Patient Lift Pendant Market Size, Share & Industry Analysis, By Product (Ceiling Lifts, Mobile Electric Lifts, Sit-to-Stand Lifts, and Bath/Shower Lifts), By Type (Wired Lift Pendants and Wireless Lift Pendants), By End-user (Hospitals and ASCs, Long-term Care Facilities, Homecare Settings, and Others), and Regional Forecast, 2026-2034

Patient Lift Pendant Market Size and Future Outlook

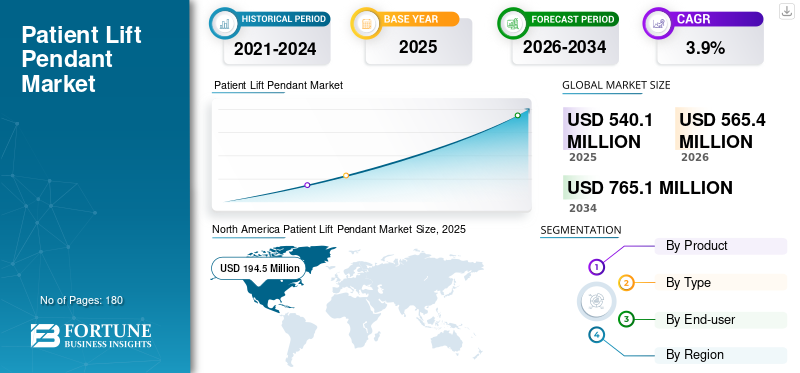

The patient lift pendant market size was valued at USD 540.1 million in 2025. The market is projected to grow from USD 565.4 million in 2026 to USD 765.1 million by 2034, exhibiting a CAGR of 3.9% during the forecast period. North America dominated the patient lift pendant market with a market share of 36.01% in 2025.

Patient lift pendants are the hand-held controls that let a caregiver operate ceiling lift, mobile electric lift, sit-to-stand device, or bath/shower lift, raising, lowering, and positioning a patient with a few button presses. In practice, the pendant is part of a broader control set that can also include the control box and electronics that manage motion, safety limits and battery status. Demand is rising as care teams are moving more patients with fewer staff, while expectations for dignity, safety, and the consistency of transfers continue to rise.

- The aging of the global population is a steady tailwind with the WHO projects that the number of people aged 60 and above will reach 1.4 billion by 2030 and 2.1 billion by 2050, increasing long-term care utilization and the need for assisted transfers.

Furthermore, Baxter, Arjo, Savaria, and Joerns Healthcare held the largest market share, driven by growing investments and calculated initiatives, such as new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

PATIENT LIFT PENDANT MARKET TRENDS

Rising Adoption of Wireless Devices and Modular Electronics is Reshaping the Overall Market

A prominent market trend is the move from purely wired hand controls to wireless options and modular control architectures. Wireless pendants help reduce cable damage, simplify cleaning, and improve maneuverability, especially in high-throughput wards. At the same time, manufacturers are treating lift controls less such as a simple handset and more such as a pendant, a control box, software/diagnostics, and service tools. This is crucial as it changes purchasing behavior. Buyers increasingly evaluate uptime, service response, and lifecycle cost, with the price of a replacement pendant. A Hillrom/Liko overview notes that an overhead lift is more than a motor and consists of many components working together, reinforcing the reason behind controls and electronics are central to performance and safety.

Another trend is portfolio expansion and lifecycle management, where companies publish updates on strategy and product direction that prioritize mobility and care efficiency. Over time, these trends support a richer control-component market than a pendants-only approach, with a growing mix of electronics, receivers and serviceable modules.

MARKET DYNAMICS

MARKET DRIVERS

Need for Safer Patient Handling Leads to Market Growth

The strongest driver is the ongoing shift from manual lifting to engineered safe-patient-handling programs across hospitals, long-term care, and homecare. As organizations prioritize staff safety and patient experience, lift utilization increases with the wear and tear on pendants, cables, buttons and control electronics. Controls are also where daily usability shows up with clear tactile buttons, reliable response and simple cleaning matter in real workflows. Thus, OEMs continue to emphasize integrated lift solutions designed around caregivers and patients.

