PET Scanners Market Size, Share & Industry Analysis By Product Type (Standalone PET Scanners, PET/CT, and PET/MRI), By Mobility (Fixed and Portable), By Application (Cardiology, Oncology, Orthopedics, Gynecology, Neurology, and Others), By End User (Hospitals, Specialty Clinics, Diagnostic Imaging Centers, and Others), and Regional Forecast, 2026-2034

PET Scanners Market Size and Future Outlook

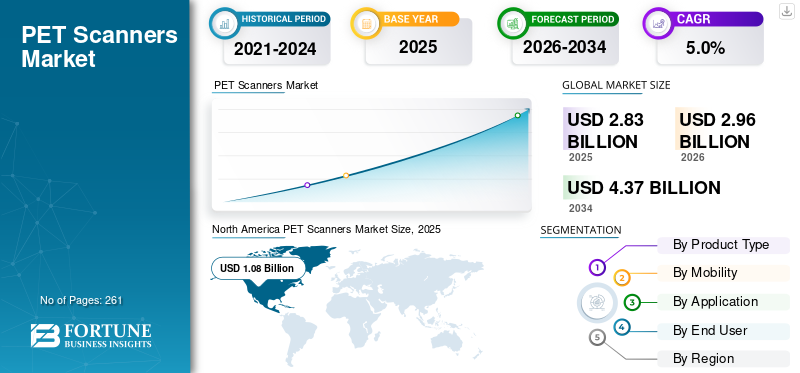

The global PET scanners market size was valued at USD 2.83 billion in 2025 and is projected to grow from USD 2.96 billion in 2026 to USD 4.37 billion by 2034, exhibiting a CAGR of 5.0% during the forecast period. North America dominated the PET scanners market with a market share of 38.16% in 2025.

PET scanners are medical imaging devices that produce 3D images of metabolic, functional, and chemical activity inside the body. The growing prevalence of chronic disorders, increasing diagnostic procedure volumes, growing early detection of diseases, and the development of healthcare infrastructure are resulting in a rising adoption rate of these systems in the market. The growing aging population is further supporting the demand for innovative medical imaging devices in the market.

- For instance, according to the 2025 data published by the National Cancer Institute (NCI), an estimated 2.0 million new cancer cases were projected to occur in the U.S.

Additionally, the increasing incorporation of technological advancements in these devices among the major players, such as GE Healthcare and Siemens Healthineers AG, among others, is further contributing to the demand for these devices in the market.

Download Free sample to learn more about this report.

PET Scanners Market Key Takeaways

- 2025 Market Size: USD 2.83 billion

- 2026 Market Size: USD 2.96 billion

- 2034 Forecast Market Size: USD 4.37 billion

- CAGR: 5.0% from 2026–2034

- North America dominated the PET scanners market with a 38.16% share in 2025.

- The fixed segment accounted for a 93.1% market share in 2025.

- The oncology segment accounted for a 71.4% market share in 2025.

North America

North America held the dominant share in 2025, valued at USD 1.08 billion.

Asia Pacific

Asia Pacific is projected to reach USD 0.73 billion by 2026.

Europe

Europe is projected to reach USD 0.81 billion by 2026.

U.S.

The market projected to reach USD 1.04 billion by 2026.

Japan

The market projected to reach USD 0.20 billion by 2026.

Read More

PET Scanners Market Trends

Increasing Demand for Technological Advancements in Products to Fuel Demand

There is an increasing demand for technologically advanced products of higher strengths, including PET/CT, PET/MRI, among others. Traditional scanning has been using standalone PET scanners; however, with the advent of technology, hybrid models are being utilized across healthcare settings.

The integration of these imaging technologies is crucial in the diagnosis of chronic disorders, including heart diseases, neurological disorders, and others. The growing technological advancements in these devices provide accuracy and resolution, minimizing the scanning time, and enhancing patient outcomes by producing high-quality images among the patient population.

