Pharma Quality Control and Compliance Market Size, Share & Industry Analysis, By Offering (Products {Instruments and Consumables}, Software, and Services), By Application (Small Molecule Drugs, Biologics and Biosimilars, Vaccines, Cell and Gene Therapies, and Others) By Function (Raw Material Quality Control, Microbiology and Contamination Control, Stability and Shelf-life Testing, In-process Quality Control, Finished Product Testing and Batch Release, and Others), By End User (Pharmaceutical & Biotechnology Companies, CROs & CDMOs, and Others), and Regional Forecast, 2026-2034

Pharma Quality Control and Compliance Market Size and Future Outlook

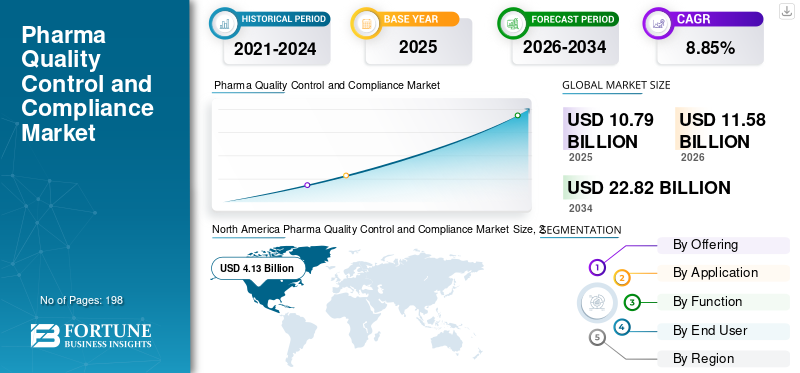

The global pharma quality control and compliance market size was valued at USD 10.79 billion in 2025. The market is projected to grow from USD 11.58 billion in 2026 to USD 22.82 billion by 2034, exhibiting a CAGR of 8.85% during the forecast period. North America dominated the pharma quality control and compliance market with a market share of 38.27% in 2025.

Pharmaceutical quality control and compliance systems are utilized to evaluate drug quality, ensure GMP compliance, oversee regulated documentation, and assist in release decisions related to raw materials, in-process batches, finished products, microbiological tests, stability, and validation processes. The market is expanding as pharmaceutical and biotechnology firms are boosting investments in QC tools, consumables, digital quality systems, and outsourced GMP testing to handle the increasing manufacturing complexity in small molecules, biologics, vaccines, and cell and gene therapies. The demand is further bolstered by an increased emphasis on contamination control, data integrity, batch-release efficiency, validation and qualification processes, along with cloud-based quality management systems that enhance audit preparedness and regulatory adherence.

Key players operating in the global market include Thermo Fisher Scientific Inc., Agilent Technologies, Waters Corporation, Sartorius AG, and others. These firms are focusing on technological advancements in their products, strategic collaborations, and portfolio expansion to maintain market presence.

Download Free sample to learn more about this report.

PHARMA QUALITY CONTROL AND COMPLIANCE MARKET TRENDS

Shift toward Automated Compliance Solutions is a Significant Trend Observed in the Global Market

Pharmaceutical and biotechnology firms are shifting from manual, paper-based, and disjointed quality processes to automated systems that can more consistently handle deviations, CAPA, document management, training, batch review, and audit preparedness. This change is occurring as regulated manufacturers require quicker decision-making, improved traceability, reduced documentation errors, and enhanced data integrity within increasingly complex operations. Automated compliance tools assist companies in standardizing procedures across various locations, shortening review cycle durations, and enhancing preparedness for inspections and GMP audits. The trend is intensifying as biologics, sterile products, and advanced therapies rise, leading to an increase in the volume of quality events and compliance documentation that need to be addressed in real time. Consequently, pharmaceutical firms are investing more resources into eQMS, LIMS, digital batch release, and AI-driven workflow platforms that link quality, manufacturing, and regulatory systems.

- For instance, in January 2025, Honeywell launched the TrackWise Life Sciences Platform which was designed to transform how life sciences organizations approach integrated manufacturing and quality management through digital transformation and advanced automation.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand Due to Increasing Drug Development Activities to Boost Market Growth

The growing need stemming from heightened drug development activities is a major factor driving the pharma quality control and compliance market growth. Pharmaceutical and biotechnology firms are broadening their pipelines to include small molecules, biologics, and advanced therapies, which require increased testing of raw materials, in-process controls, microbiology, stability studies, validation, and batch-release assistance. An increase in development programs also raises the demand for GMP-compliant analytical methods, enhanced documentation systems, and stricter compliance controls as candidates transition from development to clinical and commercial manufacturing. This directly enhances the need for QC instruments, consumables, quality software, and outsourced testing/compliance services.

