PET Packaging Market Size, Share & Industry Analysis, By Packaging Type (Rigid Packaging and Flexible Packaging), By Product Type (Bottles & Jars, Caps & Closures, Trays & Clamshells, Bags & Pouches, Films & Wraps, Sachets & Stick Packs, and Cans & Containers), By End-user (Food & Beverage, Pharmaceutical, Personal Care & Cosmetics, Automotive, Electricals & Electronics, Chemicals, Building & Construction, Agriculture, Household, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

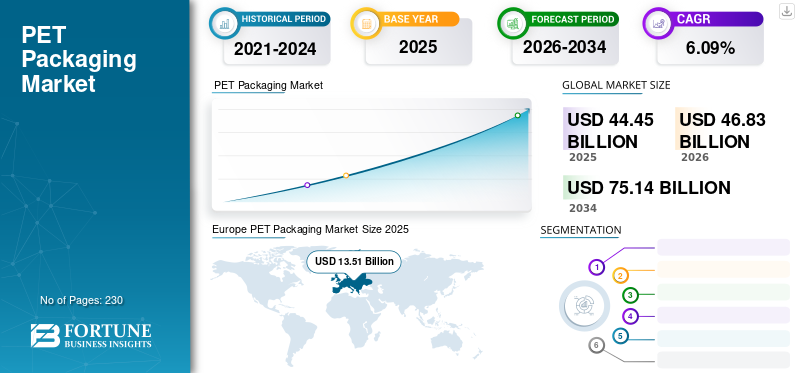

The global PET packaging market size was valued at USD 44.45 billion in 2025 and is projected to grow from USD 46.83 billion in 2026 to USD 75.14 billion by 2034, exhibiting a CAGR of 6.09% during the forecast period. Europe dominated the PET packaging market with a market share of 30.39% in 2025.

Compared with other materials, Polyethylene Terephthalate (PET) has excellent flexibility and toughness, enabling it to be used in highly lightweight packaging, saving raw materials, and natural resources. In other words, PET's exceptional capacity-to-weight ratio is crucial to its energy efficiency and climate change mitigation. This reduces packaging production, the transportation of packaged goods, and the loss of packaged goods caused by their use. As a highly stable and inert polymer, PET offers excellent barrier properties, protecting it from the external environment without interfering with the packaged product. Packaging made of PET is perfect for food and beverage, as it is safe and increases shelf-life, reducing food waste and the significant environmental impact of food production. Polyethylene terephthalate packaging meets stringent food safety criteria and is an excellent form of packaging. It can be formed into a massive range of shapes, adapting well to different packaging designs with high levels of complexity, emphasizing corporate identity, or lending a distinctive shelf presence to the product it contains. It offers consumers convenience through its strength, lightweight, transparency, and safety.

The COVID-19 pandemic adversely impacted the market. The demand for groceries, restaurants and food service establishments declined due to the closure of public places. However, the demand for non-food luxury packaging and the end products, such as containers, bottles & jars, and trays is boosting the market growth.

Download Free sample to learn more about this report.

Global PET Packaging Market Overview

Market Size & Forecast:

- 2025 Market Size: USD 44.45 billion

- 2026 Market Size: USD 46.83 billion

- 2034 Forecast Market Size: USD 75.14 billion

- CAGR: 6.09% (2026–2034)

Market Share:

- Europe dominated with 30.39% market share in 2025

Regional Insights:

- North America: Largest regional market, led by the U.S. with strong plastic industry growth and recyclable plastic adoption

- Europe: Significant market with rising ready-to-eat food trends and investment in chemical recycling technologies

- Asia Pacific: Substantial market share, led by China’s high PET bottle consumption and Southeast Asia’s growing beverage demand

- Latin America: Increasing bottled water consumption driving PET packaging demand (e.g., Mexico’s large bottled water market)

PET Packaging Market Trends

Growing Awareness of Eco-friendly Products is Driving the Growth of the Market

Manufacturers face substantial challenges regarding sustainability while using plastic material for packaging products of consumer goods. However, developing plastic material with its recycling streams helps neutralize sustainability issues. In Europe, recycling rates have been improving gradually. PET is characterized by extreme lightness compared to other materials used for bottling and, more specifically, for packaging.

