Operating Room Management Market Size, Share & Industry Analysis, By Component (Software and Services), By Deployment (On-Premise, Cloud-based, and Hybrid), By Workflow (Pre-operative, Intra-operative, and Post-operative), By Type (Anesthesia Information Management, Data Management & Communication, Operating Room Scheduling Management, Operating Room Supply Management, Performance Management, and Others), By End User (Hospitals & ASCs, Specialty Surgical Centers, and Others), and Regional Forecast, 2026-2034

Operating Room Management Market Size Future Outlook

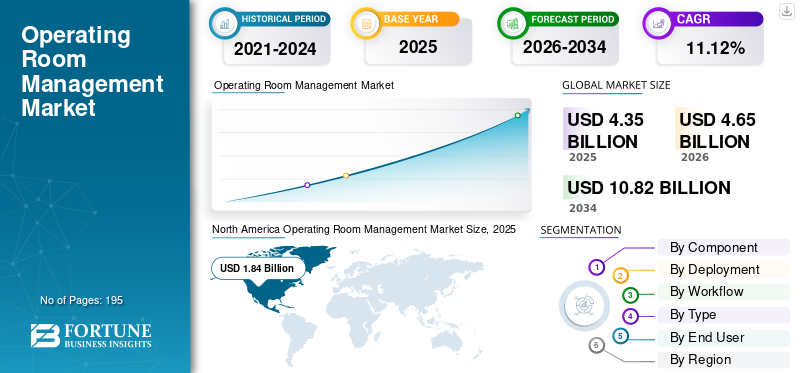

The global operating room management market size was valued at USD 4.35 billion in 2025. The market is projected to grow from USD 4.65 billion in 2026 to USD 10.82 billion by 2034, exhibiting a CAGR of 11.12% during the forecast period. North America dominated the global operating room management market with a market share of 42.3% in 2025.

Operating Room (OR) management refers to the planning, coordination, and day-to-day control needed to run surgical operating rooms efficiently, safely, and on schedule. This market is witnessing strong growth owing to more predictable schedules, fewer cancellations/delays, better patient outcomes, and higher OR utilization, along with other factors.

The market comprises various key industry players, such as Oracle, Epic Systems Corporation, and Surgical Information Systems. These companies are focusing on innovative product offerings to maintain their market presence.

Download Free sample to learn more about this report.

Operating Room Management Market KEY TAKEAWAYS

- 2025 Market Size: USD 4.35 Billion

- 2026 Market Size: USD 4.65 Billion

- 2034 Forecast Market Size: USD 10.82 Billion

- CAGR: 11.12% from 2026–2034

- North America dominated the global operating room management market with a 42.3% share in 2025.

- The on-premise segment is projected to account for 57.3% of the market in 2026.

- The intra-operative segment is projected to account for 45.8% of the market in 2026.

North America

The region led the market in 2025, driven by advanced operating room technologies and rising surgical volumes.

Europe

Europe is expected to grow due to healthcare digitization, hospital infrastructure investments, and demand for workflow management solutions.

Asia Pacific

Asia Pacific is expected to grow strongly, driven by healthcare infrastructure expansion, rising surgical procedures.

U.S.

Demand for workflow optimization, operating room efficiency, and advanced surgical management platforms is driving market growth.

Japan

Healthcare digitalization, rising surgical volumes, and efforts to improve operating room efficiency are supporting market growth.

Read More

OPERATING ROOM MANAGEMENT MARKET TRENDS

Shift Toward Cloud and Hybrid Deployment is a Prominent Trend Observed in the Market

The shift toward cloud and hybrid deployment is a prominent market trend in the OR management market. This trend can be attributed to increasing demand from hospitals for faster rollouts, easier multi-site scaling, and remote-access analytics without fully replacing mission-critical on-premise perioperative systems. Owing to this, many providers are adopting a hybrid model, retaining core perioperative/EHR workflows on-premise while moving optimization, coordination, and analytics layers to the cloud to improve agility and operational resilience. This approach also supports continuous updates, easier integration via APIs, and quicker onboarding of new facilities or surgery centers. At the same time, cloud deployments help operational leaders access real-time dashboards from anywhere and standardize workflows across networks, critical when staffing and OR capacity are tight, thereby supporting the overall global operating room management market growth.