- For instance, in April 2025, Novartis announced plans to invest USD 23 billion over five years to expand its U.S. based manufacturing and R&D footprint, including 10 facilities, of which 7 are new.

MARKET RESTRAINTS

Stringent Regulatory Requirements to Limit Market Growth

Stringent regulatory requirements are a key market restraint as they increase cost, complexity, and time needed to maintain GMP-compliant operations. Drug manufacturers must invest heavily in validated systems, documentation controls, quality oversight, data integrity, environmental monitoring, employee training, and audit readiness to meet FDA, EMA, and other regulatory standards. Even minor gaps in quality-unit oversight, cleaning validation, contamination control, or batch documentation can trigger warning letters, remediation costs, delayed product release, or supply disruption. These requirements are especially burdensome for smaller manufacturers and for companies expanding into biologics, sterile products, or multi-site global operations. While strict regulations support product safety, they also raise operating costs and slow implementation of new processes, facilities, and product transfers.

- For instance, in August 2025, the U.S. FDA issued a warning letter to Amneal Pharmaceuticals following a March 2025 inspection of its facility in Gujarat, India. The letter summarized significant CGMP violations for finished pharmaceuticals, illustrating how non-compliance can lead to regulatory action, remediation burden, and potential operational disruption.

MARKET OPPORTUNITIES

Growing Adoption of Outsourced Quality Control Services to Offer Market Growth Opportunities

The increasing use of outsourced quality control services present a significant opportunity in the pharmaceutical quality control and compliance sector. Pharmaceutical and biotech firms are progressively delegating QC tasks to specialized partners to achieve quicker turnaround times, GMP-certified lab capacity, and enhanced analytical skills without incurring significant internal capital expenditures. This is gaining significance as biologics, vaccines, and cell and gene therapies necessitate increasingly intricate release testing, contamination management, method verification, and stability assistance. Outsourcing aids companies in handling fluctuating production volumes, alleviating stress on internal QA/QC teams, and enhancing flexibility during scaling or multi-site production. Furthermore, international service providers can facilitate standardized testing in various regions, which is beneficial for businesses functioning in several regulatory markets.

- For instance, Eurofins Scientific, and Charles River Laboratories are some of the companies that offer quality control services.

MARKET CHALLENGES

Complexity of Maintaining Consistent Quality Standards across Global Supply Chains Pose a Prominent Challenge to Market Growth

The challenge of ensuring uniform quality standards throughout global supply chains is a significant issue in the pharmaceutical quality control and compliance market. Pharmaceutical companies are progressively sourcing APIs, excipients, intermediates, packaging materials, and finished-dose manufacturing support from various countries, complicating the maintenance of consistent GMP execution across all sites and suppliers. Variations in supplier quality systems, documentation methodologies, testing intensity, data integrity measures, and regulatory development can lead to inconsistencies that increase compliance risk. This issue becomes increasingly significant when businesses handle extensive, multi-layer supply chains for biologics, sterile medications, or high-volume generics, where even a minor quality deficiency can postpone batch release or initiate remediation. It also heightens the necessity for supplier qualification, audit programs, contamination control, traceability, and unified quality management systems across different regions. Consequently, businesses need to invest more in supervision, verification, digital quality solutions, and third-party testing to ensure global operations remain coordinated.

- For instance, in July 2025, the WHO noted that contaminated medicines often arise from systemic vulnerabilities in the global supply chain of pharmaceutical excipients.

Segmentation Analysis

By Offering

Wide Use of QC Instruments and Consumables Allowed the Products Segment to Dominate

In terms of offering, the market is divided into products, software, and services. The products segment is further divided into instruments and consumables.

The products segment led the global pharma quality control and compliance market share in 2025. The segment's dominance is due to the vital function of instruments and consumables in everyday pharmaceutical quality control tasks, including raw material analysis, in-process evaluations, microbiological assessments, sterility evaluations, stability testing, and batch release of finished products. Additionally, each regulated manufacturing facility necessitates a tangible QC arrangement, leading to consistently elevated expenses for chromatography systems, microbiological testing equipment, monitoring instruments, reagents, media, filters, and reference substances.

- For instance, in May 2024, Sartorius announced the launch of its 4th generation Sterisart Universal pump for sterility testing. The system is designed to meet the strict quality and safety standards of the pharmaceutical and biotechnology industries, while also supporting 21 CFR Part 11 compliant documentation for stronger data integrity and audit readiness.

