Orbital Transfer Vehicle Market Size, Share & Industry Analysis, By Type (Orbital Transfer, Orbit Raising/GEO Injection OTV, In-Orbit Logistics, Servicing-Enabled OTV, and Disposal/End-of-Life OTV), By Vehicle Type (Free-Flying Space Tug, OTV Space Bus, Attachable Propulsion Module, Dispenser-Integrated OTV, and Modular/Reconfigurable OTV), By Payload (Nano (<10 kg), Micro (10–100 kg), Small (100–500 kg), Medium (500–2,000 kg), and Heavy (>2,000 kg)), By End User (Government space agencies, Commercial space agencies, and Public-private partnerships), and Regional Forecast, 2026-2034

Orbital Transfer Vehicle Market Size and Future Outlook

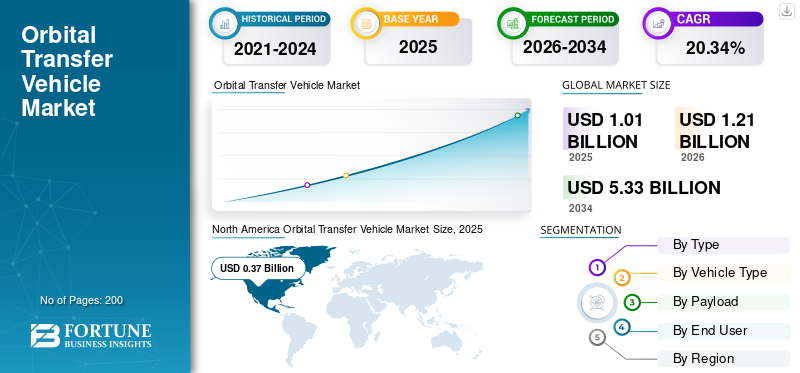

The global orbital transfer vehicle market size was valued at USD 1.01 billion in 2025. The market is projected to grow from USD 1.21 billion in 2026 to USD 5.33 billion by 2034, exhibiting a CAGR of 20.34% during the forecast period. North America dominated the orbital transfer vehicle market with a market share of 36.63% in 2025.

Orbital Transfer Vehicles (OTVs), or space tugs, are spacecraft designed to transport payloads from Low Earth orbit (LEO) to higher orbits such as GEO or other destinations, performing maneuvers such as altitude, inclination, and phase changes. They comprise propulsion systems (chemical/electric), power subsystems (solar panels, batteries), guidance/navigation, thermal controls, and docking mechanisms. Used for satellite deployment, constellation adjustments, in-orbit servicing, debris removal, and lunar/interplanetary missions. Driving factors include rising satellite mega constellations, small satellite launches, propulsion advancements, commercial space investments, and space infrastructure growth.

Key players include Impulse Space, Northrop Grumman, Rocket Lab, Firefly Aerospace, Blue Origin and among others. These major players developed high-thrust Mira OTV for rapid GEO transfers, advanced MEV for satellite life extension, and offered Photon for small satellite orbital delivery.

Download Free sample to learn more about this report.

Orbital Transfer Vehicle Market KEY TAKEAWAYS

- 2025 Market Size: USD 1.01 billion

- 2026 Market Size: USD 1.21 billion

- 2034 Forecast Market Size: USD 5.33 billion

- CAGR: 20.34% from 2026–2034

- North America dominated the orbital transfer vehicle market with a 36.63% share in 2025.

- Servicing-enabled OTV segment is anticipated to grow at the highest CAGR of 21.31% during the forecast period.

- Modular/Reconfigurable OTV segment is projected to grow at a CAGR of 22.11% during the forecast period.

Asia Pacific

Asia Pacific is projected to reach USD 0.33 billion by 2026, driven by expanding indigenous space programs and satellite launches.

North America

North America reached USD 0.37 billion in 2025, supported by NASA contracts and strong commercial space investments.

Europe

Europe is projected to reach USD 0.35 billion by 2026, driven by ESA-led in-orbit servicing initiatives.

U.S.