- For instance, in November 2023, Siemens Healthineers AG received FDA approval for the Biograph Vision X, a positron emission tomography/computed tomography scanner (PET/CT).

Market Dynamics

Market Drivers

Increasing Prevalence of Chronic Disorders to Fuel Market Growth

The rising prevalence of chronic conditions, such as cardiovascular disorders, cancer, among others, is anticipated to increase the diagnosis and treatment rate among patients globally. The growing aging population is another crucial factor resulting in the rising patient population suffering from these disorders.

- For instance, according to 2024 statistics published by the Centers for Disease Control & Prevention (CDC), about 1 in 20 adults has coronary artery disease in the U.S.

This, coupled with rising technological advancements in the products and improving healthcare access, is further supporting the adoption rate of these devices in the market. Therefore, the factors above, coupled with the growing focus of key players on introducing research and development activities to launch innovative products, are anticipated to boost the adoption rate of these devices, thereby supporting the global market size.

Download Free sample to learn more about this report.

Other Prominent Drivers

- Growth of radiopharmaceuticals and theranostics is increasing PET utilization and repeat scans.

Market Restraints

High Cost Associated with these Devices to Hamper Market Growth

There is a growing demand for imaging medical devices, including PET/CT scanners, PET/MRI scanners, and others in healthcare facilities. However, one of the crucial factors that hampers the adoption of these systems is the high cost associated with these devices. The upfront cost associated with the purchase and implementation of imaging devices is very high, owing to the addition of developing costs, distributors’ margins, and service costs.

Additionally, the growing advancements in these devices among the major players are resulting in growing prices, further making it challenging for small hospitals and clinics to adopt these devices, thereby hindering the market growth significantly, particularly in the emerging countries.

- For instance, according to the statistics published by PatientImage, the cost of a new PET/CT scanner ranges from USD 0.5 million to over USD 5.0 million.

Market Opportunities

Expansion of Applications for PET Scanners to Create an Opportunity

There is an increasing acceptance of these products in several fields of medicine. A growing number of medical specialists are adopting these systems due to the diverse range of medical applications associated with these devices. According to several studies, molecular imaging, which includes PET scanners, offers the ability to accurately diagnose the biological response to disease treatment in individual patients over time.

Furthermore, imaging procedures are becoming much faster due to the adoption of advanced technology in these systems. Molecular Point-Of-Care (POC) enables more accurate and faster diagnosis by providing quick detection and infection control among the patient population.

- According to a 2021 survey published by the National Center for Biotechnology Information (NCBI), approximately 93% of respondents believed that POCT could enhance their care in the U.S.

Market Challenges

Limited Diagnostic Centers in Developing Countries to Hinder Market Growth

There is a growing demand for diagnostic procedures among the patient population. However, limited availability of technologically advanced products, limited healthcare expenditure, coupled with an inadequate reimbursement framework, especially in emerging countries, are resulting in limited access to healthcare facilities among the patient population.

Additionally, a limited number of clinical facilities and limited professionals, among others, are some of the crucial factors, resulting in the delayed diagnostic procedures among the patient population, particularly in emerging countries, including Brazil, China, among others.

- For instance, according to 2025 data published by the International Trade Administration (ITA), it was reported that the healthcare expenditure is USD 135.0 billion in Brazil.

Other Prominent Challenges

- The short half-life of many PET tracers hampers the market growth.

SEGMENTATION ANALYSIS

By Product Type

Increasing Number of Product Launches Led to PET/CT Segmental Dominance

Based on the product type, the market is classified into standalone PET scanners, PET/CT, and PET/MRI.

The PET/CT segment held the largest revenue share in 2025. The growth is due to the growing prevalence of chronic conditions among the patient population, resulting in an increasing number of diagnostic procedures globally. This, along with the rising emphasis of key players on launching novel products, is further expected to contribute to the global PET scanners market growth.

