Pet Food Ingredients Market Size, Share & Industry Analysis, By Pet Type (Dog, Cat, and Others), By Application (Dry Pet Food, Wet Pet Food, and Treats & Chews), By Source (Animal Sourced, Plant-Sourced, and Others), By Ingredient Type (Proteins [Animal-derived proteins, Plant-derived proteins, and Specialty Proteins], Grains & Cereals, Fats & Oils, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

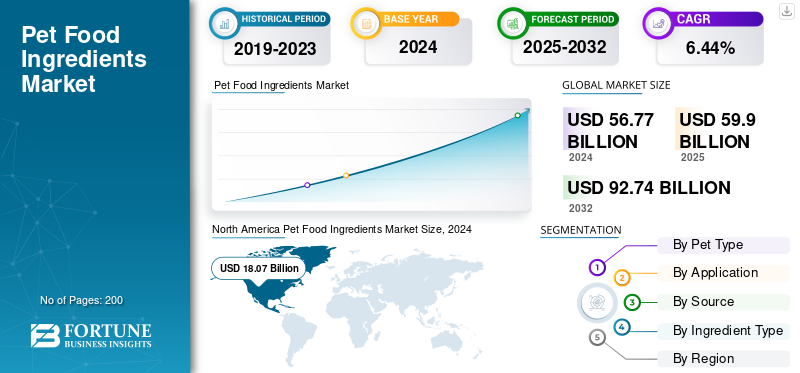

Pet Food Ingredients Market Size and Future Outlook

The global pet food ingredients market size was valued at USD 59.9 billion in 2025. The market is projected to grow from USD 63.34 billion in 2026 to USD 106.61 billion by 2034, exhibiting a CAGR of 6.72% during the forecast period. North America dominated the pet food ingredients market with a market share of 31.64% in 2025.

Pet food ingredients are the raw materials and additives combined to create nutritionally balanced food for pets, including sources of protein, carbohydrates, fats, vitamins, minerals, fibers, and functional additives. The market's expansion is catalyzed by rising pet ownership, increased awareness about pet nutrition, premiumization trends, and sustained innovation in ingredient sourcing and formulation. Growing awareness of pet health, human-grade ingredients, and fortified formulations containing probiotics, omega-3 fatty acids, and plant-derived proteins is reshaping the product portfolios of major manufacturers.

In addition, the industry is dominated by key players in the global market, including Archer-Daniels-Midland Company (ADM), Cargill, Incorporated, DSM-Firmenich AG, BASF SE, Kerry Group plc, and others.

Download Free sample to learn more about this report.

Pet Food Ingredients Market KEY TAKEAWAYS

- 2025 Market Size: USD 59.90 billion

- 2026 Market Size: USD 63.34 billion

- 2034 Forecast Market Size: USD 106.61 billion

- CAGR: 6.72% from 2026–2034

- North America dominated the pet food ingredients market with a 31.64% share in 2025.

- The dog segment held the largest market share, accounting for 58.82% in 2026.

- The dry pet food segment dominated the market with a 65.39% share in 2026.

North America

North America generated USD 18.95 billion in 2025 and is projected to reach USD 19.92 billion in 2026, supported by high pet ownership and premium pet food demand.

Europe

Europe accounted for 25.59% of the global market in 2025, reaching USD 15.33 billion and benefiting from growing demand for high-quality pet nutrition.

Asia Pacific

Asia Pacific was valued at USD 12.60 billion in 2025 and is projected to reach USD 13.45 billion in 2026, driven by rising pet adoption and urbanization.

U.S.

U.S. The market is projected to reach USD 14.37 billion by 2026, supported by increasing spending on premium and functional pet food products.

Japan

Japan The market is projected to reach USD 1.50 billion by 2026, driven by demand for specialized nutrition and high-quality pet food ingredients.

