Patient Positioning Device Market Size, Share & Industry Analysis, By Product (Tables {Surgical Tables, Examination Tables, and Others}, Chairs, Accessories, and Others), By Application (Surgery, Diagnostics, and Others), By End-user (Hospitals and ASCs, Diagnostic Centers, and Others), and Regional Forecast, 2026-2034

Patient Positioning Device Market Size and Future Outlook

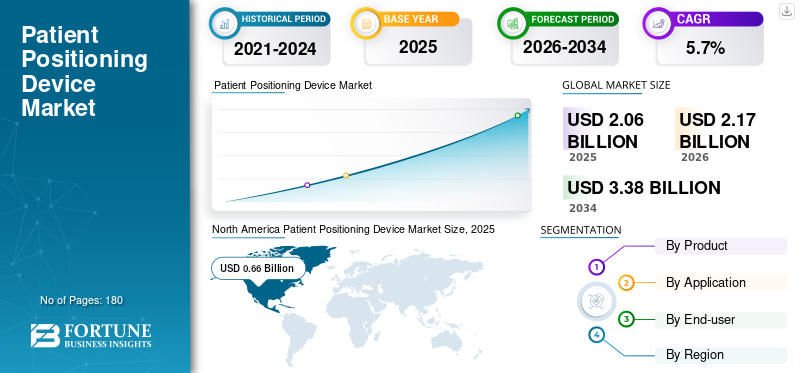

The global patient positioning device market size was valued at USD 2.06 billion in 2025. The market is projected to grow from USD 2.17 billion in 2026 to USD 3.38 billion by 2034, exhibiting a CAGR of 5.7% during the forecast period. North America dominated the patient positioning device market with a market share of 32.03% in 2025.

The global market encompasses tables, chairs, accessories, and related support systems used to safely and accurately position patients during surgery, diagnostics, and other clinical procedures. These devices help clinicians maintain the required posture, improve access to the treatment site, and reduce the risk of strain, pressure-related injury, and workflow disruption. An expansion in the market is observed as hospitals and ambulatory care providers handle a rising volume of surgical and diagnostic procedures while also placing greater emphasis on patient safety, efficiency, and procedural consistency. Growth is also supported by the broader expansion of the medical devices industry, increased healthcare utilization among aging populations, and the steady shift toward outpatient care models that require reliable, easy-to-use positioning solutions across multiple settings.

Further, STERIS, Stryker, Getinge AB, and Baxter International commanded the highest market share, supported by rising investments and strategic initiatives, including product introductions, alliances, and collaborative partnerships.

Download Free sample to learn more about this report.

Patient Positioning Device Market KEY TAKEAWAYS

- 2025 Market Size: USD 2.06 billion

- 2026 Market Size: USD 2.17 billion

- 2034 Forecast Market Size: USD 3.38 billion

- CAGR: 5.7% from 2026–2034

- North America dominated the patient positioning device market with a 32.03% share in 2025.

- Tables led the market due to their role in surgeries and diagnostics.

- The Hospitals & Ambulatory Surgery Centers (ASCs) segment is projected to account for the largest market share of 70.7% in 2026.

North America

The USD 0.66 billion market in 2025 is supported by advanced healthcare infrastructure and diagnostics.

Europe

The market is projected to reach USD 0.68 billion in 2026, growing at a 4.9% CAGR.

Asia Pacific

The market is projected to reach USD 0.54 billion market in 2026.

U.S.

The market is forecast to reach USD 0.60 billion in 2026.

Japan

The market is projected to reach USD 0.12 billion in 2026.

Read More

PATIENT POSITIONING DEVICE MARKET TRENDS

Ergonomic and Procedure-specific Designs Reshaping Buying Preferences to Boost Market Demand

A clear market trend is a shift from generic support products toward more specialized, workflow-aware designs. Buyers are no longer seeking only for durable tables or cushions; they increasingly prefer products that fit specific procedures, improve staff handling, and integrate smoothly into high-throughput clinical environments. This is encouraging the development of modular accessories, multi-position systems, pressure-relief materials, and ergonomic designs that help reduce repositioning time between cases.