- For instance, in November 2025, GE HealthCare received CE approval for its Omni 128cm total body PET/CT, a next-generation imaging product designed to advance precision care.

The PET/MRI segment is expected to grow at a CAGR of 5.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Mobility

Growing Product Launches Led to Dominance of Fixed Segment

Based on mobility, the market is segmented into fixed and portable.

The fixed segment dominated the global market in 2025. By mobility, the fixed segment held the share of 93.1% in 2025. The growth is due to the growing prevalence of chronic conditions such as cancer and others, resulting in a rising demand for fixed products, thereby contributing to the adoption rate of these products in the market.

- For instance, in January 2026, Siemens Healthineers AG received U.S. FDA approval for Siemens Healthineers’ Biograph One, a positron emission tomography/magnetic resonance (PET/MR) scanner with an aim to provide advanced devices.

The segment of portable is set to flourish with a growth rate of 5.9% across the forecast period.

By Application

Growing Prevalence of Cancer Led to Dominance of Segment

Based on application, the market is segmented into cardiology, oncology, orthopedics, gynecology, neurology, and others.

The oncology segment dominated the global market in 2025. By application, the oncology segment accounted for 71.4% in 2025. The growth is due to the increasing prevalence of chronic conditions, including various types of cancer, among others, resulting in a growing number of diagnostic procedures globally, thereby contributing to the adoption rate of these devices in the market.

- For instance, according to the data published by the Centers for Disease Control & Prevention (CDC), it was reported that about 218,893 new lung cancer cases were reported in the U.S. in 2022.

The segment of neurology is set to flourish with a growth rate of 6.5% across the forecast period.

By End-user

Increasing Number of Hospitals Led to Segmental Dominance

Based on end user, the market is segmented into hospitals, specialty clinics, diagnostic imaging centers, and others.

The hospitals segment dominated the market in 2025. The increasing prevalence of chronic disorders, rising number of diagnostic procedures in hospitals, increasing number of healthcare settings, such as hospitals, among others, are some of the crucial factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold a 61.3% share in 2026.

- For instance, according to 2025 data published by Statistisches Bundesamt, there are about 1,874 hospitals in Germany.

In addition, diagnostic imaging centers’ end users are projected to grow at a 5.4% CAGR during the forecast period.

PET Scanners Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America PET Scanners Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 1.05 billion, and also took the leading share in 2025 with USD 1.08 billion. The increasing prevalence of chronic disorders, high healthcare spending, and adoption of advanced imaging, among others, are some of the factors contributing to the growth of the segment in the market.

- For instance, according to 2022 data published by the Alzheimer’s Association, over 7 million Americans are living with Alzheimer’s disease.

U.S. PET Scanners Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.04 billion in 2026, accounting for roughly 35.0% of global sales.

Europe

Europe is projected to record a growth rate of 3.6% in the coming years, which is the second highest among all regions, and reach a valuation of USD 0.81 billion by 2026. The strong installed base and increasing theranostics programs in major European countries are anticipated to support the market growth.

U.K. PET Scanners Market

The U.K. market in 2026 is estimated at around USD 0.14 billion, representing roughly 4.7% of global revenues.

Germany PET Scanners Market

Germany’s market size is projected to reach approximately USD 0.18 billion in 2026, equivalent to around 6.2% of global sales.

Asia Pacific

The Asia Pacific market is estimated to reach USD 0.73 billion in 2026 and secure the position of the third-largest region. The fastest installation growth is driven by China, Japan, and India’s expanding oncology imaging infrastructure and adoption of advanced diagnostics, further anticipated to support the development of the market. In the region, India and China are both estimated to reach USD 0.10 billion and USD 0.30 billion, respectively, in 2026.

Japan PET Scanners Market

The Japan market in 2026 is estimated at around USD 0.20 billion, accounting for roughly 6.6% of global revenues. Japan has historically reported a relatively high prevalence of various types of cancer, with a growing number of such scans among the patient population.

