Parachute Market Size, Share & Industry Analysis, By Product Type (Ram Air Parachute, Round Wing Parachute, Rogallo Wing Parachute, Annular Parachute, Cruciform Parachute), By Application (Military, Civil Aircrafts, Rescue and Recovery, Break Chutes), By Component (Canopy, Ropes, Cords, Webbings, Metals) And Regional Forecast, 2026-2034

Parachute Market Size and Future Outlook

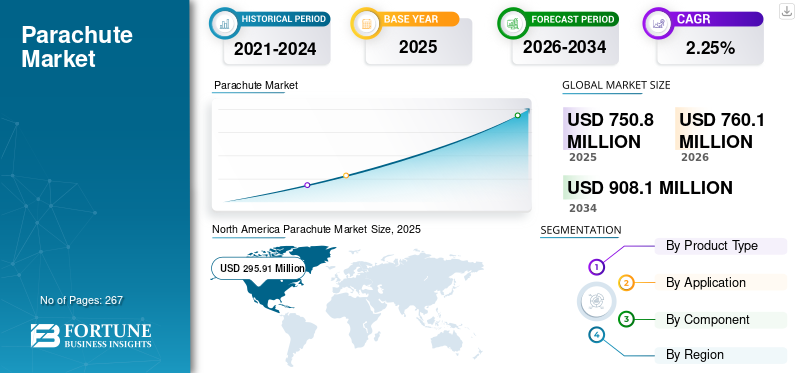

The global parachute market size was valued at USD 750.8 million in 2025. The market is projected to grow from USD 760.1 million in 2026 to USD 908.1 million by 2034, exhibiting a compound annual growth rate CAGR of 2.25% during the forecast period. North America dominated the global parachute market with a market share of 39.41% in 2025.

The global parachute market represents a specialized segment of the aerospace and safety systems industry, centered on equipment designed to slow descent, enable controlled landing, or provide emergency recovery for personnel, aircraft, cargo, and increasingly, unmanned systems. In its simplest terms, a parachute is a fabric-based aerodynamic decelerator; however, modern systems have evolved far beyond that, integrating advanced fibers, engineered canopies, structural webbings, automatic activation devices, and mission-specific designs for use in sports, the military, and industry.

The competitive landscape comprises a mix of defense-grade manufacturers and sport aviation specialists, with leading players including Airborne Systems, Spekon, Mills Manufacturing, Zodiac Aerosafety, Performance Designs, NZ Aerosports, Para-Avis, and Sup’Air, each serving a distinct niche, ranging from airborne troop systems to high-performance ram-air sport canopies.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Defense Modernization and Expansion of Airborne Operations to Fuel Market Growth

The key driver for the parachute market is ongoing defense modernization and the need to sustain high-readiness airborne forces. Governments are refreshing aging troop static-line systems, cargo delivery parachutes, and ejection seat recovery canopies to meet new safety, load, and mission profiles. Next-generation fighters, transport aircraft, and special operations units all require more capable personnel and cargo parachutes with improved stability, reduced opening shock, and increased payload margins. At the same time, most NATO countries and several Asian and Middle Eastern states are increasing the intensity of training for airborne units, which directly increases wear and replacement demand. This defense-driven base is relatively resilient to economic cycles, providing long-term visibility for key suppliers.

- In March 2025, the U.S. Army awarded Airborne Systems North America a USD 11.38 million contract to produce next-generation T-11 parachutes, signaling continued fleet renewal in personnel airdrop systems.

MARKET RESTRAINTS:

Stringent Safety, Liability, and Certification Burdens to Act as A Restraint for Growth

A major brake on parachute market growth is the extremely high bar for safety and certification. Parachutes are life-critical systems; a single malfunction can lead to loss of life, legal exposure, and immediate regulatory scrutiny. This drives lengthy test programs, conservative design choices, and costly qualification campaigns, especially for military ejection seats, cargo systems, and man-carrying sport gear. Operators and manufacturers must manage recurring inspections, repack cycles, and traceability for components such as cartridges, lines, and webbings. Any incident can trigger fleet-wide inspections or temporary groundings, disrupting demand and cash flow while also forcing redesigns. This risk profile naturally slows the adoption of novel concepts and materials, even when performance benefits are clear, as regulators and customers prioritize proven reliability over speed.

