Oral Biologics Drugs Market Size, Share & Industry Analysis, By Drug Class (GLP-1 Receptor Agonists, Dual Incretin Agonists, Somatostatin Analogs, Insulins, Growth Hormone & Analogs, Parathyroid Hormone Analogs, & Others), By Disease Indication (Type 2 Diabetes, Obesity / Weight Management, Acromegaly / Pituitary Disorders, Osteoporosis / Bone Metabolism Disorders, & Others), By Product Type (Tablets, Capsules, Oral Solution/Syrup, Oral Powder/Granules, Orodispersible Film/Tablet, & Others), By Age Group (Pediatric & Adults), By Distribution Channel, and Regional Forecast, 2026-2034

Oral Biologics Drugs Market Size and Future Outlook

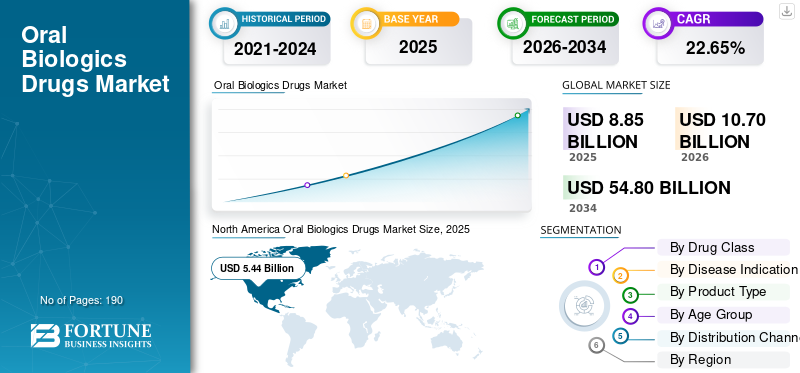

The global oral biologics drugs market size was valued at USD 8.85 billion in 2025. The market is projected to grow from USD 10.70 billion in 2026 to USD 54.80 billion by 2034, exhibiting a CAGR of 22.65% during the forecast period. North America dominated the oral biologics drugs market with a market share of 61.47% in 2025.

The market focuses on developing and commercializing therapies that can be taken orally. The global market is anticipated to grow significantly in the coming years as oral dosing can reduce the routine burden of biologic therapy and support better long-term adherence in chronic diseases. The oral administration also widens access by enabling treatment outside hospital settings. Additionally, growth is shaped by driving innovation in formulations and device-enabled delivery platforms. As more oral biologics drugs showcase clinically significant outcomes and more companies partner to de-risk delivery, the market is moving from early feasibility to broader pipeline and commercialization activity.

Furthermore, innovative techniques and oral biologics drugs technologies that deliver more sensitive results drive the global market growth.

- For instance, in August 2025, BioMed X collaborated with Novo Nordisk, a leading global healthcare company in Denmark. The partnership addressed the efficient oral delivery of therapeutic peptides.

Furthermore, leading players in the industry, such as Novo Nordisk A/S, Chiesi Farmaceutici S.p.A., Eli Lilly and Company, and Rani Therapeutics Holdings, Inc., are directing their resources toward research and development activities, expanding their offerings, and strengthening their market positions.

Download Free sample to learn more about this report.

ORAL BIOLOGICS DRUGS MARKET TRENDS

Strategic Collaborations among Pharmaceutical Companies to Provide Effective Biologics Drugs

The global market trend gaining traction is the increase in strategic partnerships among pharmaceutical companies to develop oral delivery platforms. There are various technical risks associated with the manufacturing of oral biologics drugs. Further, these pharmaceutical companies are focusing more on reducing timelines by optimizing operations. When a pharmaceutical company pairs a high-value biologic with a proven oral-delivery platform, it can move faster than building a delivery system, while also protecting pipeline economics by sharing development costs. This dynamic is driving greater collaboration with platform developers to scale and validate across multiple assets, thereby expanding patient uptake and improving long-term adherence.