Consolidation also supports investment in connected care and installed-base servicing. Additionally, companies focus on patient mobility solutions and on reinforcing their long-term focus on mobility ecosystems that generate ongoing aftermarket demand. As more facilities standardize protocols and train staff on lift use, pendant and control-component replacement becomes a routine budget line rather than an exception.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Pricing Pressure to Limit Market Growth

Even as lift usage expands, buyers often seek to manage total costs through bundling, standardizatio and tender-based purchasing, especially in public systems. Many lift pendant sales are bundled with a lift system purchase or maintenance contract, which can squeeze standalone pricing for control components. Hospitals and care networks may also rationalize suppliers to reduce SKU complexity and training burden, limiting smaller vendors’ access to large accounts.

In developed markets, a sizable share of demand is replacement-driven, so procurement teams may delay noncritical replacements, extend service life, or shift to refurbished components when budgets tighten. Another limiter is interoperability where pendants and control boxes are often model-specific, and compatibility constraints can discourage upgrades, such as moving from wired to wireless, unless the facility is also refreshing its lift fleet. Cleaning and infection-control practices can create tension; facilities want durable, sealed controls, but higher-spec designs can raise costs. The outcome is a market that grows steadily, but where unit growth does not always translate into proportional revenue growth unless suppliers can defend value through reliability, serviceability, and workflow benefits.

MARKET OPPORTUNITIES

Upgrading the Installed Base with Smarter and More Serviceable Controls to Create Significant Growth Opportunities

A large opportunity lies in the installed base: millions of transfers use older lifts, where the control experience is functional but outdated. Facilities increasingly want control that are easier to disinfect, harder to damage, and simpler to service, as downtime disrupts care and forces unsafe workarounds. This creates space for upgraded pendant designs, including improved ergonomics, sealed interfaces, clearer feedback and control boxes/electronics that enhance diagnostics and reduce troubleshooting time. Product positioning in the market reflects this push toward usability and versatility.

On the OEM side, the breadth of parts catalogs and accessories under established brands, such as Hillrom/Baxter’s Liko ecosystem, showing the size of aftermarket potential when controls are treated as serviceable, replaceable modules. As care shifts toward home and alternate sites, opportunities also emerge for simplified kit-based replacements, reducing the technical barrier for maintenance partners and accelerating replacement cycles.

MARKET CHALLENGES

Compatibility, Maintenance Complexity, and the Realities of Frontline Use Complicate Market Growth

One of the major challenge is compatibility where control boxes and pendants are often specific to lift models and generations, creating friction when facilities run mixed fleets across buildings or care settings. That increases inventory burden and can slow replacement when the right part isn’t on hand. Even when parts are available, installing and validating controls requires biomedical engineering time or trained service partners, resources that are in short supply in many regions. The real-world durability where pendants get dropped, tugged, disinfected repeatedly, and used by many hands every day with design choices that look fine on paper can fail in practice.

Finally, procurement and clinical teams don’t always align as procurement may optimize price, while frontline staff value ergonomics, speed, and reliability. This gap can delay upgrades to newer control platforms, even when those upgrades reduce downtime. The market also faces the challenge of proving ROI where control-component innovations must demonstrate measurable outcomes, such as fewer incidents, faster transfers, and less downtime, to win budget priority. Still, the large and growing care footprint, illustrated by the scale of nursing home beds in the U.S. and accelerating global aging, keeps the underlying need strong even when adoption is uneven.

Segmentation Analysis

By Product

Large Install Base of Mobile Electric Lifts to Drive Segment Growth

Based on product, the market is segmented into ceiling lifts, mobile electric lifts, sit-to-stand lifts and bath/shower lifts.

