Packaging Coatings Market Size, Share & Industry Analysis, By Resin Type (Epoxies, Acrylics, Polyurethane, and Others), By Substrates (Metal, Plastic, Glass, and Paper & Paperboard), By Application (Cans & Containers, Bags & Pouches, Boxes, Caps & Closures, Aerosols, and Others), By End-use Industry (Automotive, Food & Beverages, Personal Care & Cosmetics, Pharmaceuticals, Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

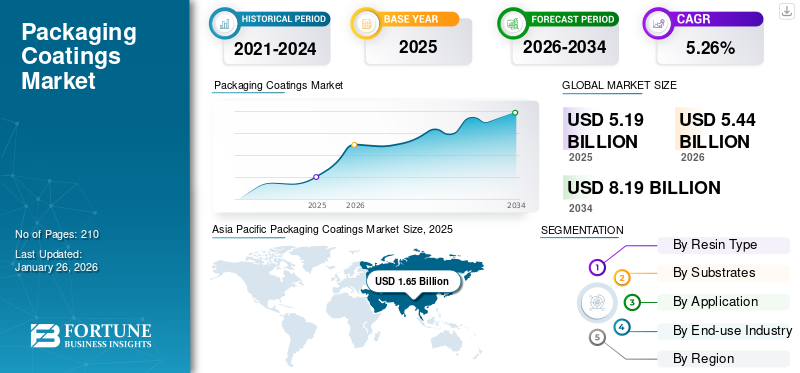

The global packaging coatings market size was valued at USD 5.19 billion in 2025. It is projected to be worth USD 5.44 billion in 2026 and reach USD 8.19 billion by 2034, exhibiting a CAGR of 5.26% during the forecast period. Asia Pacific dominated the packaging coatings market with a market share of 31.72% in 2025.

Packaging coatings are substances applied to packaging materials such as paper, cardboard, or plastic to improve their functionality and aesthetic appeal. The market is a dynamic sector integral in enhancing the durability, aesthetics, and functionality of various packaging materials across industries such as food and beverage, pharmaceuticals, and consumer goods. Rapidly growing demand for coatings from the food and beverage sector drives the market growth.

Axalta Coating and Akzo Nobel N.V. are the leading manufacturers, accounting for the largest global market share.

Download Free sample to learn more about this report.

Packaging Coatings Market Key Takeaways

- 2025 Market Size: USD 5.19 billion

- 2026 Market Size: USD 5.44 billion

- 2034 Forecast Market Size: USD 8.19 billion

- CAGR: 5.26% from 2026–2034

- Asia Pacific dominated the packaging coatings market with a 31.72% share in 2025.

- Epoxies segment is projected to lead the market with a 41.92% share in 2026.

- Cans and containers segment will account for a 39.71% market share in 2026.

Asia Pacific

Asia Pacific generated USD 1.65 billion in 2025 and is projected to reach USD 1.74 billion in 2026.

Europe

Europe was valued at USD 1.04 billion in 2025 and is projected to reach USD 1.09 billion in 2026.

North America

North America accounted for 24.76% of the global packaging coatings market in 2025.

U.S.

The U.S. market is expected to reach USD 1.06 billion by 2026.

Japan

The Japan market is expected to reach USD 0.33 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Environmental Awareness & Growth of E-commerce Sector Drives Market Growth

There is a significant shift towards biodegradable and eco-friendly coatings, driven by consumer demand and stringent environmental regulations. Manufacturers are innovating to develop coatings that are both effective and environmentally benign. Growing environmental awareness and strict regulations are leading to a transition towards sustainable coatings for packaging. Coatings that are water-based and bio-based are becoming more popular because of their reduced volatile organic compound (VOC) emissions and ability to be recycled. Both consumers and governments are pushing for environmentally friendly packaging options, encouraging manufacturers to innovate in this area. The rise in e-commerce has heightened the need for robust and protective packaging. Coatings capable of enduring the challenges of shipping and handling are crucial for maintaining product integrity during delivery.

Rapidly Growing Food & Beverage Sector Drives the Market Growth

The market for packaging coatings is closely tied to the food and beverage sector. This industry emphasizes the importance of product protection, resulting in a higher demand for packaging that shields contents from moisture, oxygen, and contaminants. Packaging coatings have emerged as one of the most notable trends around the globe. These coatings function as inhibitors that extend the shelf life of the packaged items and include biodegradable elements, tackling the problem of harmful substances. Regulatory guidelines play a crucial role in the packaging sector.

