Pin Insertion Machine Market Size, Share & Industry Analysis, By Method (Automatic, Semi-automatic, and Manual), By Technology (Press-fit, Through-hole, and Surface-mount), By Insertion Platform (PCBs, Coil Frames, Lead Frames, Transformers, Plastic Connectors, and Metal Components), By Application (Consumer Electronics, Telecommunications, Medical, Automotive, Aerospace & Defense, Energy & Power, and Others) and Regional Forecast, 2026 - 2034

Pin Insertion Machine Market Size and Future Outlook

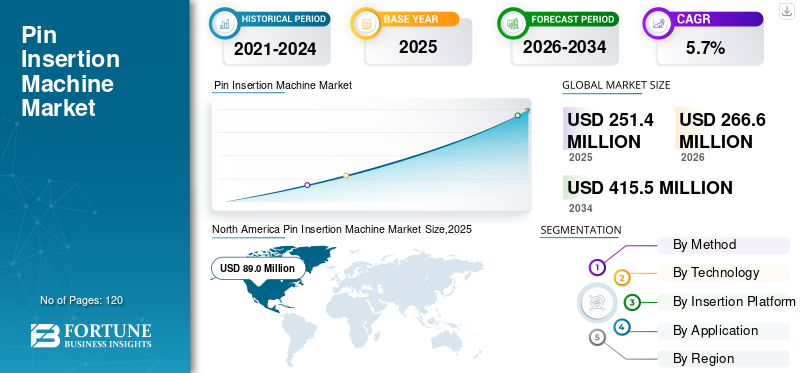

The global pin insertion machine market size was valued at USD 251.4 million in 2025. The market is projected to grow from USD 266.6 million in 2026 to USD 415.5 million by 2034, exhibiting a CAGR of 5.7% during the forecast period. North America dominated the global pin insertion machine market with a market share of 35.4% in 2025.

The global pin insertion machine market comprises automated equipment used to accurately insert electronic pins and terminals into printed circuit boards and components, supporting high-speed and high-precision electronics assembly across industries. The global market growth continues to expand as electronic component manufacturers increasingly adopt automated pin insertion machines to achieve high precision, high speed, and high-volume assembly operations. With production lines becoming more digitalized under Industry 4.0, manufacturers are shifting toward fully automated and software-integrated systems to streamline the manufacturing process, enhance throughput, and reduce human error. Rising demand across consumer electronics, telecommunications equipment, and automotive electronics further strengthens the need for advanced pin insertion technology capable of supporting miniaturized and complex device architectures.

- In 2025, leading equipment providers introduced AI-enabled insertion platforms equipped with predictive calibration systems to optimize cycle accuracy and minimize downtime, reflecting the industry’s shift toward smarter and more connected assembly solutions.

As global competition intensifies, players in the global pin insertion machine industry such as TE Connectivity, Autosplice, and ShinMaywa Industries are implementing advanced robotics, machine vision, and real-time analytics to meet the growing demand for automation. The pin insertion machine industry is expected to experience steady growth as manufacturers prioritize flexible assembly lines, reduced operational costs, and sustainable, energy-efficient production processes.

IMPACT OF GENERATIVE AI

Adoption of AI-driven Automation to Accelerate Manufacturing Efficiency

Generative AI is proving to be a significant force that will dominate the electronics manufacturing world by making faster designs, automating some parts of decision-making, and by allowing improvements in machine performance through simulation. In the domain of pin insertion, AI is doing all these things and more it is not only marking optimum tool paths, but also forecasting risks of component misalignment, and suggesting corrective measures instantaneously. All these functions combined lead to a tremendous cut down in the rework rates, reduced setup times, and thus overall production efficiency improved.

At the same time, generative AI is helping the manufacturers to predict the trends of component demand and to adjust their inventory accordingly, which is a big step toward the supply chain management. The more factories are using the AI-driven platforms, the more it becomes necessary to have a stronghold on the areas of system transparency, ethical data usage, and operation reliability. On one hand, the technology is empowering the workers by increasing their capabilities, while on the other hand, it is making it necessary for the organizations to find a middle ground between automation and governance in order to secure the deployment across the production environments as safe and ethical.

