Automotive Night Vision System Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, LCVs and HCVs), By Technology (Thermal Imaging Systems and Near-Infrared Systems), By System Type (Active Night Vision and Passive Night Vision), By Display Type (HUD, Instrument Cluster, and Central Display), By Component (Infrared Camera/Thermal Sensor, Image Processing Unit, Display Unit, Software & Algorithms, and others), By Sales Channel (OEM and Aftermarket), and Regional Forecasts, 2026-2034

Automotive Night Vision System Market Size and Future Outlook

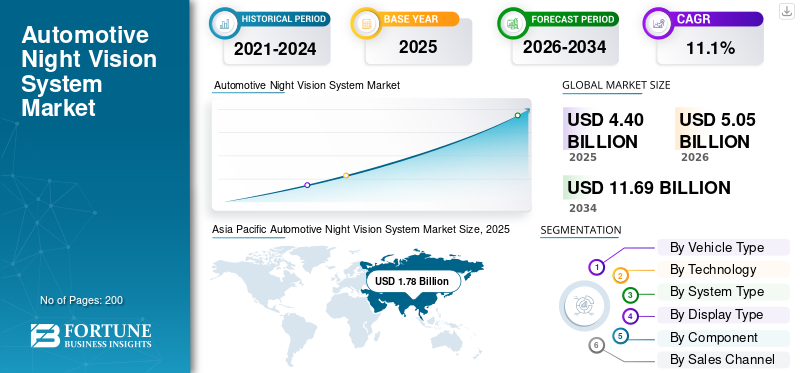

The automotive night vision system market size was valued at USD 4.40 billion in 2025. The market is projected to grow from USD 5.05 billion in 2026 to USD 11.69 billion by 2034, exhibiting a CAGR of 11.1% during the forecast period. Asia Pacific dominated the automotive night vision system market with a market share of 40.45% in 2025.

The market represents a specialized segment within vehicle safety and sensing solutions that enhances driver visibility during low-light and adverse light conditions. This market includes systems equipped with infrared sensors and advanced cameras that detect pedestrians, animals, and objects beyond the reach of conventional headlights. By using night vision technology, vehicles can provide early warnings and improve pedestrian detection, thereby strengthening overall road safety standards.

The demand for global automotive night vision solutions is rising alongside the increasing integration of Advanced Driver Assistance Systems (ADAS) in modern vehicles. Automakers are steadily integrating night vision capabilities with other safety technologies, such as automatic emergency braking and collision warning systems. The market is particularly prominent in luxury vehicles, where premium safety features are becoming standard expectations. However, as production scales and component costs gradually reduce, adoption is expanding into mid-range passenger cars and selected commercial vehicles.

Technological progress in thermal imaging and the evolution of the night vision cameras are enabling clearer imaging, faster processing, and improved object classification. These improvements are supporting higher adoption of these such solutions globally. Regional demand patterns differ, with strong Asia Pacific market growth driven by vehicle production volume, while Europe market remains supported by premium OEM concentration.

In the coming years, the market is expected to evolve through cost optimization, improved sensor performance, and deeper integration into ADAS platforms. Key players such as Valeo, Continental AG and Aptiv are focusing on product innovation, partnerships, and expanding OEM contracts to strengthen their competitive position.

Download Free sample to learn more about this report.

Automotive Night Vision System Market Key Takeaways

- 2025 Market Size: USD 4.40 Billion

- 2026 Market Size: USD 5.05 Billion

- 2034 Forecast Market Size: USD 11.69 Billion

- CAGR: 11.10% from 2026–2034

- Asia Pacific dominated the automotive night vision system market with a 40.45% share in 2025.

- The OEM sales segment is expected to register the highest CAGR of 11.20% during the forecast period.

- The Instrument cluster segment is expected to grow at a CAGR of 9.40% during the forecast period.

Asia Pacific

Asia Pacific generated USD 1.78 billion in 2025.

North America

North America is projected to reach USD 1.22 billion in 2026, growing at a CAGR of 11.20%.