MARKET RESTRAINTS

Fluctuations in Raw Material Prices Obstruct Market Growth

Raw materials, especially those derived from petroleum, including polyurethanes, epoxies, and acrylics, are highly reactive to changes in demand. This reactivity is influenced by factors such as crude oil prices, disruptions in the supply chain, political unrest, and stringent environmental regulations. When the costs of critical raw materials rise, coating manufacturers encounter increased expenses. As a result, they are compelled to raise their prices to accommodate these additional costs. Numerous sectors rely on petrochemical by-products, which significantly influence the fluctuation in raw material prices in the coatings sector. Since the resins and solvents used in packaging coatings originate from petroleum, the volatility in costs is closely tied to fluctuations in crude oil prices, thus hampering the packaging coatings market growth.

MARKET OPPORTUNITIES

Technological Advancements Will Generate Growth Opportunities

The adoption of energy-curable coatings, such as UV and EB coatings, is on the rise due to their rapid curing times and reduced environmental impact. Additionally, digital inkjet coatings are gaining traction for their precision and efficiency in packaging applications. The demand for digitally compatible coatings is being propelled by the rise of short-run, on-demand packaging, which is fueled by e-commerce and specialized products. Coatings that change color in response to temperature or light, such as thermochromic and photochromic coatings used for freshness indicators, are increasingly popular. Advances such as nano-engineered coatings and smart packaging are improving product safety and extending shelf life. For example, nano-coatings provide enhanced barriers against moisture and gases, while smart coatings can detect and react to changes in the environment, maintaining product quality.

MARKET CHALLENGES

Regulatory, Compliance, and Performance Pose Challenges to the Market Growth

Navigating the complex landscape of global regulations concerning food safety and environmental standards poses a significant challenge for manufacturers. Navigating the various and rigorous environmental regulations in different areas can pose difficulties for manufacturers. Ensuring compliance frequently demands a substantial investment in research and development to produce effective yet compliant coatings. Creating coatings that achieve high performance while being eco-friendly is a complex task. Finding the right balance between these factors necessitates ongoing innovation and experimentation.

Download Free sample to learn more about this report.

PACKAGING COATINGS MARKET TRENDS

Regulatory-Driven Innovation Globally Emerges as a Key Market Trend

Consumers are increasingly conscious of environmental concerns and are seeking sustainable packaging options. Retailers such as Carrefour, Tesco, and Lidl are urging suppliers to remove plastic and non-recyclable coatings, which is driving the demand for environmentally friendly coating alternatives. Various regions enforce some of the strictest regulations concerning chemicals, emissions, and packaging waste (such as REACH, the Green Deal, and the Single-Use Plastics Directive). This compels companies to implement eco-friendly coatings, including water-based, low-VOC, BPA-free, and compostable solutions.

IMPACT OF COVID-19

The global market faced challenges due to COVID-19. Significant supply chain disruptions caused production to cease during the initial phases of the pandemic. As the COVID-19 outbreak unfolded, individuals were required to remain at home. Manufacturing unit interruptions had a worldwide effect on the packaging coating sector. Government-mandated closures and lockdowns stifled market growth. Nevertheless, in the aftermath of the pandemic, the market is expected to experience substantial growth driven by the rising demand for food and beverages on a global scale.

SEGMENTATION ANALYSIS

By Resin Type

Significants Benefits Boosts the Segment Growth of Epoxies

Based on the resin type, the market is segmented into epoxies, acrylics, polyurethane, and others.

The Epoxies segment is projected to dominate the market with a share of 41.92% in 2026. Epoxies are the dominant resin type segment and are projected to witness significant growth in the forecast period. Epoxy coatings provide extended durability and require minimal maintenance or replacement, rendering them as a cost-efficient choice for packaging manufacturers. The strong durability of epoxy-based coatings leads to reduced packaging failures and decreased waste over time, resulting in both financial and ecological advantages. With outstanding chemical resistance, epoxy coatings are perfect for packaging items that contain chemicals or are sensitive to environmental fluctuations.