Another strong trend is the move toward procedure-specific solutions for orthopedic, neurological, bariatric, and minimally invasive surgeries, where positioning precision directly affects clinical access and team comfort. Infection prevention is also influencing product design, with greater attention to cleanability, material durability, and reusable systems that withstand repeated disinfection. In diagnostic and outpatient settings, demand is gradually shifting toward compact products that support patient comfort without compromising clinician access. Altogether, the market is moving away from one-size-fits-all equipment and toward segmented solutions built around clinical use cases, workflow efficiency, and safety-driven procurement.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Higher Surgical Throughput Boosts Need for Dependable Positioning Systems Driving Market Growth

One of the strongest growth drivers in this market is the sustained rise in surgical and procedure-based care. Patient positioning devices are not optional support products; they are part of the practical infrastructure that allows surgeons, anesthetists, and diagnostic teams to work efficiently and safely. As healthcare systems perform more orthopedic, cardiac, neurological, gastrointestinal, oncological, and day-care procedures, the need for positioning tables, supports, straps, cushions, and specialty accessories naturally increases. The shift toward minimally invasive, precision-led interventions adds another layer of demand, as even small errors in posture or alignment can affect visibility, access, comfort, and procedural flow. Hospitals are also under pressure to improve operating room productivity and reduce avoidable complications, which makes well-designed positioning systems more valuable than basic furniture.

In parallel, the rise of ambulatory surgery is widening the customer base beyond large hospitals, creating demand for compact, ergonomic, and procedure-friendly solutions in outpatient settings. In effect, more procedures lead to greater equipment wear, increased replacement demand, and a greater preference for products that support repeatable patient setup.

MARKET RESTRAINTS

Budget Pressure and Uneven Capital Spending Continue to Slow Purchasing Decisions to Limit Market Growth

Despite steady demand, the market faces a clear restraint in the form of cost sensitivity across healthcare providers. Patient positioning devices fall into a category with high clinical importance. Still, procurement teams often weigh them against competing priorities such as imaging upgrades, monitoring systems, surgical tools, IT integration, and staffing needs. This is especially true for advanced surgical tables, powered chairs, and specialized accessories designed for bariatric, orthopedic, or complex multi-position procedures. In many hospitals, purchasing cycles are lengthy, budget approvals are layered, and replacement may be deferred unless the product directly affects procedural capacity or compliance.

Smaller facilities and cost-conscious centers may continue using legacy equipment longer than it is ideal, limiting faster market penetration of premium systems. The challenge is even more visible in emerging markets, where reimbursement limitations, import costs, and currency fluctuations can influence buying behavior. Accessories may witness repeated demand, but capital equipment purchases tend to be more sensitive to annual budgets and tender timing. As a result, the market grows steadily, but not as quickly as its underlying clinical need would suggest, as economics often shape the timing of adoption.

MARKET OPPORTUNITIES

Outpatient Expansion and Workflow-focused Upgrades to Create Significant Growth Opportunities

A major opportunity in this market lies in modernizing care settings beyond the traditional hospital operating room. Ambulatory surgical centers, specialty clinics, diagnostic centers, and short-stay procedure units are expanding in many countries, and these facilities require patient positioning solutions tailored to faster turnover, limited floor space, and staff-efficient workflows. This opens room for vendors to offer lighter, modular, and easier-to-clean systems that balance clinical performance with operational practicality.

Another opportunity comes from replacement demand. Many providers already own basic tables and supports, but they are increasingly seeking upgraded products that improve ergonomic handling, pressure redistribution, infection control, and compatibility with modern procedural workflows. There is also room for product differentiation through specialty positioning systems for robotic surgery, complex imaging, bariatric procedures, and prolonged interventions. As hospitals focus more sharply on safety metrics and procedure standardization, manufacturers that can show better positioning accuracy, easier setup, and lower maintenance burden are mostly to gain share. The market, therefore, has a meaningful opportunity not only in new installations but also in value-added upgrades to existing healthcare infrastructure.

MARKET CHALLENGES

Clinical Variability and Product Standardization Remains a Difficulty Across Care Settings

One of the main challenges in this market is that patient positioning is highly dependent on procedure type, patient condition, clinician preference, and facility infrastructure. A product that works well in a large tertiary hospital may not suit a day-surgery center, and a solution designed for general surgery may not meet the needs of advanced spine, robotic, or bariatric procedures. This makes standardization difficult for both buyers and manufacturers. Facilities often want versatile equipment, but clinical teams may request specialty support, which can increase procurement and inventory management complexity. Training is another challenge. Even strong products can underperform if staff are not familiar with optimal setup, accessory compatibility, or patient safety considerations during long procedures.