- For instance, in June 2025, LeanTaaS introduced iQueue for Surgical Clinics, positioning it as an AI-powered, cloud-based end-to-end surgical coordination platform integrated with iQueue for Operating Rooms.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Need to Improve Operating Room Efficiency KPIs is Propelling Market Growth

The increasing need to improve operating room efficiency KPIs, especially first-case on-time starts, room turnover time, block utilization, and instrument turnaround, is a key driver of the global operating room management market growth. Even modest performance improvement can results into more surgical capacity, fewer cancellations, and better margin protection. As a result, hospitals are increasingly treating the OR as a controlled production system, prompting investment in OR management tools that standardize governance, reduce day-of delays, and give teams real-time visibility into bottlenecks. Thus, all these factors are driving the demand for operating room management solutions.

- For instance, in May 2025, Qventus reported measurable KPI-linked outcomes from its surgical growth/OR utilization solution.

MARKET RESTRAINTS

High Upfront Implementation Costs to Hamper Market Growth

High upfront implementation costs are a major market restraint on the growth of the operating room management market. Hospitals often require investment in workflow redesign, interface development, data migration, training, and go-live support, all of which add substantial investment costs. These costs are especially burdensome for multi-site health systems, where standardizing perioperative processes across facilities increases consulting and change-management intensity. Capital constraints can delay procurement decisions, push providers toward phased deployments, or limit adoption to only the highest-ROI modules. Additionally, high upfront costs also raise the risk of longer payback periods if surgical volumes fluctuate or staffing shortages prevent full utilization gains.

- For instance, according to an article published in September 2024, Northwell Health planned an Epic EHR switch expected to cost about USD 1.2 billion, highlighting the high upfront costs.

MARKET OPPORTUNITIES

Rising Adoption of AI/analytics for Capacity and Block-Time Optimization to Offer Market Growth Opportunities

Rising adoption of AI and advanced analytics for OR capacity, case-duration prediction, and block-time optimization represents a major market opportunity. Hospitals and ASCs are under pressure to create capacity without adding ORs or staff, through data-driven optimization. AI models can forecast case durations, late starts, turnover delays, and underutilized blocks, enabling perioperative leaders to proactively reallocate time, smooth schedules, and reduce cancellations. This evolution expands the value proposition of QR management solutions from basic scheduling to prescriptive recommendations, which increases willingness to pay and drives upsell of optimization modules. It also opens opportunities for vendors to introduce AI teammates/automation that coordinate tasks across pre-op readiness, intra-day OR adjustments, and post-op flow.

- For instance, in May 2025, Qventus launched new AI teammates and reported ROI outcomes for its Surgical Growth Solution, alongside multiple client wins and platform expansions.

MARKET CHALLENGES

Data Security and Patient Privacy Concerns Pose a Critical Challenge to Market Growth

Data security and patient privacy concerns remain a significant challenge in this operating room management market, as these systems handle sensitive patient and procedural data. As hospitals move toward cloud/hybrid models and multi-site data flows, they must meet strict privacy and security requirements, which can slow procurement, lengthen vendor due diligence, and increase total cost. In addition, there is also a risk of ransomware on healthcare IT systems affecting operating systems and patient safety risks, including cancellations.

- For instance, according to an article published in January 2025, Change Healthcare witnessed a cyberattack that impacted about 190 million people and caused widespread disruption.

Segmentation Analysis

By Component

Rising Number of Deployments to Propel Segmental Growth

Based on component, the market is divided into software and services.