Acrylics are the second-largest segment and are expected to grow rapidly in the coming years. The growing consumer inclination towards eco-friendly materials fuels the growth. There is a strong demand for waterborne acrylic resins because of their low levels of volatile organic compounds, which are essential for organizations aiming to comply with strict environmental laws.

By Substrates

Rising Demand for Metal-based Packaging Propels the Segmental Growth

Based on substrates, the market is segmented into metal, plastic, glass, and paper & paperboard.

The Metal segment is expected to lead the market, contributing 38.79% globally in 2026. Metal held the largest packaging coatings market share in the substrates segment. Metal leads as it is a preferred packaging option for preserving food and beverage items in the shape of metal cans and containers. Massive growth in the food and beverage sector, along with the rising demand for canned food products amongst the millennial population, also drives the market growth.

Plastic is the second most dominant substrate segment and will grow in the upcoming years. Plastics are preferred due to their adaptability and multifunctionality, which makes them suitable for a wide range of packaging uses. The expansion of sectors such as consumer goods, food and beverages, and pharmaceuticals fuels the increasing demand for plastic packaging solutions. This leads to a heightened need for innovative coatings that improve performance and sustainability.

By Application

Increasing Demand for Cans and Containers from Food Sector Boosts the Segmental Growth

Based on the application, the market is segmented into cans & containers, bags & pouches, boxes, caps & closures, aerosols, and others.

The Cans and containers segment will account for 39.71% market share in 2026. Cans and containers dominated the packaging coatings market. Cans represent the largest segment. The increase in the need for processed foods including canned soups, vegetables, and beverage cans has impacted the food industry supply chain. Since cans protect against corrosion and spoilage, they are extensively utilized for packaged foods and drinks, contributing to the growth of this segment.

Bags and pouches are the second most dominating application segment and are expected to grow rapidly in the coming years. Pouches have gained significant popularity in food packaging thanks to their resealable features, minimal environmental impact, and cost efficiency. They are frequently utilized for packaging items such as granola, energy beverages, coffee, soups, snacks, and a range of other food products. The growing demand for flexible packaging is influenced by factors such as convenience, lightweight construction, and capability to prolong the shelf life of goods.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Rapidly Growing Food & Beverages Sector Fuels the Segment’s Growth

Based on the end-use industry, the market is segmented into automotive, food & beverages, personal care & cosmetics, pharmaceuticals, and others.

The Food and beverages segment is expected to account for 33.46% of the market in 2026. Food and beverages held the largest market share in the end-use industry segment. The segment leads due to the prolonged shelf life that it offers to food items and ability to prevent contamination. The effectiveness of barrier packaging relies on the coating layers that block the passage of oxygen and UV rays, thereby preserving the quality of printed information. The rise in global consumption of packaged foods has heightened the demand for coatings within the food industry.

Automotive is the second most dominant end-use industry segment and will experience significant growth. Packaging coatings provide multiple advantages to the automotive industry by safeguarding parts throughout storage and transit. These coatings, such as VCI (volatile corrosion inhibitors) and other tailored materials, inhibit corrosion, damage, and contamination, guaranteeing that components reach their destination in excellent condition. Henceforth, such remarkable benefits boosts the segment’s growth.

PACKAGING COATINGS MARKET REGIONAL OUTLOOK

The market has been studied across five main regions: North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

Asia Pacific Packaging Coatings Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Rising Consumer Preferences for Food Drive the North American Market Growth

The North America region captured 24.76% of the global market in 2025, generating USD 1.29 billion in revenue, and is projected to reach USD 1.35 billion in 2026. North America is the second most dominating region of the packaging coatings market. North America stands out as the fastest-growing market, largely because of its consistent growth fueled by consumer preferences focused on sustainability and convenience. Manufacturers invest in the food and beverage products to meet consumer demand. Specifically, the U.S. and Canada have a substantial and well-established consumer base with significant disposable income levels. This results in a strong demand for packaged goods, including food and beverages, pharmaceuticals, cosmetics, and consumer electronics. The U.S. market is expected to reach USD 1.06 billion by 2026.

- Based on information from the Economic Research Service (ERS) of the USDA, American consumers allocated an average of 11.2% of their disposable income to food in 2023, as shown in the ERS chart. This percentage aligns with the level recorded in 2022. The proportion of income used for food purchased for home consumption fell from 5.6% to 5.3%, whereas the portion spent on dining out rose from 5.6% to 5.9%.

