Precipitated Silica Market Size, Share & Industry Analysis, By Application (Tire Rubber, Oral Care, Food Feed, Industrial, and Others), and Regional Forecast, 2026-2034

Precipitated Silica Market Size and Future Outlook

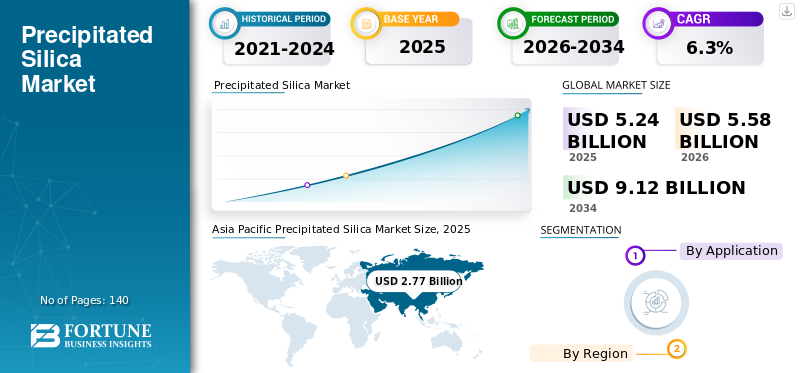

The global precipitated silica market size was valued at USD 5.24 billion in 2025. The market is projected to grow from USD 5.58 billion in 2026 to USD 9.12 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period. Asia Pacific dominated the precipitated silica market with a market share of 52.86% in 2025.

Precipitated silica is a synthetic amorphous silica generally produced through the reaction of sodium silicate with mineral acid, followed by precipitation, filtration, drying, and finishing. It is widely used as a reinforcing filler in tires and technical rubber, an abrasive and thickener in oral care, an anticaking and free-flow aid in food and feed, and a performance additive in silicone rubber, coatings, plastics, and other specialty industrial systems. Solvay identifies the tire industry, nutraceutics, and toothpaste among its main silica markets. At the same time, Quechen and Madhu Silica publicly show commercial exposure across rubber, oral care, animal nutrition, and silicone or broader industrial uses.

The market is dominated by several key players, including Solvay, Evonik Industries AG, Quechen Silicon Chemical Co., Ltd., and Madhu Silica Pvt. Ltd.

Download Free sample to learn more about this report.

PRECIPITATED SILICA MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 5.24 Billion

- 2026 Market Size: USD 5.58 Billion

- 2034 Forecast Market Size: USD 9.12 Billion

- CAGR: 6.3% from 2026–2034

- Asia Pacific dominated the market with a 52.86% share in 2025.

- Tire rubber was the largest application segment.

- Oral care was the second-largest application segment.

North America

North America is expected to reach USD 0.78 billion in 2026.

Europe

Europe is projected to reach USD 1.22 billion in 2026, growing at a CAGR of 5.5%.

Asia Pacific

Asia Pacific reached USD 2.77 billion in 2025 and remains the largest regional market.

U.S.

The market is projected to reach USD 0.73 billion in 2026, accounting for 13.0% of global sales.

Japan

The market is estimated to reach USD 0.28 billion in 2026, accounting for 5.0% of global revenue.

Read More

PRECIPITATED SILICA MARKET TRENDS

Functional Shift toward High-Dispersibility to Boost Market Development

A major market trend is the transition from broad-volume silica supply toward more specialized, higher-value grades designed for precise end-use performance. In tires, this is especially visible in highly dispersible silica used for green tires, where compound efficiency, wet grip, rolling resistance, and handling are critical. Solvay positions Zeosil Premium around top-tier tire-label performance, and Quechen markets easy-dispersible silica and dedicated industrial rubber grades aimed at advanced tire formulations.

The market is also moving toward lower-carbon and circular silica platforms. Solvay has expanded its circular silica strategy through bio-circular and waste-sand-based feedstock programs, including its Italy facility, inaugurated in January 2026, along with Asian plant conversions planned starting in 2026. Quechen has also published an SGS-verified product carbon footprint declaration for precipitated hydrated silica, indicating that carbon transparency is increasingly important in procurement, especially in global tire and consumer goods supply chains.