U.S. is projected to reach USD 0.27 billion by 2026, fueled by NASA and Space Force investments in orbital transfer technologies.

Japan

Japan is projected to reach USD 0.06 billion by 2026, supported by JAXA-led advancements in orbital transfer and lunar technologies.

Read More

ORBITAL TRANSFER VEHICLE MARKET TRENDS

AI navigation and Autonomous Operation is a Market Trend

AI navigation and autonomous operations represent a pivotal trend in the OTV market, enabling precise orbit maneuvers without constant ground oversight. NASA studies emphasize AI for real time trajectory optimization, collision avoidance, and docking in crowded LEO/GEO environments, cutting mission costs via machine learning models such as neural networks for predictive pathing. Autonomous systems integrate sensor fusion (LiDAR, star trackers) with reinforcement learning to handle uncertainties in satellite servicing and debris mitigation, as demonstrated in 2025 NASA’s Jet Propulsion Laboratory (JPL) rover tech adapted for space tugs.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Surging Demand for Satellite Mega Constellations to Drive Market Growth

Surging demand for satellite mega-constellations drives the orbital transfer vehicle market growth by necessitating efficient post launch orbital adjustments. Launch vehicles deploy these satellites into initial low Earth orbits, but precise relocation to operational slots such as different inclinations, altitudes, or phasing within dense constellations requires specialized tugs for last mile delivery. This enables global broadband coverage, Earth observation networks, and resilient communications architectures.

MARKET RESTRAINTS

Expensive Materials Leading to High Development Costs Creates Market Restraints

High development costs restrain the market due to expensive materials including high thrust composites and radiation hardened electronics needed for vacuum reliability. Extensive qualification testing thermal vacuum chambers, vibration rigs, propulsion hot fires spans years to verify zero failure performance for multimillion dollar missions. Furthermore, demonstrating reusability also demands costly docking testbeds and refurbishment protocols which adds overhead cost for development.

MARKET OPPORTUNITIES

In-Orbit Servicing Creates New Market Opportunities

In-orbit servicing creates new market opportunities by extending satellite lifespans through refueling, repairs, and relocations, reducing replacement launch costs amid aging GEO assets. NASA's studies highlight robotic docking for life extension missions, enabling satellite operators to defer decommissioning and maximize infrastructure value. This supports mega constellations via on-demand upgrades and debris mitigation, while fostering propellant depots for sustained operations. Emerging cislunar applications include habitat servicing, unlocking scalable space logistics beyond Earth orbit for commercial and government missions.

MARKET CHALLENGES

Lack of Standardized Docking Interfaces Present a Major Market Challenge

Lack of standardized docking interfaces creates a significant market challenge for OTVs, as diverse satellite designs from multiple manufacturers lack universal mechanical or robotic capture mechanisms. This heterogeneity demands custom adapters for each mission, escalating engineering costs, development timelines, and integration risks during grappling operations. Without industry-wide standards such as NASA's iROSA or ESA docking ports, interoperability fails across legacy and modern assets, hindering scalable in-orbit servicing and life-extension demos essential for commercial viability.

Segmentation Analysis

By Type

Increased Launch Frequency to Boost Orbital Transfer Segmental Growth

Based on the type, the market is segmented into orbital transfer, orbit raising/GEO injection OTV, in-orbit logistics, servicing-enabled OTV, and disposal/end-of-life OTV.

In 2025, the orbital transfer segment dominated the global market. The segmental growth is mainly as growing demand for relocating satellites from low Earth orbit drop off points to precise operational slots such as geostationary or sun-synchronous orbits due to increased launches.

The servicing-enabled OTV segment is anticipated to rise with a highest CAGR of 21.31% over the forecast period.

By Vehicle Type

Reduced Launch Costs to Boost Airborne Segment Growth

Based on vehicle type, the market is segmented into free-flying space tug, OTV space bus, attachable propulsion module, dispenser-integrated OTV, and modular/reconfigurable OTV.