The software segment is anticipated to rise with a CAGR of 12.03% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Broad Manufacturing Base of Small Molecule Drugs Supported the Segmental Dominance

Based on application, the market is classified into small molecule drugs, biologics and biosimilars, vaccines, cell and gene therapies, and others.

The small molecule drugs segment accounted for the dominant share due to the extensive worldwide manufacturing capacity for tablets, capsules, injectables, and other traditional pharmaceutical items, leading to significant and ongoing demand for raw material testing, in-process inspections, dissolution assessments, impurity evaluations, stability research, and batch release of finished products. Additionally, small molecule products are manufactured in larger batch volumes at more locations than advanced modalities, which ensures that expenditures on QC instruments, consumables, and compliance systems remain robust. Furthermore, the segment is set to hold 54.3% share in 2026.

- For instance, in October 2025, Merck broke ground on a USD 3.0 billion pharmaceutical Center of Excellence in Elkton, Virginia. The company stated that the expansion includes both active pharmaceutical ingredient and drug product investment supporting small molecule manufacturing and testing.

The vaccines segment is anticipated to rise with a CAGR of 9.22% over the forecast period.

By Function

Critical Need for Final Quality Verification Before Commercial Release Allowed the Segment to Dominate

On the basis of function, the market is divided into raw material quality control, microbiology and contamination control, stability and shelf-life testing, in-process quality control, finished product testing and batch release, regulatory compliance management, validation & qualification / quality systems management, and others.

In 2025, the market was primarily led by the finished product testing and batch release segment and is set to hold a 21.3% share in 2026. The segment's dominance stems from the necessity that each pharmaceutical batch must undergo final specification checks prior to shipment, rendering this function essential in both small molecule and biologic production. Additionally, finished product testing combines assay, impurity, dissolution, sterility, potency, and documentation review activities, thus encompassing a significant portion of QC and compliance expenditures. As delays during the batch-release phase can directly impact product availability, working capital, and time to market, manufacturers keep investing significantly in quicker, more dependable, and better-connected release processes. The ongoing requirement for final product validation and release preparedness reinforces the segment's robust market position.

- For instance, in May 2025, Veeva highlighted the growing need to streamline complex batch release workflows and improve product supply decisions through a centralized and automated approach.

The regulatory compliance management segment is anticipated to rise with a CAGR of 10.84% over the forecast period.

By End User

Pharmaceutical & Biotechnology Companies Led Demand due to High Spending on Quality Control and Regulatory Compliance

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, CROs & CDMOs, and others.

The pharmaceutical & biotechnology companies segment dominated the market in 2025 as they directly own drug development, manufacturing, batch release, and regulatory compliance responsibilities. Furthermore, they are the primary buyers of QC instruments, consumables, quality software, microbiology systems, validation tools, and compliance services needed to maintain GMP standards across internal manufacturing networks. Since they manage product quality from raw material testing to finished-product release, their spending remains higher than outsourced players in overall value terms. Furthermore, the segment is set to hold 71.4% share in 2026.

- For instance, in July 2024, Biogen announced an USD 2 billion manufacturing investment in North Carolina. The company stated that its campuses include sophisticated quality control laboratories to ensure the safety, efficacy, and purity of the medicines.

In addition, CROs/CDMOs are projected to witness a growth rate of 10.95% during the forecast period.

Pharma Quality Control and Compliance Market Regional Outlook

By geography, the market is divided into Latin America, Asia Pacific, Europe, North America, and the Middle East & Africa.

North America

North America Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest share of the market and attained USD 3.88 billion in 2024 and maintained its dominance in 2025 with USD 4.13 billion. North America is expanding due to its solid foundation in pharmaceutical, biotechnology, and advanced therapy production. The area allocates significant funds for GMP compliance, validation, sterility assurance, batch-release testing, and digital quality systems.

U.S. Pharma Quality Control and Compliance Market

The U.S. market led North America and is projected to be approximately USD 3.85 billion in 2026, representing about 33.3% of the global market.

Europe

Europe’s market is estimated to grow at a CAGR of 7.90% during the forecast period fueled by a wide pharmaceutical manufacturing network, strong biologics and vaccine production base, and well-established GMP environment. The region also benefits from strong CDMO presence, which supports outsourced QC testing and compliance services.

U.K. Pharma Quality Control and Compliance Market

The U.K. market is estimated at around USD 0.48 billion for 2026, representing roughly 4.2% of global revenues.

Germany Pharma Quality Control and Compliance Market

Germany is projected to reach approximately USD 0.67 billion in 2026, equivalent to around 5.8% of global sales.

