Plastic to Fuel Market Size, Share & Industry Analysis, By Technology (Pyrolysis, Gasification, Hydrothermal Liquefaction (HTL), and Catalytic Depolymerization), By Fuel Type (Diesel / Fuel Oil, Naphtha / Light Oil, Gasoline-range fuels, Syngas, and Others), By Feedstock Type (Polyolefins (PE, PP), Polystyrene (PS), Polyethylene Terephthalate (PET), and Mixed Plastic Waste), and Regional Forecast, 2026-2034

Plastic to Fuel Market Size and Industry Overview

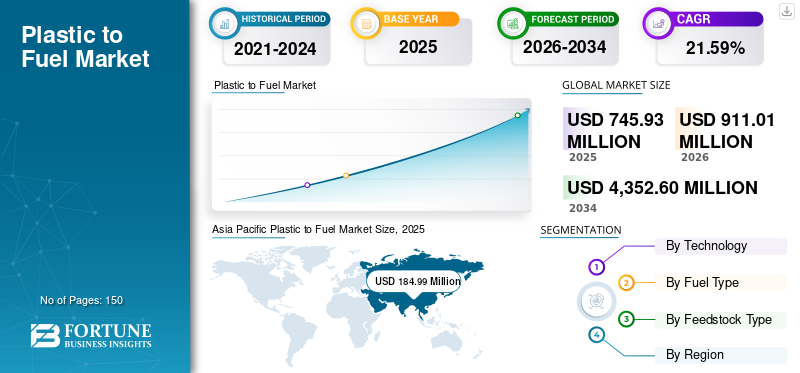

The global plastic to fuel market size was valued at USD 745.93 million in 2025 and is expected to reach USD 911.01 million by 2026. The market is projected to reach USD 4,352.60 million by 2034, with a CAGR of 21.59% over 2026-2034. Asia Pacific dominated the plastic to fuel market with a market share of 24.79% in 2025.

Governments in India and Japan are enforcing strict recycling and waste-to-energy mandates, promoting a circular economy to reduce pollution. The market is expected to experience high growth due to increasing industrialization and the need to process rising volumes of industrial and municipal plastic waste.

Plastic to Fuel (PTF) is a chemical recycling process that converts non-recyclable or difficult-to-recycle waste plastics into usable energy products, primarily synthetic crude oil, diesel, gasoline, and hydrogen. This technology breaks down polymer chains using heat (pyrolysis), catalysts, or gasification in the absence of oxygen to turn waste into high-value energy, addressing both plastic pollution and the need for alternative fuels.

Brightmark is a notable player in the plastic-to-fuel industry, focusing on turning waste plastics into fuels and wax using proprietary pyrolysis technology. While Brightmark is a key innovator in North America, other companies in the global market include Agilyx Corporation, Brightmark LLC, Plastic Energy Ltd. Quantafuel ASA, and Nexus Circular.

Download Free sample to learn more about this report.

Plastic to Fuel Market Key Takeaways

- 2025 Market Size: USD 745.93 million

- 2026 Market Size: USD 911.01 million

- 2034 Forecast Market Size: USD 4,352.60 million

- CAGR: 21.59% (2026–2034)

- Asia Pacific dominated the market with a 24.79% share in 2025.

- The pyrolysis segment dominated the market with a 72.84% share in 2025.

- The naphtha/light oil segment accounted for the largest market share of 38.95% in 2025.

Asia Pacific

Asia Pacific generated USD 184.99 million in 2025 and is projected to reach USD 229.03 million in 2026.

North America

North America held USD 157.40 million in 2025.

Europe

Europe accounted for USD 138.53 million in 2025.

U.S.

U.S. market reached USD 137.96 million in 2025, accounting for approximately 18.50% of the global market.

Japan

Japan market reached USD 21.64 million in 2025, accounting for approximately 2.90% of global revenues.

Read More

PLASTIC TO FUEL MARKET TRENDS

Transition toward Circular Economy and Refinery Integration Shapes Market Trends

The plastic-to-fuel market is increasingly aligned with circular economy goals, where waste plastics are converted into valuable fuel products or feedstock for petrochemical processes. Companies are integrating plastic conversion technologies with existing refinery infrastructure to improve efficiency and product quality.

- For instance, in March 2026, Re Sustainability and Indian Oil Corporation signed a MoU to launch India's first national initiative for collecting and recycling used lubricating oil. The partnership targets structured recovery of 100 KTA annually, building re-refining facilities to produce Group I/II+ base oils, fostering a circular economy, reducing crude imports, and enhancing environmental sustainability.