Download Free sample to learn more about this report.

PIN INSERTION MACHINE MARKET TRENDS

Shift Toward Fully Automated and Vision-Guided Insertion Platforms Drives Market Evolution

The manufacturers are moving from manual and semi-automatic systems to fully automated, vision-assisted insertion platforms that can identify pin alignment, check tolerances, and rectify deviations in no time. The increasing requirement for precision in the assembly of electronic components has been the main reason for the quick uptake of the systems, especially in the case of high-density PCBs and microelectronic modules.

Industry 4.0 technologies such as integrated data monitoring systems, error-proofing technologies, and real-time performance dashboards are becoming standard expectations among the end users, thereby improving the traceability and transparency of operations in the production lines.

- In 2024, several automation companies unveiled new-generation robotic pin insertion modules with enhanced cross-line communication capabilities to support digital factory ecosystems under Industry 4.0.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Precision Electronic Assemblies to Propel Market Growth

As electronic devices become increasingly compact and functionally complex, manufacturers require pin insertion solutions that can deliver precision, reliability, and repeatability at high speeds. The growing use of connectors, coil frames, transformers, and surface-mount components across consumer electronics and automotive applications has amplified the demand for automated insertion machinery.

Companies are investing in more advanced insertion platforms to reduce assembly time, minimize defect rates, and maintain consistent quality in high volume production. Vendors offering integrated machine vision, force-control feedback, and intelligent process calibration continue to dominate the global market for pin insertion machine.

- In 2025, major automotive electronics suppliers expanded their automated assembly lines to incorporate next-generation insertion machines capable of adapting to multiple connector formats with minimal changeover time.

MARKET RESTRAINTS

High Initial Investment and Skilled Workforce Shortage Limit Adoption

The high initial cost of advanced insertion equipment is one of the main reasons why small and mid-sized manufacturers still hesitate to invest, even though there is a strong trend toward automation. Not only the machinery itself, but also the integration, software calibration, and regular maintenance require heavy capital expenditure for these systems.

Moreover, the greater technical complexity of the automated insertion platforms causes the need for skilled technicians to operate them and fix problems. The lack of sufficiently trained staff results in operational difficulties being magnified and large-scale market acceptance being delayed.

- A 2024 industry workforce analysis revealed that over 58% of electronics manufacturers face difficulties in hiring skilled automation technicians capable of handling advanced robotic and AI-supported assembly systems

MARKET OPPORTUNITIES

Growing Integration of Robotics and AI to Create Lucrative Growth Opportunities

The integration of robotics, machine vision, and AI-driven diagnostic tools presents major opportunities for next-generation pin insertion machines. Real-time defect detection, predictive maintenance, adaptive insertion force modulation, and automated tool alignment are emerging as key differentiators for market players.

Furthermore, rising investments in electric vehicles, smart appliances, and telecommunications equipment fuel the demand for high-speed, precise, and reliable insertion systems capable of handling diverse component geometries and materials

- In 2025, leading automation providers launched modular, software-configurable insertion platforms designed to support AI-based insertion path optimization and remote monitoring functionality

Download Free sample to learn more about this report.

Segmentation Analysis

By Method

Automatic Segment Dominates Market Owing to Precision and High-Speed Capabilities

Based on method, the market segmented into automatic, semi-automatic, and manual.

To know how our report can help streamline your business, Speak to Analyst

The automatic segment dominated the global market for pin insertion machine with highest market share as well as CAGR of 7.5% due to its ability to deliver high precision, consistent cycle performance, and reduced dependency on manual labor. Automated systems support high-speed operations and advanced monitoring features, making them ideal for high-volume production lines across consumer electronics and automotive sectors.

- In March 2025, Panasonic Factory Solutions unveiled its next-generation fully automated pin insertion platform equipped with AI-driven alignment correction and predictive maintenance capabilities. The system was adopted by several major electronics OEMs to boost high-volume production efficiency, reinforcing the strong industry shift toward automatic pin insertion machines.