- For instance, in October 2025, Chugai Pharmaceutical Co., Ltd. collaborated with Rani Therapeutics to develop and commercialize an oral product combining RaniPill with the company's rare disease antibody. Such partnerships to de-risk the delivery of oral biologics drugs are expected to boost market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Surging Clinical and Regulatory Validation of Oral Biologic-Class Therapies to Fuel Market Growth

The rising clinical and regulatory drug validation is one of the key drivers propelling oral biologics drugs market growth. The proven effectiveness of these drugs provides healthcare providers the confidence to employ them at scale. As more drugs demonstrate outcomes beyond symptom control, such as hard endpoint benefits, companies can justify higher development spend and faster commercialization plans. They also reduce injection burden and can improve persistence in chronic diseases, which further lifts demand. These factors, collectively, accelerate partnering for oral-delivery technologies, expand late-stage pipelines, and increase investment in manufacturing/formulation capabilities suited for oral peptides and proteins. As adoption rises, the oral format encourages the growth of oral biologics drugs programs.

Underscoring these advantages, vendors are prioritizing new product launches and their subsequent approvals from the relevant regulatory bodies, accelerating market growth.

- For instance, in October 2025, Novo Nordisk announced the FDA approval of Rybelsus (oral semaglutide) for cardiovascular risk reduction in adults with type 2 diabetes at high risk, strengthening the clinical value proposition for oral biologics drugs and supporting wider uptake. Such developments are expected to drive market growth.

MARKET RESTRAINTS

Low and Variable Oral Bioavailability for Biologics May Hamper Market Growth

A major restraint for the global market is the low and variable oral bioavailability of peptides and proteins in oral format. Since the gastrointestinal tract is designed to break down large molecules and block their absorption, only a small, inconsistent fraction of the dose reaches the bloodstream, significantly impacting bioavailability. Companies often need higher doses, complex formulations, and tight dosing/food instructions to achieve reliable efficacy. This increases development time and cost, raises the risk of variable real-world outcomes, and makes regulators and payers more cautious about broad adoption. As a result, fewer candidates progress smoothly through late-stage trials and commercialization is concentrated in a limited set of molecules where exposure can be controlled.

- For instance, in March 2025, Pharmaceutics (MDPI) published a review titled 'Barriers and Strategies for Oral Peptide and Protein Therapeutics Delivery: Update on Clinical Advances'. The review highlighted that the oral delivery of peptide/protein therapeutics is significantly hindered by enzymatic degradation, instability, and poor GI permeability, which results in low bioavailability, directly reinforcing why this factor restrains market expansion.

MARKET OPPORTUNITIES

Development of Combination Therapies in a Single Pill Offers Lucrative Market Growth Opportunities

A strong growth opportunity observed in the global market is the development of combination therapies in a single pill. Many chronic diseases are multifactorial and often require multiple mechanisms of action to achieve better outcomes. When two biologic-class agents can be co-formulated into a single oral dose, it can simplify treatment, improve patient adherence, and reduce discontinuation rates when patients juggle multiple medicines. This creates a clear advantage for the company, with simpler regimens that can drive stronger clinical differentiation and broader prescribing, ultimately improving the commercial case for investing in oral biologics drugs platforms that can reliably deliver combination payloads.

- For instance, in May 2022, Oramed Pharmaceuticals Inc. received a patent grant from the U.S. FDA for a combination therapy of oral pharmaceutical compositions comprising insulin and GLP-1 for treating diabetes. Such developments support the direction toward single-pill combination oral biologic strategies and offer market growth opportunities.

MARKET CHALLENGES

Dose-Size Limitations for Large-Molecule Therapies to Pose a Challenge to Market Growth

A key challenge to the growth of the market is the dose-size limitation for large-molecule therapies. Most biologics require relatively high and reliable systemic exposure, but the oral route can deliver only a limited payload in a practical tablet/capsule size. When absorption is inefficient, companies often need to increase doses to achieve therapeutic levels, which increases the size and complexity of the dosage form and may still not eliminate variability. These limitations make it difficult to translate many higher-dose compounds into oral products, slow clinical progress, and limit the development of molecules.