A parallel trend is the increasing use of application-specific specialty grades in oral care, food, feed, and silicone rubber. Quechen differentiates oral-care silica into dental thickener and dental abrasive grades, and also serves the animal nutrition and silicone rubber industries. This shift indicates that the market is no longer driven solely by bulk filler demand, but increasingly by controlled morphology, purity, dispersibility, and documentation.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Green and Energy-Efficient Tire Formulations is Supporting Market Growth

The key driver in the market is the expansion of green and energy-efficient tire formulations. Solvay explicitly states that its high-performance silica helps reduce rolling resistance and improve tire performance, linking this directly to fuel economy, CO2 reduction, and EV range extension. This makes precipitated silica strategically important for conventional vehicles and for electric vehicles, where efficiency gains are even more critical.

Broader mobility trends further reinforce this driver. The IEA reports that electric car sales exceeded 17 million in 2024, accounting for more than one in five cars sold globally. As EV adoption expands, tire makers continue to focus on balancing weight, grip, durability, and energy efficiency, all of which support silica-rich compound systems. Evonik’s decision to expand precipitated silica production in Charleston by 50% to meet regional demand, particularly from the tire industry, is a strong real-world indicator of ongoing structural demand.

A second major support factor is application diversification. Public producer disclosures show that the product is not dependent on a single end use. Solvay highlights tire, nutraceutics, and toothpaste; Quechen Silicon Chemical Co., Ltd. serves rubber, oral care, animal nutrition, and silicone rubber; and Madhu Silica markets over 50 grades across tires, oral care, detergents, food, pharmaceuticals, pesticides, and related uses. This broad range of products provides resilience to the market and helps stabilize growth when one downstream sector weakens.

MARKET RESTRAINTS

Energy-Intensive Production to Restrain Industry Expansion

Precipitated silica manufacturing is a relatively process-intensive chemical operation involving silicate chemistry, precipitation, separation, drying, and controlled finishing. This makes the industry sensitive to energy costs, sodium silicate pricing, acid inputs, environmental compliance, and logistics volatility. Even when demand remains positive, margin expansion can be limited by these upstream pressures. The decision by Evonik Industries to close two North American silica plants in 2025 while concentrating production at larger, more competitive hubs illustrates the importance of scale and operational efficiency in sustaining long-term profitability.

Another restraint is that the product cannot be readily substituted in high-value applications. In tire compounds, oral-care systems, food formulations, and specialty rubber, customers typically qualify chemistry composition and particle morphology, structure, dispersibility, purity, and handling behavior. Public supplier communications from Solvay, Quechen, and Madhu repeatedly emphasize specialized grades and technical performance, suggesting that switching suppliers or reformulating products can be slow and qualification-intensive. These dynamics moderate competitive turnover and can slow the pace at which newer grades achieve widespread commercial adoption.

MARKET OPPORTUNITIES

Growing Product Usage in Oral Care and Personal Care Formulations is Creating New Market Opportunities

One of the clearest opportunities in the market is lower-carbon and circular precipitated silica. Solvay first launched bio-circular silica in Europe and later broadened its circular strategy by announcing waste-sand-based raw material conversion in Asia, before inaugurating Europe’s first bio-circular silica facility in Italy in 2026. These moves indicate that sustainability is shifting from a branding theme toward a practical route for product differentiation and future premiumization, especially in tire-related applications tied to ESG and Scope 3 emission targets.

Another attractive opportunity lies in oral care and personal care formulations, where the product is used as a cleaning abrasive and as a rheology- and texture-control ingredient. Solvay’s Tixosil portfolio is positioned around toothpaste and oral-care performance, while Quechen offers distinct dental thickener and dental abrasive grades. This suggests that oral care remains one of the most promising specialty segments for value-added silica growth, rather than relying solely on volume-driven expansion.