The software segment is expected to hold the largest global operating room management market share. The dominance can be attributed to the increasing number of deployments, rising licensing and subscription revenues, and technological advancements in the products. Moreover, new product launches by operating players are also aimed at propelling the segmental revenue generation.

- For instance, in January 2025, LiveData introduced PeriOp Manager software across 88 Veterans Affairs hospitals across the U.S.

The services segment is anticipated to rise with a CAGR of 9.39% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

High Demand from Hospitals & ASCs Boosted On-premise Segment Growth

On the basis of deployment, the market is divided into on-premise, cloud-based, and hybrid.

The on-premise segment dominated the global market in 2025. Key factors supporting the dominance of the segment include high demand from hospitals & ASCs, advantages offered by these solutions such as very high uptime, low latency, and deterministic performance, and others. The segment is set to hold 57.3% share in 2026.

The cloud-based segment is anticipated to rise with a CAGR of 13.67% over the forecast period.

By Workflow

Intra-Operative Segment Dominated due to its Ability to Support Patient Safety

On the basis of workflow, the market is divided into pre-operative, intra-operative, and post-operative.

The intra-operative segment captured the highest share of the global market in 2025. The dominance of this segment is mainly driven by the fact that intra-op is the most time-critical and compliance-intensive phase, requiring real-time coordination between surgeons, anesthesia, and nursing teams. Hospitals prioritize intra-op solutions as they directly support patient safety protocols, anesthesia and nursing documentation, device data capture, medication/implant usage capture, and immediate visibility into case progress, all of which are essential for clinical governance and billing completeness. In addition, intra-op systems are deeply embedded into core perioperative platforms and interoperable device ecosystems, creating high switching costs and strong recurring software demand. Furthermore, the segment is set to hold 45.8% share in 2026.

- For instance, in October 2025, Provation announced a new release of Provation iPro AIMS with streamlined workflows and intelligent automation.

The pre-operative segment is anticipated to rise with a CAGR of 12.21% over the forecast period.

By Type

Increasing Focus on Measurable ROI to Propel Performance Management Segment Growth

Based on type, the market is divided into anesthesia information management, data management & communication, operating room scheduling management, operating room supply management, performance management, and others.

The performance management segment is expected to account for the largest global operating room management market share. The dominance is driven by increasing focus of hospitals on measurable ROI, improvement in utilization, on-time starts, turnover time, cancellations, and staffing productivity. Furthermore, the segment is set to hold 27.2% share in 2026.

- For instance, LeanTaaS’s iQueue for Operating Rooms is one of the leading solutions for performance management.

The operating room scheduling management segment is anticipated to rise with a CAGR of 12.58% over the forecast period.

By End User

Hospitals & ASCs Segment Dominated due to Higher Surgical Procedures Volumes

Based on end user, the market is segmented into hospitals & ASCs, specialty surgical centers, and others.

The hospitals & ASCs segment captured the dominating position in the global market. These settings have the highest number of operating rooms, surgical procedure volumes, and perioperative complexity, which results in higher demand for operating room management solutions by them. Additionally, their larger scale also results in enterprise-wide deployments across multiple rooms and sites, increasing adoption rates and contract sizes compared to others. Furthermore, the segment is set to hold 83.5% share in 2026.

The specialty surgical centers segment is projected to grow at a CAGR of 14.97% during the study period.

Operating Room Management Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Operating Room Management Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America captured the dominating position in 2024, with a revenue generation of USD 1.73 billion, and also maintained its dominance in 2025, with USD 1.84 billion. The regional dominance is supported by the region’s advanced healthcare infrastructure and high adoption of digital health solutions in the region. In particular, the U.S. benefits from well-equipped hospitals and developed infrastructure for integration of these solutions, which supports the country’s market growth.

U.S Operating Room Management Market

The U.S. market captured the highest share of the North American market and is expected to reach approximately around USD 1.81 billion in 2026, representing around 39.0% of the global market.

