Phthalic Anhydride Market Size, Share & Industry Analysis, By Application (Plasticisers, Unsaturated Polyester Resins, Alkyd Resins and Others) and Regional Forecast, 2026-2034

Phthalic Anhydride Market Insights

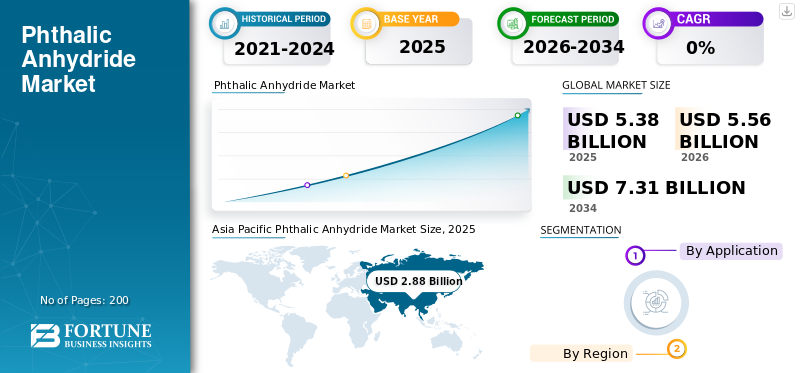

The global phthalic anhydride market size was USD 5.38 billion in 2025. The market is projected to grow from USD 5.56 billion in 2026 to USD 7.31 billion by 2034 at a CAGR of 3.5% during the 2026-2034 period. Asia Pacific dominated the global phthalic anhydride market with a market share of 53.53% in 2025.

Phthalic Anhydride is a white crystalline compound used mainly as an intermediate in producing plasticizers, alkyd resins, and unsaturated polyester resins. It is primarily derived from the oxidation of ortho-xylene and is essential in manufacturing flexible PVC, paints, and fiberglass-reinforced materials. The market is largely driven by rising demand for flexible PVC, especially in automotive and construction sectors across emerging economies. As plasticizers account for the majority of product consumption, growth in these downstream industries continues to strengthen the global demand. AEKYUNG CHEMICAL CO., LTD., I G Petrochemicals Ltd., NAN YA PLASTICS CORPORATION and POLYNT SPA are the key players operating in the market.

Download Free sample to learn more about this report.

PHTHALIC ANHYDRIDE MARKET Key Takeaways

- 2025 Market Size: USD 5.38 billion

- 2026 Market Size: USD 5.56 billion

- 2034 Forecast Market Size: USD 7.31 billion

- CAGR: 3.5% from 2026–2034

- Asia Pacific dominated the phthalic anhydride market with a 53.53% share in 2025.

- The plasticisers segment is anticipated to hold the dominant Phthalic Anhydride Market share during the forecast period.

- The unsaturated polyester resin segment is witnessing sustained demand, directly boosting segment growth.

Asia Pacific

Asia Pacific is expected to dominate the market during the forecast period, driven by rapid expansion of infrastructure and urban construction, fueling the production of flexible PVC materials.

North America

In North America, demand is sustained by its use in alkyd resins for industrial and architectural coatings.

Europe

In Europe, the product’s role in unsaturated polyester resins used in lightweight composites for automotive, construction, and marine applications drives market growth.

U.S.

The U.S. market benefits from demand for industrial and architectural coatings, particularly for corrosion resistance and aesthetic finishes in infrastructure and equipment.

Japan

Japan supports demand through the use of lightweight composites and advanced manufacturing applications.

Read More

PHTHALIC ANHYDRIDE MARKET TRENDS

Industrial Growth Driving Demand for Coatings and Paint Resins Reshaping Market

The steady expansion of industrial activity, particularly in sectors such as automotive, machinery, marine, and infrastructure, has significantly boosted demand for coatings, paints, and surface protection systems. Phthalic Anhydride plays a critical role in this space as a core raw material for alkyd resins, which are widely used in solvent-based coatings due to their durability, gloss, and adhesion properties. With increased manufacturing output and urban infrastructure investment in emerging economies, the need for industrial-grade coatings is anticipated to rise, driving phthalic anhydride market growth.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Surging Demand for Flexible PVC in Emerging Economies to Drive Market Growth

A key driver of the market is rising demand for flexible PVC, particularly in rapidly industrializing and urbanizing regions such as Asia Pacific, the Middle East and Latin America. Flexible PVC, which relies heavily on phthalate plasticizers derived from the product, is widely used in construction (e.g., flooring, pipes, wires), automotive interiors, and consumer goods. As infrastructure projects expand and housing developments accelerate in emerging economies, the demand for PVC-based materials is anticipated to surge. This growth directly fuels product consumption, as plasticizers account for the majority of usage globally. Moreover, favorable demographics, rising disposable incomes, and supportive government policies further amplify this trend across developing economies and driving market growth.

