PFAS-Free Food Packaging Market Size, Share & Industry Analysis, By Material (Paper & Paperboard, Bioplastics and Bio-Derived Polymers, Aluminum, and Others), By Product Type (Films & Wraps, Plates & Bowls, Trays, Bags & Pouches, Cups & Lids, and Others), By End Use (Packaged Food Manufacturers, Retail & Convenience Stores, Restaurants & Fast Food Outlets, and Others), and Regional Forecast, 2026-2034

PFAS-Free Food Packaging Market Size and Future Outlook

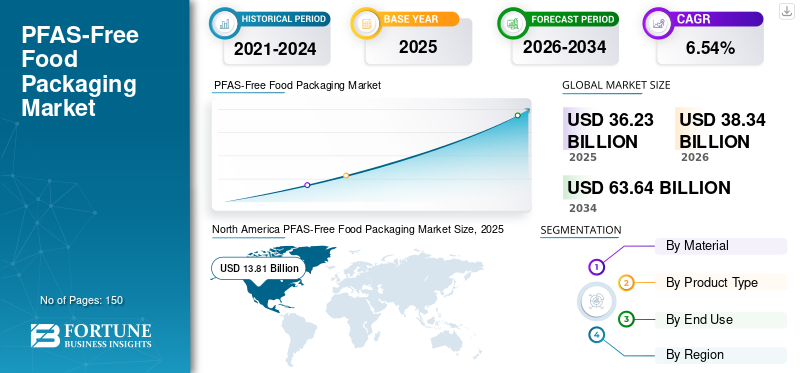

The global PFAS-free food packaging market size was valued at USD 36.23 billion in 2025. The market is projected to grow from USD 38.34 billion in 2026 to USD 63.64 billion by 2034, exhibiting a CAGR of 6.54% during the forecast period. North America dominated the pfas-free food packaging market with a market share of 38.12% in 2025

PFAS-free food packaging encompasses materials and solutions intended for the storage, transportation, and consumption of food. These materials are produced without the intentional inclusion of PFAS (per- and polyfluoroalkyl substances). Increasing regulatory restrictions on PFAS in food-contact materials, along with heightened consumer awareness of health and environmental hazards, are driving demand for safer alternatives.

Furthermore, many key industry players, such as Huhtamaki, Genpak, and Dart Container Corporation, operating in the market, are focusing on developing innovative products and conducting R&D, and contributing to the global market share.

Download Free sample to learn more about this report.

PFAS-FREE FOOD PACKAGING MARKET TRENDS

Rapid Adoption of Bio-Based Barrier Coatings is an Emerging Trend in Market

A significant trend in the global PFAS-free food packaging sector is the increasing use of bio-based and mineral barrier coatings as substitutes for fluorinated chemicals conventionally used for grease and moisture resistance. Packaging manufacturers are progressively embracing water-based dispersions, plant-derived polymers, and clay or silica coatings to ensure functionality in foodservice packaging. This transition is motivated by the need to provide oil resistance in applications such as fast-food wraps, bakery bags, and takeaway containers without using PFAS. Technological innovations are enhancing coating performance, enabling recyclable, compostable paper packaging with similar barrier properties. As sustainability objectives become more pressing in the food industry, the development of high-performance PFAS-free coatings is emerging as a key focus of innovation for packaging producers.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Global Regulatory Restrictions on PFAS are Driving Market Growth

A key factor driving the PFAS-free food packaging market growth is the increasing stringency of regulations governing PFAS in food-contact materials. Governments and regulatory bodies are progressively limiting the use of fluorinated compounds due to concerns about their environmental persistence and potential health effects. Numerous regions are implementing bans or imposing stringent restrictions on PFAS in paper and fiber food packaging, compelling foodservice providers and packaging manufacturers to shift toward safer alternatives. As compliance obligations grow globally, demand for certified PFAS-free packaging materials is expected to rise significantly.

