint Reconstruction Devices, Spinal Devices, Trauma Devices, Orthobiologics Devices, Arthroscopy Devices, and Others), By End-user (Hospitals, Orthopedic Clinic, Ambulatory Surgical Centers, and Others), and Regional Forecast, 2026-2034

Orthopedic Devices Market Size Overview

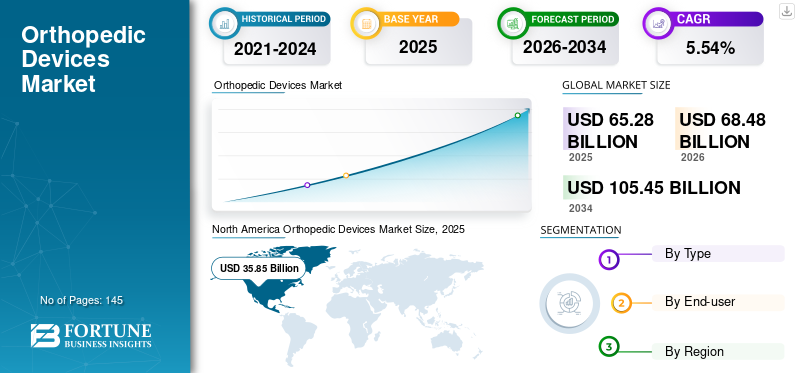

The global orthopedic devices market size was valued at USD 65.28 billion in 2025 and is projected to grow from USD 68.48 billion in 2026 to USD 105.45 billion by 2034, exhibiting a CAGR of 5.54% during the forecast period 2026-2034. North America dominated the orthopedic devices market with a market share of 54.92% in 2025.

Orthopedic devices are designed to manage musculoskeletal complications of the joints or bones. The most common orthopedic devices are rods, spacers, pins, cages, plates, and screws that act as anchors to improve and align the fractured bones. In recent years, the devices used in orthopedic surgeries have witnessed several technological advancements. Some of these include the 3D printing of materials, usage of robotics, and the integration of artificial intelligence (AI) in treatment planning, and others. For instance, according to an article published in June 2023, an innovative 3D-printed artificial knee implant was created by scientists. This product was customized as per the patient’s needs.

The orthopedic devices market growth is driven by factors such as the rising prevalence of osteoporosis and musculoskeletal diseases, technological advancements, the increasing incidence of sports and traumatic injuries, and the growing aging population. For instance, according to Definitive Healthcare, LLC., orthopedic complaints are the top reasons patients visit physicians in the U.S. The growing surgical procedures using various categories of orthopedic implants and instruments are further projected to fuel the market growth.

The COVID-19 pandemic negatively impacted the orthopedic devices market in 2020. Issues such as risk of transmission of COVID-19, lack of workforce and staff, and decline in orthopedic procedures hampered the market growth. However, patient volumes started increasing during Q3-Q4 2020 as the regulations imposed by the governments of various countries were relaxed. Therefore, the resumption of services had a positive impact on the demand for the product in 2021. The market is projected to witness steady growth prospects over the forecast period.

Download Free sample to learn more about this report.

Orthopedic Devices MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 65.28 billion

- 2026 Market Size: USD 68.48 billion

- 2034 Forecast Market Size: USD 105.45 billion

- CAGR: 5.54% from 2026–2034

- North America dominated the orthopedic devices market with a market share of 54.92% in 2025.

- The joint reconstruction devices segment is projected to dominate the market with a share of 37.51% in 2026.

- The hospitals segment is expected to lead the market, contributing 46.41% globally in 2026.

North American

The North America market was valued at USD 35.85 billion in 2025, capturing 54.92% of global revenue, and is estimated to reach USD 37.46 billion in 2026.

Europe

In 2025, Europe held 20.81% of the global market, reaching a valuation of USD 13.58 billion, and is projected to grow to USD 14.31 billion in 2026.

Asia Pacific

The market in Asia Pacific reached USD 10.74 billion in 2025, representing 16.45% of total market revenue, and is projected to reach USD 11.35 billion in 2026.

U.S.

The U.S. market size is estimated at USD 34.51 billion.

Japan

In 2026, Japan is projected at USD 2.77 billion.

Read More

Orthopedic Devices Market Trends

Rising Deployment of Computer-assisted Surgery, Robotics, and 3D Printing to Increase the Number of Orthopedic Surgeries

The increasing use of technologically advanced products in the minimally invasive surgery space, such as computer-assisted surgical devices and robotics, has led to a shift toward minimally invasive orthopedic surgeries. Minimally invasive procedures are proven to be cost-effective and precise, with additional benefits of quick recovery while reducing hospital stays. Moreover, an increasing number of orthopedic companies are upgrading their product portfolio to include robots to assist surgeons in spine, hip, and knee procedures. For instance, in May 2023, the U.S. FDA provided 510(k) clearance for the TMINI Miniature Robotic System manufactured by THINK Surgical, Inc. The system is aimed to assist orthopedic surgeons in total knee replacement surgery. Similarly, in October 2021, Medtronic Canada ULC, a subsidiary of Medtronic plc, launched the Mazor X System for robotic-guided spine surgery with an aim to expand into the robot-aided spine surgery space.