Europe

Presence of Major Manufacturers & Regulations Boosts Market Growth in Europe

Europe maintained a strong presence in the global market, reaching USD 1.04 billion in 2025, accounting for 20.09% share, and is expected to reach USD 1.09 billion in 2026. Europe is the third-largest contributor to the market. European manufacturers are at the forefront of developing bio-based and waterborne coatings, moving away from conventional solvent-based solutions. Europe possesses a significant premium market for food, cosmetics, and pharmaceuticals, which necessitates high-performance barrier coatings along with visually attractive and brand-safe packaging. These industries demand advanced coating formulations that adhere to health and safety regulations while providing strong shelf appeal. Europe enforces some of the strictest regulations globally regarding chemicals, emissions, and packaging waste (for instance, REACH, the Green Deal, and the Single-Use Plastics Directive). The U.K. market is expected to reach USD 0.21 billion by 2026, while the Germany market is expected to reach USD 0.24 billion by 2026.

- The REACH regulation of the EU stipulates that producers and importers of chemical substances are required to register these substances with the European Chemicals Agency (ECHA) to prove their safety for human health and the environment. This regulation, formally referred to as Regulation (EC) No 1907/2006, seeks to ensure a high standard of protection, evaluate chemical safety, foster innovation, and promote the adoption of alternative testing methods.

Asia Pacific

Rapidly Growing Food Sector in Major Countries Drives the Market Growth in Asia Pacific

In 2025, Asia Pacific generated USD 1.65 billion, contributing 31.72% to global market revenue, and is projected to grow to USD 1.74 billion in 2026. Asia Pacific is the dominant region of the global packaging coatings market. Factors such as rapid industrialization, urbanization, and a growing middle-class population drive the demand for packaged products, thereby boosting the need for packaging coatings. The ready-to-eat food sector, which employs a large amount of packaging coatings, caters to the fast-paced lifestyle of consumers by minimizing preparation time. Asian countries enforce rigorous food safety regulations, impacting the Asia Pacific packaging coatings market. Coatings are required to adhere to stringent compliance standards, resulting in substantial investments in research and development for targeted coatings that fulfill regulatory demands across various countries. The Japan market is expected to reach USD 0.33 billion by 2026, the China market is expected to reach USD 0.57 billion by 2026, and the India market is expected to reach USD 0.47 billion by 2026.

- The Ministry of Consumer Affairs, Food & Public Distribution (MCF) has stated that the growing number of working individuals, lack of time for food preparation, and the increasing elderly population in India are contributing factors to increased food consumption. This leads to greater demands for processed foods and ready-to-eat meals to cater to these changing consumer preferences and lifestyles,

Latin America

Rise in Demand for Metallic Coatings from the Cosmetic Sector Enhances Market Growth

The Latin America market generated USD 0.75 billion in 2025, representing 14.54% of the global market landscape, and is expected to reach USD 0.78 billion in 2026. The Latin America region will experience steady growth in the projected period. The market for packaging coatings includes different varieties, such as varnish coatings and lamination, which are commonly utilized for product boxes, labels, and retail packaging. Additionally, aqueous and metallic coatings enhance the visual appeal of products and are utilized in cosmetic packaging, gift boxes, and premium retail packaging. They also help maintain product integrity, as heat-seal coatings create secure and tamper-proof seals, thus generating high demand and driving market growth.

Middle East & Africa

Increasing Demand from Several End-use Industries Market Growth in the Middle East & Africa

Middle East & Africa recorded a market size of USD 0.46 billion in 2025, capturing 8.90% of the global market share, and is projected to reach USD 0.48 billion in 2026. The Middle East & African market is expected to grow significantly. The capacity of package coatings to deliver both glossy and matte finishes improves the product's appearance, driving market expansion. The use of vibrant colors and high-resolution imagery creates a soft texture, minimizes glare, and imparts a luxurious touch to the packaging. Additionally, the need for packaging coatings extends across multiple industries, including luxury packaging, premium consumer goods, and automotive packaging and market expansions drives market growth.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Market Participants to Witness Significant Growth Opportunities with New Product Launches

The market is highly fragmented and competitive. A few significant players are dominating the market by offering innovative packaging solutions in the packaging industry. These major market players constantly focus on expanding their customer base across regions by innovating their existing range of products. The market report also highlights the key developments by the manufacturers.