MARKET RESTRAINTS

Higher Production Costs Compared to Conventional Packaging Impede Market Growth

A significant limitation in the PFAS-free food packaging sector is the higher cost associated with alternative barrier technologies. Historically, PFAS chemicals have offered a cost-efficient solution for grease and water resistance in food packaging, especially in paper-based materials. The substitution of these chemicals typically requires advanced coatings, multilayer structures, or specialized raw materials, which can increase manufacturing costs. Furthermore, the transition may require modifications to equipment, sourcing from new suppliers, and conducting tests to ensure compliance with food safety and performance standards. For small to mid-sized packaging manufacturers, these additional expenditures can hinder the pace of adoption. Additionally, the cost sensitivity prevalent among foodservice operators and retailers further restricts the immediate large-scale replacement of traditional PFAS-containing packaging.

MARKET OPPORTUNITIES

Expansion of Sustainable Foodservice Packaging Offers Future Growth Opportunities

The swift growth of sustainable foodservice packaging presents a significant opportunity for PFAS-free solutions. Quick-service restaurants, food delivery services, and retail food chains are increasingly adopting environmentally responsible packaging to meet consumer demands and achieve corporate sustainability goals. As global food delivery and takeaway consumption continues to increase, the need for grease-resistant yet environmentally safe packaging materials is growing. This situation creates opportunities for packaging manufacturers to innovate by developing paper-based containers, molded fiber trays, and barrier-coated wraps that fulfil both performance and sustainability criteria across various foodservice applications.

MARKET CHALLENGES

Maintaining Barrier Performance Without PFAS is a Major Challenge to Market Growth

A significant challenge in the PFAS-free food packaging sector is achieving robust resistance to grease, oil, and moisture without the use of fluorinated chemicals. PFAS compounds have historically provided outstanding barrier performance, even in applications involving high temperatures or high-fat foods, such as fried items, baked goods, and microwaveable meals. Alternative coatings may occasionally struggle to match the same level of durability, heat stability, or protection for shelf life. To ensure consistent performance across various food types and environmental conditions, ongoing material innovation and testing are essential. Packaging manufacturers are required to strike a balance among barrier effectiveness, recyclability, compostability, and cost efficiency, making the development of scalable PFAS-free solutions technically challenging and resource-intensive.

Segmentation Analysis

By Material

Sustainability Compatibility, Regulatory Acceptance, and Functional Coatings Drive the Dominance of Paper & Paperboard

Based on material, the market is divided into paper & paperboard, bioplastics and bio-derived polymers, aluminum, and others.

The paper & paperboard segment is expected to account for the largest share in the coming years. Paper and paperboard are the leading materials in the market due to their sustainability, broad acceptance, and adaptability as a replacement for fluorinated chemicals. These materials are already widely used in foodservice packaging, including takeaway containers, bakery wraps, and fast-food cartons, facilitating manufacturers' shift to PFAS-free alternatives. Additionally, their comparatively lower cost, robust supply availability, and compatibility with current packaging production systems further solidify their dominant position in the PFAS-free food packaging sector.

The bioplastics and bio-derived polymers segment is expected to grow at a CAGR of 6.61% over the forecast period.

By Product Type

High Usage in Foodservice Applications, Convenience, and Barrier Performance Drive the Dominance of Films & Wraps

Based on product type, the market is segmented into films & wraps, plates & bowls, trays, bags & pouches, cups & lids, and others.

In 2025, the films & wraps segment dominated the global PFAS-free food packaging market share, primarily due to their extensive application in quick-service restaurants, takeaway establishments, bakeries, and retail food packaging. These packaging solutions offer lightweight, flexible, and cost-effective options for wrapping sandwiches, burgers, baked goods, and greasy items, all while ensuring hygiene and preserving product freshness. As the global trend of food delivery and takeaway continues to grow, demand for PFAS-free films and wraps is expected to remain strong.

The plates & bowls segment is projected to grow at a CAGR of 6.75% over the forecast period.