The European Union is leading the world's governments in accepting and adopting recycled materials to ensure 100% recyclable plastic by 2030. The EU recycling targets require the creation of 12 million tons of end markets for recycled plastic by 2025 to reach their halfway point.

The raw material for bioplastics is often renewable and biodegradable such as starch, proteins, and polylactic acid (PLA). Bioplastics are being used in commercial markets across the globe today due to the growth of available products and suppliers in recent years. All packaging plastics can be recycled at the highest rate for polyethylene terephthalate (PET). In addition to its crude oil-based components, bio-based alternatives can be used to replace some of its petroleum-based components.

PET made from bio-based materials is an efficient, economical, and effective plastic packaging solution, according to European Bioplastics. PET packaging material is elastic and contains solid fibers, making it suitable for use with containers, rigid bottles, and films. A Nestlé researcher elaborates on how the company is using 100% renewable plastic bottles to package mineral water. Due to its recyclable nature and better environmental performance, PET is being used.

Download Free sample to learn more about this report.

PET Packaging Market Growth Factors

Food and Beverage Sector Expansion Along with Pharmaceutical Growth is Boosting Sales

Globalization has led key players in the food & beverage and pharmaceutical industries to develop unique packaging solutions that cater to consumers' needs. It is expected to grow in demand due to an increasing preference for practical and easy-to-carry solutions for protecting food during transportation. Moreover, plastic packaging is being designed for food & beverage products to ensure their safe handling. Over 90% of used PET packaging in India is recycled, according to the PET Packaging Association for Clean Environment. The constant expansion of the food & beverage industry has made it necessary for market players to create unique packaging solutions to cater to the requirements of present-day consumers. Increasing preferences for easy-to-carry food & beverage packaging are driving the sales. Single-serve PET bottles now weigh less than 10 grams yet are strong enough to hold 50 times their weight in water. In the past 10 years, the average weight of a 0.5-liter PET bottle has also decreased by 48% due to the "lightweight" characteristic of PET containers.

Increasing Customization for Brand Differentiation is Propelling the Market Growth

Customized and different-sized product packaging has become popular among consumers. The manufacturers incorporate multiple items into a single package, increasing visibility and creating a unique presence on the shelf. With the help of interactive packaging of products, the consumers get attracted. Due to PET's unique properties, it is rapidly becoming the world's preferred food and beverage packaging material. Like glass, it is a solid and inert material that does not react with food, is resistant to microbial attack, and does not biodegrade. But unlike glass, PET is lightweight, easy to carry, efficient, and shatterproof.

RESTRAINING FACTORS

Ban of Single-use Plastic by Government is Expected to Hamper the Market Growth

As per the research, India banned the import of plastic waste in 2019 to promote the management of locally generated plastic waste. In some countries, the ban on single-use plastic will somehow hinder PET packaging sales and demand during the forecast period. Manufacturers in the packaging market use materials, such as paper, molded fiber, and others, considered biodegradable. Instability in raw material prices is restraining the PET packaging market. The cost of crude oil will affect the price of PET as PET resin is manufactured from crude oil. These can hamper the PET packaging market growth in the coming years.

PET Packaging Market Segmentation Analysis

By Packaging Type Analysis

Rigid Packaging Dominates the Market Due to High Consumption in the Food & Beverage Industry

The rigid packaging segment is projected to dominate the market, accounting for a 54.07% share in 2026. The extensive usage of rigid packaging in the food & beverage industry is due to its lightweight, good stability, barrier properties, and durability. The packaging type includes rigid packaging and flexible packaging. It is owing to widespread use and growing demand from various end-use industries for manufacturing products such as bottles, jars, and containers.