- In May 2024, an Air Force instructor pilot was killed when a T-6A Texan II ejection seat fired on the ground, prompting renewed scrutiny of ejection seat safety and components.

MARKET OPPORTUNITIES:

UAV, Drone, and Urban Air Mobility Recovery Systems Posing As a Major Market Opportunity

The most attractive upside for the sector lies in unmanned aircraft and future urban air mobility. As regulators open the door to drone operations over people and in dense urban areas, parachute recovery systems are emerging as a practical risk-mitigation tool to satisfy safety cases and specific operations risk assessments. This creates a new, scalable demand pool that is distinct from traditional military and sports segments. Commercial operators want compact, plug-and-play parachute kits that integrate flight termination, automatic triggering, and documented compliance with ASTM and aviation authority requirements. Suppliers that can package certified systems for popular drone platforms and docking stations are well-positioned to capture recurring business as fleets scale.

- In July 2024, EASA updated its Easy Access Rules for unmanned aircraft and adopted means of compliance that explicitly cover parachute-based mitigation. Meanwhile, in 2024, AVSS completed ASTM F3322 compliance testing for a DJI drone parachute recovery system, enabling safer flights over people.

Parachute MARKET TREND:

Move Toward Advanced Materials and Integrated Safety Systems to Pose Major Market Trends

Technology in parachute systems is shifting from “simple fabric and lines” to highly engineered, integrated safety solutions. On the hardware side, manufacturers are adopting low-porosity coated nylons, aramid webbings, and hybrid laminates to reduce weight while increasing strength and durability. On the system side, parachutes are being designed as part of comprehensive escape or recovery solutions, combining canopies, harnesses, flotation devices, oxygen supplies, and automatic activation into a single, certified package. Modern ejection seats, for example, optimize seat dynamics, parachute deployment, and pilot protection as a single system rather than independent components. This holistic approach supports wider pilot weight ranges, harsher flight envelopes, and more complex mission profiles.

- In 2024, Martin-Baker’s US16E ejection seat for the F-35, which integrates an optimized parachute and life-support package, remains a benchmark escape system that meets stringent neck-injury and pilot accommodation criteria across all F-35 variants.

MARKET CHALLENGES:

Managing Reliability, Perception, and Extreme Use Cases Present Threats to The Market Growth

Despite solid demand, the industry faces structural challenges in providing reliability under extreme conditions and maintaining public and customer confidence. Parachutes must function across a wide range of temperatures, loads, and dynamics, including supersonic regimes, for space and certain defense applications. Small anomalies, even when within design margins, can become front-page stories and raise questions about system robustness. Managing that narrative while systematically investigating and correcting issues is a constant challenge. The need for redundancy and fail-safe behavior also pushes complexity and cost, especially for multi-chute spacecraft and high-value platforms.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Round Wing Parachute Segment Dominates due to its Applications

Based on product type, the market is classified into ram air parachute, round wing parachute, Rogallo wing parachute, annular parachute, cruciform parachute, and others.

Round wing parachutes capture the largest parachute market share as they remain the workhorse for mass troop airdrop, cargo delivery, and many aircraft brake chute applications. Armed forces value their simplicity, ruggedness, and predictable opening characteristics, which make them suitable for large static-line operations and heavy-drop missions. Even as ram-air systems grow in special operations and sports, most modernization programs in airborne units focus on replacing legacy round systems (e.g., T-10) with safer, more stable descendants rather than changing the architecture entirely.

- In March 2025, Airborne Systems North America secured a USD 11.38 million U.S. Army contract to produce next-generation T-11 personnel parachutes, replacing older round T-10 systems and underscoring continued demand in this segment.

By Application

Aircraft Braking & Ejection Seats Segment Due to Its Benefits

In terms of application, the market is categorized into paragliding, skydiving, aircraft breaking & ejection seats, and others.