This trend is driven by rising regulatory pressure to reduce plastic waste and carbon emissions while maximizing resource recovery. Advanced recycling technologies are gaining traction as they enable the conversion of non-recyclable plastics into usable fuels, supporting sustainability objectives. Additionally, partnerships between waste management firms, technology providers, and oil companies are accelerating commercialization. This integration enhances scalability and economic viability, positioning plastic-to-fuel as a key solution in global waste management and energy recovery systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Plastic Waste Generation and Limited Recycling Options is Driving the Market

The rapid growth in global plastic consumption has resulted in a significant increase in plastic waste, much of which cannot be effectively managed through traditional recycling methods. Mechanical recycling is limited by contamination, degradation, and sorting challenges, leaving a large portion of plastic waste untreated. Plastic-to-fuel technologies provide an alternative pathway to handle this non-recyclable waste by converting it into usable energy products.

- In September 2025, NETL announced advancements in carbon capture research, focusing on membrane technologies for steel plant emissions and direct air capture field tests at the National Carbon Capture Center. These initiatives aim to lower costs and enhance CO2 separation efficiency for industrial applications, supporting U.S. decarbonization goals through scalable, high-purity capture solutions.

Governments and industries are seeking solutions to reduce landfill dependency and environmental pollution, which is further driving the adoption of these technologies. The ability to process mixed and contaminated plastics makes plastic-to-fuel an attractive option. As waste volumes continue to rise, the demand for efficient and scalable waste conversion solutions is expected to strongly support the plastic to fuel market growth.

MARKET RESTRAINTS

High Capital Investment and Operational Complexity Restrains Market Growth

Plastic-to-fuel technologies require substantial initial investment for plant construction, advanced equipment, and integration with existing systems. The complexity of these processes, including feedstock preparation, temperature control, and emission management, adds to operational costs. Additionally, inconsistent feedstock quality can impact process efficiency and product yield, making it difficult to maintain stable operations. Smaller players often face challenges in securing financing due to the perceived risks associated with emerging technologies. Regulatory compliance and environmental standards further increase costs, particularly in developed regions. These financial and technical barriers can slow down project deployment and limit market expansion. As a result, despite strong potential, the adoption of plastic-to-fuel solutions may be constrained by economic feasibility concerns in certain regions.

MARKET OPPORTUNITIES

Expansion in Emerging Markets with High Waste Availability is Expected to Create Lucrative Opportunities

Emerging economies present significant opportunities for the plastic-to-fuel market due to their rapidly growing plastic consumption and limited waste management infrastructure. Many of these regions face challenges related to landfill overflow and environmental pollution, creating a strong need for alternative waste treatment solutions. Plastic-to-fuel technologies can address these issues by converting abundant plastic waste into valuable energy products. Lower labor and operational costs in these regions further enhance project viability. Governments are increasingly exploring policies and incentives to promote waste to energy solutions, opening doors for investment and technology deployment. Additionally, partnerships with local authorities and private stakeholders can facilitate infrastructure development. This expanding market landscape offers substantial growth potential for companies seeking to scale their operations globally.

MARKET CHALLENGES

Feedstock Variability and Supply Chain Constraints Creates Challenges for Market Growth

One of the major challenges in the plastic-to-fuel market is the variability in feedstock composition, which can significantly affect process efficiency and output quality. Mixed plastic waste often contains contaminants, moisture, and different polymer types, requiring extensive pre-treatment and sorting. Inconsistent supply chains and lack of organized waste collection systems further complicate feedstock availability. This unpredictability can lead to operational disruptions and increased costs. Additionally, competition with mechanical recycling for high-quality plastic waste can limit access to suitable feedstock. Ensuring a steady and reliable supply of appropriate materials is critical for maintaining plant performance and profitability. Addressing these challenges requires investment in advanced sorting technologies and improved waste management infrastructure.

Segmentation Analysis

By Technology

Pyrolysis Membranes are Dominant Due to High Efficiency

Based on technology, the market is classified into pyrolysis, gasification, Hydrothermal Liquefaction (HTL), and catalytic depolymerization.

In 2025, pyrolysis dominated the with a market share of 72.84% due to its proven efficiency in converting diverse waste into high-quality fuels such as diesel and gasoline.