There is also the issue of balancing durability, comfort, and cost. Hospitals want products that last, are easy to disinfect, and support better outcomes, yet they remain cautious about premium pricing unless the return is clearly visible. For suppliers, success depends not just on manufacturing hardware but also on understanding workflows, supporting clinical education, and adapting products to diverse procurement environments across regions.

Segmentation Analysis

By Product

Wide Adoption and Applications of Tables to Drive Segment Growth

Based on product, the market is segmented into tables, chairs, accessories, and others. Furthermore, tables are further classified into surgical tables, examination tables, and others.

Tables account for the largest patient positioning device market share as they serve as the base platform for most surgical and diagnostic positioning. Whether in an operating room, procedure suite, or examination area, the table determines patient access, stability, height adjustment, posture control, and compatibility with accessories.

Additionally, the chairs segment is projected to grow at a CAGR of 6.8% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Surgery Dominates as Precise Patient Positioning is Fundamental to Safe and Efficient Intervention

By application, the market is classified into surgery, diagnostics, and others.

Surgery holds the highest share by application as positioning is central to nearly every operative workflow. Surgeons require proper alignment to gain clear access to the target anatomy. At the same time, anesthetic teams and nursing staff rely on a stable setup to manage safety and efficiency throughout the procedure. Long-duration and specialty surgeries further increase dependence on positioning tables, supports, and accessories that help reduce pressure points, improve exposure, and maintain repeatable posture. Moreover, the segment is projected to hold a 59.1% share in 2026.

Additionally, the diagnostics segment is estimated to grow at a CAGR of 6.4% during the forecast period.

By End-user

Hospitals and ASCs Lead in Demand as they Handle Highest Volume of Procedure-based Patient Care

On the basis of end-user, the market is classified into hospitals and ASCs, diagnostic centers, and others.

Hospitals and ambulatory surgery centers (ASCs) represent the largest end-user segment as they handle the highest volume of surgeries, short-stay procedures, and high-turnover clinical activity. These facilities require a broad range of surgical tables, examination tables, positioning chairs, and accessories to support routine and complex interventions. Hospitals typically account for major capital purchases, while ASCs contribute steady growth through expansion in outpatient surgery and same-day procedural care. Furthermore, the segment is set to hold a 70.7% share in 2026.

In addition, the diagnostic centers segment is projected to grow at a CAGR of 6.8% during the forecast period.

Patient Positioning Device Market Regional Outlook

Based on region, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Patient Positioning Device Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 0.63 billion, and reached USD 0.66 billion in 2025. North America is expected to maintain a strong position in the market due to its large procedural base, advanced hospital infrastructure, and high replacement spending on surgical and diagnostic equipment. The U.S. remains the main growth engine due to its extensive provider network, with the American Hospital Association reporting 6,093 hospitals. At the same time, the ambulatory care base is also deep, with more than 6,500 Medicare-certified ASCs. This creates sustained demand for surgical tables, examination tables, chairs, and accessories used across high-volume operating rooms and outpatient settings.

U.S. Patient Positioning Device Market

In 2026, the U.S. market is forecasted to represent USD 0.60 billion, capturing 27.8% of total global revenue.

Europe

Europe is expected to achieve a 4.9% growth rate in the coming years, the second-highest globally, reaching USD 0.68 billion by 2026. Europe’s growth is being supported by its mature hospital systems, strong public healthcare infrastructure, and steady modernization of surgical and diagnostic care environments. The region benefits from broad access to hospital-based and ambulatory care. At the same time, OECD reporting continues to show that outpatient surgery has become a major part of care delivery in many European health systems. This matters for these devices as a growing share of procedures is being handled in settings that need efficient, ergonomic, and space-conscious positioning equipment.

U.K. Patient Positioning Device Market

The U.K. market is projected to reach USD 0.12 billion by 2026, accounting for 5.6% of the global market revenue.