- For instance, in February 2025, a Frontiers in Drug Delivery review on grand challenges in oral drug delivery highlighted that even with ingestible-device approaches intended to enable oral biologic delivery beyond peptides, key hurdles remain around reproducible payload delivery, safety, and cost. This reinforces as to why scaling oral delivery to larger biologic doses is still a major challenge.

Segmentation Analysis

By Drug Class

New Product Launches to Impel the Dominance of the GLP-1 Receptor Agonists Segment

Based on drug class, the market is categorized into GLP-1 receptor agonists, dual incretin agonists, somatostatin analogs, insulins, growth hormone & analogs, parathyroid hormone analogs, GnRH analogs/antagonists, calcitonin analogs, immunomodulatory peptides, and others.

Among these, the GLP-1 receptor agonists segment accounted for the largest oral biologics drugs market share in 2025. GLP-1 receptor agonists address very large, high-demand chronic indications where patients and physicians actively seek alternatives to injections. When a GLP-1 can be delivered orally with proven outcomes, it lowers the barrier to initiation. These factors support better persistence and expand the treated population. Furthermore, these factors drive higher prescription volumes, larger commercial budgets, and faster payer engagement than in smaller oral biologic classes. As a result, major pharmaceutical companies are investing in R&D, partnering, new product launches, and lifecycle investments in oral GLP-1 programs, reinforcing their revenue leadership.

- For instance, in March 2025, Novo Nordisk announced that Rybelsus (oral semaglutide 14 mg) showed superior reduction in cardiovascular events in the SOUL trial. The proven effectiveness of oral biologics drugs is expected to drive the segment's growth.

The dual incretin agonists segment is expected to grow at a CAGR of 31.72% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Increasing Patient Pool for Type 2 Diabetes to Propel Segmental Growth

Based on disease indication, the market is segmented into type 2 diabetes, obesity/weight management, acromegaly/pituitary disorders, osteoporosis/bone metabolism disorders, reproductive/endocrine disorders, gastrointestinal disorders, autoimmune/inflammatory disorders, and others.

In 2025, the type 2 diabetes segment accounted for the largest share of the market by disease indication. The high share is attributed to the segment's high prevalence, long treatment duration, and clear clinical pathways, in which oral therapies are already the norm. When biologic-class efficacy can be delivered in a pill, it fits routine diabetes management and can be rapidly scaled through primary care and standard prescribing workflows. This makes adoption easier and drives higher patient uptake. Such factors lead to more attraction toward pipeline focus and commercial prioritization. The result is a stronger, more consistent demand for oral biologics drugs in type 2 diabetes. They are expanding their pipelines to offer better patient care and innovative solutions.

- For instance, in September 2025, Novo Nordisk announced an EU-label update/approval pathway milestone for Rybelsus (oral semaglutide), reflecting cardiovascular benefits from the SOUL trial, reinforcing its role in type 2 diabetes management. Such development supports the segment's growth.

The obesity/weight management segment is projected to grow at a CAGR of 31.21% during the forecast period.

By Product Type

Scalability and Cost-Effectiveness of Tablets to Fuel the Segmental Growth

Based on product type, the market is segmented into tablets, capsules, oral solutions/syrups, oral powders/granules (sachets), orodispersible films/tablets, and others.

Among these, the tablets segment dominated the market in 2025, as they are the most scalable and cost-efficient oral dosage form for chronic therapy. When companies can stabilize an oral biologic in a tablet with acceptable exposure, they achieve simpler manufacturing, easier distribution, and better patient convenience compared with more complex oral formats. This reduces friction, improving adoption and repeat refills. Over time, that operational advantage translates into higher volumes and faster commercialization for tablet-based drugs. Additionally, new product launches by key players to expand the tablet segment support the segment's dominance.