Read More

Pet Food Ingredients Market Trends

Increasing Trend of Plant-Based, Clean-Label and Alternative Proteins to Shape Industry

The expansion of plant-based and alternative proteins in organized pet food ingredients is gaining strong momentum, driven by sustainability concerns and health factors such as lactose intolerance in companion animals. In this context, insect, yeast, algal, and mycoprotein-based ingredients are being increasingly researched and commercialized as nutritious and eco-friendly protein sources. Players in the market are also launching new products in the market in order to meet the rising global market demand.

- For instance, Marsapet launched the first complete dog food featuring FeedKind Pet protein, developed by Calysta. Released under the Marsavet line, the product named MicroBell is a dry kibble dog food that is vegan, grain-free, and gluten-free, formulated to provide all essential amino acids necessary for canine health.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Pet Ownership and Premiumization of Pet Diets to Drive Market Growth

A rapid increase in global pet ownership, coupled with the trend toward premium and specialized nutrition, has become a primary driver of global pet food ingredients market growth. Households are increasingly treating pets as family members, prioritizing health, digestive care, and taste. Growth in the global pet food ingredients industry is driven by rising willingness to invest in tailored nutrition and wellness. Modern consumers increasingly demand for high-quality, functional, and specialty formulations that support digestive health, immunity, and specific life-stage needs, further fueling the market growth.

- According to the European Pet Food Industry Federation (FEDIAF), in 2024, approximately 90 million households in the European Union own a pet, which accounts for around 46%.

Market Restraints

Stringent Regulatory Frameworks and Ingredient Approval Delays to Impede Market Growth

The pet food ingredients industry is closely regulated by authorities such as the U.S. Food and Drug Administration (Center for Veterinary Medicine), the European Food Safety Authority (EFSA), and the Association of American Feed Control Officials (AAFCO). Approvals for new feed additives, probiotics, or alternative proteins can take 2–3 years, significantly delaying commercialization, hampering market growth. While these regulations enhance safety, they also raise administrative costs and slow product launches, particularly for smaller ingredient innovators and exporters entering new markets.

Market Opportunities

Expansion of Functional and Health-Oriented Pet Food Ingredients to Unlock New Growth Opportunities

The growing humanization of pets is transforming feeding behavior from basic nutrition to preventive healthcare. Pet owners increasingly seek ingredients that provide specific health benefits such as digestive health, immunity support, skin and coat enhancement, and joint care. This has driven innovation in functional ingredients, including probiotics, omega-3 fatty acids, glucosamine, postbiotics, antioxidants, and botanical extracts. The global functional pet food trend mirrors the success of human nutraceuticals, opening lucrative opportunities for ingredient manufacturers.

- According to the American Pet Products Association (APPA) report for 2024, the use of vitamins and supplements in pet food has grown by nearly 50% for dogs and 60% for cats since 2018.

SEGMENTATION ANALYSIS

By Pet Type

High Global Ownership and Spending to Lead Dog Segment’s High Market Proportion

Based on pet type, the market is segmented into dog, cat, and others.

The dog segment holds the largest global pet food ingredients market share, with a 58.82% share in 2026 and a projected CAGR of 6.33% through 2026-2034, supported by high global dog ownership rates. In 2025, the global market size for dog food ingredients was valued at approximately USD 35.27 billion, outpacing the cat and other pet segments significantly. Average annual spending on dog food is significantly higher than that for other pets, driven by consumer prioritization of nutrition, health, and specialty ingredients such as proteins, supplements, and functional additives.

- According to the Food and Agriculture Organization, the global population of pet dogs is estimated to be approximately 470 million, and the total number of pet cats and dogs is around 840 million.

The cat segment is expected to grow significantly over the forecast period with a CAGR of 6.76%.

By Source

High Nutritional Profile and Widespread Consumer Preference to Lead Animal-Sourced Segment Growth

On the basis of source, the market is segmented into animal-sourced, plant-sourced, and others.

The animal-sourced segment is expected to maintain a significant position in the global market, with a market valued at USD 33.73 billion in 2024. The growth is driven primarily due to the high nutritional value, palatability, and widespread consumer preference for meat proteins in pet diets, especially for dogs and cats. Also, meat, fish, poultry, and rendered animal meals provide complete proteins (containing all essential amino acids), fats, and essential micronutrients such as iron, zinc, and calcium.

