Point-of-Entry Water Treatment Systems Market Size, Share & Industry Analysis, By Treatment Function (Water Softeners, Whole-House Filtration Systems, Problem Water Treatment Systems, Chemical & Contaminant Reduction Systems, and Disinfection Systems), By Water Source (Municipal Water Supply and Private Wells/Groundwater), By End User (Residential, Commercial, and Others), and Regional Forecast, 2026-2034

Point-of-Entry Water Treatment Systems Market Size and Future Outlook

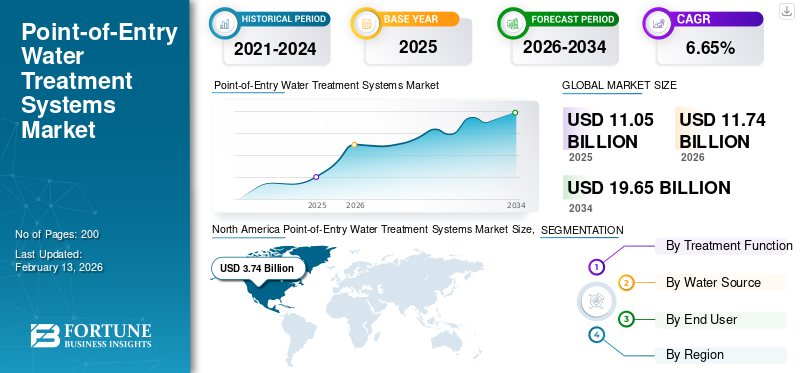

The global point-of-entry water treatment systems market size was valued at USD 11.05 billion in 2025. The market is projected to grow from USD 11.74 billion in 2026 to USD 19.65 billion by 2034, exhibiting a CAGR of 6.65% during the forecast period. North America dominated the global point-of-entry water treatment systems market with a market share of 33.85% in 2025.

The growth of point-of-entry (POE) water treatment systems is primarily driven by the increasing complexity and variability of water contamination at the source, particularly in residential and light commercial buildings. Aging municipal distribution networks, combined with the growing reliance on groundwater and mixed water sources, have led to higher concentrations of hardness minerals, heavy metals, sediment, and microbial contaminants entering buildings before point-of-use treatment can be effective. POE systems address this challenge by treating water at the building inlet, ensuring consistent water quality across all outlets. Point-of-entry water treatment systems, including water purification systems, treat all incoming water at the source to ensure safe, clean, and consistent water quality throughout the entire building.

Another key driver is the rising installation of centralized plumbing systems in new housing developments and multi-dwelling units, where whole-building treatment offers operational efficiency and long-term cost advantages. In regions with hard water, the increasing need to protect plumbing infrastructure, water heaters, and appliances from scale buildup and corrosion has accelerated the adoption of POE softeners and filtration systems. Additionally, stricter building codes and water quality standards in several countries now mandate treatment solutions that safeguard both potable and non-potable water uses within buildings.

- For instance, in March 2023, several residential communities in California, U.S., adopted point-of-entry water treatment systems in response to elevated levels of hardness and trace contaminants detected in groundwater supplies following prolonged drought conditions. Homebuilders and property managers installed centralized POE softening and filtration systems at building inlets to ensure uniform water quality across all households, protect plumbing infrastructure, and comply with updated state-level water quality and building code requirements.

Pentair plc is a global water solutions provider specializing in residential, commercial, and industrial water treatment technologies. The company offers a comprehensive portfolio of point-of-entry water treatment systems, including filtration, softening, and conditioning solutions, designed to improve water quality, protect plumbing infrastructure, and enhance operational efficiency. Point-of-entry water treatment systems, including water purification systems, are advanced water technology solutions that treat all incoming water at the source to ensure safe, clean, and consistent water quality throughout the building.

Download Free sample to learn more about this report.

POINT-OF-ENTRY WATER TREATMENT SYSTEMS MARKET TRENDS:

Increasing Adoption of Whole-House Water Purification Solutions Over Traditional POU Units is the Key Market Trend

The increasing adoption of whole-house water purification solutions over traditional POU units reflects a structural shift in how water quality challenges are being addressed at the building level. Unlike POU systems, which treat water at individual taps, whole-house point-of-entry (POE) systems respond to the growing recognition that contaminants often enter plumbing networks before reaching fixtures, affecting not only drinking water but also bathing, laundry, and appliance use. This shift has been accelerated by the rising incidence of hard-water scaling, pipe corrosion, sediment intrusion, and disinfectant byproducts, which impact the entire water distribution system on a property.

