Premium Packaging Market Size, Share & Industry Analysis, By Material (Plastic, Paper & Paperboard, Metals, Glass, and Others), By Packaging Type (Boxes & Cartons, Bottles & Jars, Sleeves & Slipcases, Inserts & Dividers, Tubes, and Others), By End-use Industry (Food & Beverages, Personal Care & Cosmetics, Apparel & Accessories, Consumer Goods, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

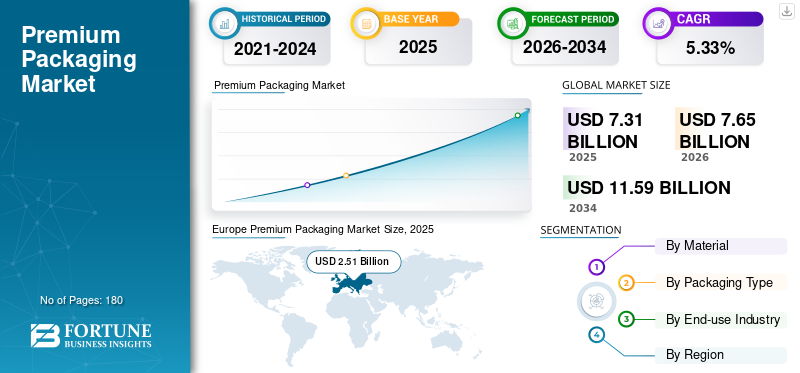

The global premium packaging market size was valued at USD 7.31 billion in 2025. The market is projected to grow from USD 7.65 billion in 2026 to USD 11.59 billion by 2034, exhibiting a CAGR of 5.33% during the forecast period. Europe dominated the global air premium packaging market with a market share of 34.34% in 2025.

Premium packaging refers to high-quality, value-added packaging that utilizes superior materials, distinctive designs, and advanced finishes to enhance brand image, product perception, and customer experience, typically associated with luxury or high-end products. The swift expansion of direct-to-consumer and e-commerce channels has generated a need for high-quality packaging that safeguards valuable items during shipping and enhances the customer experience during unboxing. This trend drives investments in engineered inserts, more robust rigid boxes, and premium mailer solutions that strike a balance between visual appeal and drop-test performance.

Furthermore, many key industry players, such as Smurfit Kappa, Huhtamäki Oyj, and Amcor Plc, operating in the market, are focusing on developing various innovative products and boosting the market development.

Download Free sample to learn more about this report.

PREMIUM PACKAGING MARKET TRENDS

Growing Demand for Digitally Enabled Packaging is a Prominent Trend Observed in the Market

Brands are progressively incorporating digital elements into high-end packaging to enhance storytelling, ensure authentication, and facilitate product traceability. Augmented reality experiences, QR Codes, and NFC tags enable brands to expand premium interactions beyond the physical packaging, combat counterfeiting, and collect data on post-purchase engagement. The growing demand for digitally enabled packaging is booming as a key trend.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Sustainability and Regulatory Pressure are Accelerating Market Growth

Brands and regulatory bodies are advocating for premium packaging to transition toward recyclable, reusable, and lower-carbon materials, aiming to minimize environmental impact. This shift is also driven by legislation, including EPR, single-use restrictions, and recycling targets, which compel packaging choices to be made further up the value chain. Consequently, premium and luxury brands are increasingly utilizing glass, mono-materials, and recyclable composites, even at a higher cost, as sustainability now conveys legitimacy and mitigates regulatory risks. Henceforth, the increasing sustainability and regulatory pressure drive the global premium packaging market growth.

MARKET RESTRAINTS

High Material and Production Costs Hampers Market Growth

High-quality substrates (such as heavy glass, metal, and specialty coatings), along with artisanal finishing, contribute to a notable increase in unit costs and complexity. For numerous mid-market brands, the profit increase from premium packaging does not consistently compensate for these additional expenses, which restricts wider acceptance. This sensitivity to costs becomes particularly pronounced during times of inflation or when supply chains become constrained. Thus, the high material and production costs hinder the market growth.

MARKET OPPORTUNITIES

Augmenting Demand for Premiumization & Gifting Offers Market Growth Opportunities

Consumers across various regions are increasingly seeking enhanced quality in their experiences, and gift packaging, limited editions, and collectible boxes contribute to perceived value, validating elevated price points. Luxury and prestige categories (such as cosmetics, spirits, and premium chocolates) significantly depend on custom, textured, and decorative packaging that reinforces brand narratives and encourages repeat purchases.

As the luxury direct-to-consumer and subscription models expand globally, suppliers have the opportunity to promote premium, branded shipping solutions that combine protection with an engaging unboxing experience. This approach can help establish a recurring revenue stream for designers and converters.

MARKET CHALLENGES

Balancing Aesthetics with Circularity Poses a Critical Challenge to Market Growth

Attaining the glossy, multi-layer appearance that consumers associate with high-end packaging, while also adhering to recycling or reuse standards, presents significant technical and commercial challenges. Coatings and laminates that convey a premium look frequently compromise recyclability, necessitating challenging compromises for designers and sustainability teams. Thus, balancing aesthetics with circularity poses a challenge to market growth.