The aircraft braking & ejection seat is the largest application segment by value, as they are both safety-critical, tightly regulated, and relatively higher-priced compared to sport or recreational canopies. Fighter and advanced trainer fleets rely on drag chutes to ensure safe landings, particularly on short or wet runways, while ejection systems require precisely engineered recovery parachutes that are regularly inspected, refurbished, and replaced to ensure optimal performance. Ongoing fighter upgrades, improvements to pilot-rescue capabilities, and export programs ensure steady, long-term demand.

- In June 2025, India’s Ordnance Equipment Factory shipped its first batch of brake parachutes for Su-30 aircraft to the Royal Malaysian Air Force, highlighting continued global investment in aircraft deceleration systems and the underlying parachute fleets.

By Component

Canopy Segment Dominates Due To Rising OEM Investments

Based on component, the market is segmented into canopy, ropes, cords, webbings, and others.

The canopy is the largest component segment as it houses the majority of the fabric, engineering, and aerodynamic design that actually delivers deceleration and controllability. Across applications ranging from troop systems, brake chutes, cargo drops, or space-capsule recovery, OEMs invest heavily in canopy shape, panel layout, coatings, and reinforcement to manage opening shock, stability, and glide characteristics. As militaries and space agencies pursue higher-altitude deployments, heavier payloads, and more precise landing requirements, canopy designs become even more complex, driving up both technical value and per-unit cost.

- In November 2025, India’s DRDO and ISRO reported the successful testing of a Military Combat Parachute System at 32,000 feet and the Gaganyaan crew-module recovery parachute system, both of which rely on sophisticated multi-stage canopy architectures to meet demanding mission profiles.

By Material Used

Nylon Is the Dominant Segment Due To its Ability to Offer Predictable Performance Under Repeated Pack-Deploy Cycles

Based on material used, the market is segmented into polyester, nylon, parachute silk, Kevlar, and others.

Nylon remains the dominant segment in the parachute market due to its strong balance of strength, elasticity, weight, and cost. Modern low-porosity Nylon 66 fabrics offer predictable performance under repeated pack-deploy cycles, making them the standard for troop, cargo, brake, and many sports canopies. Even as aramids and other high-modulus fibers are introduced, they serve as reinforcements rather than replacements, particularly in mass-produced systems where cost and manufacturability are critical. As fleets modernize, operators more often upgrade to older weaves to improved nylon constructions rather than switching to a different material family.

- In June 2025, India’s export of Su-30 brake parachutes to Malaysia, utilizing nylon 66 canopies developed by the DRDO and produced by the Ordnance Equipment Factory, highlights nylon’s continued role as the primary structural fabric in frontline aircraft parachute systems.

To know how our report can help streamline your business, Speak to Analyst

Parachute Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America Parachute Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America

North America held the dominant position in 2024, valued at USD 295.5 million, and also maintained its leadership in 2025 at USD 295.9 million. The region is the largest parachute market, driven by the sheer scale of the U.S. defense spending and a highly developed skydiving industry. The U.S. maintains one of the world’s largest airborne forces and fighter fleets, supporting the continuous procurement of personnel, cargo, brakes, and ejection parachutes. In parallel, millions of civilian skydives each year create a substantial aftermarket for sport ram-air canopies, reserves, and harness–container systems. This combination of institutional and recreational demand provides North America with a broad and stable revenue base.

- In April 2024, USPA data indicated approximately 3.65 million skydives in the U.S. Meanwhile, in March 2025, the U.S. Army awarded Airborne Systems a USD 11.38 million contract for T-11 parachute production, underscoring the continued strengthening of both civil and military demand.

Europe

Europe is the second-largest parachute market, supported by NATO airborne units, national special forces, and a very active adventure sports ecosystem. European armies operate substantial paratroop and air-assault formations, creating steady demand for troop and cargo systems. Meanwhile, alpine countries host mature paragliding and skydiving industries that regularly refresh high-performance ram-air canopies. The region is also at the forefront of regulatory frameworks for parachute-equipped drones, opening an additional niche for recovery systems.

