PET Lidding Films Market Size, Share & Industry Analysis, By Type (High-Barrier Lidding Films, Dual-Ovenable Lidding Films, Breathable Lidding Films, Resealable Films, Specialty Lidding Films, and Others), By Product Type (Trays, Cups, Bottles & Cans, and Others), By End-use Industry (Food & Beverages, Pharmaceuticals, Personal Care & Cosmetics, and Others), and Regional Forecast, 2026-2034

PET Lidding Films Market Size and Future Outlook

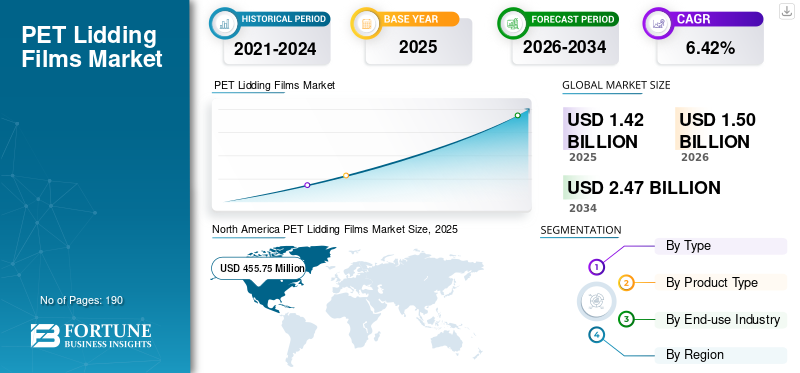

The global PET lidding films market size was valued at USD 1,422.00 million in 2025. The market is projected to grow from USD 1,502.27 million in 2026 to USD 2,471.14 million by 2034, exhibiting a CAGR of 6.42% during the forecast period. North America dominated the PET lidding films market with a market share of 32.07% in 2025.

The industry for PET lidding films encompasses the manufacturing and distribution of Polyethylene Terephthalate (PET) films utilized as sealing layers for trays and containers in sectors such as food, pharmaceuticals, and consumer packaging. These films provide clarity, seal integrity, barrier protection, and recyclability. The increasing demand for sustainable, convenient, aesthetically pleasing, and recyclable packaging, especially for ready-to-eat meals and fresh produce, is propelling the use of PET lidding films. This trend is further bolstered by their outstanding transparency, robust sealing capabilities, and compatibility with mono-material PET packaging systems.

Furthermore, many key industry players, such as Klöckner Pentaplast, Constantia Flexibles, and Graphic Packaging International, LLC, operating in the market, are focusing on developing innovative products and conducting R&D.

Download Free sample to learn more about this report.

PET LIDDING FILMS MARKET TRENDS

Shift Toward Recyclable Mono-Material PET Packaging is a Prominent Trend Observed in the Market

A significant trend influencing the global market is the rapid transition towards recyclable mono-material PET packaging structures. Brand owners, retailers, and packaging converters are increasingly focusing on packaging designs that can be easily recycled within current PET waste streams. This trend is strongly backed by sustainability commitments from leading food and consumer goods companies, many of which have established goals for 100% recyclable packaging within the next decade. Moreover, the growing demand for high-clarity packaging that improves product visibility at the point of sale is further promoting the use of such films in fresh and chilled food applications.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Convenience and Fresh Food Packaging is Propelling Market Growth

The increasing global appetite for convenience and fresh food items is a significant factor propelling the market progress. Urbanization, evolving lifestyles, and a higher involvement of working individuals are driving the demand for ready-to-eat meals, pre-sliced fruits and vegetables, chilled meat, seafood, and dairy products. Moreover, PET lidding films facilitate Modified Atmosphere Packaging (MAP) and vacuum packaging methods, which are being utilized more frequently to prolong shelf life and minimize food waste.

The expansion of organized retail, supermarket chains, and online grocery services is further promoting the use of PET-based lidding solutions, especially in developing countries. The blend of functional efficiency, visual attractiveness, and compatibility with automated packaging systems positions these films as a favored option for high-volume food packaging, thereby directly contributing to ongoing market growth.