In 2025, the dispenser-Integrated OTV segment dominated the global market. By allowing several payloads to be transported to their precise terminal orbits from a single, less expensive rideshare launch, these OTVs dramatically reduce the cost of access to space, which is the primary reason for the rapid expansion.

The modular/reconfigurable OTV segment is projected to grow at a high CAGR of 22.11% over the forecast period.

By Payload

Rise of Small Satellite Constellations to Boosts Small (100–500 kg) Segment Growth

Based on the payload, the market is segmented into nano (<10 kg), micro (10–100 kg), small (100–500 kg), medium (500–2,000 kg), and heavy (>2,000 kg).

The small (100–500 kg) segment is anticipated to witness a dominating orbital transfer vehicle market share over the forecast period. The segmental growth is due to small satellite constellations and exponential growth in LEO broadband and imaging networks.

The heavy (>2,000 kg) segment is projected to grow at a high CAGR of 21.05% over the forecast period.

By End User

To know how our report can help streamline your business, Speak to Analyst

Rise in On-Orbit Servicing Demand to boost Commercial Space Agencies Segment Growth

Based on end user, the market is segmented into government space agencies, commercial space agencies, and public-private partnerships.

The commercial space agencies segment dominated the market share. The need to manage space debris, prolong satellite life span, lower replacement costs and such other services is driving up demand for On-Orbit Servicing (OOS), which benefits commercial space agencies.

In addition, the public-private partnerships segment is projected to grow at a high CAGR of 21.54% during the study period.

Orbital Transfer Vehicle Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Orbital Transfer Vehicle Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 0.31 Billion, and also maintained the leading share in 2025, with USD 0.37 Billion. North America leads OTV development through NASA's 2025 studies awarding contracts to U.S. firms for multi-orbit transfer prototypes. The growth is also due to presence of key players including Blue Origin, Firefly Aerospace, and Rocket Lab which secured contracts for reusable tugs targeting GEO and cislunar missions.

U.S. Orbital Transfer Vehicle Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.27 billion in 2026, accounting for roughly 20.55% CAGR. The U.S. dominates via NASA/Space Force contracts awarded to six firms including Impulse Space and ULA for OTV studies.

Europe

Europe is projected to record a steady growth rate of 19.97% during the forecast period, which is the second highest among all regions, and reach a valuation of USD 0.35 billion by 2026. Europe progresses through ESA's in-orbit servicing demos and Ariane 6 integration. The need for in-orbit satellite servicing, the rise in commercial space logistics, and the increased frequency of small satellite launches are driving the emergence of OTVs in Europe.

U.K. Orbital Transfer Vehicle Market

The U.K. market in 2026 is estimated at around USD 0.08 billion, representing roughly 20.45% CAGR during the study period. The region’s growth accelerates post-Brexit via the U.K. Space Agency funding for autonomous tugs.

Germany Orbital Transfer Vehicle Market

Germany’s market is projected to reach approximately USD 0.07 billion in 2026. Germany thrives in OTV via DLR/OHB collaborations on electric propulsion for Spectrum tugs, fueled by ESA contracts ensuring GEO precision amid industrial manufacturing strengths.

Asia Pacific

Asia Pacific market value is estimated to reach USD 0.33 billion in 2026 and secure the position of the third-largest region in the market and fastest growing during the study period. The region surges via national rockets such as H3, SSLV enabling indigenous OTV ecosystems, propelled by constellation rivalries and sovereign technology mandates.

Japan Orbital Transfer Vehicle Market

The Japan market size in 2026 is estimated at around USD 0.06 billion, accounting for roughly 21.04% of CAGR during the forecast period. Japan progresses OTV through JAXA/Mitsubishi H3 precision, adapting ispace lunar tech for Earth orbits amid resilient commercial needs.

China Orbital Transfer Vehicle Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 0.08 billion. China's OTV growth powers through CALT's Long March adaptations for Tiangong/Beidou logistics, state-backed reusability amid U.S. sanctions.

India Orbital Transfer Vehicle Market

The India market size in 2026 is estimated at around USD 0.08 billion. India rapidly expands OTV via ISRO/Skyroot SSLV rideshares requiring tugs, fueled by private sector reforms and global constellation participation.

