Powerships Market Size, Share & Industry Analysis, By Power Output (Below 100 MW, 100-250 MW, 250-500 MW, and Above 500 MW), By Fuel Type (Liquefied Natural Gas (LNG), Heavy Fuel Oil (HFO), Diesel, and Coal), By Application (Commercial and Defense), and Regional Forecast, 2026-2034

POWERSHIPS MARKET SIZE AND FUTURE OUTLOOK

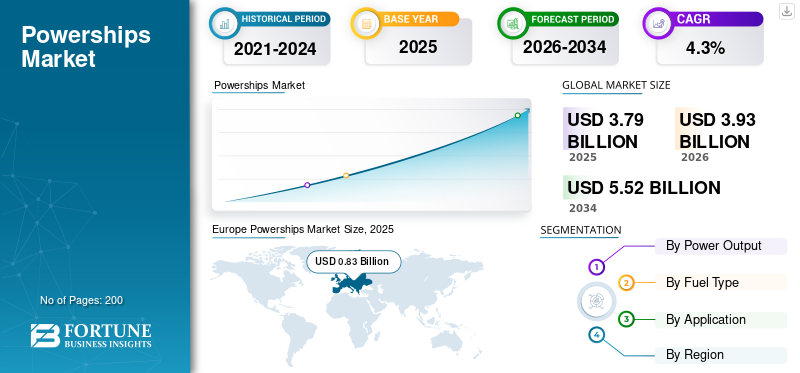

The global powerships market size was valued at USD 3.79 billion in 2025. The market is projected to grow from USD 3.93 billion in 2026 to USD 5.52 billion by 2034, exhibiting a 4.3% CAGR during the forecast period. Europe dominated the global powerships market with a market share of 21.9% in 2025.

Powerships are mobile, floating power generation units that are typically anchored in ports or coastal areas to provide a quick and flexible energy solution. These ships are equipped with advanced power generation technology, often utilizing diesel engines or gas turbines. They can produce electricity on demand to complement local energy grids, especially during peak demand times or in regions facing energy shortages.

The market analysis reveals a strong trajectory of growth, highlighting the increasing reliance on floating power solutions to address energy shortages in emerging economies. These floating power plants offer a rapid and flexible solution for providing electricity, allowing countries to address urgent energy needs without the lengthy processes associated with traditional power generation infrastructure. Innovations in technology and advancements in ship design have further enhanced their capabilities, making them more efficient and environmentally friendly. Additionally, the push for sustainable energy sources and the need for resilient power systems in the face of climate change have prompted governments and private investors to explore powerships as a viable alternative. As a result, the market has attracted considerable investments and expanded into various sectors, including emergency power supply, grid support, and renewable energy integration, positioning itself as a crucial player in the evolution of global energy solutions.

The global market is led by a small group of specialized players due to high capital requirements, complex regulatory approvals, and the need for combined marine and power-generation expertise. Karpowership (Karadeniz Holding) is the clear market leader, owing to its first-mover advantage, the largest installed fleet with over 7 GW of capacity, rapid deployment capabilities, and an integrated business model covering financing, installation, and long-term operation under PPAs. Wärtsilä and MAN Energy Solutions play critical roles as leading technology providers, supplying high-efficiency, fuel-flexible engines and power systems that enable reliable baseload and transitional LNG-based floating power solutions. Siemens Energy and GE Vernova contribute advanced turbines, generators, and grid-integration technologies, particularly for large-scale or gas-based floating power projects.

Download Free sample to learn more about this report.

Powerships Market Key Takeaways

- 2025 Market Size: USD 3.79 billion

- 2026 Market Size: USD 3.93 billion

- 2034 Forecast Market Size: USD 5.52 billion

- CAGR: 4.3% from 2026-2034

- Europe dominated the powerships market with a 21.9% share in 2025.

- The 250–500 MW segment is projected to grow at a CAGR of 5.9% during the forecast period.

- The Heavy Fuel Oil (HFO) segment is expected to register a CAGR of 4.6% during the forecast period.

Europe

Europe is projected to be the fastest-growing regional market, registering a CAGR of 5.3% during the forecast period.