MARKET RESTRAINTS

Raw Material Price Volatility and Cost Pressures Hampers Market Growth

The volatility of PET resin prices continues to be a significant constraint for the global market. The prices of PET are intricately connected to the variations in crude oil and petrochemical feedstock markets, which are affected by geopolitical tensions, supply interruptions, and shifts in global demand. Abrupt price hikes can greatly influence production expenses for film manufacturers, thereby diminishing profit margins and posing difficulties in establishing long-term contract pricing with clients. Smaller and mid-sized manufacturers are especially at risk, as they frequently do not possess the purchasing power or inventory reserves necessary to effectively navigate sharp fluctuations in costs.

MARKET OPPORTUNITIES

Innovation in Sustainable and High-Barrier Films Provides Potential Growth Opportunities

The market for PET lidding films offers considerable opportunities fueled by advancements in sustainable and high-barrier film technologies. Food and pharmaceutical producers are progressively looking for lidding films that provide superior barriers against oxygen, moisture, and aroma, all while being recyclable. This growing demand is prompting the creation of innovative coatings, multilayer yet recyclable PET structures, and the incorporation of bio-based or recycled PET materials. Manufacturers that prioritize research and development, lightweight designs, and sustainable solutions that comply with regulations are strategically positioned to seize new opportunities in the food, pharmaceutical, and specialty packaging sectors.

MARKET CHALLENGES

Intense Competition from Alternative Lidding Materials Poses a Critical Challenge to Market Growth

A significant obstacle facing the PET lidding films market growth is the fierce competition posed by alternative lidding materials, such as PE-based, PP-based, aluminum foil, and paper-based options. Each of these materials presents distinct benefits based on its intended use. Educating consumers on the recyclability benefits and ensuring that PET lidding films are compatible with current PET tray recycling processes continues to be a vital challenge. In the absence of clear differentiation, these lidding films may lose market share in price-sensitive or sustainability-focused sectors, necessitating strategic positioning and continuous driving innovation to uphold competitiveness.

Segmentation Analysis

By Type

Superior Protection and Shelf-Life Extension Drive the Dominance of High-Barrier Lidding Films

Based on the type, the market is divided into high-barrier lidding films, dual-ovenable lidding films, breathable lidding films, resealable films, specialty lidding films, and others.

The high-barrier lidding films segment is expected to account for the largest PET lidding films market share. The prevalence of these lidding films in the market is mainly attributed to their remarkable capacity which offers outstanding protection against oxygen, moisture, aroma, and microbial contamination, which directly influences product quality and extended shelf life. These functional advantages prompts manufacturers to prefer high-barrier PET films over conventional lidding alternatives.

Moreover, their compatibility with Modified Atmosphere Packaging (MAP) and vacuum-sealed packaging enables brands to prolong shelf life, minimize food waste, and adhere to rigorous quality standards, establishing a significant cause-and-effect link between barrier performance and market acceptance.

The breathable lidding films segment is expected to grow at a CAGR of 6.48% over the forecast period.

By Product Type

Convenience, Compatibility, and Food Safety Drive the Dominance of Trays in the Market

Based on product type, the market is segmented into trays, cups, bottles & cans, and others.

In 2025, the trays segment dominated the global market attributed to the unmatched convenience, structural integrity, and compatibility with various food items that they provide. They are extensively utilized in ready-to-eat meals, fresh produce, meat, dairy, and seafood, as they offer a robust foundation that safeguards products throughout transportation, handling, and storage. The application of PET lidding films on these trays improves their functionality by guaranteeing airtight seals, maintaining freshness, and prolonging shelf life, thereby establishing a direct relationship between tray design and the use of lidding films.

The cups segment is projected to grow at a CAGR of 6.48% over the forecast period.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Food & Beverages Segment Leads Owing to Freshness, Convenience, and Shelf Appeal Offered by the Films

Based on the end-use industry, the market is segmented into food & beverages, pharmaceuticals, personal care & cosmetics, and others.