Europe

Europe is projected to reach USD 1.27 billion in 2026.

U.S.

The automotive night vision system market reached USD 0.91 billion in 2025.

Japan

Growing production of technologically advanced vehicles and increasing adoption of ADAS are supporting demand for automotive night vision systems.

Read More

AUTOMOTIVE NIGHT VISION SYSTEM MARKET TRENDS

Integration of Night Vision with Multi-Display Interfaces is an Emerging Market Trend

A key trend is the integration of night vision technology with HUDs and digital clusters. Improved visualization enhances driver response time and strengthens safety technologies adoption across regions including North America and Europe.

- For instance, BMW’s Night Vision system projects alerts within the driver’s visual field, enhancing real-time awareness.

MARKET DYNAMICS

MARKET DRIVERS

Rising Focus on Road Safety and Pedestrian Protection Drives Adoption

Growing emphasis on road safety and reducing nighttime accidents is accelerating the adoption of night vision technology. Governments and safety agencies highlight the risks associated with poor light conditions, encouraging automakers to adopt enhanced safety features. As consumers demand safer vehicles, integration with ADAS drives the automotive night vision system market growth.

- For instance, the U.S. Federal Highway Administration reports higher fatality rates at night, reinforcing the need for improved visibility technologies in vehicles.

MARKET RESTRAINTS

High Cost of Thermal and Infrared Components Limits Mass Adoption

The high cost of advanced infrared sensors and thermal imaging technology remains a key restraint. These systems are typically offered in luxury vehicles, restricting broader penetration into entry-level cars. Cost sensitivity in developing markets may slow expansion of the market.

- For instance, OEM option pricing shows night vision packages are positioned as premium add-ons, reflecting elevated hardware and integration costs.

MARKET OPPORTUNITIES

Expanding Integration with ADAS Platforms Creates Growth Potential

The ongoing expansion of ADAS provides strong opportunity for integrating night vision into comprehensive safety ecosystems. As vehicles transition toward higher autonomy levels, the need for redundant sensing systems strengthens demand for night vision camera solutions.

- For instance, Teledyne FLIR states its thermal modules are deployed in over one million vehicles, indicating scalability beyond niche luxury applications.

MARKET CHALLENGES

Limited Awareness in Emerging Markets Restricts Penetration

Despite technological advancements, limited awareness in emerging economies and cost constraints in commercial vehicles pose challenges. Without regulatory mandates, growth of market may vary significantly.

- For instance, Industry associations note that advanced safety features are often optional in developing markets, slowing feature adoption rates.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

SUVs Lead Market Due to Premium Safety Feature Concentration

On the basis of vehicle type, the market is segmented into hatchback/sedan, SUVs, LCVs and HCVs.

SUVs dominates the market as they are strongly linked to luxury vehicles and advanced safety features, including night vision technology. Their higher price positioning supports stronger adoption of automotive night vision system compared to smaller passenger cars.

- For instance, in January 2024, BMW confirmed that its Night Vision system remains available on high-end X-series SUVs, which represent a significant portion of its premium vehicle lineup.

Hatchback/Sedan segment is expected to grow at a CAGR of 9.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Thermal Imaging Technology Dominates Due to its Superior Detection Capability

On the basis of technology, the market is segmented into thermal imaging systems and near-infrared systems.

Thermal imaging technology held highest automotive night vision system market share due to reliable performance in poor light conditions and enhanced pedestrian detection using infrared sensors. Its stronger detection range supports wider market penetration.

- For instance, in January 2024, Valeo and Teledyne FLIR announced expanded cooperation to deliver next-generation automotive thermal imaging systems, targeting broader OEM deployment.

Near-Infrared Systems segment is expected to grow at a CAGR of 8.5% over the forecast period.

By System Type

Passive Systems Dominate Market Owing to Integration of Thermal Sensing

On the basis of system type, the market is segmented into active night vision and passive night vision.

