Ozempic Market Size, Share & Industry Analysis, By Indication (Type 2 Diabetes Mellitus, T2DM with Established CVD / CV Risk Reduction Use, T2DM with CKD / Renal Risk Reduction Use, and Others), By Dose (0.25 mg / Initiation Use, 0.5 mg, 1 mg, and 2 mg), By Type (Branded and Generic), By Form (Prefilled Multi-dose Pens, Prefilled Single-dose Pens, and Others), By Age Group (Pediatrics and Adults), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, and Others), and Regional Forecast, 2026-2034

Ozempic Market Size and Future Outlook

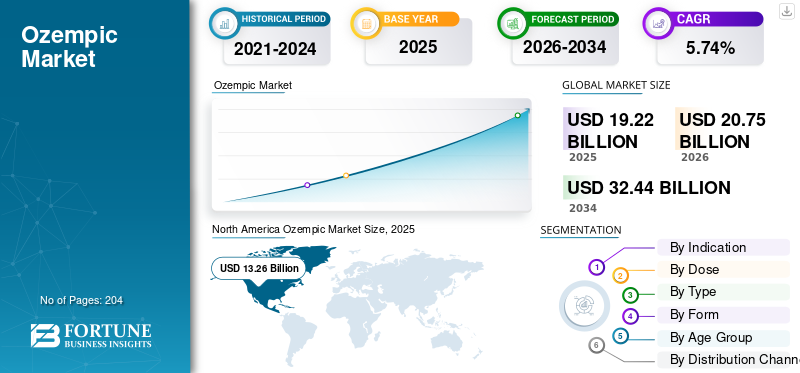

The global Ozempic market size was valued at USD 19.22 billion in 2025. The market is projected to grow from USD 20.75 billion in 2026 to USD 32.44 billion by 2034, exhibiting a CAGR of 5.74% during the forecast period. North America dominated the ozempic market with a market share of 68.99% in 2025. North America dominated the ozempic market with a market share of 68.99% in 2025.

The global Ozempic market is centered around semaglutide, a once-weekly GLP-1 receptor agonist mainly used in adults with type 2 diabetes mellitus, and its commercial demand is increasingly supported by its broader cardio-renal value beyond glucose control. The market is benefiting from the rising global burden of diabetes, obesity, and related cardiovascular and kidney complications, which is pushing physicians to prefer therapies that can address multiple risks with one product. Ozempic is also gaining stronger clinical relevance because its approved use now extends to reducing major adverse cardiovascular events in adults with type 2 diabetes and established cardiovascular disease.

Major market players include Novo Nordisk along with generic manufacturers such as Torrent Pharmaceuticals Ltd., Zydus Lifesciences, Sun Pharmaceutical Industries Limited, among others.

Download Free sample to learn more about this report.

OZEMPIC MARKET TRENDS

Growing Focus On High-Risk Comorbidity Population is a Significant Market Trend

The market is progressively shifting from utilizing Ozempic solely for blood sugar management to targeting patients with type 2 diabetes who also have cardiovascular disease or chronic kidney disease. This change is significant as these patients face an increased risk of hospital stays, quicker disease advancement, and elevated treatment expenses, prompting doctors to focus on therapies that provide greater clinical advantages. Consequently, Ozempic is being more firmly established in intricate diabetes treatment, where cardiovascular and renal risk reduction is important along with glycemic control. This trend is additionally assisting the product in achieving greater significance in long term treatment routines rather than solely as a means to lower HbA1c. Moreover, it facilitates broader implementation in specialist-managed care environments where patients frequently arrive with various metabolic and organ-related issues. For instance, in January 2025, Novo Nordisk announced that the United States FDA approved Ozempic (semaglutide) to reduce the risk of kidney disease worsening/kidney failure and cardiovascular death in adults with type 2 diabetes and CKD.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Global Burden of Obesity and Type 2 Diabetes is Propelling the Market Growth

The rising global burden of obesity and type 2 diabetes is a major driver of growth in the global market. As the number of people living with excess weight and diabetes increases, the need for long-term medicines that can improve blood sugar control and support weight reduction is also rising. This is directly pushing the demand for Ozempic because semaglutide is well-positioned amongst patients who need stronger metabolic control, especially those with multiple risk factors. The driver is becoming stronger as health systems increasingly recognize obesity as a chronic disease that also raises the risk of type 2 diabetes and related complications. The International Diabetes Federation said in 2025 that the global burden of type 2 diabetes continues to increase, while the WHO said in December 2025 that obesity affects more than 1 billion people globally. These trends are expanding the addressable patient pool for GLP-1 therapies such as Ozempic and supporting continued global market demand. All these factors cumulatively accelerarting the adoption in the market.