Whole-house systems are increasingly favored in new residential construction, multi-dwelling units, and light commercial buildings, where centralized treatment reduces long-term maintenance costs and ensures uniform water quality across all outlets. The trend is further reinforced by the need to protect water heaters, boilers, and smart plumbing fixtures, which are more sensitive to mineral buildup and particulate contamination.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Infrastructure-Level Water Quality Compliance in Residential and Commercial Buildings to Drive Market Size

The most influential drivers of the adoption of POE water treatment systems have been the tightening of infrastructure-level water quality compliance requirements across residential and commercial buildings. Increasing detection of contaminants such as lead, PFAS, iron, manganese, and microbial agents at distribution and source water levels has exposed the limitations of relying solely on municipal treatment or point-of-use solutions. As a result, building owners and developers are prioritizing treatment at the main water inlet to ensure consistent compliance across all water outlets.

- In 2025, updated plumbing and building safety codes in several regions began emphasizing whole-building water quality control, particularly for non-drinking applications such as bathing, laundry, and HVAC systems. These changes have driven demand for centralized POE systems capable of handling variable water chemistry before it interacts with internal plumbing networks. Point-of-entry water treatment systems, including water purification systems, are water technology solutions designed to reduce water pollution by treating all incoming water at the source and ensuring safe, clean water throughout the building.

MARKET RESTRAINTS

High System Integration and Retrofitting Complexity in Existing Buildings to Restrain Market Growth

During 2024-2025, one of the key restraints on the adoption of POE water treatment systems has been the technical and structural complexity of integrating them into existing buildings. Unlike point-of-use devices, POE systems must be installed at the main water inlet, requiring sufficient physical space, compatible plumbing layouts, and stable pressure conditions. Many older residential and commercial properties, particularly those constructed before modern plumbing standards, lack the clearance, drainage access, or pipe configuration needed to support centralized treatment units.

Retrofitting challenges are especially pronounced in urban multi-story buildings and densely populated housing complexes, where water inlets are often located in confined utility shafts or underground service rooms. Modifying these areas to accommodate POE systems can involve rerouting pipes, installing floor penetrations, or upgrading electrical systems for automated valves and monitoring modules.

MARKET OPPORTUNITIES

Integration of POE Systems in New Residential Developments and Smart Buildings Driving Growth Opportunities

The significant opportunity for POE water treatment systems is emerging through their integration into new residential developments, planned communities, and smart building projects. As urban expansion accelerates, developers are increasingly designing buildings with centralized mechanical rooms and standardized plumbing layouts, making it easier to incorporate POE systems at the construction stage rather than as retrofits. This shift allows water treatment to be embedded as a core utility, similar to electrical and HVAC systems.

- In 2026, smart buildings are expected to place greater emphasis on real-time resource monitoring and preventive infrastructure management, aligning closely with advanced POE systems equipped with sensors, automated regeneration, and performance diagnostics. These capabilities enable building managers to monitor water quality parameters, system efficiency, and maintenance requirements remotely, reducing operational downtime and extending equipment life.

MARKET CHALLENGES

Managing Variable Source Water Quality and System Performance Consistency Presents Significant Market Challenges

One of the most pressing challenges for POE water treatment systems is maintaining consistent performance amid highly variable source water quality. Many residential and light commercial buildings rely on groundwater or blended water supplies that experience seasonal fluctuations in mineral concentration, turbidity, microbial presence, and organic matter. These variations can strain POE systems designed around stable inlet parameters, leading to reduced treatment efficiency, premature media exhaustion, or frequent regeneration cycles.

Segmentation Analysis

By Treatment Function

Water Softeners are Dominant due to High Prevalence of Hard Water and Scale Issues

Based on treatment function, the market is classified into water softeners, whole-house filtration systems, problem water treatment systems, chemical & contaminant reduction systems, and disinfection systems.

In 2025, the water softeners dominated the market share. Water softeners dominate the point-of-entry water treatment systems segment primarily as hard water is widespread across residential and commercial water supplies. High concentrations of calcium and magnesium can cause scale buildup in pipes, water heaters, and appliances, leading to reduced efficiency, increased energy consumption, and higher maintenance costs. Water softeners address these issues at the inlet level, protecting the entire plumbing system and extending equipment lifespan.

The chemical & contaminant reduction systems segment is experiencing the highest point-of-entry water treatment systems market growth, with an 8.03% CAGR.