The semi-automatic segment recorded the second highest CAGR of 2.3% during the forecast period.

By Technology

Press-Fit Technology Leads Due to Reliable, Solder-Free Interconnect Solutions

By technology, the market segmented into press-fit, through-hole, and surface-mount.

The press-fit segment retains the largest market share along with the highest CAGR of 6.9% as it allows for robust, solder-free connections, reduces thermal stress on components, and is suitable for eco-friendly manufacturing processes. Its increasing usage for intricate PCBs and automotive electronics strengthens its superiority and attractiveness in the fields where precision is critical.

- In February 2025, Bosch announced the expansion of its automotive electronics division with the installation of advanced press-fit insertion lines for ECU manufacturing. The investment aimed to improve connection reliability and eliminate soldering defects, highlighting the growing adoption of press-fit technology in high-performance electronic assemblies.

The through-hole segment recorded the second highest CAGR of 4.0% during the forecast period.

By Insertion Platform

PCBs Segment Holds Largest Market Share Driven by High Consumption in Electronics Assembly

Based on insertion platform, the market includes PCBs, coil frames, lead frames, transformers, plastic connectors, and metal components.

The PCBs segment maintains a leading position in the market due to the unceasing expansion of consumer electronics, telecommunications, and medical device manufacturing. The increased demand for multi-layer PCBs and dense component arrangements drives the requirement for advanced pin insertion machines that are able to perform high-speed and high-precision operations simultaneously. For instance,

- In January 2025, Foxconn integrated new high-speed PCB pin insertion systems across its smartphone and IoT device production units. The upgrade improved assembly accuracy for dense multilayer PCBs, underscoring why PCBs remain the dominant insertion platform across global electronics manufacturing.

The lead frames segment recorded the highest CAGR of 8.6% during the forecast period.

By Application

Consumer Electronics Segment Leads Due to High Production Volume and Rapid Product Cycles

The market segmented by application into consumer electronics, telecommunications, medical, automotive, aerospace & defense, energy & power, and others.

The consumer electronics segment holds the highest market share driven by increasing production of smartphones, wearables, home appliances, and smart devices. Frequent product upgrades, shorter life cycles, and rising demand for high-density connectivity components further enhance the adoption of automated pin insertion systems. For instance,

- In April 2025, Samsung Electronics deployed advanced automated pin insertion robots in its semiconductor and consumer device plants to support rising production volumes of smart home devices and wearables. The move reflects growing investments in automated assembly within the consumer electronics sector, which continues to lead market demand.

The automotive segment exhibits the second highest CAGR of 6.7% during the forecast period, owing to electrification trends and rising electronic content in vehicles.

Pin Insertion Machine Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and Middle East & Africa.

NORTH AMERICA

North America holds the highest pin insertion machine market share due to its advanced manufacturing infrastructure, strong automation adoption, and high presence of major electronics and automotive OEMs. The region continues to dominate as companies increasingly invest in Industry 4.0 technologies and next-generation automated insertion platforms.

North America Pin Insertion Machine Market Size,2025 (USD million)

To get more information on the regional analysis of this market, Download Free sample

The U.S. pin insertion machine market is driven by strong demand from electronics manufacturing, automotive electronics, and industrial automation sectors. Increasing investments in smart factories, robotics, and AI-enabled assembly systems are accelerating the adoption of advanced pin insertion technologies across the country.

- In 2025, U.S.-based automation manufacturers invested heavily in AI-powered insertion tools to support precision-driven electronics assembly.

EUROPE

Europe shows steady growth in the pin insertion machine landscape, supported by its well-established automotive, industrial electronics, and aerospace manufacturing sectors. The region’s strong emphasis on quality standards, precision engineering, and sustainability-driven production reshapes manufacturing lines toward automated pin insertion technologies and smart factory systems.

- In 2025, Infineon Technologies announced significant upgrades to its PCB and semiconductor module assembly lines in Germany by integrating high-speed press-fit pin insertion systems, reinforcing Europe’s commitment to advanced automation across critical electronic manufacturing processes.