- For instance, according to the data published by the U.S. Centers for Disease Control and Prevention in January 2026, the estimated number of individuals with diagnosed or undiagnosed diabetes in the U.S. was 40.1 million in 2023.

MARKET RESTRAINT

High Treatment Cost and Reimbursement Limitations to Hamper Market Growth

Significant treatment expenses and reimbursement restrictions pose a considerable limitation in the global market. Ozempic is an expensive treatment, thus its elevated cost can hinder access for numerous patients, particularly in regions with restricted insurance coverage or stringent reimbursement policies. This limits access, postpones the start of therapy, and may decrease long-term adherence to treatment even when clinical need is high. The limitation puts pressure on budget-conscious healthcare systems, where insurers carefully evaluate expensive diabetes medications prior to providing extensive coverage. It also places pressure on Novo Nordisk to utilize discounts, savings initiatives, and price cuts to maintain demand. The requirement for enhanced affordability assistance illustrates that expenses continue to be a genuine obstacle to broader market growth.

- For instance, in February 2025, Novo Nordisk announced a significant reduction in the U.S. list price for Ozempic, Wegovy, and Rybelsus to expand access of these products.

MARKET OPPORTUNITIES

Shift from Glucose Control to Cardio-Renal Care to Offer Market Growth Opportunities

Shift from glucose control to broader cardio-renal positioning is a key opportunity in the global market. Earlier, Ozempic was mainly seen as a medicine for lowering blood sugar levels in type 2 diabetes, but the market opportunity is now expanding because the product is increasingly becoming relevant in patients who also have cardiovascular and kidney risks. This creates a larger commercial opportunity for Novo Nordisk, as physicians and health systems are looking for therapies that can manage diabetes while also helping reduce serious long-term complications. It also supports stronger use of Ozempic in specialist-led treatment pathways, especially for high-risk patients with chronic kidney disease or established cardiovascular disease. As a result, the product is moving into a broader cardiometabolic care model rather than being limited to glucose control alone. This shift can help improve prescribing range, patient retention, and the overall value perception of the brand across major markets. All these factors are expected to drive the market growth in the coming years.

- For instance, Novo Nordisk’s Ozempic’s label has been expanded to include reduction of the risk of kidney disease progression, kidney failure, and cardiovascular death in adults with type 2 diabetes and chronic kidney disease, highlighting the product’s growing role beyond glucose management into broader cardio-renal care.

MARKET CHALLENGES

Competition from Alternative GLP-1 and Diabetes Therapies Present a Major Obstacle to Market Expansion

Competition from alternative GLP-1 and diabetes therapies is a key market challenge in the global Ozempic market growth. The challenge is rising because it is no longer competing only with older diabetes drugs, but also with newer GLP-1 and dual-incretin therapies that are showing strong blood sugar, weight-loss, and cardiovascular results. This increases pressure on Novo Nordisk to defend prescriptions, maintain pricing power, and increase access across major markets. It also makes physician’s choice more competitive, especially when rival therapies show strong outcomes in high-risk type 2 diabetes patients. As a result, the market’s growth depends not only on its demand expansion, but also on how well it performs against competing branded options in commercial settings. This pressure is already visible in Novo Nordisk’s recent access and pricing actions, which reflects a more competitive GLP-1 environment. All of the above the factors cumulatively affect the market growth.

Segmentation Analysis

By Indication

High Prevalence And Strongest Prescription Volumes Of Type 2 Diabetes To Propel Segmental Growth of Type 2 Diabetes Mellitus

Based on the indication, the market is divided into Type 2 Diabetes Mellitus, T2DM with established CVD / CV risk reduction use, T2DM with CKD / renal risk reduction use, and others.

The type 2 diabetes mellitus segment captured the largest global Ozempic market share. This is due to its highly approved and most established use across routine clinical practice. Furthermore, it is primarily prescribed for adults with type 2 diabetes, which makes this indication the broadest treated patient base and the strongest prescription volumes. It also benefits from higher physician familiarity, longer market presence, and more consistent reimbursement support than its narrower cardio-renal sub-indications. As the global type 2 diabetes burden continues to rise, the demand for once-weekly therapies that improve glycemic control and support long-term disease management is also increasing. This is allowing Type 2 diabetes mellitus segment to contribute the highest revenue share within the indication category. The segment also remains commercially important as it acts as the core entry point for dose initiation and long-term continuation on Ozempic in major markets.

- For instance, in August 2025, Novo Nordisk introduced a new offer in the U.S. that enables self-paying, eligible type 2 diabetes patients to access authentic, FDA-approved Ozempic for USD 499 per month, reflecting the product’s continued commercial focus on the core type 2 diabetes population.