To know how our report can help streamline your business, Speak to Analyst

By Water Source

Municipal Water Supply is Dominant Due to Widespread Coverage and Consistent Year-Round Availability

Based on water source segmentation, the market is classified into municipal water supply and private wells/groundwater.

In 2025, the municipal water supply segment dominated the global market. Municipal water supply is a dominant source for point-of-entry water treatment systems due to its extensive coverage in urban and suburban areas and its consistent year-round availability. Although municipally treated water quality can deteriorate during distribution due to aging pipelines, residual disinfectants, and sediment intrusion.

The private wells/groundwater segment is expected to grow at a 5.90% CAGR.

By End User

Residential Segment Dominated Market Due to High Household Installations and Whole-House Treatment Demand

Based on end-user, the market is classified into residential, commercial, and others.

In 2025, the residential segment dominated the global market. This growth is primarily driven by the high volume of single-family homes and low-rise housing units that benefit from centralized whole-house water treatment. Homeowners increasingly install POE systems to address issues such as hard water, chlorine taste and odor, sediment, and aging distribution pipes that affect all household water outlets.

The commercial segment is expected to grow at a CAGR of 6.41%.

Point-of-Entry Water Treatment Systems Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Point-of-Entry Water Treatment Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest point-of-entry water treatment systems market share in 2025 at USD 3.74 billion and also expected to lead in 2026 with USD 3.94 billion.

North America leads market due to the widespread prevalence of hard water and aging municipal distribution infrastructure. Many residential and commercial buildings experience scale buildup, chlorine residuals, and secondary contamination, driving demand for whole-house treatment solutions.

U.S. Point-of-Entry Water Treatment Systems Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market reached at around USD 2.82 billion in 2025, accounting for roughly 25.52% of the global market.

Europe

Europe is projected to grow at 7.16% over the coming years, the third-highest among regions, and reached a valuation of USD 2.32 billion by 2025. Many European countries rely on groundwater sources with high mineral content, increasing demand for POE softening and filtration systems to prevent scale formation in plumbing and heating systems. The region’s widespread use of centralized heating and hot water systems makes inlet-level treatment critical for operational efficiency and equipment longevity.

Germany Point-of-Entry Water Treatment Systems Market

The German POE water treatment systems market in 2025 was around USD 0.61 billion. It is expected to reach USD 0.66 billion in 2026, representing roughly 5.54% of global point-of-entry water treatment systems revenues.

Asia Pacific

Asia Pacific reached USD 3.36 billion in 2025 and secured second place in the market. In the region, India and China reached USD 0.79 billion and USD 1.40 billion, respectively, in 2025.

Asia Pacific is a leading region in the market, driven by rapid urbanization, large-scale residential construction, and an increasing reliance on variable water sources. Many countries in the region depend on groundwater and mixed supplies that often contain high levels of hardness, iron, and microbial contaminants, creating strong demand for inlet-level treatment.

Japan Point-of-Entry Water Treatment Systems Market

The Japan POE water treatment systems market in 2025 was around USD 0.33 billion, accounting for roughly 2.95% of global point-of-entry water treatment systems revenues. In Japan, POE water treatment systems are driven by strict water quality standards and aging urban infrastructure.

China Point-of-Entry Water Treatment Systems Market

China’s POE water treatment systems market is projected to be significant worldwide, with 2025 revenues was around USD 1.40 billion, representing roughly 12.71% of the global market.

India Point-of-Entry Water Treatment Systems Market

The Indian POE water treatment systems market in 2025 was around USD 0.79 billion, accounting for roughly 7.12% of global revenues.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of USD 0.69 billion in 2025.

Latin America is witnessing growing adoption of POE water treatment systems as reliance on groundwater and decentralized water sources in residential and commercial buildings increases. Variability in water quality, including high mineral content and sediment presence, has heightened demand for centralized filtration and softening solutions.

Brazil Point-of-Entry Water Treatment Systems Market

Brazil's market value reached USD 2.84 billion in 2025, accounting for roughly 2.58% of the global market.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market reached USD 0.93 billion in 2025.

In the Middle East & Africa, point-of-entry water treatment systems are driven by high water hardness and reliance on desalinated and groundwater sources. Growing residential construction and the need to protect plumbing and appliances are supporting demand for centralized inlet-level treatment solutions.

GCC Point-of-Entry Water Treatment Systems Market

The GCC POE water treatment systems market reached USD 0.40 billion in 2025, accounting for roughly 3.63% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors Actively Expanding their Market Share via Partnerships, Business Expansion, and Technological Advancements

The global market is highly consolidated, with prominent players including 3M, DuPont, Pentair plc, BWT Holding GmbH, and others. Companies operating in the market are adopting targeted growth strategies to strengthen technical capabilities, expand their manufacturing presence, and improve access to high-demand sectors.