Hydrothermal Liquefaction (HTL) emerges as the fastest-growing segment with an estimated CAGR of 26.35% over the forecast period, leveraging water-based processes for superior handling of wet plastics and biomass, promising scalable, low-emission alternatives amid rising sustainability demands.

By Fuel Type

Naphtha/light Oil Fuel Hold Largest Share Due to Versatility in Petrochemical Production

Based on fuel type, the market is classified into diesel / fuel oil, naphtha / light oil, gasoline-range fuels, syngas, and others.

In 2025, the naphtha/light oil dominated by accounting for a market share of 38.95%, prized for their versatility in petrochemical production and high market value from mixed plastic feedstocks.

The diesel / fuel oil emerges as the fastest-growing segment with a CAGR of 21.06%, driven by surging industrial demand, maritime shipping needs, and advancements in refining yields from pyrolysis processes.

To know how our report can help streamline your business, Speak to Analyst

By Feedstock Type

Polyolefins (PE, PP) Lead Due to its High Yield Offering Over its Counterparts

Based on feedstock type, the market is classified into Polyolefins (PE, PP), Polystyrene (PS), Polyethylene Terephthalate (PET), and mixed plastic waste.

In 2025, Polyolefins such as polyethylene (PE) and polypropylene (PP) dominated the plastic to fuel market share with 53.89%, offering high yields of valuable fuels due to their simple hydrocarbon structures ideal for pyrolysis conversion.

Mixed plastic waste emerges as the fastest-growing segment with a CAGR of 23.35%, fueled by abundant availability, cost-effective collection from diverse sources, and innovations enabling efficient processing of challenging blends.

Plastic to Fuel Market Regional Outlook

By geography, the Market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Plastic to Fuel Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the largest share in 2025, valued at USD 184.99 million and is estimated to reach USD 229.03 million in 2026. The region leads the plastic-to-fuel market growth through massive plastic waste volumes from rapid urbanization and industrialization in China, India, and Southeast Asia. Supportive government policies promote renewable energy technologies, while investments in waste management infrastructure accelerate adoption of pyrolysis and gasification plants for local fuel production.

China Plastic to Fuel Market

The Chinese market reached around USD 58.80 million in 2025, accounting for roughly 7.88% of the global revenues. China drives explosive market growth through massive plastic waste fuel generation from its manufacturing dominance and urban expansion. The 2018 import ban shifted focus to domestic processing, spurring pyrolysis plants and policy support for energy recovery. Investments in advanced technologies address landfill pressures, positioning China as Asia Pacific's leader amid rising sustainability mandates and circular economy initiatives.

India Plastic to Fuel Market

India's market is projected to be one of the largest worldwide, with 2025 revenues reaching USD 44.29 million, representing approximately 5.94% of the global market.

Japan Plastic to Fuel Market

In 2025, Japan accounted for USD 21.64 million, accounting for approximately 2.90% of global revenues.

North America

The North American market hit USD 157.40 million in 2025 and exhibits strong growth fueled by advanced recycling, plastic to fuel technologies and favorable regulations addressing over thirty-five million tons of annual plastic waste, particularly in the U.S. Corporate sustainability initiatives and technological innovations drive scalable conversion facilities, positioning the region as a leader in high-efficiency fuel output.

U.S. Plastic to Fuel Market

With North America's strong contribution and the U.S. dominance in the region, the U.S. market’s 2025 estimation was USD 137.96 Million, accounting for roughly 18.50% of the global market.

Europe

Europe’s market valuation was at USD 138.53 million in 2025 as it advances steadily via stringent circular economy mandates and the Green Deal, increasingly investing in plastic recycling for energy recovery across Germany, France, and the U.K. Sustainability ambitions reduce landfill dependency, boosting chemical recycling and waste-to-fuel projects that align with broader emission reduction goals.

Germany Plastic to Fuel Market

The German market accounted for USD 33.70 million in 2025 and is projected to reach USD 41.95 million in 2026, representing approximately 4.52% of the global industry revenues.

Latin America

Latin America is expected to witness moderate growth during the forecast period. The market is set to reach a valuation of USD 159.99 million in 2026. Latin America shows promising expansion in Brazil, Mexico, and Argentina, where industrial hubs generate substantial plastic to fuel conversion. Rising environmental regulations and infrastructure investments promote sustainable practices, fostering market penetration through technological adoption and circular economy principles.

Brazil Plastic to Fuel Market

Brazil's market achieved USD 67.21 million in 2025, accounting for a very minor share of the global market.