The T2DM with CKD / renal risk reduction use segment is anticipated to rise with a CAGR of 16.84% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Dose

0.5 mg Dominated the Market Due to Its Broad Use as the Standard Maintenance Dose

Based on the dose, the market is divided into 0.25 mg / initiation use, 0.5 mg, 1 mg, and 2 mg.

The 0.5 mg segment is anticipated to capture the largest global market share in 2025. as it is the first standard maintenance dose after the initial 0.25 mg initiation dose, giving it the widest active patient base. Additionally, it also offers a practical balance between blood sugar control and tolerability, which supports broader physician preference in routine type 2 diabetes management. Furthermore, the segment is set to hold 37.8% share in 2026.

- For instance, in January 2026, Novo Nordisk launched the “There’s Only One Ozempic” campaign covering Ozempic 0.5 mg, 1 mg, and 2 mg, reflecting continued commercial focus on the brand’s core approved dose strengths.

The 2 mg segment is anticipated to rise with a CAGR of 12.69% over the forecast period.

By Type

Strong Market Penetration of and Trust for Branded Products to Boost Their SegmentGrowth

In terms of type, the market is divided into branded and generic.

The branded segment dominated the global market in 2025 owing to strong trust in the original Novo Nordisk product and the absence of broad generic competition in major markets. Novo Nordisk has a broad range of branded Ozempic products. Furthermore, physicians and patients prefer branded Ozempic because it has established clinical evidence, approved dosing strengths, and wide recognition in type 2 diabetes treatment. It also benefits from stronger marketing support, better product visibility, and higher confidence around quality and supply compared with non-branded or unofficial alternatives. Furthermore, the segment is set to hold 99.1% share in 2026.

The generic segment is anticipated to rise with a CAGR of 36.96% over the forecast period.

By Form

Prefilled Multi-dose Pens Dominated the Market Oiwing to Their Better Convenience for Weekly Long-term Use

In terms of form, the market is divided into prefilled multi-dose pens, prefilled single-dose pens, and others.

The prefilled multi-dose pens segment captured the highest share of the global market in 2025 as this form is easier and more practical for routine for once-a-week treatment. Furthermore, it supports patient convenience by allowing repeated weekly dosing from the same pen, which makes regular use simpler than less flexible formats. It also helps improve treatment adherence, as patients prefer ready-to-use devices that reduce preparation steps and fit easily into long-term diabetes management. In addition, physicians are more comfortable prescribing pen-based injectable formats because they are already widely used in diabetes care. Furthermore, the segment is set to hold 91.4% share in 2026.

- For instance, in February 2025, Novo Nordisk announced that the U.S. FDA had declared the Ozempic shortage resolved and that all doses were being shipped regularly, which supports the continued leadership of the pen-based format in the market.

The prefilled single-dose pens segment is anticipated to rise with a CAGR of 16.47% over the forecast period.

By Age Group

High Prevalance And Usage Amongst Adults to Boost Segmental Dominance

On the basis of age group, the market is divided into pediatrics and adults.

The adults segment captured the highest share of the global market in 2025 as Ozempic is primarily approved and prescribed for adults with type 2 diabetes. Furthermore, type 2 diabetes is far more common in adults than in pediatric patients, so adult patients account for most routine prescriptions and long-term use. It also benefits from stronger physician familiarity, broader diagnosis rates, and more established treatment pathways in adult diabetes care. As the adult population with diabetes, obesity, and related cardiovascular or kidney risks continues to grow, demand for Ozempic is also increasing in this group. Furthermore, the segment is set to hold 98.5% share in 2026.

- For instance, in March 2025, Novo Nordisk launched its “My Ozempic Era” campaign highlighting real stories of adults living with type 2 diabetes using Ozempic.

The pediatrics segment is anticipated to rise with a CAGR of 17.81% over the forecast period.

By Distribution Channel

High Distribution Volume by Retail Pharmacies to Support Segment’s Leading Position

Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and others.

In 2025, the retail pharmacies segment held the leading position in the global market as they are the most common and convenient channel for patients to refill long-term prescription medicines. Furthermore, adults using Ozempic for type 2 diabetes usually depend on nearby retail pharmacy networks for regular weekly treatment, which gives this channel the highest prescription flow. It also benefits from broad geographic presence, easier patient access, and stronger integration with insurance claims and savings programs. Furthermore, the segment is set to hold 50.3% share in 2026.

In addition, online pharmacies are projected to witness 10.57% growth rate during the forecast period.

Ozempic Market Regional Outlook

By geography, the market is studied across Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

North America

North America Ozempic Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America established itself as the regional market leader, with a valuation of USD 12.67 billion in 2024 and growing up to USD 13.26 billion in 2025. The region is supported by high diagnosed prevalence of type 2 diabetes, strong physician awareness of GLP-1 therapies, and broad use of branded chronic medicines in outpatient care. The region also benefits from stronger commercial activity by Novo Nordisk, including direct patient access programs, savings offers, and recent U.S. list-price actions to improve affordability.