- For instance, in March 2024, a federal court granted final approval to 3M’s settlement with U.S. public water suppliers to address contamination from PFAS, or “forever chemicals,” in drinking water. Under the agreement, 3M will commit up to USD 10.3 billion over 13 years to support remediation and testing efforts for public water systems nationwide affected by PFAS detections. The settlement is part of the company’s broader shift away from PFAS manufacturing by the end of 2025, aimed at reducing environmental risk and supporting improvements in water quality.

Other key players in the global market include Culligan, Watts, Aquasana, Inc., and Calgon Carbon Corporation, among others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY POINT-OF-ENTRY WATER TREATMENT SYSTEMS COMPANIES PROFILED

- 3M (U.S.)

- BWT Holding GmbH (Austria)

- Watts (U.S.)

- DuPont (U.S.)

- Aquasana, Inc. (U.S.)

- Pentair plc (U.S.)

- Calgon Carbon Corporation (U.S.)

- Culligan (U.S.)

- EcoWater Systems LLC (U.S.)

- GE Appliances (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Pentair’s water solutions portfolio continued to gain recognition in the home water treatment sector, with independent reviews highlighting its whole-house filtration and softening systems for delivering reliable, high-quality water treatment with eco-friendly features.

- March 2025: DuPont Water Solutions launched the enhanced WAVE PRO online modeling tool for ultrafiltration design, helping water professionals plan and optimize water treatment systems across potable and industrial applications. The tool enables users to simulate various process conditions with high accuracy, thereby enhancing system selection and operational efficiency across diverse water-quality scenarios.

- January 2025: Calgon Carbon finalized a nine-year exclusive supply agreement with American Water to support PFAS treatment at more than 50 sites across 10 U.S. states. Under the deal, Calgon Carbon will provide granular activated carbon products, equipment, and reactivation services through 2033 to help treat contaminants in drinking water, enhancing regional utility capability to meet environmental standards and protect communities.

- September 2024: Danish manufacturer Grundfos completed the acquisition of Culligan’s Commercial & Industrial (C&I) division, including operations in the U.K., Italy, and France. The transaction expanded Grundfos’s advanced water-treatment technology capabilities while enabling Culligan to further focus on residential and local-dealer network water-treatment solutions globally.

- May 2023: DuPont Water Solutions was named Water Technology Company of the Year at the Global Water Awards, recognizing its deployment of advanced purification technologies, including FilmTec nanofiltration membranes in major municipal drinking water upgrade projects such as the Jiaxing drinking water plant in China, helping address pollutants and improve water security for a growing urban population. This award highlighted DuPont’s role in advancing sustainable water-treatment technologies worldwide.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.65% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Treatment Function, Water Source, End User, and Region |

|

By Treatment Function |

· Water Softeners · Whole-House Filtration Systems · Problem Water Treatment Systems · Chemical & Contaminant Reduction Systems · Disinfection Systems |

|

By Water Source |

· Municipal Water Supply · Private Wells/Groundwater |

|

By End User |

· Residential · Commercial · Others |

|

By Region |

· North America (By Treatment Function, Water Source, End User, and Country) o U.S. o Canada · Europe (By Treatment Function, Water Source, End User, and Country) o U.K. o Germany o France o Spain o Italy o Rest of Europe · Asia Pacific (By Treatment Function, Water Source, End User, and Country) o China o India o Japan o Australia o South Korea o Rest of Asia Pacific · Latin America (By Treatment Function, Water Source, End User, and Country) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Treatment Function, Water Source, End User, and Country) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.05 billion in 2025 and is projected to reach USD 19.65 billion by 2034.

In 2025, North Americas market value stood at USD 3.74 billion.

The market is expected to grow at a CAGR of 6.65% over the forecast period.

The water softeners segment led the market by treatment function.

Rising variability in source water quality and increasing hardness levels are driving demand for whole-building water treatment at the inlet level. Growing residential construction and the need to protect plumbing systems and appliances from scale and corrosion further support the adoption of point-of-entry water treatment systems.

3M, DuPont, Pentair plc, and BWT Holding GmbH, among others are prominent players in the market.

North America dominated the market in 2025.

An increased focus on whole-house water quality control and long-term protection of plumbing and appliances is expected to favor the adoption of point-of-entry water treatment systems.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us