By End Use

To know how our report can help streamline your business, Speak to Analyst

High Packaging Demand, Regulatory Compliance Pressure, and Sustainability Commitments Drive Dominance of Packaged Food Manufacturers

Based on the end use, the market is segmented into packaged food manufacturers, retail & convenience stores, restaurants & fast food outlets, and others.

The packaged food manufacturers segment is expected to hold a dominant market share over the forecast period. This dominance is attributed to their need for substantial quantities of food-contact packaging across various product categories, including ready meals, snacks, frozen foods, bakery items, and convenience foods. As regulatory scrutiny of PFAS in food-contact materials intensifies, packaged food companies face significant pressure to ensure compliance and mitigate potential health risks associated with fluorinated substances. The ongoing expansion of the packaged food industry, along with the growth of retail distribution channels, further reinforces this segment's leading market share.

The retail & convenience stores segment is projected to grow at a CAGR of 6.52% over the forecast period.

PFAS-Free Food Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America PFAS-Free Food Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 13.02 billion and maintained its leading position in 2025 at USD 13.81 billion. The market in North America is largely propelled by robust regulatory momentum and corporate sustainability efforts. Numerous state-level prohibitions on PFAS in food-contact materials are hastening the shift toward safer alternatives. Moreover, leading foodservice chains and retailers are actively embracing PFAS-free packaging to fulfil consumer demands and uphold environmental responsibilities.

U.S. PFAS-Free Food Packaging Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 11.14 billion in 2025, accounting for roughly 30.76% of global sales. The U.S. plays a significant role in the market, driven by growing federal and state regulations that limit PFAS in food-contact materials. Intense demand from consumers, environmental organizations, and prominent foodservice companies is hastening the shift toward PFAS-free paper-based and coated packaging alternatives.

Europe

Europe reached a valuation of USD 6.12 billion in 2025 and is projected to grow at a CAGR of 6.20% in the coming years. The growth of the European market is primarily driven by stringent chemical regulations and policies that promote a circular economy. Regulatory frameworks that emphasize reducing hazardous substances and using sustainable materials are motivating packaging manufacturers to replace PFAS-based coatings.

U.K PFAS-Free Food Packaging Market

The U.K. market in 2025 was valued at USD 1.13 billion, representing approximately 3.12% of global revenues.

Germany PFAS-Free Food Packaging Market

Germany's market was valued at USD 1.32 billion in 2025, equivalent to around 3.65% of global sales.

Asia Pacific

Asia Pacific was valued at USD 8.13 billion in 2025 and secured the position of the second-largest region in the market. In the region, India and China are both estimated to reach USD 2.00 billion and USD 2.65 billion, respectively, in 2025. In the Asia Pacific region, the market is primarily propelled by the swift growth of the foodservice and packaged food sectors. The rise in urbanization, the increase in takeaway and food delivery, and heightened environmental consciousness are fostering the use of safer packaging materials.

Japan PFAS-Free Food Packaging Market

The Japanese market in 2025 was valued at USD 1.09 billion, accounting for roughly 3.02% of global revenues. Robust food safety regulations, advancements in packaging technology, and a growing emphasis on sustainable packaging options significantly impact Japan's market growth.

China PFAS-Free Food Packaging Market

China's market is projected to be one of the largest worldwide, with 2025 revenues valued at around USD 2.65 billion, representing roughly 7.31% of global sales.

India PFAS-Free Food Packaging Market

The Indian market in 2025 was valued at USD 2.00 billion, accounting for roughly 5.51% of global sales.

Latin America

The Latin America region is expected to witness moderate growth during the forecast period. The Latin America market was valued at USD 4.91 billion in 2025. The market for PFAS-free food packaging in Latin America is slowly evolving, driven by heightened environmental consciousness and a rising demand for sustainable PFAS-free packaging solutions within the foodservice industry.