Segmentation Analysis

By Material

Sustainability, Versatility, and Premium Appeal Drive Paper & Paperboard Segment Dominance

Based on the material, the market is divided into paper & paperboard, plastics, glass, metals, and others.

The paper and paperboard segment is expected to account for the largest share of the market. The segment leads the market due to its ideal combination of sustainability, cost efficiency, and high-end aesthetics. This material is extensively recyclable, lightweight, and suitable for luxurious finishes such as embossing, foiling, and specialty coatings. Additionally, it complies with regulatory standards and meets brand expectations for environmentally friendly yet visually distinctive packaging in the luxury, cosmetics, food, and gifting sectors.

The glass segment is expected to grow at a CAGR of 5.37% over the forecast period.

By Packaging Type

Superior Brand Presentation and Protection Drive Dominance of Boxes & Cartons Segment

Based on packaging type, the market is segmented into boxes & cartons, bottles & jars, sleeves & slipcases, inserts & dividers, tubes, and others.

In 2025, the boxes and cartons segment dominated the global market. The growth of this segment is driven by its exceptional surface area for branding, its ability to support high-quality decorative finishes, and its provision of robust product protection and stackability. This makes it particularly suitable for luxury goods, cosmetics, food and beverages, and gifting purposes, while also aligning effectively with sustainability objectives through the use of recyclable paperboard sustainable materials.

The tubes segment is projected to grow at a CAGR of 5.67% over the forecast period.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

High Consumption Volumes and Premiumization Drive Food & Beverages Segment Dominance

Based on the end-use industry, the market is segmented into food & beverages, fashion & apparel, personal care & cosmetics, consumer goods, and others.

The food & beverages segment is expected to hold a dominant market share over the forecast period. The growth of this segment is driven by its extensive consumer base and the continuous premiumization of items such as chocolates, confectionery, specialty foods, and alcoholic beverages. In this context, appealing, protective, and sustainable packaging is crucial for brand differentiation, shelf appeal, product freshness, and the demand for gifting on retail and e-commerce platforms.

The personal care & cosmetics segment is projected to grow at a CAGR of 4.85% over the forecast period.

Premium Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Europe Premium Packaging Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant premium packaging market share in 2024, valued at USD 2.02 billion, and maintained its leading position in 2025, with a value of USD 2.10 billion. In North America, the market is being driven by the rapid growth of e-commerce and Direct-to-Consumer (DTC) brands, which require packaging that can safeguard high-value items during transit while also providing a memorable unboxing experience.

U.S Premium Packaging Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.69 billion in 2025, accounting for roughly 23.13% of global premium packaging sales. In the U.S., the narrative surrounding premium packaging closely mirrors the growth of Direct-to-Consumer (DTC) models and a push for personalization. Digital printing and on-demand finishing enable brands to create small, highly branded production runs that enhance customer loyalty and promote "Instagrammability."

Europe

Europe is projected to record a growth rate of 5.84% in the coming years, the second-highest among all regions, recording a valuation of USD 2.51 billion in 2025. Stringent environmental regulations and a robust consumer demand for sustainable, premium products drive the growth of Europe's high-end packaging sector. Simultaneously, Europe's rich luxury tradition fosters a demand for artisanal touches, such as embossing, rigid boxes, and specialty papers, prompting converters to invest in recyclable luxury and traceability solutions.

U.K Premium Packaging Market

The U.K. premium packaging market in 2025 recorded a valuation of USD 406.69 million, representing approximately 5.56% of global premium packaging revenues.

Germany Premium Packaging Market

Germany’s premium packaging market reached a valuation of USD 587.72 million in 2025, equivalent to around 8.04% of global premium packaging sales.

Asia Pacific

Asia Pacific recorded a valuation of USD 1.28 billion in 2025 and secured the position of the third-largest region in the market. In the region, India and China are recorded a valuation of USD 360.61 million and USD 410.61 million, respectively, in 2025. The Asia Pacific region is experiencing the most rapid growth in the premium packaging sector, driven by increasing disposable incomes, swift premiumization in the beauty, spirits, and confectionery categories, as well as a dynamic travel-retail market. Additionally, there is an increasing consumer demand for premium protective packaging as Direct-to-Consumer (DTC) and cross-border online luxury purchases continue to rise.

Japan Premium Packaging Market

The Japan premium packaging market in 2025 was estimated to be around USD 206.52 million, accounting for approximately 2.83% of global premium packaging revenues.

Japan's high-end packaging sector is influenced by a cultural focus on craftsmanship, presentation, and product integrity, where consumers expect flawless finishing, small or boutique packaging, and outstanding quality control.

China Premium Packaging Market

China’s premium packaging market was projected as one of the largest worldwide, with revenues estimated at around USD 410.61 million in 2025, representing roughly 5.62% of global premium packaging sales.