The market shows continued growth potential in food and feed applications, where silica serves as an anticaking agent or carrier material. The U.S. FDA regulations permit the use of silicon dioxide for anticaking in food, and producers such as Quechen and Madhu Silica openly market grades for animal nutrition, anticaking, and other additive functions. While these applications are smaller than tire rubber in volume, they contribute to a more diversified and margin-stable market structure.

MARKET CHALLENGES

Challenge in Maintaining Consistent Quality across a Wide Range of Applications Hinders Market Growth

A central challenge for precipitated silica producers is improving performance and sustainability without rendering their products uneconomic for downstream customers. Tire manufacturers, oral-care formulators, and food or industrial users increasingly seek improved environmental profiles, while remaining highly cost-sensitive. Circular feedstocks, renewable energy integration, and carbon-footprint transparency can strengthen market positioning, yet they also require capital, certification, supply-chain redesign, and customer acceptance. Solvay’s circular silica investments and Quechen’s carbon footprint disclosures show that the market is moving in this direction, although the transition remains commercially complex.

Another challenge lies in maintaining consistent quality across a wide range of applications. The same broad product family serves tires, toothpaste, feed premixes, food powders, silicone rubber, and industrial systems, each with different purity, performance, documentation, and regulatory expectations. This raises the importance of process control, technical service, and global supply consistency. Producers with broader portfolios and stronger application support are therefore better placed than suppliers, primarily on commodity-focused suppliers.

Segmentation Analysis

By Application

To know how our report can help streamline your business, Speak to Analyst

Tire Rubber Segment Dominated the Market, Driven by Shift Toward Lower-Rolling-Resistance

In terms of application, the market is categorized into tire rubber, oral care, food feed, industrial, and others.

The tire rubber segment held the dominant precipitated silica market share. The shift toward lower-rolling-resistance and higher-performance tire compounds continues to drive silica consumption, especially in passenger-car and premium tire categories. Solvay’s silica portfolio is explicitly linked to energy-efficient tires, while Evonik’s Charleston expansion was justified by strong tire-linked demand in North America. Moreover, this segment is anticipated to expand at an annual compound growth rate of 6.2% over the study period.

The oral care segment remains the second-largest segment in the market and is anticipated to expand at an CAGR of 5.7% over the study period. The product is widely used in toothpaste systems for cleaning, polishing, thickening, and texture control. Quechen offers both dental abrasive and dental thickener silica, while Solvay identifies toothpaste as one of its main silica markets. This segment is attractive because product performance and consistency matter more than simple filler economics.

The food feed segment is smaller than tire rubber, but is strategically important as it provides regulatory-backed, diversified demand. U.S. FDA rules permit silicon dioxide as an anticaking agent in food, and Quechen and Madhu both market silica for feed or anti-caking related uses. This segment helps balance the cyclical exposure of the tire market and gives suppliers access to more specialized, compliance-driven niches.

Precipitated Silica Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Precipitated Silica Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region held the largest market share, reaching USD 2.59 billion, and maintained its leadership in 2025 with USD 2.77 billion. The region benefits from its concentration of tire manufacturing, oral-care production, technical rubber processing, and integrated chemical supply chains. Quechen’s broad market footprint in China and Madhu Silica’s large manufacturing base in India both reinforce the region’s position as the main center of both consumption and supply. By 2026, the Chinese market is anticipated to reach USD 1.67 billion.

China Precipitated Silica Market

China remains the most important country market within the Asia Pacific due to its scale in tire materials, consumer products, and specialty chemical production. Quechen presents itself as a major silica supplier with strong exposure to rubber, oral care, animal nutrition, and silicone rubber. This scale supports China’s role as both a volume market and a specialty-grade growth market.

To know how our report can help streamline your business, Speak to Analyst

Japan Precipitated Silica Market

The Japanese market is estimated to reach around USD 0.28 billion by 2026, accounting for roughly 5.0% of global revenue.

India Precipitated Silica Market

The Indian market is estimated at around USD 0.33 billion by 2026, accounting for roughly 5.9% of global revenues.