To know how our report can help streamline your business, Speak to Analyst

Mobile electric lifts typically account for a large share as they are the workhorse option and they move between rooms, don’t require ceiling infrastructure, and fit many transfer scenarios in hospitals, long-term care and homecare. That flexibility expands the installed base, which drives recurring demand for control components through routine wear, accidental damage and preventive replacement.

Additionally, the ceiling lifts segment is projected to grow at a CAGR of 4.7% during the forecast period.

By Type

Wide Utilisation of Wired Lift Pendants to Propel Segment Growth

By type, the market is classified into wired lift pendants and wireless lift pendants.

Wired pendants remain dominant in many settings as they are familiar, cost-effective, and widely compatible with older lift fleets. Facilities with mixed or aging equipment often standardize on wired replacements to avoid interoperability issues and keep training simple. Wired controls also suit environments where battery management and pairing procedures for wireless devices are seen as extra steps. Moreover, the segment is projected to hold a 67.5% share in 2026.

Additionally, the wireless lift pendants segment is estimated to grow at a CAGR of 5.3% during the forecast period.

By End-user

Advanced Healthcare Infrastructure in Hospitals & ASCs to Propel Segment Growth

On the basis of end-user, the market is classified into hospitals and ASCs, long-term care facilities, homecare settings, and others.

Hospitals and ASCs tend to hold a high share as they manage high patient throughput, higher-acuity mobility needs and strict workflow expectations. Transfers occur across departments such as ED, ICU, surgery recovery and imaging, resulting in heavy daily use of lift controls and accelerating replacement cycles for pendants and electronics. Hospitals also run formal safe-patient-handling programs and equipment maintenance schedules, which makes control-component replacement more systematic. Furthermore, the segment is set to hold 41.4% share in 2026.

In addition, the homecare settings segment is projected to grow at a CAGR of 5.4% during the forecast period.

Patient Lift Pendant Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

North America

North America Patient Lift Pendant Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 187.0 million, and reached USD 194.5 million in 2025. The huge installed base largely drives growth in North America. Hospitals, nursing homes and homecare providers experience high daily transfer volumes. Hence, control components, such as pendants, control boxes and electronics, see steady replacement demand due to wear, cable stress, drops and preventive maintenance. The region also has strong adoption of safe patient handling protocols, higher labor costs and ongoing staffing pressure, which push facilities to rely more on mechanical lifts and keep them operational with timely spares.

U.S. Patient Lift Pendant Market

In 2026, the U.S. market is forecasted to represent USD 181.4 million, capturing 32.1% of total global revenue.

Europe

Europe is expected to achieve a 2.7% growth rate in the coming years, the second-highest globally, reaching USD 161.8 million by 2026. Europe’s growth is anchored in aging demographics and a structurally large long-term care footprint, but the pattern is more tender and replacement led than purely expansionary. Public procurement and framework buying create periodic waves of upgrades. Similarly, hospitals and care homes maintain older mixed fleets that require model-specific controls, supporting a recurring aftermarket for compatible pendants and control boxes. Many countries also prioritize caregiver safety and standardization, which tends to increase lift utilization and, in turn, the replacement frequency of controls.

U.K. Patient Lift Pendant Market

The U.K. market is projected to reach USD 27.1 million by 2026, accounting for 4.8% of the global market revenue.

Germany Patient Lift Pendant Market

Germany's market is forecasted to reach about USD 28.9 million by 2026, representing roughly 5.1% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 139.3 million, ranking as the third-largest globally. Asia Pacific is typically the fastest-growing region as demand is coming from both fleet expansion and aftermarket replacement. Rapidly aging populations in developed markets and improving access to institutional and homecare services in emerging markets are increasing the number of assisted transfers performed every day. Many facilities are still moving from manual handling toward structured lift programs, so adoption is climbing from a lower base, especially for mobile and sit-to-stand lifts that don’t require ceiling infrastructure.

Japan Patient Lift Pendant Market

Japan is projected to generate approximately USD 24.2 million in revenue by 2026, contributing nearly 4.3% to the global market.