The food & beverages segment holds and is also expected to hold a dominant market share over the forecast period due to the steady demand for fresh, convenient, and ready-to-eat products across the globe. Additionally, the clarity and printability of PET films improve product visibility and shelf attractiveness, which affects consumer buying choices, promoting further adoption. The rising trend of on-the-go consumption, pre-packaged meals, chilled drinks, and fresh-cut produce has heightened the necessity for packaging solutions that offer protection, convenience, and presentation benefits.

The pharmaceuticals segment is projected to grow at a CAGR of 6.32% over the forecast period.

PET Lidding Films Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America PET Lidding Films Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 429.97 million, and maintained its leading position in 2025, with a value of USD 455.75 million. In North America, the market is propelled by a robust demand for ready-to-eat meals, fresh-cut produce, and dairy items. Sustainability initiatives and regulations that advocate for recyclable packaging foster the adoption of mono-PET lidding films.

U.S. PET Lidding Films Market

Based on North America’s strong contribution and the U.S.’s dominance within the region, the U.S. market was analytically approximated around USD 375.22 million in 2025, accounting for roughly 26.39% of global sales. In the U.S., the expansion of the market is driven by a rise in the consumption of both pre-packaged and fresh foods, along with strict FDA regulations concerning food safety and packaging standards.

Europe

Europe is projected to grow at 6.42% over the coming years, the third-highest among regions, and reach a valuation of USD 357.92 million by 2025. The market in Europe is primarily influenced by sustainability mandates and circular economy initiatives throughout the EU.

Consumer demand for recyclable and environmentally friendly packaging, coupled with the need for fresh and chilled food products, promotes a significant uptake of these lidding films.

U.K. PET Lidding Films Market

The U.K. market in 2025 reached USD 42.95 million, representing approximately 3.02% of global revenues.

Germany PET Lidding Films Market

Germany’s market reached approximately USD 81.21 million in 2025, equivalent to around 5.71% of global market sales.

Asia Pacific

Asia Pacific reached USD 312.56 million in 2025 and secured the position of the second-largest region in the market. In the region, India and China both reached USD 66.32 million and USD 104.67 million, respectively, in 2025. The Asia Pacific market is propelled by swift urbanization, increasing disposable incomes, and heightened demand for packaged foods. The expansion of retail penetration, growth in foodservice, and preference for convenient, ready-to-eat meals are enhancing the adoption of these films. Furthermore, awareness of sustainability is progressively impacting packaging decisions in developed Asia Pacific nations.

Japan PET Lidding Films Market

The Japanese market in 2025 reached around USD 52.45 million, accounting for roughly 3.69% of global revenues. In Japan, convenience stores and the ready-to-eat food industry serve as significant catalysts for growth. Consumers place a high value on fresh, safe, and visually attractive packaged foods, leading to a heightened demand for high-barrier PET lidding films. Innovations in packaging that emphasize shelf-life extension and convenience further promote the adoption of this segment within the country.

China PET Lidding Films Market

China’s market has been projected to be one of the largest globally, with 2025 revenues reaching around USD 104.67 million, representing roughly 7.36% of global sales.

India PET Lidding Films Market

The Indian market in 2025 reached around USD 66.32 million, accounting for roughly 4.66% of global market revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of USD 176.19 million in 2025. The regional market is driven by a growing consumption of packaged food and urbanization. The expansion of contemporary retail chains and foodservice establishments stimulates the demand for ready-to-eat meals and chilled products.

In the Middle East & Africa, South Africa reached USD 34.33 million in 2025. The growth of the market in MEA is bolstered by increase in foodservice, popularity of packaged convenience foods, and expansion of modern retail.

Saudi Arabia PET Lidding Films Market

The Saudi Arabian market is valued approximately USD 51.02 million by 2025, accounting for roughly 3.59% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Launch and Acquisitions by Key Players to Propel Market Progress

The global market has a semi-consolidated structure, with prominent players including Klöckner Pentaplast, Constantia Flexibles, and Graphic Packaging International, LLC. The significant market shares of these companies are due to numerous strategic initiatives, including collaborations among operating entities to advance research.