ASIA PACIFIC

Asia Pacific records the highest CAGR, driven by rapid electronic component manufacturing expansion across China, South Korea, Japan, and India. Rising demand for consumer electronics, EV components, telecom equipment, and high-volume PCB assembly supports robust adoption of automated and semi-automated pin insertion machines in the region.

- In March 2025, Shenzhen-based electronics manufacturers announced large-scale deployment of AI-enabled automated pin insertion machines to enhance PCB production efficiency, reflecting Asia Pacific’s accelerating shift toward high-speed and precision-driven assembly automation.

MIDDLE EAST and AFRICA

The Middle East and Africa area are experiencing a gradual but steady spread of automatic pin insertion machines due to the growing diversification of countries' economies toward electronics, renewable energy projects, and smart infrastructure development. The governments' support through industrialization projects and the continuous demand for faster and less expensive manufacturing processes are the main factors behind this expansion.

SOUTH AMERICA

In the case of South America, moderate growth is still the trend with Brazil and Mexico, for example, gradually increasing their respective markets of consumer electronics assembly and automotive components manufacturing. On the other hand, new production-line automation and PCB assembly investment for telecommunication and household electronics are on the rise and they are driving the region's pin insertion machine market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Automation Ecosystems and Global Manufacturing Expertise Drive Market Leadership

Global pin insertion machine market’s top players are investing in advanced automation technologies, precision insertion platforms, and AI-assisted diagnostics in order to better their competition. Their proficiency in providing fast, flexible, and reliable insertion solutions for electronic components production allows them to cater to various sectors, i.e., automobile, consumer electronics, telecom, and medical equipment, among others.

The above-mentioned companies are still growing their presence by entering into partnerships, developing new products, and adopting Industry 4.0 technologies, thus, making their impact in the international market more prominent and stronger.

LIST OF KEY PIN INSERTION MACHINE COMPANIES PROFILED

- TE Connectivity (Switzerland)

- Autosplice (U.S.)

- ShinMaywa Industries (Japan)

- Weber Assembly Systems (Germany)

- Arburg (Germany)

- ASM Assembly Systems (Germany)

- Fischer Connectors (Switzerland)

- Schleuniger AG (Switzerland)

- BDM Electronics (U.S.)

- Hyrel Automation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: ASMPT unveiled its completely new SIPLACE V placement platform at productronica 2025, positioning it as a new era in SMT placement with around 30% higher performance, enhanced flexibility, and big-data-ready architecture for high-volume automotive, IT, and network infrastructure manufacturing.

- July 2025: Arburg reopened its extensively renovated and expanded Technology Center (ATC) in Rednitzhembach, Germany, transforming it into a modern, energy-efficient hub for customer trials, training, and application development after a multi-year upgrade program.

- June 2025: Komax and Schleuniger (Switzerland) officially opened a new Center of Competence in Tianjin, China, combining state-of-the-art production facilities with engineering and customer-support functions to reinforce their presence in the fast-growing Asian wire-processing and automation market.

- May 2025: ASMPT SMT Solutions launched its WORKS Integration platform, a central data-exchange and integration layer that connects ASMPT hardware and software with third-party and customer systems, forming the digital backbone for intelligent, fully integrated SMT production lines.

- June 2024: ASMPT SMT Solutions reorganized its SMT segment in the U.S., splitting operations into separate North and South America regions to sharpen market focus, strengthen local customer relationships, and improve service coverage for electronics manufacturing clients.

REPORT COVERAGE

The global pin insertion machine market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Method, Technology, Insertion Platform, Application, Region |

| By Method |

|

| By Technology |

|

| By Insertion Platform |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 251.4 million in 2025 and is projected to reach USD 415.5 million by 2034.

In 2025, the market value stood at USD 57.9 million.

The market is expected to exhibit a CAGR of 5.7% during the forecast period of 2026-2032.

The consumer electronics segment led the market by application.

Rising demand for high-precision electronic assemblies is driving the market growth

TE Connectivity, Autosplice, ShinMaywa Industries, Weber Assembly Systems are some of the prominent players in the market.

North America dominated the market in 2025.

The automotive sector is expected to grow with the highest CAGR.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us