- For instance, in September 2025, Entera Bio reported positive updates from its EB613 tablets (oral PTH [1-34]) program, highlighting the continued development of oral biologic tablets.

In addition, the oral powder/granules (sachets) segment is projected to grow at a CAGR of 24.59% during the study period.

By Age Group

Effectiveness of Oral Biologics Drugs in Adult Heavy Disease Indications to Propel Adult Segment Growth

Based on age group, the market is segmented into pediatric and adult.

In 2025, the adult segment dominated the market based on age group. The largest opportunities lie in adult-heavy diseases such as type 2 diabetes, obesity/weight management, and post-menopausal bone disorders. This results in the segment's dominance. As these conditions rise with age, adult patients represent the larger addressable pool and the long duration of therapy. These factors have led key companies to prioritize adult trials, adult labeling, and adult commercialization first. Underscoring these advantages, many key companies are also focusing on research and development and pipeline expansions of many oral biologics drugs specifically for the adult segment.

- For instance, in October 2025, Entera Bio shared clinical data for EB613 in early postmenopausal women, reflecting the adult-focused development of oral biologics drugs.

In addition, the pediatric segment is projected to grow at a CAGR of 24.39% during the study period.

By Distribution Channel

Vast Distribution Network of Drug Stores and Retail Pharmacies to Push Segment Growth

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

The drug stores & retail pharmacies dominate the market by distribution channel, as these settings are the epicenter for providing routine drugs and are built for high refill frequency and broad geographic access. When therapies move from clinic-administered injections to oral regimens, dispensing naturally shifts toward community pharmacies that can handle repeat prescriptions at scale. This improves convenience and continuity of supply, supporting adherence and driving higher unit volumes. As a result, manufacturers increasingly align access strategies with pharmacy-based distribution models.

- For instance, in October 2025, Chiesi selected PANTHERx Rare to distribute MYCAPSSA, showing continued investment in pharmacy-led distribution to improve patient access.

The online pharmacies segment is projected to grow at a CAGR of 26.18% over the study period.

Oral Biologics Drugs Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Oral Biologics Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at a value of USD 4.56 billion and maintained its leading position in 2025 with a value of USD 5.44 billion. The market in North America is expected to grow significantly over the forecast period, driven by large populations with type 2 diabetes and obesity, as well as strong pipeline development. Further, increasing research and development and rising investment in the region are anticipated to support the market's growth.

U.S. Oral Biologics Drugs Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market value can be estimated at around USD 5.93 billion in 2026, accounting for roughly 55.42% of the global market.

Europe

The Europe market is projected to grow at a rate of 21.24% over the forecast period, the second-highest among all regions, and reach a valuation of USD 2.17 billion by 2026. The area is expected to experience robust growth as health systems prioritize cardio-metabolic risk reduction and increasing willingness to adopt these drugs.

U.K. Oral Biologics Drugs Market

The U.K. market is estimated to touch a value of around USD 0.41 billion in 2026, representing roughly 4.53% of the global market.

Germany Oral Biologics Drugs Market

The Germany's market is projected to reach approximately USD 0.48 billion in 2026, equivalent to around 4.53% of the global market.

Asia Pacific

The Asia Pacific market is estimated to reach USD 1.76 billion in 2026 and secure the position of the third-largest region in the market. The area has a large diabetes burden and strong demand for therapies that reduce injection dependency and clinic load. Such factors are driving the product demand in the region.

Japan Oral Biologics Drugs Market

The Japanese market is estimated to reach a value of around USD 0.30 billion in 2026, accounting for approximately 2.79% of the global market.

China Oral Biologics Drugs Market

The China market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.60 billion, representing approximately 5.60% of global sales.

India Oral Biologics Drugs Market

The India market is estimated at around USD 0.23 billion in 2026, accounting for roughly 2.13% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.18 billion in 2026. The region is experiencing market growth driven by rising investments in healthcare infrastructure and specialty pharmacy networks. In the Middle East & Africa, the GCC is set to reach USD 0.03 billion in 2026.