Major players in the industry include Axalta Coating, Akzo Nobel N.V., BASF SE, Arkema Group, Berger Paints India Limited, Chemetall, and others. Numerous other companies operating in the market are focused on market scenarios and delivering advanced packaging solutions.

List of the Key Packaging Coatings Companies Profiled in the Report

- Axalta Coating (U.S.)

- Akzo Nobel N.V. (Netherlands)

- BASF SE (Germany)

- Arkema Group (U.S.)

- Berger Paints India Limited (India)

- Chemetall (Germany)

- Dow Inc. (U.S.)

- Evonik Industries AG (Germany)

- FGN Fujikura Kasei Global Network (Japan)

- Henkel AG & Co. KgaA (Germany)

- Jamestown Coating Technologies (U.S.)

- Jotun (Norway)

- Kangnam Jevisco Co. Ltd (South Korea)

- PPG Industries, Inc. (U.S.)

- The Sherwin-Williams Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In April 2025, Amcor, a worldwide leader in creating and manufacturing sustainable packaging solutions, declared the completion of its new advanced coating facility for healthcare packaging located in Selangor, Malaysia. This modern facility is the first in Asia to utilize innovative air knife coating technology, enhancing the availability of high-quality, sterile packaging for healthcare clients throughout the region.

- In February 2025, Cosmo Specialty Chemicals introduced new oil- and grease-resistant (OGR) barrier coatings aimed at sustainable packaging solutions. Positioned as eco-friendly alternatives to traditional polyethylene (PE) coatings, these products are being phased out in response to environmental issues. The company released two variants of OGR coatings – OGR 145B and OGR 145S – to meet diverse industry needs. These water-based formulations are designed to facilitate the packaging sector’s transition to greener manufacturing practices.

- In January 2025, Stahl, a leading company in specialty coatings for flexible materials, announced its membership in CEFLEX, a joint European effort aimed at making all flexible packaging completely circular and compliant with the PPWR. This collaboration strengthens Stahl’s dedication to promoting sustainability and innovation throughout the packaging coatings value chain while solidifying its status as a global frontrunner in specialty coatings.

- In June 2024, Arkema, a frontrunner in specialty materials, revealed a significant advancement in manufacturing methods that incorporate as much as 40% post-consumer recycled content from discarded packaging products into its powder coating resins. This innovative technology will enable end markets to more effectively meet the growing societal demands for resource conservation and climate impact reduction.

- In July 2024, AkzoNobel introduced the Securshield 500 series for the metal packaging sector. The Securshield 500 range of easy open-end coatings aims to assist manufacturers and their clients in fulfilling existing and upcoming regulatory standards while offering a more sustainable solution that delivers greatly enhanced performance over current organosol-based options.

INVESTMENT ANALYSIS AND OPPORTUNITIES

- In October 2024, Brisbane-based Earthodic raised USD 6 million in initial funding to advance the creation of recyclable bio-based coatings for paper packaging, aiming to grow its presence in the US market. The start-up’s unique Biobarc coating provides an eco-friendly barrier that could substitute traditional petrochemical or plastic-based options, potentially minimizing packaging waste.

REPORT COVERAGE

The market research report provides a detailed market analysis. The packaging coatings market overview also focuses on key aspects, such as top key players, competitive landscape, product/service types, market segments, Porter's five forces analysis, and leading segments of the product. Besides, the report offers insights into the packaging coatings market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market intelligence & growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.26% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Resin Type

|

|

By Substrates

|

|

|

By Application

|

|

|

By End-use Industry

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 5.19 billion in 2025.

The market will likely grow at a CAGR of 5.26% over the forecast period.

The food and beverages end-use industry segment will lead the market in the forecast period.

The Asia Pacific market size stood at USD 1.65 billion in 2025.

The key market drivers are rising environmental awareness & growth of e-commerce sector and rapidly growing food & beverage sector.

Some of the top players in the market are Axalta Coating Systems, Akzo Nobel N.V., BASF SE, Arkema Group, Berger Paints India Limited, Chemetall, and others.

The global market size is expected to reach USD 8.19 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us