By Product Type Analysis

Demand for PET Flexible Packaging as a Sustainable Solution to Gain Momentum

Based on product type, the market is segmented into bottles & jars, caps & closures, trays & clamshells, bags & pouches, films & wraps, sachets & stick packs, and cans & containers. In terms of market share, the films & wraps segment holds a dominant share of the global market due to the rising usage of flexible packaging in online delivery. The films & wraps segment is expected to lead the market by product type, contributing 23.08% of the total market share in 2026.

To know how our report can help streamline your business, Speak to Analyst

By End-user Analysis

Demand for PET Containers in the Food & Beverage Industry to Gain Momentum

The food & beverages end-use industry segment dominated the global PET packaging market with a market share of 31.05% in 2026. Prepared meals mainly lead the food & beverage packaging sector due to easy portability, long shelf life, and easy preparation. Prepared food consists of frozen meals, snacks, drinks, and more. Food generally requires less preparation and is cooked in warm, usable containers. The increasing demand due to the busy lifestyle of consumers and the elderly has led to the widespread use of convenience foods. Essential features that consumers look for in convenience foods are nutritional value, ease of packaging, product appeal, and product safety. The food & beverages segment is anticipated to account for 31.05% of the market share in 2026.

REGIONAL INSIGHTS

Europe PET Packaging Market Size 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The market analysis has been done across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The North America region is likely to dominate the global PET packaging market share over the forecast period. In North America, the U.S. is projected to witness a surge in demand for plastic packaging. As per Plastics Industry Association (PLASTICS), the U.S. plastics industry remained one of the economy’s largest sectors and continued to grow in 2020. The U.S. market is projected to reach USD 10.24 billion by 2026. The North America region captured 23.87% of the global market in 2025, generating USD 10.61 billion in revenue, and is projected to reach USD 10.98 billion in 2026.

Europe

The UK market is projected to reach USD 1.80 billion by 2026, while the Germany market is projected to reach USD 2.16 billion by 2026. Furthermore, due to the expanding plastic industry, adopting recyclable plastic packaging such as PET is boosting sales. In Europe, the emerging trend of ready-to-eat food consumption has increased the demand for product packaging such as single-serve and small-sized PET. According to PLASTICS EUROPE, in 2020, the turnover of the European plastic industry was USD 335 billion, which showed a slight decrease compared to the previous year, mainly due to the impact of COVID-19 crisis on the majority of customer industries. In 2021, plastic producers planned significant investments in chemical recycling technologies. Europe maintained a strong presence in the global market, reaching USD 13.51 billion in 2025, accounting for 30.39% share, and is expected to reach USD 14.26 billion in 2026.

Asia Pacific

The Asia Pacific region holds a significant market share of PET packaging. As per Plastic Packaging in Southeast Asia and China, PET bottles' total annual household packaging consumption is 5,474,000 tons in China. The rising consumption of beverages in Latin America is boosting the demand for PET packaging. In Mexico, the consumption of bottled water market was 9,959 million gallons in 2020. The Japan market is projected to reach USD 1.51 billion by 2026, the China market is projected to reach USD 2.66 billion by 2026, and the India market is projected to reach USD 2.17 billion by 2026. In 2025, Asia Pacific generated USD 13.7 billion, contributing 30.83% to global market revenue, and is projected to grow to USD 14.67 billion in 2026.

Middle East & Africa

Middle East & Africa recorded a market size of USD 1.45 billion in 2025, capturing 3.27% of the global market share, and is projected to reach USD 1.53 billion in 2026.

Latin America

The Latin America market generated USD 5.17 billion in 2025, representing 11.64% of the global market landscape, and is expected to reach USD 5.39 billion in 2026.

List of Key Companies in PET Packaging Market

Key Participants in the Market Witnessing Significant Growth Opportunities

The global market is highly fragmented and competitive. In terms of market share, a few major players dominate the market by offering innovative packaging in the packaging industry. These major players in the market are constantly focusing on expanding their customer base across the regions.