Germany Patient Positioning Device Market

Germany's market is forecasted to reach about USD 0.15 billion by 2026, representing roughly 6.9% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 0.54 billion, ranking as the third-largest globally. The region is projected to be the fastest-growing region, driven by a large patient pool, expanding hospital capacity, rising healthcare investment, and improving access to surgery and diagnostics. Compared with North America and Europe, many countries in the region are still building out their procedure infrastructure, which gives the market more room to grow through both first-time installations and ongoing upgrades.

Japan Patient Positioning Device Market

Japan is projected to generate approximately USD 0.12 billion in revenue by 2026, contributing nearly 5.4% to the global market.

China Patient Positioning Device Market

China’s market is forecast to reach approximately USD 0.17 billion by 2026, contributing about 7.8% to global revenues.

India Patient Positioning Device Market

India is forecast to contribute approximately USD 0.07 billion to the market by 2026, corresponding to about 3.3% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate patient positioning device market growth, with Latin America expected to reach around USD 0.14 billion by 2026. Latin America is expected to grow at a healthy pace due to the gradual expansion of hospital capacity, rising private healthcare participation, and improving access to diagnostic and surgical services in larger urban markets. The Middle East & Africa region is growing from a smaller base, but the outlook remains positive owing to healthcare infrastructure development, rising private-sector participation, and capacity expansion in key markets, especially across the GCC.

GCC Patient Positioning Device Market

By 2026, the GCC is expected to generate approximately USD 0.04 billion in the market, accounting for nearly 2.0% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Product Development Enhances Market Standing of Prominent Industry Players

The competitive landscape is moderately fragmented, with a handful of multinational medtech companies leading the market. At the same time, a long tail of regional and specialty manufacturers competes in accessories, procedure-specific positioning, and radiotherapy immobilization. Large competitors in the industry including STERIS, Stryker, Getinge AB, and Baxter International are strong as they offer broad OR-table and accessory portfolios and sell through established hospital relationships, which gives them scale in surgical positioning.

Furthermore, there are other major manufacturers in the market including Mizuho OSI, Skytron, LLC, CQ Medical, and Schaerer Medical AG. However, these companies compete through ongoing technological advancements, the growing demand for improved healthcare infrastructure, and efforts to improve therapy outcomes.

LIST OF KEY PATIENT POSITIONING DEVICE COMPANIES PROFILED

- STERIS (U.S.)

- Stryker (U.S.)

- Getinge AB (Sweden)

- Baxter International (U.S.)

- Mizuho OSI (U.S.)

- Skytron, LLC (U.S.)

- CQ Medical (U.S.)

- Schaerer Medical AG (Switzerland)

- SchureMed (U.S.)

- Orfit Industries (Belgium)

KEY INDUSTRY DEVELOPMENTS

- December 2025: CQ Medical acquired Bionix’s Radiation Therapy business unit, expanding its patient positioning and marking product portfolio.

- June 2025: C-RAD announced a 10 MSEK order to equip a new Texas satellite cancer facility with Catalyst+ HD and Sentinel 4DCT SGRT solutions.

- February 2025: Orfit highlighted the ongoing success of its collaboration with ZAP Surgical Systems, centered on patient positioning solutions for the ZAP-X radiosurgery platform.

- September 2024: Elekta announced that its AI-powered adaptive CT-Linear Accelerator, Elekta Evo, is available for sale and marketing in Europe, having received the CE mark.

- July 2024: CQ Medical, the new global leader in patient radiotherapy positioning and healthcare innovations that advance human care, showcased its patented solutions at the AAPM Annual Meeting in Los Angeles.

- May 2024: Elekta introduced its newest linear accelerator, Evo, a CT-based system featuring advanced AI-driven high-resolution imaging. This technology supports both offline and real-time adaptive radiation therapy, while also enhancing conventional image-guided radiation treatment capabilities.

- March 2024: Getinge AB announced the launch of the Corin OR table and Ezea surgical light at the Association of periOperative Registered Nurses (AORN) conference in Nashville, Tennessee.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, End-user, and Region |

| By Product |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.06 billion in 2025 and is projected to reach USD 3.38 billion by 2034.

In 2025, the market value stood at USD 0.66 billion.

The market is expected to exhibit a CAGR of 5.7% during the forecast period.

The tables segment led the market by product.

The key factors driving the market are the rising number of surgical procedures.

STERIS, Stryker, Getinge AB, and Baxter International are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us