The plant-sourced segment is expected to grow significantly at a CAGR of 7.04% over the forecast period.

By Application

Dry Pet Food Segment Dominates Market Due to its Strong Demand from Pet Owners Globally

On the basis of application, the market is segmented into dry pet food, wet pet food, and treats & chews.

The dry pet food segment dominates the global market, holding 65.39% share in 2026, due to its unmatched convenience, cost-effectiveness, long shelf life, and ease of storage and transportation. Additionally, its broad consumer adoption and practicality make it the default choice for mass-market pet owners, supporting widespread distribution through both brick-and-mortar and online retail channels.

The treats & chews segment is anticipated to grow at a CAGR of 7.33% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Ingredient Type

Protein Segment Dominates Market as it is Essential for Pet Health & Nutrition

On the basis of ingredient type, the market is segmented into proteins, grains & cereals, fats & oils, and others.

The protein segment accounted for 50.45% of the market share in 2025 and is expected to maintain this majority share through the coming years. The segment is further divided into animal-derived proteins, plant-derived proteins, and specialty proteins. Proteins are the fundamental building blocks for growth, muscle maintenance, immunity, enzyme production, and hormone production in pets. Both animal and plant proteins provide essential amino acids that are vital for the health of dogs and cats.

The others segment is anticipated to grow at a CAGR of 6.57% during the forecast period.

Pet Food Ingredients Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Pet Food Ingredients Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 18.95 Billion in 2025, representing 31.64% of the global market landscape, and is expected to reach USD 19.92 Billion in 2026. The U.S. leads the region, followed by Canada and Mexico. High disposable incomes, widespread pet ownership, and preference for premium, human-grade ingredients underpin growth. According to the American Pet Products Association (APPA), 66% of U.S. households own at least one pet, and total annual spending on pets exceeded USD 147 billion in 2023. The U.S. market is projected to reach USD 14.37 billion by 2026.

Europe

Europe represents a high-value market emphasizing sustainability, regulatory compliance, and ingredient quality. Europe contributed 25.59% to the global market in 2025, with a valuation of USD 15.33 Billion, and is projected to reach USD 16.15 Billion in 2026. The region benefits from the strong presence of FEDIAF (European Pet Food Industry Federation), which enforces strict nutritional and safety standards. The UK market is projected to reach USD 2.86 billion by 2026. The Germany market is projected to reach USD 2.41 billion by 2026.

Asia Pacific

Asia Pacific accounted for USD 12.6 Billion in 2025, representing 21.03% of the global market share, and is projected to reach USD 13.45 Billion in 2026. Increasing disposable incomes in emerging economies, such as China, India, and Japan, enable consumers to spend more on premium pet food products that offer enhanced nutrition and quality. The Japan market is projected to reach USD 1.5 billion by 2026. The China market is projected to reach USD 3.97 billion by 2026. The India market is projected to reach USD 2.14 billion by 2026.

South America

South America is witnessing robust growth driven by rapid urbanization, increasing pet humanization, and the availability of low-cost feedstock ingredients. Brazil dominates the regional market, followed by Argentina and Chile.

Middle East & Africa

In 2025, Middle East & Africa held 7.70% of the global market, reaching a valuation of USD 4.61 Billion, and is projected to grow to USD 4.91 Billion in 2026. Middle East & Africa is an emerging high-potential region with rising pet adoption rates coupled with growing urbanization, especially in Gulf Cooperation Council (GCC) countries such as Saudi Arabia, UAE, and Kuwait, which boosts demand for premium and diverse pet food formulations.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Focus on Strategic Partnership and Innovation to Support Market Growth

The global pet food ingredients market is moderately consolidated, with leading companies focusing on strategic partnerships, acquisitions, and innovation in ingredient sourcing. Key players include ADM, Darling Ingredients, Kemin Industries, Roquette, BASF, Omega Protein, Symrise, and several other companies. Market consolidation is balanced by regional and niche specialty ingredient providers who are increasing competition by offering customized and sustainable solutions.