Passive night vision holds higher share as they operate using thermal sensing without emitting light, improving stability and ADAS compatibility. Their integration with ADAS supports segment expansion.

- For instance, in March 2024, Teledyne FLIR highlighted that its passive thermal camera modules are deployed in over one million vehicles worldwide.

Active night vision segment is expected to grow at a CAGR of 9.2% over the forecast period.

By Display Type

HUD Segment Leads Market Due to Enhanced Driver Awareness

On the basis of display type, the market is segmented into HUD, instrument cluster, and central display.

Head-Up Displays (HUD) segment dominate as they project alerts directly within the driver’s line of sight, strengthening road safety and adoption across North America and Europe. HUD integration enhances visibility without distracting drivers.

- For instance, in February 2024, Audi confirmed that its night vision assistant integrates warnings into the windshield display in select premium models.

Instrument cluster segment is expected to grow at a CAGR of 9.4% over the forecast period.

By Component

Infrared Camera Segment Holds the Largest Share As it is the Core Sensing Hardware

On the basis of component, the market is segmented into infrared camera/thermal sensor, image processing unit, display unit, software & algorithms, and others.

The infrared camera segment accounts for the largest value share as it forms the core sensing hardware. Continuous improvements in resolution and detection range support higher system pricing.

- For instance, in June 2024, Teledyne FLIR introduced upgraded automotive-qualified thermal modules designed for improved detection performance and scalable OEM integration.

Software & algorithms segment is expected to grow at a CAGR of 14.4% over the forecast period.

By Sales Channel

OEM Channel Dominates Market Through Factory-Level Integration

On the basis of sales channel, the market is segmented into OEM and aftermarket.

OEM sales dominate as factory-installed systems ensure seamless integration with safety technologies and vehicle electronics. This segment is expected to grow at a CAGR of 11.2% over the forecast period.

Aftermarket penetration remains limited due to calibration complexity and high cost.

- For instance, in April 2024, Mercedes-Benz continued offering Night View Assist Plus as a factory-installed safety feature in selected premium models.

Aftermarket segment is expected to grow at a CAGR of 9.5% over the forecast period.

Automotive Night Vision System Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and Rest of the World.

Asia Pacific

Asia Pacific Automotive Night Vision System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held a dominant share in 2025, valuing at USD 1.78 billion, and also maintained the leading share in 2024, with USD 1.52 billion. The Asia Pacific market dominates due to high vehicle production volumes and growing demand for advanced safety solutions. Integration with ADAS in premium vehicles further strengthens growth.

- For instance, according to the IEA (April 2024, Global EV Outlook 2024), China sold about 8.1 million electric cars in 2023, supporting advanced technology integration across the Asia Pacific market.

China Automotive Night Vision System Market

China’s market is projected to be one of the largest and its 2025 revenue was at USD 0.96 billion, representing roughly 21.9% of global sales.

India Automotive Night Vision System Market

India market in 2025 was at USD 0.09 billion, accounting for roughly 2.1% of global revenue.

Europe

Europe is estimated to reach USD 1.27 billion in 2026 and secure the position of the second-largest region in the market. The Europe market remains strong due to concentration of premium OEMs and early adoption of thermal imaging technology. Strict safety standards and strong luxury vehicle demand sustain regional growth.

Germany Automotive Night Vision System Market

Germany market in 2025 was at USD 0.47 billion, accounting for roughly 10.6% of global revenues.

U.K. Automotive Night Vision System Market

U.K. market in 2025 reached at USD 0.28 billion, accounting for roughly 6.4% of global revenues.

North America

North America is projected to record a growth rate of 11.2% in the coming years, and reach a valuation of USD 1.22 billion by 2026. Market growth in North America is driven by increasing awareness of road safety and demand for advanced safety features. The U.S. market benefits from strong luxury vehicle sales and rising integration of night vision technology. The U.S. shows steady expansion in premium SUV and pickup segments, supporting broader global adoption.

U.S. Automotive Night Vision System Market

Based on North America’s strong contribution, the U.S. market was at USD 0.91 billion in 2025, representing roughly 20.7% of market.