Asia Pacific

Asia Pacific held strong market demand in 2025, supported by rising investments in maritime infrastructure.

North America

North America is witnessing steady growth due to increasing naval modernization and maritime security initiatives.

U.S.

The market is projected to grow at a CAGR of 4.5% during the forecast period.

Japan

Expanding maritime capabilities and rising demand for special purpose ships are supporting market growth.

Read More

POWERSHIPS MARKET TRENDS

Powerships Evolve from Emergency Power to Long-Term, Gas-Based Transition Energy Solutions

The market is currently shaped by a shift from short-term emergency power toward longer-tenure, transition power solutions, driven by grid instability, delayed onshore capacity additions, and fuel diversification goals in emerging economies. A key trend is the growing move from Heavy Fuel Oil (HFO) to gas-based and dual-fuel powerships, with LNG increasingly favored due to lower emissions and compliance with tightening environmental regulations; new deployments over the past few years have been predominantly gas or dual-fuel capable.

Another major development is the use of powerships as interim baseload assets, where contracts are extending from typical 3-5 years to 10-20 years, reflecting their role in bridging renewable integration gaps and replacing aging thermal plants. The market is also seeing larger unit sizes, with individual powership capacities now commonly exceeding 200-500 MW, improving economies of scale for utilities. Overall, powerships are increasingly positioned not just as stop-gap solutions, but as strategic, fast-deployable power infrastructure aligned with energy transition and energy security objectives.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Global Demand for Efficient and Flexible Energy Solutions Supports Market Growth

The powerships market growth is propelled by several key drivers that cater to the growing global demand for efficient and flexible energy solutions. First and foremost, the increasing need for reliable power supply in developing regions and areas affected by natural disasters is a significant factor driving the market development. These ships provide rapid deployment capabilities, allowing them to address urgent energy needs seamlessly. Additionally, the rise in offshore renewable energy projects, such as wind and solar, has generated further interest in energy-efficient ships as they can serve as flexible power sources that complement existing grid systems and enhance energy security.

The technological advancements in power generation, including the integration of hybrid systems that utilize both traditional and renewable energy sources, are also stimulating market growth. Moreover, the ongoing global shift toward cleaner energy solutions, supported by stronger regulatory frameworks and policies aimed at reducing carbon emissions, is encouraging innovation among ship manufacturers.

MARKET RESTRAINTS

High Capital Investments Required for Construction Opens Up Ways for Other Alternative Options

The high capital investment required for the construction of special purpose ships often leads stakeholders to explore alternative energy solutions that may present lower upfront costs and financial risks. For instance, onshore renewable energy projects, such as solar farms and wind installations, can typically be developed at a more manageable scale and have become increasingly cost-competitive due to advancements in technology and economies of scale. Additionally, battery storage systems are gaining traction as they offer flexible and efficient energy management, allowing for the integration of intermittent renewable sources without the significant capital burden associated. Furthermore, microgrid systems and localized energy solutions can address specific community needs without requiring extensive investments in floating power generation. As a result, the necessity for a large initial capital outlay for special purpose ships may compel investors and energy planners to consider these alternative options that align more closely with budget constraints and evolving energy demands.

MARKET CHALLENGES

Regulatory and Environmental Scrutiny to Hinder Market Growth and Pose a Critical Challenge to Market Growth

Regulatory and environmental scrutiny is emerging as one of the most critical constraints on the market, as governments, port authorities, and local communities increasingly challenge the environmental footprint of floating fossil-fuel-based generation. Powerships operating on heavy fuel oil or diesel face rising opposition due to concerns around air emissions, marine pollution, and alignment with national decarbonization commitments, leading to tighter permitting processes, operational restrictions, and in some cases early contract terminations or non-renewals. Environmental impact assessments are becoming more stringent, project approval timelines are lengthening, and compliance costs are rising due to the need for emissions control systems, fuel switching, or partial gas conversion. This scrutiny is particularly pronounced in regions adopting net-zero roadmaps, where powerships are now expected to demonstrate a clear role as temporary or transition assets rather than long-term baseload solutions. As a result, regulatory risk has become a key factor influencing project bankability, contract duration, and technology selection across the market.