Key Players in Pet Food Ingredients Market

|

Rank |

Company Name |

|

1 |

Archer-Daniels-Midland Company |

|

2 |

Cargill, Incorporated |

|

3 |

DSM-Firmenich AG |

|

4 |

BASF SE |

|

5 |

Kerry Group plc |

List of Key Pet Food Ingredients Companies Profiled in Report

- Archer-Daniels-Midland Company (ADM) (U.S.)

- Cargill, Incorporated (U.S.)

- DSM-Firmenich AG (Switzerland)

- BASF SE (Germany)

- Nestlé Purina PetCare (U.S.)

- Mars Petcare, Inc. (U.S.)

- Kerry Group plc (Ireland)

- Symrise AG (Germany)

- Ingredion Incorporated (U.S.)

- Nutreco N.V. (Trouw Nutrition) (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Fredun Pharmaceuticals launched Snacky Jain, India’s first Jain functional pet food product, which is entirely plant-based and free from meat, root vegetables such as onion and garlic, and all animal-derived ingredients including honey.

- October 2025: Leaft Foods launched Alfalfa Protein Concentrate (APC), a leaf-based protein ingredient extracted from alfalfa plants, specifically designed for pet food applications. APC provides protein levels similar to those of meat while generating approximately 99% lower carbon emissions than beef or lamb. The ingredient contains omega-3 and omega-6 fatty acids, antioxidants, and vitamin K, making it nutritionally beneficial for pets.

- April 2025: ADM opened its first wet pet food manufacturing facility in Mexico, located in Yecapixtla, Morelos, with an investment of USD 39 million. The new facility includes three production lines and would produce wet food for ADM’s Ganador and Minino brands. This expansion strengthens ADM's position as one of the top two pet food manufacturers in Mexico.

- August 2024: Above Food Ingredients expanded its plant-based pet food ingredient business through the acquisition of The Redwood Group's (TRG) Specialty Crop Food Ingredient division for USD 34 million. This division, based in Montana and Kansas, supplies high-quality grains, cereals, oilseeds, pulses, and other alternative protein sources for both human and pet food markets.

- April 2024: dsm-firmenich introduced an omega-3 ingredient for pets called Veramaris Pets, which is an algal oil designed for cat and dog foods. This ingredient contains 60% EPA (eicosapentaenoic acid) and DHA (docosahexaenoic acid), the highest concentration available in the market, offering more than double the potency of equivalent fish oil.

- February 2024: Kerry launched its first postbiotic ingredient named Plenibiotic, derived from Lactobacillus casei subsp. 327, designed to support gut and skin health for both humans and pets. This rice-derived postbiotic is shelf-stable, effective at low doses, and tolerant to various processing and storage conditions.

- December 2020: Nestlé Purina PetCare invested USD 550 million to expand its pet food manufacturing facility in Hartwell, Georgia, U.S. The expansion is expected to create up to 130 new jobs in Hart County, increasing the facility's workforce to approximately 370 employees. The Hartwell plant produces several of Purina's flagship brands, including Fancy Feast, and plans to include Friskies brand cat food as part of the expanded operations.

REPORT COVERAGE

The global pet food ingredients market report analyzes the market in depth and highlights crucial aspects such as global market trends, supply chain, secondary research, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.72% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Pet Type

|

|

By Application

|

|

|

By Source

|

|

|

By Ingredient Type

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 59.9 billion in 2025 and is anticipated to reach USD 106.61 billion by 2034.

At a CAGR of 6.72%, the global market will exhibit steady growth over the forecast period.

By pet type, the dog segment leads the market.

North America held the largest market share in 2025.

Rising pet ownership and the premiumization of pet diets drive the market growth.

Archer-Daniels-Midland Company (ADM), Cargill, Incorporated, DSM-Firmenich AG, BASF SE, and Kerry Group plc are the leading companies in the market.

Expansion in plant-based and alternative proteins is shaping the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us