Major players operating in the market include Berry Global, Amcor, Sonoco Products Company, Huhtamaki, and Gerresheimer. Significant companies constitute more than 50% of the market, and many regional and local players dominate the remaining market. Numerous other players operating in the industry are focused on delivering advanced packaging solutions.

List of Key Companies Profiled:

- Berry Global (U.S.)

- Amcor (Australia)

- Sonoco Products Company (U.S.)

- Huhtamaki (Finland)

- Gerresheimer (Germany)

- Klöckner Pentaplast (U.S.)

- Schur Flexibles Group (Austria)

- Clondalkin Flexible Packaging (Amsterdam)

- Constantia Flexibles (Austria)

- Novolex Holdings, Inc. (U.S.)

- Dunmore (U.S.)

- Printex Transparent Packaging (U.S.)

- MD Group (U.K.)

- PDG PLASTIQUES (France)

KEY INDUSTRY DEVELOPMENTS:

- May 2022 - A new line of 100% PET Processor Trays has been launched by Tekklex Consumer Products, which addresses common packaging challenges faced by poultry processors, particularly higher-end products labeled organic, non-GMO, or sustainably sourced. TekniPlex's new trays are made from 100% PET and contain up to 50% post-industrial recycled content. Furthermore, they are 100% recyclable, appealing to consumers' heightened sustainability awareness.

- May 2022 –Packaging solutions provider Alpla Group, in partnership with Austrian mineral water bottler Vöslauer, developed a new returnable PET bottle that reduces carbon emissions by about 30%. The fully-recyclable PET mono-material bottle weighs 55 grams and is about 90% lighter than the returnable glass.

- April 2022 – Sidel launched PressureSAFE, a PET aerosol container for home and personal care products that is approved for recycling in traditional PET streams and claims to have a lower carbon footprint than aluminum alternatives.

- December 2021 - LanzaTech announced that Migros, Switzerland's largest retailer, is producing the world's first PET bottle made from captured carbon dioxide emissions that would otherwise enter the atmosphere as carbon dioxide. Polyethylene terephthalate is a polyester that is molded into plastic bottles and containers to package food and beverages, personal care products, and many other consumer products.

- February 2020 - Orbital by Quinn is a food packaging solution produced using 100% recycled PET material, eliminating the non-recycled plastic found in most PET food packaging. Orbital is certified by the European Food Safety Authority as entirely suitable for food packaging applications.

REPORT COVERAGE

An Infographic Representation of PET Packaging Market

View Full Infographic

View Full InfographicTo get information on various segments, share your queries with us

The research report presents a comprehensive industry assessment by offering valuable insights, facts, industry-related information, and historical data. Several methodologies and approaches are adopted to make meaningful assumptions and views to formulate the research report. Furthermore, the report covers a detailed analysis of market segments, including packaging type, product type, end-user, and regions, helping our readers get a comprehensive global industry overview.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

|

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Packaging Type

|

|

By Product Type

|

|

|

By End-user

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights study shows that the global market was valued at USD 44.45 billion in 2025.

The global market is projected to grow at a CAGR of 6.09% over the forecast period.

The market size of Europe stood at USD 13.51 billion in 2025.

Based on packaging type, the rigid packaging segment holds the dominating share in the global market.

The global market size is expected to reach USD 75.14 billion by 2034.

Increasing adoption of PET packaging across the pharmaceutical and food & beverage sectors is expected to drive sales in the market.

The top players in the market are Berry Global, Amcor, Sonoco Products Company, Huhtamaki, Gerresheimer, Klöckner Pentaplast, Schur Flexibles Group, Clondalkin Flexible Packaging, Constantia Flexibles, and Novolex Holdings, Inc.

- 2021-2034

- 2025

- 2021-2024

- 230

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us