U.S. Ozempic Market

The U.S. market dominated the North American market and can be analytically approximated at around USD 13.05 billion in 2026, accounting for roughly 62.9% of global market.

Europe

Europe is anticipated to maintain a consistent growth, expanding with a CAGR of 7.51% in the next few years and estimated to attain a market size of USD 3.43 billion by 2026. A large established diabetes population, mature reimbursement systems in many countries, and strong acceptance of guideline-based diabetes treatment, are crucial elements driving market growth in the region.

U.K. Ozempic Market

The U.K. market in 2026 is estimated at around USD 0.62 billion, representing roughly 3.0% of global revenues.

Germany Ozempic Market

Germany market size is projected to reach approximately USD 0.80 billion in 2026, equivalent to around 3.8% of global sales.

Asia Pacific

The Asia Pacific region is expected to reach USD 2.37 billion by 2026, cementing its status as the third-largest regional market. The region’s main growth engine is its largest diabetes pool, which is highest in the globe, especially across the Western Pacific and South-East Asia regions. The market is also being driven by rising obesity, growing diagnosis rates, and expanding patient awareness of newer metabolic therapies.

Japan Ozempic Market

Japan market in 2026 is estimated at around USD 0.64 billion, accounting for roughly 3.1% of global revenues.

China Ozempic Market

China’s market is projected to reach revenues of around USD 0.52 billion in 2026, representing roughly 2.5% of global sales.

India Ozempic Market

The India market in 2026 is estimated at around USD 0.32 billion, accounting for roughly 1.6% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to post moderate growth rates. The Latin American market is expected to reach USD 0.75 billion by 2026, while the GCC in the Middle East & Africa is expected to achieve a valuation of USD 0.27 billion. A rising burden of diabetes and obesity, especially in urban populations, along with gradual improvement in access to modern chronic disease therapies are supporting the growth in these regions.

South Africa Ozempic Market

The South Africa market is projected to reach around USD 0.10 billion in 2026, representing roughly 0.5% of global market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Emphasize Brand Expansion and Access Strategies to Strengthen Market Position

The global Ozempic market is highly consolidated, with Novo Nordisk holding the dominant position. This is due to its ownership of the Ozempic brand and its strong global commercial presence. The company continues to benefit from large-scale product sales, broad physician familiarity, and an expanding role for Ozempic in type 2 diabetes patients with cardiovascular and kidney risk.

On the other hand, Torrent Pharmaceuticals Ltd., Zydus Lifesciences, Sun Pharmaceutical Industries Limited, are among the other prominent players in this market. These companies are focusing on the launch of generic products to gain market share.

- For instance, in February 2026, generic semaglutide injections were launches by Zydus Lifesciences in India.

LIST OF KEY OZEMPIC COMPANIES PROFILED

- Novo Nordisk (Denmark)

- Torrent Pharmaceuticals Ltd. (India)

- Zydus Lifesciences (India)

- Sun Pharmaceutical Industries Limited (India)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Novo Nordisk announced that Health Canada approved Ozempic to reduce the risk of Major Adverse Cardiovascular Events (MACE) in adults with type 2 diabetes and established cardiovascular disease and/or CKD.

- March 2026: Sun Pharmaceutical Industries Limited introduced its semaglutide injection under the brand names Noveltreat and Sematrinity in India.

- March 2026: Zydus Lifesciences launched semaglutide generic in reusable pen in India.

- November 2025: Novo Nordisk launched an introductory self-pay offer under which Ozempic was made available at a limited-time price of USD 199 per month to new self-pay patients,

- September 2025: Novo Nordisk Canada and Pocketpills announced a collaboration to provide enhanced online pharmacy and prescription support for Ozempic and Wegovy.

REPORT COVERAGE

The global market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, and the introduction of new products, and pipeline analysis. Furthermore, it outlines collaborations, mergers & acquisitions, along with the prevalence of key diseases across key countries and regions. The global market forecast report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.74% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Indication, Dose, Type, Form, Age Group, Distribution Channel, and Region |

| By Indication |

|

| By Dose |

|

| By Type |

|

| By Form |

|

| By Age Group |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 19.22 billion in 2025 and is projected to reach USD 32.44 billion by 2034.

In 2025, the market value stood at USD 13.26 billion.

The market is expected to exhibit a CAGR of 5.74% during the forecast period of 2026-2034.

By indication, the type 2 diabetes mellitus segment is expected to lead the market.

The rising global burden of obesity and type 2 diabetes are primarily driving market expansion.

Novo Nordisk and Sun Pharmaceutical Industries Limited are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 204

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us