Europe

Europe is expected to experience substantial precipitated silica market growth in the coming years. The region is projected to grow at a CAGR of 5.5% and reach a valuation of USD 1.22 billion by 2026. Europe remains a high-value market due to its strong emphasis on tire performance, sustainability, regulated consumer applications, and premium industrial demand. Solvay’s silica business is closely tied to energy-efficient tires and premium application areas such as toothpaste and nutraceutics, and its circular silica investments in Europe highlight the region’s strategic importance for next-generation materials.

U.K. Precipitated Silica Market

The U.K. market is estimated at around USD 0.14 billion by 2026, accounting for roughly 2.4% of global revenues.

Germany Precipitated Silica Market

Germany’s market is estimated at around USD 0.26 billion by 2026, accounting for roughly 4.6% of global revenues.

North America

The North American market is expected to reach USD 0.78 billion by 2026. North America is a mature but attractive market, supported by tire manufacturing, oral-care demand, food-related silica uses, and increasing interest in regional supply resilience. Evonik’s Charleston expansion was explicitly tied to strong silica demand in North America, especially from the tire industry, and the project also supports more local silica sourcing for regional customers. By 2026, the U.S. market alone is projected to reach USD 0.73 billion.

U.S. Precipitated Silica Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market is expected to around USD 0.73 billion by 2026, accounting for roughly 13.0% of global sales.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions will experience moderate growth within this market. The Latin American market is projected to reach USD 0.32 billion by 2026. Latin America and the Middle East & Africa are smaller in scale than APAC, Europe, and North America, yet they are still relevant growth markets for the product. Demand is supported by tires, technical rubber, oral care, and selected industrial applications, often through import-supported supply chains or regional distributors. These regions are unlikely to dominate global demand, although they provide steady incremental growth and diversification opportunities for producers with export reach.

GCC Precipitated Silica Market

The GCC market in 2026 is estimated to reach USD 0.09 billion, accounting for approximately 1.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Specialized Grades, Dispersion Performance, and Application Support Are Strengthening Competitive Differentiation

The market is moderately concentrated, with a mix of global technology-driven producers and large regional suppliers. Competitive strength depends heavily on high dispersion performance, control of morphology, consistency, regulatory documentation, and application engineering support. In premium areas such as green tires, oral care, and regulated food or feed applications, these factors matter more than price alone. Solvay, Evonik Industries AG, Quechen Silicon Chemical Co., Ltd., and Madhu Silica Pvt. Ltd. all position their silica businesses around specialized grades and application-specific solutions rather than purely commodity-volume selling.

LIST OF KEY PRECIPITATED SILICA COMPANIES PROFILED

- Evonik Industries AG (Germany)

- Solvay (Belgium)

- Quechen Silicon Chemical Co., Ltd. (China)

- Madhu Silica Pvt. Ltd. (India)

- Qemetica Silica (Poland)

- Tosoh Corporation (Japan)

- Fuji Silysia Chemical Ltd. (Japan)

- PQ Corporation (U.S.)

- Oriental Silicas Corporation (Taiwan)

- Denka Company Limited (Japan)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Solvay inaugurated Europe’s first bio-circular silica facility in Livorno, Italy, aligned with sustainability targets and upcoming EU rules for tires.

- January 2025: Evonik announced Smart Effects, combining its silica and silanes businesses in a strategic move to strengthen advanced-materials positioning.

- December 2024: PPG completed the sale of its silica products business to Qemetica, transferring a precipitated silica portfolio serving major global customers.

- January 2024: Evonik announced a 50% precipitated silica capacity expansion at its Charleston, South Carolina, site to serve growing demand, especially from the tire industry in North America.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, with market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of % from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Application and Region |

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 5.24 billion in 2025 and is projected to reach USD 9.12 billion by 2034.

Recording a CAGR of 6.3%, the market is slated to exhibit steady growth during the forecast period.

In terms of application, the tire rubber segment led in 2025.

Asia Pacific held the highest market share in 2024.

Expansion of green and energy-efficient tire formulations is the key factor driving market growth.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us