India Premium Packaging Market

The Indian premium packaging market in 2025 was estimated to be around USD 360.61 million, accounting for roughly 4.93% of global premium packaging revenues.

Latin America and the Middle East & Africa

The Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market reached a valuation of USD 0.88 billion in 2025. In Latin America, the growth of premium packaging is more specific to certain sectors. The increasing demand for premium tiers in food and beverage, personal care, and spirits drives the need for enhanced rigid and decorative packaging. However, cost sensitivity and inconsistent recycling and collection infrastructure limit the adoption of extremely high-cost luxury formats.

In the Middle East & Africa, South Africa reached a valuation of USD 0.16 billion in 2025.

Saudi Arabia Premium Packaging Market

The Saudi Arabia premium packaging market was projected to reach approximately USD 122.32 million in 2025, accounting for roughly 1.67% of global premium packaging revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding New Product Launches by Key Players to Propel Market Progress

The global premium packaging market has a semi-consolidated market structure, comprising prominent players such as Smurfit Kappa, Huhtamäki Oyj, and Amcor Plc. The significant market share of these companies is due to numerous strategic activities, including collaboration among operating entities to advance research activities through various ongoing clinical trials.

- For instance, in December 2025, UPM presented UPM Circular Renewable Black, an innovative advancement that transforms the perception of black as a color in eco friendly packaging. UPM Circular Renewable Black is the first bio-based, Near-Infrared (NIR) detectable, carbon-negative pigment globally. It facilitates high-quality packaging solutions that merge exceptional design with complete recyclability and robust sustainability performance.

Other notable players in the global market include Crown, Stoelzle Glass Group, and Ardagh Group S.A. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY PREMIUM PACKAGING COMPANIES PROFILED

- Smurfit Kappa(Ireland)

- Huhtamäki Oyj(Finland)

- Amcor Plc (Switzerland)

- Crown (U.S.)

- Stoelzle Glass Group (Austria)

- Ardagh Group S.A. (Luxembourg)

- GPA Global (U.K.)

- O-I Glass (U.S.)

- MM Packaging (Austria)

- Graphic Packaging (U.S.)

- Milon Plastics LLP (India)

- Premium Packaging Solutions (India)

- TNT Group (France)

- Premiumpack GmbH (Austria)

- Arkay (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Stora Enso broadened its range of premium packaging solutions with Ensovelvet, a novel uncoated Solid Bleached Sulfate (SBS) board featuring a soft, velvet-like texture on both sides. This board is perfectly designed for high-end applications, including cosmetics, fragrances, and various luxury consumer goods.

- July 2025: Sappi demonstrated its superior packaging capabilities at LuxePack Monaco 2025. The company presented its renowned Algro paperboard and Fusion containerboard collections for sustainable luxury packaging at a shared booth with the prominent paper and paperboard laminator, Kapag.

- September 2025: The TNT Group redefined the boundaries of luxury packaging through the use of anodized, injection-molded aluminum. The company’s innovative, patent-pending injected aluminum technology features a glossy anodized finish that combines the circularity benefits of aluminum with the adaptability of die-cast materials. It achieves aesthetic characteristics comparable to those of zamak.

- July 2025: Graphic Packaging International, a global leader in sustainable consumer packaging, collaborated with Unilever to support the recent launch of its flagship toothpaste brand, WHITE NOW. The updated collection, now accessible in select European markets, is showcased through high-quality packaging that offers vibrant shelf presence and a remarkable, modern design.

- January 2025: Avery Dennison South Asia, a worldwide leader in materials science and packaging solutions, has unveiled its Premium Labels range. This latest offering features a collection of textured substrates for premium labeling, meticulously crafted to enhance consumer experiences through distinctive surface textures and patterns.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.33% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Packaging Type, End-use Industry, and Region |

|

By Material |

· Paper & Paperboard · Plastics · Glass · Metals · Others |

|

By Packaging Type |

· Boxes & Cartons · Bottles & Jars · Sleeves & Slipcases · Inserts & Dividers · Tubes · Others |

|

By End-use Industry |

· Food & Beverages · Fashion & Apparel · Personal Care & Cosmetics · Consumer Goods · Others |

|

By Region |

· North America (By Material, Packaging Type, End-use Industry, and Country) o U.S. o Canada · Europe (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Germany o U.K. o France o Italy o Spain o Russia o Poland o Romania o Rest of Europe · Asia Pacific (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Brazil o Mexico o Argentina o Rest of Latin America · Middle East & Africa (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Saudi Arabia o UAE o Oman o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 7.31 billion in 2025 and is projected to reach USD 11.59 billion by 2034.

In 2025, the Europe market value stood at USD 2.51 billion.

The market is expected to exhibit a CAGR of 5.33% during the forecast period of 2026-2034.

By material, the paper and paperboard segment is expected to lead the market.

Growing sustainability and regulatory pressure are the key factors driving the market.

Smurfit Kappa, Huhtamäki Oyj, Amcor Plc, Crown, Stoelzle Glass Group, and Ardagh Group S.A. are major players in the global market.

Europe dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us