Europe

Europe is projected to witness a CAGR of 10.77% in the coming years. The region is anticipated to become the second-highest among all regions. The region would reach a valuation of USD 1.24 billion by 2026. The market growth is driven by increasing hospital modernization initiatives and a rising number of government healthcare investments.

U.K Operating Room Management Market

The U.K. operating room management market in 2026 is estimated at around USD 0.28 billion, representing roughly 6.0% of global revenues.

Germany Operating Room Management Market

Germany’s operating room management market is projected to reach approximately USD 0.25 billion in 2026, equivalent to around 5.5% of global sales.

Asia Pacific

The Asia Pacific region is projected to be valued at USD 1.09 billion in 2026 and secure the position of the third-largest region in the global operating room management industry. Expanding hospital networks and increasing healthcare expenditure have majorly driven market growth.

Japan Operating Room Management Market

The Japan operating room management market in 2026 is estimated at around USD 0.33 billion, accounting for roughly 7.0% of global revenues.

China Operating Room Management Market

China’s operating room management market is projected to reach revenues of around USD 0.20 billion in 2026, representing roughly 4.3% of global sales.

India Operating Room Management Market

The India operating room management market in 2026 is estimated at around USD 0.19 billion, accounting for roughly 4.2% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions would witness a slower growth rate in this market. The Latin America market is set to reach a valuation of USD 0.21 billion in 2026. Increasing healthcare IT investments in the region, especially in Gulf countries, coupled with rising initiatives for digital health infrastructure, is driving market growth.

Saudi Arabia Operating Room Management Market

The operating room management market in Saudi Arabia is projected to reach around USD 0.05 billion in 2026, representing roughly 1.5% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Strategic Initiatives by Leading Companies to Strengthen Their Market Position

The global market for operating room management is semi-consolidated in structure. Leading companies such as Oracle, Epic Systems Corporation, and Surgical Information Systems account for the dominating shares in the global market. These players are adopting various strategic initiatives such as new product launches, partnerships & collaborations, and others to maintain their market positions.

Other key players in the operating room management market include LeanTaas, Getinge AB, and others. During the forecast period, these companies are focusing on offering innovative solutions and collaborations with end users to gain market share.

LIST OF KEY OPERATING ROOM MANAGEMENT COMPANIES PROFILED

- Epic Systems Corporation (U.S.)

- Oracle (U.S.)

- Surgical Information Systems (U.S.)

- Harris Computer Corporation (Picis Clinical Solutions, Inc.) (U.S.)

- LeanTaaS (U.S.)

- Getinge AB (Sweden)

- Medline Industries, LP. (U.S.)

- Censis (U.S.)

- Qventus (U.S.)

- NEXUS AG. (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Provation Software, Inc. launched an updated Provation iPro AIMS focused on modernizing anesthesia documentation with streamlined workflows and automation.

- August 2025: Epic Systems Corporation announced upcoming OR-focused enhancements, including operating room direct scheduling and block management insights

- December 2024: KARL STORZ United States introduced Pathway.AI, a new tool powered by the Artisight Smart Hospital Platform in the U.S.

- October 2024: Oracle Health announced significant updates to Oracle Health Data Intelligence, emphasizing cloud/AI-enabled analytics across healthcare networks.

- September 2024: Provation and MEDITECH joined the MEDITECH Alliance Program to improve interoperability and streamline anesthesia documentation.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 11.12% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Component

By Deployment

By Workflow

By Type

By End User

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.35 billion in 2025 and is projected to reach USD 10.82 billion by 2034.

In 2025, the market value stood at USD 1.84 billion.

The market is expected to exhibit a CAGR of 11.12% during the forecast period (2026-2034).

By component, the software segment is expected to lead the market.

The shift toward cloud and hybrid deployment is the key factor driving the market.

Oracle, Surgical Information Systems, and Epic Systems Corporation are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 195

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us