- North America witnessed a growth from USD 35.85 Billion in 2025 to USD 37.46 Billion in 2026.

Download Free sample to learn more about this report.

Orthopedic Devices Market Growth Factors

Rising Occurrence of Traumatic Injuries and Orthopedic Disorders to Fuel the Market Growth

A rapid rise in the incidence of musculoskeletal diseases and orthopedic injuries leading to limited mobility and agonizing physical pain is the primary factor expected to fuel the demand for the product during the forecast period. According to a report published by the American Academy of Orthopedic Surgeons in 2019, about 6.8 million patients with orthopedic injuries need medical attention every year in the U.S. alone. Moreover, a substantial surge in the occurrence of osteoporosis (brittle bone), which is characterized by the physical weakening of bone tissues and low bone-to-mass density ratio, is expected to propel the demand for orthopedic surgical devices in the coming years. For instance, according to data published by Bone Health and Osteoporosis Foundation, the number of American individuals having osteoporosis is around 10 million. Additionally, another 44 million individuals have low bone density, which in turn leads to higher risk of bone damage.

Rising Elderly Population to Boost Surgical Procedural Volume, Driving Market Growth

An evidential surge in the elderly population is supplementing the market growth due to the fact that elderly people are highly susceptible to hip fractures. As per a report published by the American Academy of Orthopaedic Surgeons in 2021, over 300,000 adults aged 65 and above are hospitalized every year for hip fractures. Moreover, about 30% of senior citizens fall every year, leading to a rise in the number of orthopedic injuries, which is fueling the demand for orthopedic devices.

The expansion in research and technological progressions in orthopedics, the growing number of people with obesity, and the adoption of sedentary and inactive lifestyles are anticipated to lead to a growing demand for the product in the coming years. In addition, rising expenditure in the research sector by prominent companies for the development of advantageous and minimally invasive devices for orthopedic surgeries is expected to propel the market growth during the forecast period.

RESTRAINING FACTORS

Post-Surgical Complications and Steep Price of Surgical Implantation May Hamper the Market Growth

Despite the increasing incidence of orthopedic injuries and rising geriatric population across the globe, the high costs of the procedure and postoperative complications are limiting the market growth. According to Richard Kim Medicine, the average cost of total shoulder arthroplasty in Ohio, U.S., is USD 18,165, whereas the same procedure costs around USD 30,000 in Florida. These costs are continuously rising since the past few years.

On the other hand, several risks are associated with these procedures. A few risks and complications associated with orthopedic surgical procedures include blood effusion, neuroparalysis, infections post-surgery, dislocation, venous thrombosis, and a lack of full range of motion. These factors restrain the market growth to a certain extent.

Orthopedic Devices Market Segmentation Analysis

By Type Analysis

Joint Reconstruction Devices Segment Dominates Due to the Increasing Number of Knee and Hip Replacements

The market is segmented by type into spinal devices, joint reconstruction devices, trauma devices, orthobiologics devices, arthroscopy devices, and others.

The joint reconstruction devices segment is projected to dominate the market with a share of 37.51% in 2026. An increasing number of procedures, such as shoulder and extremities reconstructions, knee and hip replacements, and other musculoskeletal procedures related to these joints, are contributing to the growth of the segment.

The arthroscopy devices (sports medicine/soft tissue repair) segment is projected to expand at a significantly high growth rate during the forecast period owing to the growing introduction of new products in the market and increasing sports-related soft tissue injuries.

- For instance, according to data published by the Australian Institute of Health and Welfare, in the year 2020-2021, the number of sports injury hospitalizations in the country was 66,500. Fracture and soft tissue injuries were leading the number by accounting for 53% and 17% of the total cases respectively.

To know how our report can help streamline your business, Speak to Analyst

By End-user Analysis

Hospitals Continue to be a Leading Segment owing to Adequate Reimbursement Policies Provided by Hospitals

Based on end-user, the market is divided into hospitals & ASCs, orthopedic clinics, and others.

The hospitals segment is expected to lead the market, contributing 46.41% globally in 2026. The hospitals segment accounted for the highest market share and is projected to grow at a significant CAGR over the forecast period. Orthopedic devices are primarily used in hospitals as they are implanted surgically. In addition, a large patient pool suffering from orthopedic injuries is mostly treated in hospitals. Apart from the treatment, adequate reimbursement policies provided by hospitals are also a key factor responsible for the high proportion of patients being treated in hospitals. However, the increasing adoption of minimally invasive procedures is anticipated to result in a preferential shift toward ambulatory surgery centers.

REGIONAL INSIGHTS

North America Orthopedic Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America market was valued at USD 35.85 billion in 2025, capturing 54.92% of global revenue, and is estimated to reach USD 37.46 billion in 2026. This region is characterized by an increase in the number of orthopedic surgeries and rising demand for advanced healthcare services coupled with adequate reimbursement policies for orthopedic instruments. These factors, along with high patient awareness of technologically advanced orthopedic devices and the presence of new treatment options, are responsible for the region's dominant share in the global market. In 2026, the U.S. market size is estimated at USD 34.51 billion.