For instance, Karpowership has increasingly emphasized gas-fired and dual-fuel powership deployments, positioning LNG-based floating power as a lower-emission transition solution in response to regulatory pressure and public scrutiny in multiple host countries.

SEGMENTATION ANALYSIS

By Power Output

Growing Demand for Rapid-response Power Solutions is Driving 100-250 MW Segment Growth

By power output, the market is classified into below 100 MW, 100-250 MW, 250-500 MW, and above 500 MW.

The 100-250 MW segment is currently dominating the market due to its balanced capacity that meets the energy demands of both developing and developed regions. This capacity range provides sufficient power generation to supply large industrial applications, infrastructure projects, and urban centers without the excessive costs and logistical challenges associated with larger ships. Moreover, the growing need for flexible, rapid-response power solutions in regions facing energy shortages or unreliable grid systems has driven demand for this segment. Ships within this range can be deployed quickly, offering an immediate solution to energy crises while supporting renewable energy integration and backup power needs. Furthermore, the ability to adapt to varying fuel sources, including LNG, makes the 100-250 MW power output segment an attractive option for operators looking to reduce their carbon footprint while still ensuring energy security. As countries increasingly focus on energy resilience and diversification, this segment's dominance is likely to continue as it effectively bridges the gap between traditional power generation methods and the shift toward more sustainable energy practices.

The 250-500 MW is anticipated to rise with a CAGR of 5.9% over the forecast period. The 250-500 MW power output segment is expected to experience significant growth during the forecast period, driven by several key factors that position it as an attractive solution for large-scale energy needs. As countries strive to enhance their energy infrastructure and meet growing electricity demands, powerships of this capacity range provide a robust and scalable option for utility-scale projects. Additionally, ongoing investments in technology and advancements in maritime engineering are expected to enhance the performance and competitiveness of this segment, making 250-500 MW power output a preferred choice for countries looking to bolster their energy security and sustainability efforts in the coming years.

By Fuel Type

Liquefied Natural Gas (LNG) Segment Dominated Market Due to Its Ability to Produce Low Carbon Emissions

Based on fuel type, the market is divided into Liquefied Natural Gas (LNG), Heavy Fuel Oil (HFO), diesel, and coal.

The Liquefied Natural Gas (LNG) segment has emerged as the dominant fuel type within the market, capturing significant attention due to its numerous advantages over traditional fuels. As global demand for cleaner energy sources intensifies, LNG stands out due to its lower carbon emissions and reduced environmental impact compared to oil-fired and diesel-fired engines. This shift is particularly important in regions striving to meet stricter environmental regulations and transition toward more sustainable energy practices. Additionally, LNG-fueled ships are engineered for higher operational efficiency, enabling them to generate reliable energy while minimizing operational costs. The infrastructure for LNG supply is also expanding, facilitating easier access and logistics for powership operations. With technological advancements enhancing the performance and safety of LNG utilization and the growing emphasis on energy security, the LNG segment is well-positioned to lead the market growth in the coming years, catering to the needs of both emerging economies and developing nations.

The Heavy Fuel Oil (HFO) is anticipated to rise with a CAGR of 4.6% over the forecast period, driven by several factors despite the increasing shift toward cleaner fuels. HFO remains a cost-effective option for many shipping and power generation operators, particularly in regions where capital and operational expenditures favor established, lower-cost energy sources.

To know how our report can help streamline your business, Speak to Analyst

By Application

Growing Focus on Cost-effective Operations is Supporting Demand across Commercial Segment

Based on application, the market is divided into commercial and defense.

The commercial segment is currently dominating the competitive landscape, driven by the burgeoning demand for reliable and flexible energy solutions across various industries. As businesses look to optimize their operations amid fluctuating energy prices and increasing regulatory pressures, powerships provide a viable alternative by offering quick deployment and scalability for power generation. This flexibility is particularly advantageous for commercial enterprises operating in remote or underserved regions where traditional grid connections may be unreliable or non-existent. Additionally, the ability of these ships to utilize a range of fuel types, including LNG, HFO, and renewables, further enhances their appeal. The commercial sector's ongoing investment in infrastructure and capacity expansion, coupled with the rising need for energy security and resilience amidst global energy transitions, solidifies the position of the commercial segment.