Asia Pacific

The Asia Pacific region is experiencing rapid growth and is expected to grow at the highest CAGR by 2034, even if it currently trails North America and Europe in absolute size. Defense modernization programs in India, China, and other regional powers are expanding airborne logistics, special forces, and fighter capabilities, directly increasing demand for cargo, combat, and brake parachutes. At the same time, adventure tourism hubs across India, Nepal, Southeast Asia, and Oceania are scaling up paragliding and tandem skydiving operations, which are lifting sales of ram-air canopies.

Rest of the World

The rest of the world includes the Middle East & Africa, and Latin America regions. The Middle East & Africa region is smaller in volume but characterized by high-value defense programs and concentrated flagship operators. Gulf states continue to invest in elite airborne units, special forces, and modern fighter fleets, all of which require advanced personnel parachutes, brake chutes, and ejection-recovery systems. Latin America is the smallest of the major regions, yet it remains strategically important, with Brazil serving as the primary anchor market.

COMPETITIVE LANDSCAPE

Key Players:

A Wide Range of Product Offerings by Key Companies Supported their Leading Position

The parachute market is moderately concentrated, anchored by a small group of defense-oriented manufacturers and several specialized sport-canopy OEMs. On the military side, Airborne Systems remains the global reference player in personnel, cargo, precision airdrop, and space recovery systems, supplying the U.S. and allied forces with advanced troop and guided cargo parachutes. Mills Manufacturing and North American Aerodynamics offer a comprehensive range of airborne troop, cargo, extraction, and deceleration chutes, serving as key suppliers to the U.S. Department of Defense and over 60 allied militaries.

In Europe, Spekon is a leading producer of military and sport parachutes, with in-house R&D and a wide portfolio across troop, tactical, and sport applications. On the sport side, Performance Designs and a few peers dominate high-performance ram-air canopies, reserves, and specialty designs for skydiving and canopy piloting, reinforcing a clear split between defense and recreational value pools.

LIST OF KEY COMPANIES PROFILED:

- Airborne Systems (U.S.)

- Mills Manufacturing (U.S.)

- Spekon (Sächsische Spezialkonfektion GmbH) (Germany)

- Performance Designs (U.S.)

- NZ Aerosports (New Zealand)

- Paraavis (Russia)

- Supair (France)

- Butler Parachute Systems (U.S.)

- National Parachute Industries (U.S.)

- CIMSA Ingeniería de Vuelo (Spain)

KEY INDUSTRY DEVELOPMENTS:

- June 2025 – Acron Aviation signed a multi-year contract with Air Cairo to deliver an outsourced FDM service via its Flight Data Connect (FDC) platform covering 36 aircraft across ATR, Embraer, and Airbus types. This strengthens Air Cairo’s safety and operational-performance analytics.

- June 2025 – Textron Aviation expanded its FDM service options by incorporating GE Aerospace’s C-FOQA offering for Cessna Citation business jets and SkyCourier aircraft. This broadens FDM access in the business-aviation segment and accelerates data-driven operations.

- June 2025 – GE Aerospace reported that its FlightPulse pilot-app user base surged from ~40,000 to over 60,000 commercial pilots in one year, with expectations to exceed 70,000 by year-end. This reflects the rising adoption of pilot-facing FDM tools and increased engagement in individual performance analytics.

- October 2025 – Directorate General of Civil Aviation (India) announced it would deploy a centralized software system to collect and monitor real-time flight data from airlines and OEMs. Choosing Tata Consultancy Services as a vendor raises regulatory-led impetus for FDM infrastructure in large emerging-market fleets.

- June 2024- A European defense ministry awarded a new contract for next-generation ram-air parachutes featuring autonomous glide correction, boosting special-forces operational range and accelerating modernization programs.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The global parachute market analysis provides an in-depth study of the market size & forecast by all segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 2.25% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Product Type

By Component

By Material Used

By Application

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 750.8 million in 2025 and is projected to reach USD 908.1 million by 2034.

In 2025, the market value stood at USD 295.91 Million.

The market is expected to exhibit a CAGR of 2.25% during the forecast period (2026-2034).

The canopy segment leads the market in terms of components.

Defense modernization and expansion of airborne operations are key factors driving market growth.

Airborne Systems (U.S.), Mills Manufacturing (U.S.), and Spekon (Sächsische Spezialkonfektion GmbH) (Germany) are prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 267

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us