Europe

In 2025, Europe held 20.81% of the global market, reaching a valuation of USD 13.58 billion, and is projected to grow to USD 14.31 billion in 2026. Europe accounts for the second-highest market share, owing to the increasing number of surgeries, rising healthcare expenditure by the population, and growing awareness toward technologically advanced orthopedic equipment in the region. In 2026, the U.K. market size is estimated at USD 1.66 billion, while Germany is projected to reach USD 3.83 billion.

Asia Pacific

The market in Asia Pacific reached USD 10.74 billion in 2025, representing 16.45% of total market revenue, and is projected to reach USD 11.35 billion in 2026. However, the Asia Pacific orthopedic devices market is projected to register a comparatively higher CAGR during the forecast period. Factors such as a huge patient population and expanding healthcare spending in the region are supplementing the market growth in Asia Pacific. Moreover, the increasing purchasing power of the masses in developing economies, such as China and India, will influence the growth of the market. In 2026, Japan is projected at USD 2.77 billion, China at USD 3.92 billion, and India at USD 1.25 billion.

Latin America and Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 2.01 billion, representing 3.08% of global demand, and is projected to grow to USD 2.1 billion in 2026.

Latin America maintained a strong presence in the global market, reaching USD 3.1 billion in 2025, accounting for 4.75% share, and is expected to reach USD 3.25 billion in 2026.

List of Key Companies in the Orthopedic Devices Market

Adoption of Portfolio Diversification and Branding Strategies to Help Companies Gain Competitive Edge

A diversified product portfolio of implantable orthopedic devices and constant innovations leading to new device introductions are the prominent factors responsible for the growth of the companies operating in the market. However, the presence of regional and domestic players with innovative orthopedic devices is making the market more competitive. This is projected to impact the global market in terms of pricing pressure. Moreover, the consolidation strategy is emerging as a winning imperative for industry giants.

Some of the key operating players in the market include Stryker, Zimmer Biomet, Smith & Nephew, and Johnson & Johnson Services Inc. These companies' dominance can be attributed to their strong product portfolio coupled with global presence through a wide distribution network.

Apart from these players, some other entities include Medtronic, NuVasive Inc., Arthrex Inc., and Integra LifeSciences, among others.

LIST OF KEY COMPANIES PROFILED:

- Stryker (U.S.)

- Johnson & Johnson Services, Inc. (U.S)

- Zimmer Biomet (U.S.)

- Smith & Nephew (U.S.)

- Medtronic (Ireland)

- NuVasive, Inc. (U.S.)

- Arthrex Inc. (U.S.)

- Globus Medical (U.S.)

- Össur Corporate (Iceland)

- Integra LifeSciences (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- July 2023 – Stryker launched a new autonomous Ortho Q Guidance system for improved speed and efficiency.

- February 2023 - OSSIO, Inc., a fast-growing orthopedic devices company, announced the launch of the new OSSIOfiber Compression Staple. The staple allows the company to provide solutions for many hindfoot and midfoot procedures, including midfoot fusions, Lapidus fusions, and procedures associated with flatfoot correction.

- January 2023 - Orthofix Medical Inc., a global spine and orthopedics company, announced the launch of Mariner Deformity Pedicle Screw System. The system is used to detect the unique clinical requirements of complex adult deformity spine cases.

- March 2022 - Pixee Medical launched a Knee+ AR computer-assisted orthopedic solution in the U.S. The new solution was developed for total knee arthroplasty and was claimed to be the first Augmented Reality (AR) guidance system.

- November 2020 - Olympus Corporation announced that it acquired FH ORTHO SAS, a France-based orthopedic company. The acquisition aims to expand Olympus Corporation orthopedics segment for minimally invasive surgery.

- July 2020 - Smith & Nephew announced the launch of the RI.HIP NAVIGATION for Total Hip Arthroplasty (THA), which was designed to help maximize accuracy and reproducibility by delivering patient-specific component alignment – a critical factor for surgeons when assessing individual THA cases.

REPORT COVERAGE

The research report covers a detailed analysis and overview. It focuses on key aspects such as competitive landscape, type, end-user, and region. Besides this, it offers insights into the market trends, market drivers, market dynamics, and other vital insights. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.54% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By End-user

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global orthopedic devices market stood at USD 65.28 billion in 2025 and is projected to reach USD 105.45 billion by 2034.

The market is expected to exhibit a CAGR of 5.54% during the forecast period (2026-2034).

Based on type, the joint reconstruction devices segment is set to lead the market during the forecast period.

The rising prevalence of osteoporosis and musculoskeletal diseases, growing technological innovations, increasing incidence of sports and traumatic injuries, and growing geriatric population globally are the key factors driving the market growth.

Stryker, Johnson & Johnson Services, Inc., and Zimmer Biomet are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 145

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us