Asia Pacific

Asia Pacific’s market size is expected to reach a valuation of USD 2.76 billion in 2026 and is the fastest growing region because of the swift increase in pharmaceutical production capabilities in China and India. The area is experiencing increased investment in QC laboratories, microbiological testing, contamination management, and GMP-compliant manufacturing systems to facilitate both local supply and export markets.

Japan Pharma Quality Control and Compliance Market

In 2026, Japan is set to reach USD 0.56 billion, accounting for roughly 4.9% of global revenues.

China Pharma Quality Control and Compliance Market

China’s market is projected to reach around USD 0.89 billion in 2026, representing roughly 7.7% of global sales.

India Pharma Quality Control and Compliance Market

In 2026, India is estimated to achieve USD 0.52 billion, accounting for roughly 4.5% of global revenues.

Latin America and Middle East & Africa

The growth in Latin America and the Middle East & Africa is anticipated to be moderate in the coming years driven by increasing investment in local pharmaceutical manufacturing, rising focus on regulatory compliance, and efforts to reduce dependence on imported medicines. The region’s market size is estimated at around USD 0.75 billion for 2026.

The GCC market is projected to reach approximately USD 0.20 billion in 2026, representing about 1.8% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Integrated QC Portfolios and Expanding Digital Compliance Capabilities to Support Players Market Position

The global market reflects a semi-fragmented competitive landscape, consisting of Thermo Fisher Scientific Inc., Agilent Technologies Inc., Waters Corporation, Sartorius AG, and other major companies which also represent a significant revenue. The considerable market presence of these companies is supported by their broad portfolios and strong geographic presence. Furthermore, these players are focusing on integrated quality ecosystems that connect QA, QC, training, validation, batch release, and compliance workflows, which is anticipated to strengthen their competitive position.

Other significant participants include Charles River Laboratories, Eurofins Scientific, LabVantage Solutions Inc., and LabWare. These firms are anticipated to focus on product improvement, and integrated product, and new product launches to elevate their market position.

- For instance in August 2024, Veeva Systems announced growing momentum for Veeva Vault LIMS, a cloud-based QC solution unified with Veeva Vault Quality. The company stated that this setup helps life sciences companies connect QA and QC processes, reduce paper-based documentation, and support more informed batch release decisions.

LIST OF KEY PHARMA QUALITY CONTROL AND COMPLIANCE COMPANIES

- Thermo Fisher Scientific Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Waters Corporation (U.S.)

- Veeva Systems (U.S.)

- Honeywell International Inc. (U.S.)

- Sartorius AG (Germany)

- Charles River Laboratories (U.S.)

- Eurofins Scientific (Luxembourg)

- LabVantage Solutions Inc. (U.S.)

- LabWare (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Charles River revealed its intention to acquire PathoQuest. Charles River stated that the agreement would enhance its biologics testing abilities by incorporating rapid, advanced GMP testing solutions, such as PathoQuest’s iDTECT quality-control platform for identifying adventitious agents and characterizing cell lines and viral vectors.

- May 2025: Waters Corporation announced that Empower Software now supports biologics data acquisition and QC analysis from Wyatt MALS and RI instruments.

- March 2025: LabVantage released LabVantage 8.9, the latest version of its LIMS platform. The update is designed to improve lab productivity, ensure accuracy and compliance, and simplify complex workflows, with added automation and AI-driven efficiencies relevant to regulated QC environments.

- March 2025: LabWare expanded its SaaS portfolio with LabWare ASSURE, alongside LabWare QAQC and LabWare GROW.

- January 2025: Veeva and Zifo revealed a collaborative product effort to expedite the modernization of quality control. The integration merges Veeva LIMS with Zifo’s qcKen platform, enabling companies to import data from source documents or different LIMS systems, alleviating master-data setup challenges and accelerating LIMS implementation and site deployment.

REPORT COVERAGE

The global pharma quality control and compliance market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides understanding of essential factors, including technological progress, product innovations, regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, as well as key developments in the industry within the market. The report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.85% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Application, Function, End User, and Region |

| By Offering |

|

| By Application |

|

| By Function |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 10.79 billion in 2025 and is projected to reach USD 22.82 billion by 2034.

In 2025, North Americas market value stood at USD 4.13 billion.

The market is expected to exhibit a CAGR of 8.85% during the forecast period of 2026-2034.

By offering, the products segment is expected to lead the market.

Increasing demand due to growing drug development activities, stronger focus on contamination control, and growing outsourcing to CROs/CDMOs are primarily driving market expansion.

Thermo Fisher Scientific Inc., Agilent Technologies, Waters Corporation, and Sartorius AG are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us