MARKET RESTRAINTS

Feedstock Volatility to Restrain Market Growth

Volatility in the prices of key feedstocks, particularly ortho-xylene and to a lesser extent, naphthalene, poses a significant restraint for phthalic anhydride producers. As the product is primarily manufactured via the catalytic oxidation of ortho-xylene, any fluctuation in crude oil or aromatics pricing directly affects production costs and profitability. This volatility is further amplified by geopolitical tensions, refining capacity shifts, and seasonal demand changes in related markets such as gasoline and para-xylene. Producers without integrated upstream capabilities are especially exposed, facing margin compression and pricing challenges. While long-term supply contracts and feedstock hedging strategies have become vital, they cannot fully eliminate exposure to this unpredictable cost variable.

MARKET OPPORTUNITIES

Strategic Integration to Create Market Growth Opportunities

Phthalic anhydride producers have significant opportunities to enhance profitability through strategic backward and forward integration. Backward integration into ortho-xylene production secures feedstock supply and reduces exposure to raw material price volatility. Forward integration into downstream products such as plasticizers, alkyd resins, or polyester intermediates, enables producers to capture greater value across the chain, differentiate offerings, and serve high-margin niche markets. This approach also strengthens supply reliability for end-use industries including PVC, coatings, and composites. As global competition intensifies and regulatory pressures upsurges, integrated business models could improve cost efficiency and create long-term resilience in volatile market conditions.

MARKET CHALLENGES

Competitive Pressure from Non-Phthalate Alternatives to Create Challenges for Market Growth

The market faces growing pressure from the adoption of non-phthalate and bio-based plasticizers, particularly in developed regions with stringent regulatory environments. Consumers and manufacturers are shifting toward alternatives including bio-based esters due to health and environmental concerns linked to traditional phthalates. This trend is driven by evolving legislation and rising sustainability expectations. As downstream users reformulate products to meet compliance and consumer demand, producers may face a decreasing market demand for traditional plasticizer applications, hampering long-term growth.

SEGMENTATION ANALYSIS

By Application

Surging Demand for Flexible PVC in Construction and Infrastructure to Drive Market Growth

Based on the application, the market is segmented into plasticisers, unsaturated polyester resins, alkyd resins and others.

The plasticisers segment is anticipated to hold the dominant Phthalic Anhydride Market share during the forecast period. The primary factor driving the segment is the rapid growth of flexible PVC demand, particularly in the construction, infrastructure, and automotive sectors. Phthalate plasticizers are essential for imparting flexibility, durability, and workability to PVC, which is widely used in cables, flooring, pipes, synthetic leather, and roofing membranes. Emerging markets across the globe are witnessing large-scale urbanization and infrastructure expansion, significantly boosting flexible PVC consumption. This directly accelerates demand for phthalic anhydride derived plasticizers, sustaining their dominant share in the market.

The unsaturated polyester resin is extensively used in fiberglass-reinforced plastics, enabling cost-effective, corrosion-resistant, and structurally robust components. Emerging economies are progressively adopting these composites in water tanks, panels, and infrastructure, while developed markets use them in renewable energy such as wind turbines. This sustained demand is prompting an increase in unsaturated polyester resins demand, directly boosting segment growth.

To know how our report can help streamline your business, Speak to Analyst

PHTHALIC ANHYDRIDE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific Phthalic Anhydride Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The Asia Pacific region is expected to dominate the market during the forecast period. In Asia Pacific, the major drivers of Phthalic Anhydride demand is the rapid expansion of infrastructure and urban construction, fueling the production of flexible PVC materials. Countries such as China, India, Vietnam, and Indonesia continue investing in housing, transport, and industrial development sectors as these heavily rely on phthalate plasticizers for use in flooring, cables, and synthetic leather. The region’s dominance in PVC manufacturing, combined with low-cost production bases and a growing middle class, makes plasticizers the backbone of product consumption, driving regional market growth.