Middle East & Africa

In the Middle East & Africa, South Africa was valued at USD 0.77 billion in 2025. In the Middle East & Africa, market growth is driven by the burgeoning quick-service restaurant industry and the rise of food delivery services. Although regulations specific to PFAS are still in development, international food brands and global packaging suppliers are launching PFAS-free options to comply with global sustainability standards and meet consumer safety expectations.

Saudi Arabia PFAS-Free Food Packaging Market

The Saudi Arabian market was valued at USD 1.34 billion in 2025, accounting for roughly 3.69% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Emphasize Product Introductions and Acquisitions to Propel Market Revenue

The global market has a semi-consolidated structure, with major players including Huhtamaki, Genpak, and Dart Container Corporation. The significant market shares of these packaging companies are due to numerous strategic initiatives, including collaborations among operating entities to advance research.

- For instance, in September 2024, Huhtamaki launched a new line of PFAS-free molded fiber foodservice packaging tailored for quick-service restaurants and takeaway uses. This solution incorporates plant-based materials and cutting-edge barrier technologies that resist grease and moisture without the use of fluorinated chemicals.

Pactiv Evergreen, Sabert Corporation, and Smurfit Kappa are other key companies in the market. They are expected to focus on new product introductions, strategic alliances, and collaborations to boost their global market shares in the coming years.

LIST OF KEY PFAS-FREE FOOD PACKAGING COMPANIES PROFILED

- Huhtamaki (Finland)

- Genpak (U.S.)

- Dart Container Corporation (U.S.)

- Pactiv Evergreen (U.S.)

- Sabert Corporation (U.S.)

- Smurfit Kappa (Ireland)

- Stora Enso (Finland)

- Graphic Packaging International (U.S.)

- Mondi (U.K.)

- DS Smith (U.K.)

- UPM (Finland)

- Detpak (Australia)

- PulPac (Sweden)

- Vegware (Scotland)

- ProAmpac (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2024: Stora Enso expanded its range of PFAS-free barrier-coated paperboard for foodservice packaging, including takeaway boxes, cups, and trays. The company has improved its dispersion barrier technology to provide robust resistance against grease and moisture, all while ensuring recyclability within current paper recovery systems.

- April 2024: Graphic Packaging International introduced new PFAS-free paperboard packaging solutions aimed at fast-food and convenience food applications. These products employ proprietary barrier technologies engineered to resist grease and heat while remaining recyclable. This launch is indicative of the company's wider strategy to remove fluorinated substances from food-contact packaging.

- February 2024: Smurfit Kappa announced the expansion of its Better Planet Packaging initiative, which now includes PFAS-free paper-based solutions for foodservice packaging, including wraps, trays, and takeaway boxes. The company has developed specialized coatings that resist oil and grease without using fluorinated chemicals.

- November 2023: Mondi launched a functional barrier paper free of PFAS for use in food packaging applications, including bakery items, confectionery, and takeaway foods. This innovative solution serves as a substitute for traditional fluorinated coatings, all the while ensuring grease resistance and safeguarding the products.

- August 2023: Pactiv Evergreen introduced a range of molded fiber foodservice containers that are free from PFAS, specifically aimed at quick-service restaurants and institutional food providers. These containers are engineered to accommodate hot, greasy foods, including fried items and ready-to-eat meals, while ensuring that no PFAS chemicals are intentionally added.

REPORT COVERAGE

The market analysis includes a comprehensive study of market size & forecast across all market segments included in the market reports. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, along with their regional prevalence. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.54% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material, Product Type, End Use, and Region |

| By Material |

|

| By Product Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 36.23 billion in 2025 and is projected to reach USD 63.64 billion by 2034.

In 2025, the market value in North America stood at USD 13.81 billion.

The market is expected to grow at a CAGR of 6.54% over the forecast period of 2026-2034.

In terms of material, the paper & paperboard segment is expected to lead the market.

Increasing global regulatory restrictions on PFAS are driving market growth.

Huhtamaki, Genpak, Dart Container Corporation, Pactiv Evergreen, Sabert Corporation, and Smurfit Kappa are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us