South Africa Oral Biologics Drugs Market

The South African market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 0.07% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Pipeline Candidates by Pivotal Players to Impel Market Progress

The global oral biologics drugs market represents a semi-fragmented competitive structure, with companies such as Novo Nordisk A/S, Chiesi Farmaceutici S.p.A., Eli Lilly and Company, and Rani Therapeutics Holdings, Inc. holding significant market share. Strategic collaborations, technological advancements, expanding pipelines, and escalated investments in the sector drive these companies' market share gains.

- For instance, in February 2026, Eli Lilly and Company collaborated with Innovent Biologics, Inc. to advance novel oncology and immunology medicines and deliver new drugs for patients worldwide. Such developments aimed to drive market growth.

Other notable companies in the global market include Oramed Pharmaceuticals Inc., Chugai Pharmaceutical Co., Ltd., and OPKO Health, Inc. These industry participants are expected to prioritize strategic collaborations, technological advancements, and new product rollouts to strengthen their positions during the forecast period.

LIST OF KEY ORAL BIOLOGICS DRUGS COMPANIES PROFILED

- Novo Nordisk A/S (Denmark)

- Chiesi Farmaceutici S.p.A. (Italy)

- Eli Lilly and Company (U.S.)

- Rani Therapeutics Holdings, Inc. (U.S.)

- Oramed Pharmaceuticals Inc. (Israel)

- Entera Bio Ltd. (Israel)

- Chugai Pharmaceutical Co., Ltd. (Japan)

- OPKO Health, Inc. (U.S.)

- Ironwood Pharmaceuticals, Inc. (U.S.)

- Salix Pharmaceuticals. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Novo Nordisk partnered with Vivtex Corporation to develop next-generation oral biologic medicines for obesity, diabetes, and associated comorbidities.

- August 2025: BioMed X collaborated with Novo Nordisk in Denmark. This partnership aimed to address challenges in modern drug development, the efficient oral delivery of therapeutic peptides.

- August 2025: Piramal Pharma Solutions collaborated with New Amsterdam Pharma Company N.V. to open a dedicated oral solid dosage (OSD) form suite at Piramal's facility in Sellersville, Pennsylvania, U.S. The development aimed for increased operational efficiency to deliver its investigational drug therapy, if approved, to patients in need.

- December 2024: Lonza announced an expansion of services to support smart capsule companies in their endeavors to develop orally delivered biologics.

- September 2024: Evonik launched EUDRACAP colon-specific capsules for targeted delivery of oral drugs. EUDRACAP colon is a functional, ready-to-fill capsule on the market targeting the ileo-colonic region.

REPORT COVERAGE

The global oral biologics drugs market analysis includes a comprehensive study of market size & forecast across all market segments covered in the report. It contains details on the market dynamics and trends expected to drive the global market over the forecast period. It provides information on key aspects, including pipeline analysis, new product launches, and the regulatory landscape. Additionally, it details partnerships, mergers & acquisitions, and key industry developments. The global market research report also provides a detailed competitive landscape, including market share and profiles of major operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 22.65% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Disease Indication, Product Type, Age Group, Distribution Channel, and Region |

| By Drug Class |

|

| By Disease Indication |

|

| By Product Type |

|

| By Age Group |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 8.85 billion in 2025 and is projected to reach USD 54.80 billion by 2034.

In 2025, the market value stood at USD 5.44 billion.

The market is expected to grow at a CAGR of 22.65% over the forecast period of 2026-2034.

By drug class, the GLP-1 receptor agonists segment led the market in 2025.

The rising prevalence of chronic diseases such as diabetes is anticipated to drive the market growth.

Novo Nordisk, Chiesi Farmaceutici S.p.A., Eli Lilly and Company, Rani Therapeutics Holdings, Inc., and Oramed Pharmaceuticals Inc. are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us