Rest of the World

Growth in rest of the world is gradual but improving as commercial vehicles and passenger car manufacturers adopt more safety technologies. Adoption remains selective due to high cost, but expanding safety awareness supports future potential.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovation and OEM-Centric Competition Defines Market Competition

The competitive landscape of the market is characterized by technology-driven differentiation and strong OEM partnerships. Leading companies compete on sensor performance, system reliability and integration capabilities with ADAS platforms. The ability to enhance infrared sensors resolution and optimize thermal imaging technology plays a central role in securing contracts from premium automakers.

Manufacturers are increasingly focusing on reducing the high cost associated with night vision systems to expand beyond luxury vehicles into broader segments. Strategic collaborations with Tier-1 suppliers and semiconductor firms allow companies to strengthen their position in the night vision camera solutions. Furthermore, players are expanding their footprint across North America, Europe and Asia Pacific to capture regional growth and improve their market share.

Companies are also investing in R&D to support improved pedestrian detection, faster processing, and compatibility with multiple display formats such as HUD and instrument clusters. Strengthening supply chains and securing long-term OEM contracts remain essential competitive strategies.

- For instance, in January 2024, Valeo and Teledyne FLIR expanded their collaboration to advance thermal imaging for automotive safety systems, targeting wider OEM integration.

LIST OF KEY AUTOMOTIVE NIGHT VISION SYSTEM COMPANIES PROFILED

- Valeo (France)

- Continental AG (Germany)

- Denso Corporation (Japan)

- Bosch (Germany)

- Autoliv (Sweden)

- Magna International (Canada)

- ZF Friedrichshafen (Germany)

- Hella GmbH (Germany)

- Hyundai Mobis (South Korea)

- Aptiv (Ireland)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Teledyne FLIR OEM, a business unit of Teledyne Technologies, announced state-of-the-art advancements in infrared imaging, emphasizing its position as the world’s largest volume manufacturer of ITAR-free infrared sensors and thermal modules. Delivering tens of thousands of thermal modules weekly for automotive and other applications, the unit highlighted vertical integration and scalable production capability.

- November 2025: Teledyne Technologies reported FLIR segment revenues exceeding USD 900 million for the year, highlighting sustained demand for automotive and industrial thermal imaging applications.

- October 2025: Continental AG announced further development of integrated sensing platforms combining radar and thermal technologies for enhanced pedestrian and obstacle detection systems.

- October 2025: Raytron Technology and BYD partnered to integrate Raytron’s automotive infrared thermal imaging system into the Yangwang U8L, enhancing night driving safety. The system delivers up to 300 m detection range, identifying pedestrians and obstacles well beyond headlight reach, improving reaction time under low light conditions.

- September 2025: Bosch expanded its ADAS sensor manufacturing footprint to strengthen supply resilience for camera and perception technologies supporting nighttime safety solutions.

- August 2025: Hyundai Mobis revealed advancements in next-generation ADAS sensing modules designed to improve object recognition in low-visibility conditions for premium vehicle platforms.

- July 2025: Denso Corporation reported increased investment in sensing technologies and AI-driven perception systems as part of its electrification and ADAS growth strategy.

- May 2025: ZF Group introduced enhanced camera-based safety modules aimed at strengthening nighttime object recognition and integration with centralized vehicle computing architectures.

REPORT COVERAGE

The automotive night vision system market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, Technology, System Type, Display Type, Component, Sales Channel and Region |

| By Vehicle Type |

|

| By Technology |

|

| By System Type |

|

| By Display Type |

|

| By Component |

|

| By Sales Channel |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.40 billion in 2025 and is projected to reach USD 11.69 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.78 billion.

The market is expected to exhibit a CAGR of 11.1% during the forecast period of 2026-2034.

SUV segment led the market by vehicle type.

Rising focus on road safety and pedestrian protection is driving the market growth.

Valeo, Continental AG, Denso, and Aptiv are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us