Rest of the World

The rest of the world region includes the Middle East & Africa and Latin America. The region’s OTV growth emerges through strategic partnerships and sovereign investments, with Brazil's Alosus advancing dispenser integrations at Alcantara for Earth observation rideshares, leveraging cost advantages and international collaborations. UAE's EDGE Group and Yahsat fund hybrid propulsion R&D for communications servicing. The Middle East & Africa and Latin America market is set to reach a valuation of USD 0.05 billion and USD 0.03 billion in 2026, respectively.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements in Propulsion Systems Fuel Market Expansion

The OTV market remains fragmented, with new space startups challenging incumbents, featuring key players such as Impulse Space (Mira OTV), Rocket Lab (Photon), Firefly Aerospace (Alpha), Blue Origin (Blue Ring), Northrop Grumman (MEV), and Intuitive Machines, among others.

Leading players are focusing on advancing electric/hybrid propulsion technologies to improve efficiency. For instance, Rocket Lab refines Photon's Hall thrusters to enable efficient LEO-GEO hops, while Impulse Space is developing high-thrust Mira bipropellant stages. Additionally, Blue Origin is integrating AI-based navigation in Blue Ring for autonomous docking, and Northrop Grumman is upgrading MEV’s robotic arms for satellite grappling and related applications.

LIST OF KEY ORBITAL TRANSFER VEHICLE COMPANIES PROFILED

- Impulse Space Inc. (U.S.)

- Rocket Lab Inc. (U.S.)

- Firefly Aerospace (U.S.)

- Blue Origin (U.S.)

- Northrop Grumman Inc. (U.S.)

- Intuitive Machines (U.S.)

- OHB SE (Germany)

- ArianeGroup (France)

- Skyroot Aerospace (India)

- D-Orbit (Italy)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Telespazio, a joint venture between Leonardo and Thales, and ispace, Inc., a multinational lunar space exploration company, have signed a Letter of Intent to begin a technical and business partnership. This was signed to support usage of OTV for the expansion of the lunar economy and take advantage of Moonlight Communication and Navigation Services' capabilities.

- August 2025: The updated version of Impulse Space's high-thrust, highly maneuverable spacecraft, Mira, for payload hosting and deployment was unveiled. Impulse Space is a leader in in-space mobility.

- August 2025: Six companies were given contracts by NASA to conduct orbital transfer vehicle studies in order to investigate potential uses of OTVs for NASA missions in the future. Firm fixed-price contracts worth USD 1.4 million are awarded to Arrow Science and Technology, Blue Origin, Firefly Aerospace, Impulse Space, Rocket Lab, and United Launch Alliance (ULA).

- July 2025: Leading space technology and infrastructure services provider named Intuitive Machines, Inc. has won a Phase Two government contract worth USD 9.8 million to develop its OTV via Critical Design Review (CDR).

- June 2023: In order to improve Firefly's on-orbit solutions and support clients' satellites and spacecraft during their lifecycle, Firefly Aerospace announced the acquisition of Spaceflight Inc. Firefly's extensive range of affordable space transportation services, which includes responsive launch and in-space mobility, on-orbit hosting and servicing, and lunar delivery operations, is further strengthened by the acquisition.

REPORT COVERAGE

The global orbital transfer vehicle industry analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the aerospace and defense springs market for piston engine over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, porter’s five forces analysis, company profiles and retrofitting program. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 20.34% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Vehicle Type, Payload, End User, and Region |

| By Type |

|

| By Vehicle Type |

|

| By Payload |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.01 billion in 2025 and is projected to reach USD 5.33 billion by 2034.

In 2025, the market value stood at USD 0.37 billion.

The market is expected to exhibit a CAGR of 20.34% during the forecast period.

By type, the orbital transfer segment is expected to dominate the market.

The surging demand for satellite mega constellations is anticipated to drive the market growth.

Impulse Space, Northrop Grumman, Rocket Lab, Firefly Aerospace, and Blue Origin are few market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us