To know how our report can help streamline your business, Speak to Analyst

North America

In North America, Phthalic Anhydride demand is sustained by its use in alkyd resins for industrial and architectural coatings. With a mature construction market and consistent industrial maintenance cycles, coatings formulated with alkyds remain in strong demand, particularly for corrosion resistance and aesthetic finishes in infrastructure and equipment. The existing producers are focusing on specialty applications such as high-performance coatings, pigment intermediates, and engineered resins, where the product is used in more customized formulations.

Europe

In Europe, the product’s role in unsaturated polyester resins used in lightweight composites for automotive, construction, and marine applications drive the market growth. Producers in the region are redirecting PA toward high-value, low-emission resins, particularly in FRP applications. Lightweight composites made with unsaturated polyester resins are key to improving fuel efficiency and reducing emissions, aligning with Europe's Green Deal targets and driving market growth in tandem.

Latin America

In Latin America, product demand is driven by recovery and expansion of residential and commercial construction, which is prompting downstream consumption of both plasticizers and alkyd resins. Flexible PVC is widely used in regional infrastructure projects for piping, cabling, and synthetic leather, while alkyd-based paints and coatings remain popular due to cost efficiency and ease of application. Countries such as Brazil, Mexico, and Colombia are experiencing growth in domestic coatings demand, linked to both renovation cycles and industrial activity. This rising consumption of coatings and plasticizer resins continues to support stable product demand across the region.

Middle East & Africa

In the Middle East & Africa, Phthalic Anhydride demand is being propelled by ongoing industrialization and investment in infrastructure, particularly in fast-developing economies such as Saudi Arabia and South Africa. Massive government-led construction initiatives, combined with electrification and urban housing development, are boosting flexible PVC consumption, thereby increasing demand for product-based plasticizers. Simultaneously, a growing domestic market for paints and coatings is supporting the use of PA in alkyd resin manufacturing. With expanding chemical capacity, the region is increasingly producing phthalic anhydride locally to support downstream demand for plastics and construction materials.

COMPETITIVE LANDSCAPE

Key Industry Players

Integration Strategies Intensify Competition in Global Market

The global phthalic anhydride market exhibits moderate to high competitive rivalry, driven by regional production clusters, cost competitiveness, and integration strategies. Producers compete on scale, feedstock access (ortho-xylene), and downstream linkages to plasticizers and resins. A major trend is the forward integration into value-added products, notably plasticizers and polyester resins, to capture margin stability and reduce market exposure. Leading players such as AEKYUNG CHEMICAL CO., LTD., I G Petrochemicals Ltd., NAN YA PLASTICS CORPORATION and POLYNT SPA dominate the market, leveraging global distribution networks and technical expertise.

LIST OF KEY PHTHALIC ANHYDRIDE COMPANIES PROFILED:

- AEKYUNG CHEMICAL CO., LTD. (South Korea)

- AIR WATER PERFORMANCE CHEMICAL INC. (Japan)

- I G Petrochemicals Ltd. (India)

- LANXESS (Germany)

- NAN YA PLASTICS CORPORATION (Taiwan)

- POLYNT SPA (Italy)

- Shanghai Douwin Chemical Co.,Ltd. (China)

- Stepan Company (U.S.)

- Thirumalai Chemicals (India)

- UPC Technology Corporation (Taiwan)

- Other Key Players

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading applications of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Volume (Kiloton); Value (USD Billion) |

|

Growth Rate |

CAGR of 3.5% during 2026-2034 |

|

Segmentation |

By Application, and By Geography |

|

By Application |

· Plasticisers · Unsaturated Polyester Resins · Alkyd Resins · Others |

|

By Geography |

North America (By Application, By Country)

Europe (By Application, By Country)

Asia Pacific (By Application, By Country)

Latin America (By Application, By Country)

Middle East & Africa (By Application, By Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 5.38 billion in 2025 and is projected to record a valuation of USD 7.31 billion by 2034.

In 2025, Asia Pacific stood at USD 2.88 billion.

Registering a CAGR of 3.5%, the market will exhibit steady growth during the forecast period of 2026-2034.

The plasticiser application is expected to lead this market during the forecast period.

Surging demand for flexible PVC in emerging economies to drive market growth.

AEKYUNG CHEMICAL CO., LTD., I G Petrochemicals Ltd., NAN YA PLASTICS CORPORATION and POLYNT SPA are the major players operating in the market.

Asia Pacific dominated the market in terms of share in 2025.

Industrial growth driving demand for coatings and paint resins to create market growth opportunities.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us