The defense segment is anticipated to witness significant growth with the CAGR growing up to 4.7% in the coming years, driven by increasing global security concerns and the modernization of naval fleets. As nations invest in enhancing their maritime capabilities, the demand for versatile special-purpose ships used for various defense operations, including surveillance, logistics, and amphibious assaults has surged. The versatility of powerships, which can operate in diverse environments and respond to a range of military scenarios, makes them an attractive solution for naval forces. As governments prioritize defense spending to address emerging threats, the special-purpose ships segment is poised for robust growth, reflecting the evolving dynamics of modern military strategies.

POWERSHIPS MARKET REGIONAL OUTLOOK

The market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

Europe

Europe Powerships Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Europe is projected to be the fastest-growing region in the market, with a CAGR of 5.3% over the forecast period, and is expected to maintain a significant market share. This growth is supported by advanced maritime engineering capabilities, strong port infrastructure, and increasing investments in energy security and grid resilience. Several European countries are prioritizing flexible and cleaner power solutions to manage energy transition challenges, including renewable intermittency and supply disruptions. Additionally, rising focus on emergency preparedness, offshore energy support, and strategic energy backup capacity is further strengthening demand for specialized floating power solutions across the region.

Germany Powerships Market

Germany is anticipated to rise with a CAGR of 4.9% over the forecast period. Germany held the highest share of power plant deployment primarily due to its acute short-term capacity requirements triggered by structural energy transitions and external supply shocks. Following the accelerated nuclear phase-out and coal exit commitments, Germany faced periods of tight reserve margins, which were further intensified by disruptions in pipeline gas supply. In response, powerships and floating power barges were leveraged as rapid, grid-connected interim solutions, particularly to support gas-fired generation and ensure grid stability during peak demand and winter months.

Asia Pacific

Asia Pacific held a strong demand for market in 2025, driven by a combination of rapid industrialization, increasing energy demands, and strategic military investments among its nations. China, India, and Japan are significantly expanding their maritime capabilities to address both economic growth and security challenges, leading to a surge in demand for special purpose ships, which are crucial for both commercial and defense applications.

China Powerships Market

In Asia Pacific, China holds the highest market share primarily due to its strong industrial ecosystem, rather than widespread domestic deployment of powerships for grid power. China dominates the region through its shipbuilding capacity, power equipment manufacturing strength, and EPC integration capabilities, enabling the development and export of floating power plants to overseas markets. China is anticipated to rise with a CAGR of 4.6% over the forecast period.

North America

North America, led by the U.S., continues to focus on modernizing its naval fleet and ensuring maritime security, prompting heightened interest in versatile power vessels for strategic military operations. Additionally, the emphasis on sustainability and the need for reliable power generation systems in response to climate change are propelling the development and deployment of hybrid and renewable-powered ships in both regions.

U.S. Powerships Market

The U.S. is anticipated to rise with a CAGR of 4.5% over the forecast period. The growth of powerships in the U.S. is relatively limited compared to emerging markets, as the country has a well-developed and diversified power generation infrastructure. However, opportunities exist in niche applications such as emergency power supply following hurricanes and extreme weather events, particularly in coastal and island regions like Puerto Rico. Increasing climate-related grid disruptions and the need for rapid, temporary capacity deployment during peak demand or infrastructure outages may create selective demand.

Rest of the World

The Rest of the World dominates the market primarily as it includes Middle East & Africa and Latin America, where structural power deficits, rapid demand growth, and limited grid resilience make fast-deployable generation essential. Many countries in these regions face chronic capacity shortfalls, aging thermal plants, seasonal hydropower variability, or delayed onshore power projects, creating immediate demand for floating power solutions that can be commissioned within months rather than years. Key instances include the widespread use of power plants across Sub-Saharan Africa to stabilize national grids, deployments in the Middle East to support peak demand and fuel transition strategies, and projects in Latin America to offset drought-related hydroelectric shortages. In these markets, powerships are often contracted as multi-year baseload or interim capacity under government-backed PPAs, rather than short-term emergency assets. The Rest of the World hold 49.5% of the powerships market share across the globe.

COMPETTIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Major Market Players Emphasize Investments in R&D Activities to Develop Innovative Products

Karadeniz Holding is expected to be a leading key player in the market due to advancements in research and development and continuous innovation in the field of marine systems, innovative approach to mobile power generation, and its extensive experience in the sector. By leveraging advanced technologies and a fleet of efficient, environmentally friendly floating power plants, the company can rapidly deploy energy solutions to regions facing electricity shortages or crises. Moreover, Siemens is enhancing their capabilities in energy transition technologies, contributing to the market's expansion through innovative solutions that address both electricity generation and distribution needs. MAN Energy Solutions is also pivotal in this sector, focusing on the development of efficient marine engines that comply with stringent emissions regulations while optimizing fuel consumption.

LIST OF KEY POWERSHIPS COMPANIES PROFILED IN REPORT

- Karadeniz Holding (Turkey)

- Siemens (Germany)

- General Electric (U.S.)

- MAN Energy Solutions (Germany)

- Caterpillar (U.S.)

- Hyundai Heavy Industries (South Korea)

- Mitsubishi Heavy Industries (Japan)

- Rolls-Royce (U.K.)

- Wärtsilä (Finland)

- Aggreko (U.K.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Karpowership and Seatrium have celebrated the naming of Karadeniz LNGTS Americas, the fifth member of Karpowership's LNG Terminal Ship (LNGTS) fleet. The ceremony also saw both companies sign a strategic partnership to convert the Karpowership's next-generation Powership and LNGTS fleet.

- July 2025: Mitsui O.S.K. Lines, Ltd. (MOL), a leading global shipping company, entered into a Memorandum of Understanding (MoU) with Kinetics, the energy transition arm of Karpowership, a global leader in floating power solutions. The agreement aims to collaboratively develop an advanced next-generation Floating Data Center platform.

- March 2025: Karpowership, Turkiye’s builder, owner, and operator of floating power plants (powerships), has contracted German engine maker MAN Energy Solutions (MAN ES) to deliver dual-fuel engines for its newbuilds.

- August 2024: Karpowership, a leading international energy firm, announced to invest USD 1 billion in LNG-to-power infrastructure in Mozambique, which will serve the entire South African Power Pool (SAPP). This initiative aims to improve the energy framework within the country and the broader SAPP by delivering dependable and affordable electricity to 5 million people.

- July 2024: Karadeniz Holding, recognized for operating the world's largest fleet of floating power plants, partnered with Japan's Mitsui O.S.K. Lines (MOL) to develop a new powership under the KARMOL brand. The steel cutting ceremony for the vessel occurred on July 5 2024, at Sedef Shipyard, with plans to launch the ship by May 2026, as announced by the company.

- May 2024: Karpowership revealed that it had signed a memorandum of intent (MoI) with Brazil's Petrobras to leverage their combined expertise in the natural gas and power industries.

- April 2024: Seatrium announced that it would transform three LNG carriers into Floating Storage Regasification Units (FSRUs) for the Turkish company Karpowership, with the possibility of a fourth project in the future. The yard has successfully completed 11 FSRU conversions since 2007.

- January 2023: The Turkish Company, Karpowership entered into a Memorandum of Understanding (MoU) with the state-owned JSC Energy Company of Ukraine (ECU) aimed at strengthening cooperation in electricity supply. This partnership will expedite the deployment of 500 Megawatts (MW) of floating power stations to help address the country's energy crisis.

REPORT COVERAGE

The powerships market report includes detailed market analysis and focuses on key aspects such as leading companies, services, and product applications. Besides this, the report offers insights into the market trends and highlights vital industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the market's growth over recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.3% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Power Output

|

|

By Fuel Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

The market was valued at USD 3.79 billion in 2025 and is projected to reach USD 5.52 billion by 2034.

The market is expected to register a CAGR of 4.3% during the forecast period.

The market is driven by the need for immediate, flexible, and reliable energy solutions in a rapidly changing global energy landscape.

Europe is estimated to be the fastest-growing region during the forecast period.

Karadeniz Holding, Siemens, General Electric, MAN Energy Solutions, and Caterpillar are the leading players in the market.

Energy deficit & rapid electrification in emerging economies is providing ample of opportunities in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us