- For instance, in August 2025, Constantia Flexibles participates in FACHPACK 2025 after a phase of strategic investments, technological progress, and portfolio growth, solidifying its status in premium flexible packaging and leadership in sustainability. Earlier in 2025, Constantia Flexibles finalized the acquisition of Aluflexpack, a prominent European provider of tailored flexible packaging solutions. This strategic decision considerably enhances Constantia Flexibles’ presence in high-value sectors, especially within the food and pharmaceutical markets, while also improving its technological expertise and regional manufacturing capabilities.

Other notable players in the global market include Amcor plc, Sealed Air, and KM Packaging Services Ltd. These companies are expected to prioritize new product launches and collaborations to increase their global market shares during the forecast period.

LIST OF KEY PET LIDDING FILMS COMPANIES PROFILED

- Klöckner Pentaplast (U.K.)

- Constantia Flexibles (Austria)

- Graphic Packaging International, LLC (U.S.)

- Amcor plc (Switzerland)

- Sealed Air (U.S.)

- KM Packaging Services Ltd. (U.K.)

- WINPAK Ltd. (Canada)

- Cosmo Films Ltd (India)

- PLASTOPIL (Israel)

- Coveris Holdings (Austria)

- Uniflex Packaging (Belarus)

- FLAIR Flexible Packaging Corporation (Canada)

- Tilak Polypack Pvt. Ltd. (India)

- TCL Packaging (U.K.)

- Mitsubishi Polyester Film GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Cosmo Films broadened its flexible packaging offerings with a new selection of BOPP, CPP, and BOPET-based films designed specifically for pet food packaging. This launch features a new high-heat resistant TR-BOPP film, as well as enhanced barrier and lidding films, reinforcing the company’s dedication to providing next-generation, food-safe packaging.

- June 2025: KM Packaging announced the launch of K-Peel 4GX, a new specification for mono PET lidding film. K-Peel 4GX features a low seal initiation point and can seal effectively even in the presence of contamination. Clean peels can be achieved at temperatures as low as 110°C with a dwell time of just 0.3 seconds. K-Peel 4GX provides a clean peel suitable for ambient, chilled, or frozen applications and is also ovenable.

- April 2025: Camvac introduced a 60% PCR barrier lidding film. The latest commercial innovation from Camvac is a post-consumer recycled (PCR) grade PET barrier film called ExtraPET PCR. This new product expands Camvac's current ExtraPET film lineup, which is mainly utilized in the food and converter sectors, and aligns with Camvac's expanding Camvert collection of sustainable packaging

- February 2024: The establishment of the new polyester film production line at Mitsubishi Polyester Film GmbH, which has a capacity of 27,000 tons of HOSTAPHAN PET films, has commenced in the Kalle Albert industrial zone located in Wiesbaden. At present, 4000m3 of concrete is being utilized to pour the floor slab. The completion of this significant project, which involves an investment of approximately USD 143 million, is proceeding as planned and is expected to be finalized by the conclusion of the first quarter of 2025.

- October 2022: KM Packaging introduced a new range of sustainable lidding films to align with APCO's national objectives. These lidding products are categorized into four sections, encompassing KM's already extensive K-Peel, K-Seal, K-Foil, and K-Reseal lidding lines. Additionally, this collection of sustainable lidding film solutions is being offered in various other regions, including Europe, where CEFLEX has primarily concentrated its efforts and promoted the adoption of PE and PP-based solutions to attain circularity in flexible packaging.

REPORT COVERAGE

The PET lidding films market analysis includes a comprehensive study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, as well as their prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.42% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Type, Product Type, End-use Industry, and Region |

| By Type |

|

| By Product Type |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1,422.00 million in 2025 and is projected to reach USD 2,471.14 million by 2034.

In 2025, the market value of North America stood at USD 455.75 million.

The market is expected to grow at a CAGR of 6.42% over the forecast period of 2026-2034.

By type, the high-barrier lidding films segment is expected to lead the market.

Rising demand for convenience and fresh food packaging is propelling market growth.

Klockner Pentaplast, Constantia Flexibles, and Graphic Packaging International, LLC are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us