Middle East & Africa

The Middle East & Africa accounted for a market share of 14.08% in 2025 valued at USD 105.02 million. The region experiences emerging growth amid increasing waste challenges and energy diversification efforts. Limited data highlights potential in urban centers, where oil-rich nations explore alternatives and African countries invest in waste-to-energy to address pollution and energy access, though infrastructure lags hinder pace.

GCC Plastic to Fuel Market

The GCC market is projected to reach approximately USD 56.86 million in 2025, accounting for around 7.62% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors Increasing Market share via Partnerships, Business Expansion, And Technological Advancement

The global market is consolidated, featuring a mix of major global and regional market players. Top-tier companies include Agilyx Corporation, Brightmark LLC, Plastic Energy Ltd., Quantafuel ASA, and Nexus Circular. In March 2026, TotalEnergies and Plastic Energy launched France's first advanced plastics recycling plant at the Grandpuits zero-crude site, processing 15,000 tons of hard-to-recycle household plastic waste annually via pyrolysis into synthetic oil feedstock. This milestone supports circular economy goals, diverting waste from landfills and incineration while advancing TotalEnergies' 30% recycled polymer target by 2030.

LIST OF KEY PLASTIC TO FUEL MARKET COMPANIES PROFILED

- Agilyx Corporation (U.S.)

- Brightmark LLC (U.S.)

- Plastic Energy Ltd. (U.K.)

- Quantafuel ASA (Norway)

- Nexus Circular (U.S.)

- Recycling Technologies Ltd. (U.K.)

- Vadxx Energy (Canada)

- Klean Industries Inc. (Canada)

- OMV AG (Austria)

- Shell plc (U.K.)

- ExxonMobil Corporation (U.S.)

- Chevron Phillips Chemical Company (U.S.)

- SABIC (Saudi Arabia)

- Licella Holdings Limited (Australia)

KEY INDUSTRY DEVELOPMENTS

- March 2026: CSIR-IICT signed a MoU with 2 Degrees Clicon Pvt. Ltd. to advance plastic-to-fuel technology, converting non-recyclable plastics such as snack packets into industrial fuels such as alternate diesel and petro polymer fuel. This Hyderabad collaboration promotes sustainable waste management and reduces fossil fuel reliance.

- March 2026: Neste has commissioned the world's largest facility at its Porvoo, Finland refinery to upgrade liquefied waste plastic (LWP) into high-quality petrochemical This investment processes up to 150,000 tons annually from hard-to-recycle plastics such as multi-layer packaging, scaling chemical recycling while cutting fossil use and emissions.

- March 2026: Cuba launched the Pyralis project in Holguín, employing pyrolysis to convert plastic waste into fuel. Processing 100 kg of plastic yields about 100 liters of pyrolysis oil, refinable into gasoline and diesel, aiding recycling and local energy needs.

- August 2025: US-China researchers developed a groundbreaking one-step method to convert toxic mixed plastic waste into petrol with over 95% efficiency at room temperature. Using light isoalkanes and catalysts, it produces gasoline-range hydrocarbons, chemical raw materials, and hydrochloric acid, promoting a scalable circular economy.

- February 2025: Petgas converts plastic waste into fuel via pyrolysis, processing 1.5 tons weekly to yield 365 gallons of gasoline, diesel, and kerosene with 50% fewer emissions than traditional fuels. Fuel is donated locally, aiming for a circular economy to combat Gulf of Mexico pollution.

REPORT COVERAGE

The global plastic to fuel market analysis provides an in-depth study of the market size & forecast by all the segments included in the report. It contains details on the market dynamics and industry trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The report also encompasses a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Market Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 21.59% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Technology, Fuel Type, Feedstock Type, and Region |

| By Technology |

|

| By Fuel Type |

|

| By Feedstock Type |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 745.93 million in 2025 and is projected to reach USD 4,352.60 million by 2034.

In 2025, Asia Pacific’s market value stood at USD 184.99 million.

The market is expected to exhibit a CAGR of 21.59% during the forecast period of 2026-2034.

The naphtha/light oil sector led the feedstock type segment.

Rising water scarcity along with increasing plastic waste generation and limited recycling options is driving the market.

Agilyx Corporation, Brightmark LLC, Plastic Energy Ltd., Quantafuel ASA, and Nexus Circular, are some of the prominent players in the market.

Asia Pacific dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us