China Patient Lift Pendant Market

China’s market is forecast to reach approximately USD 41.5 million by 2026, contributing about 7.3% to global revenues.

India Patient Lift Pendant Market

India is forecast to contribute approximately USD 21.6 million to the market by 2026, corresponding to about 3.8% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate market growth, with Latin America expected to reach around USD 34.1 million by 2026. Latin America’s growth is driven by the gradual modernization of hospital and long-term care infrastructure, the expansion of private healthcare capacity in major urban centers and a steady shift toward safer transfer practices as facilities contend with staffing constraints. Growth in the Middle East & Africa is fueled by expanding hospital capacity in select markets, increased investment in healthcare modernization, and a rising focus on quality and caregiver safety, especially in higher-income Gulf countries, where new builds and equipment upgrades are more frequent.

GCC Patient Lift Pendant Market

By 2026, the GCC is expected to generate approximately USD 9.1 million in the market, accounting for nearly 1.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The competitive landscape is moderately consolidated at the top and highly fragmented in the long tail. A handful of global patient-handling OEMs capture a prominent share as they control system compatibility, have OEM-approved spare parts programs, and sell through facility procurement frameworks and service networks. Alongside them is a strong tier of regional lift specialists that compete on ceiling-lift coverage, ergonomics and service responsiveness in local healthcare systems. Key players such as Baxter, Arjo, Savaria and Joerns Healthcare held the largest market share.

Overall, competition is shaped by installed-base lock-in, aftermarket availability, and total cost of ownership. Differentiation is increasingly about modularity and serviceability, and the shift toward wireless/connected controls is raising the bar on reliability, pairing/security, and lifecycle support.

Moreover, other key players, such as Guldmann, Etac, Human Care Group, and Prism Healthcare Group, compete through ongoing technological advancements, the growing demand for improved healthcare infrastructure, and efforts to improve therapy outcomes.

LIST OF KEY PATIENT LIFT PENDANT COMPANIES PROFILED

- Baxter (U.S.)

- Arjo (Sweden)

- Savaria (Canada)

- Joerns Healthcare (U.S.)

- Guldmann (Denmark)

- Etac (Sweden)

- Human Care Group (Sweden)

- Prism Healthcare Group (U.K.)

- Invacare (U.S.)

- Winncare (France)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Arjo, a global leader in medical device technology, announced the launch of Maxi Move 5, the latest generation of one of the company’s best-selling products.

- January 2025: Arjo, a global leader in medical device technology, has presented Symbliss, an innovative assisted bathing system setting a new standard in the healthcare industry. Symbliss supports workflows that reduce caregiver injuries, optimize efficiencies in care settings and enables person-centered wellness experiences.

- November 2024: Invacare Holdings Corporation and MIGA Holdings LLC announced the acquisition of Invacare’s North American business by MIGA.

- March 2024: Etac launched Molift Transfer Pro, which provides comfortable and safe seated transfers, reduces the strain on caregivers, and enables early rehabilitation.

- December 2022: Industry coverage highlighted LINAK’s LIFT50 now IPX6 washable, reflecting ongoing upgrades in lift control solutions focused on cleanability/durability, key pain points for hand controls and control electronics.

- December 2021: Baxter International Inc., a global medtech leader, announced it has completed its acquisition of Hillrom.

- March 2021: Savaria Corporation, a global leader in the accessibility industry, is pleased to announce the successful completion of its recommended cash offer to acquire all of the issued and outstanding shares of Handicare Group AB.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.9% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Product, Type, End-user, and Region |

| By Product |

|

| By Type |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 540.1 million in 2025 and is projected to reach USD 765.1 million by 2034.

In 2025, North Americas market value stood at USD 194.5 million.

The market is expected to exhibit a CAGR of 3.9% during the forecast period of 2026-2034.

The mobile electric lifts segment led the market by product.

The key factors driving the market are the rising demand for safe patient-handling equipment.

Baxter, Arjo, Savaria, and Joerns Healthcare are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us