China PET Scanners Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.30 billion, representing roughly 10.0% of global sales.

India PET Scanners Market

The Indian market size in 2026 is estimated at around USD 0.10 billion, accounting for roughly 3.2% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.17 billion in 2026. The growth is due to growing installations for such scanners across healthcare settings. The Middle East & Africa are also anticipated to grow due to increasing medical tourism and rising healthcare access in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.06 billion in 2026.

South Africa PET Scanners Market

The South Africa market is projected to reach around USD 0.03 billion in 2026, representing roughly 1.1% of global revenues.

Competitive Landscape

Key Industry Players

Rising Strategic Initiatives Among Key Players to Support Market Dominance of these Companies

A strong device portfolio and continuous focus on strategic initiatives globally are key factors supporting the leadership of major companies. In 2025, leading players such as GE Healthcare and Siemens Healthineers AG hold a significant position in the market. Additionally, the increasing emphasis on inorganic growth strategies by key companies to expand the production capacity is expected to further strengthen their global PET scanners market share.

- For example, in October 2024, GE HealthCare began manufacturing its all-in-one Omni Legend PET/CT scanner at a new production facility in Waukesha, Wisconsin, with an aim to strengthen its presence in the U.S. market.

Other prominent companies, including Koninklijke Philips N.V., and others, are also expanding their presence in the market. Their growth is mainly driven by increased investments in research and development activities aimed at introducing new advanced devices among other players and strengthening their competitive market position.

List of Key PET Scanners Companies Profiled

- GE Healthcare (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Canon Medical Systems Corporation (Japan)

- United Imaging Healthcare Co., Ltd. (China)

- Bruker (U.S.)

- Mediso Ltd. (Hungary)

- MinFound Medical Systems Co., Ltd (China)

- Shimadzu Corporation (Japan)

- Neusoft Medical Systems Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Yale Positron Emission Tomography (PET) Center is studying an ultra-high-performance brain-dedicated scanner called the NeuroEXPLORER (NX) to advance brain PET imaging.

- October 2025: GE Healthcare collaborated with Erasmus MC University Medical Center (Erasmus MC) to evaluate a next-generation total body positron emission tomography/computed tomography (PET/CT) technology. This helped the company to increase its brand presence.

- September 2024: Shimadzu Corporation expanded its subsidiary for analytical and measuring instruments and medical systems in Mexico. This helped the company to increase its brand presence in the LATAM region.

- July 2024: Positron Corporation launched PET & PET-CT imaging devices, presenting its new NeuSight PET-CT 3D 64 slice scanner, to increase its presence in North American Markets.

- June 2024: Siemens Healthineers AG received U.S. FDA approval for the Biograph Trinion positron emission tomography/computed tomography (PET/CT) system at the 2024 Society of Nuclear Medicine and Molecular Imaging (SNMMI) Annual Meeting.

- June 2024: CANON MEDICAL SYSTEMS CORPORATION collaborated with Hermes Medical Solutions to focus on precision medicine with their PET/CT medical imaging products.

- June 2023: United Imaging, a player manufacturing advanced medical imaging and radiotherapy equipment launched next generation PET/CT systems uMI Panorama, with an aim to strengthen its product portfolio.

REPORT COVERAGE

The report provides a detailed global PET scanners market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, mobility, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Mobility, Application, End User, and Region |

| By Product Type |

|

| By Mobility |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 2.83 billion in 2025 and is projected to reach USD 4.37 billion by 2034.

In 2025, the market value stood at USD 1.08 billion.

Growing at a CAGR of 5.0%, the market will exhibit steady growth over the forecast period.

By product type, the PET/CT segment is the leading segment in this market.

The introduction of innovative PET scanners is one of the major factors driving the markets growth.

GE Healthcare and Siemens Healthineers AG are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic disorders, the increasing number of diagnostic procedures, among others, are some of the crucial factors anticipated to boost the adoption of these products globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us